Sample Category Title

EUR/USD Eying 1.2154 Key Support as Markets Seek ECB Draghi’s View on Q1 Slowdown

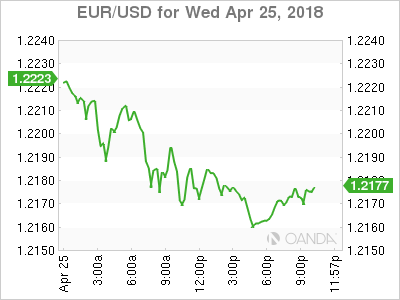

Dollar retreats mildly in Asian session today but remains the strongest one for the week. US 10 year yield finally took out 3% level overnight with some conviction. TNX hit as high as 3.035 before closing at 3.024, up 0.041. The development helped lifted Dollar Index above key near term resistance at 91.01 to close at 91.17. The stage is set for Dollar to reverse its medium term down trend. Though, the greenback still have one more hurdle to overcome. That is, 1.2154 support in EUR/USD. That would very much depends on today's ECB rate decision and press conference, as well as US Q1 GDP data tomorrow.

Markets seek ECB Draghi's view on Q1 slowdown

There is little chance of any change in monetary policy nor language in today's ECB rate decision and press conference. President Mario Draghi will most likely continue to sound cautious and noncommittal. Expectations are indeed on the June meeting where ECB will release new economic projections, and will likely signal what it's going to do after asset purchase program expires in September.

Nonetheless, today's meet may not be a non-event. Since the March meeting, Eurozone's economic data have surprised to the downside. It would be of great interest to see the policymakers' interpretation of the situation. All in all, we expect the members to view the first quarter slowdown as driven by temporary factors, e. g.: weather, which do not affect the monetary stance. More in ECB Preview: Caution over Recent Slowdown Won't Affect QE Schedule

And some suggested readings on ECB:

- No Change to ECB Guidance Yet

- ECB Preview – Not On Draghi's Watch

- ECB Meeting: Staying "Cautious" for Now?

Moody's affirms US Aaa rating, stable outlook.

Moody's Investor Service affirmed US Aaa rating. Outlook was also maintained as stable. Moody's noted that "exceptional economic strength" of the US, very high strength of its institution, very low exposure to credit related-shocks. And that "counter balance" the lower fiscal strength.

The rating agency also noted that "diversity, dynamism, and competitiveness" of the US economy, Dollar's status as the "pre-eminent international reserve currency" and the "very large size and depth" of the treasury market. These advantages will "offset rising fiscal pressures" from "ageing-related entitlement spending, higher debt service payments", and recent policy actions that will likely lower revenues and increase expenditures.

For now, Moody's expected US and China to reach a trade deal eventually. However, Moody's Senior Credit Officer William Foster said that "if things ultimately progress in a way that is outside of the base case, that would be negative for both countries and for the global market place, but our expectation is this will be negotiated back from the headlines you're reading."

Canada Freeland: "Good" and "constructive" progress made in NAFTA talks

Canadian Foreign Minister Chrystia Freeland, Mexican Economy Minister Ildefonso Guajardo and US Trade Representative Robert Lighthizer are still carrying on with NAFTA renegotiation in Washington.

Freeland hailed yesterday that "there is a very strong, very committed, good-faith effort for all three parties to work 24/7 on this and to try and reach an agreement." And, some "good" and "constructive" progress was made. They are working on "a set of "proposals based on the creative ideas the U.S. came up with in March".

But there are still some major differences. For example, Canada is firm on it's stance that object the including of a "sunset clause" what would allow one of the three members to quit after five years. Freeland said that the withdrawal mechanism is "absolutely unnecessary".

Also Freeland reiterated Canada's opposition to US steel and aluminum tariffs, which is currently exempted until May 1. She said "Canada's position has been clear from the outset and that is that Canada expects to have a full and permanent exemption from any quotas or tariffs."

Fitch affirms Japan's 'A' IDR rating with stable outlook. Trade protectionism poses a downside risk

Fitch Ratings affirmed Japan's Long-Term Foreign-Currency Issuer Default Rating (IDR) at 'A' with a Stable Outlook. Fitch noted Japan's "balance the strengths of an advanced and wealthy economy, with high governance standards and strong public institutions, against weak medium-term growth prospects and high public debt." And, "strong external finances marked by a persistent current account surplus and large net external credit and international investment positions relative to peers."

Fitch expected Japan GDP growth to slow to 1.3% in 2018 and 0.7% in 2019. However, "trade protectionism poses a downside risk to the outlook, exemplified by the imposition of a 25% tariff on US imports of steel and aluminium, including from Japan." Also, "spillovers from trade tensions between the US and China are also a risk, as are tensions on the Korean peninsula." Regarding inflation, Fitch projected headline inflation to reach only 1.2% at the end of 2018, and rise temporarily to 2.8% at the end of 2019 due to sales tax hike.

The monetary settings under BoJ's yield curve control framework will "remain broadly unchanged for the foreseeable future". Fitch noted recent slowdown in asset purchase has been sufficient to sustain the share of outstanding JGBs held by the central bank at around 40%-45%. And, "this level of BoJ ownership is within levels that would prevent the emergence of problems for JGB market liquidity, which the BoJ continues to monitor closely."

South Korean Moon and North Korean Kim to plant the tree of "peace and prosperity" on Friday

South Korean President Moon Jae-in will meet with North Korean leader Kim Jong-un in a historical encounter tomorrow on Friday. That's the first highest level summit between the two countries for in more than a decade.

According South Korean chief of staff, the meeting will start at 10:30 a.m. (0130 GMT) at the Peace House in Panmunjom, a village just north of the de facto border between North and South Korea. Kim will then cross the border at 9:30 a.m. (0030 GMT). Moon and Kim will then have lunch separately before holding a tree-planting ceremony in the afternoon.

In the ceremony, a pine tree will be planted on the demarcation line, as a symbol of "peace and prosperity". Soil from Mount Paektu in North Korea and Mount Halla in South Korea will be used. Also, the tree with be watered with water brought from the Taedong River in the North and the Han River in the South.

A second round of talk will then be held after a walk in Panmunjom. A pact will then be signed by Kim and Moon, with an announcement. And the encounter will conclude with dinner on the South's side and watch a video clip themed 'Spring of One'.

On the data front

Australia import price index rose 2.1% qoq in Q1, well above expectation of 1.2% qoq. German will release Gfk consumer confidence, UK will release BBA mortgage approvals and CBI reported sales. Later in the day, US will release jobless claims, trade balance, wholesale inventories and durable goods orders.

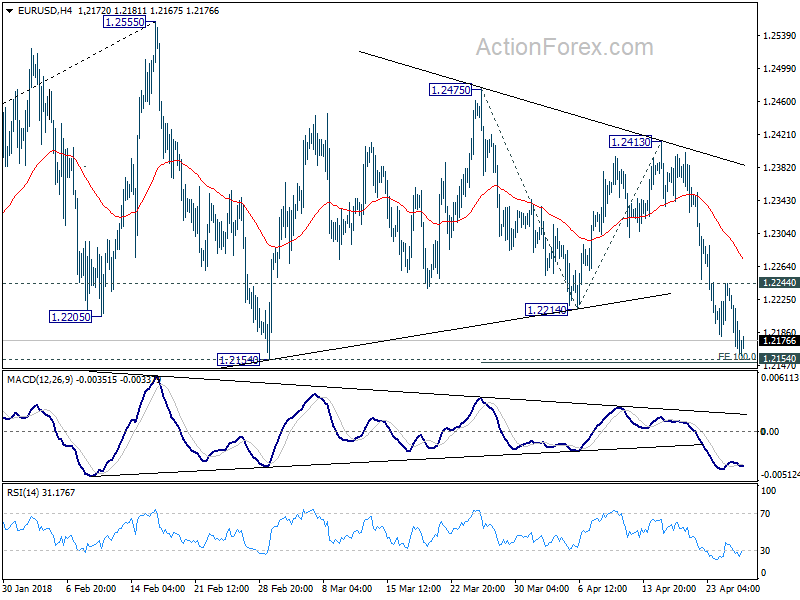

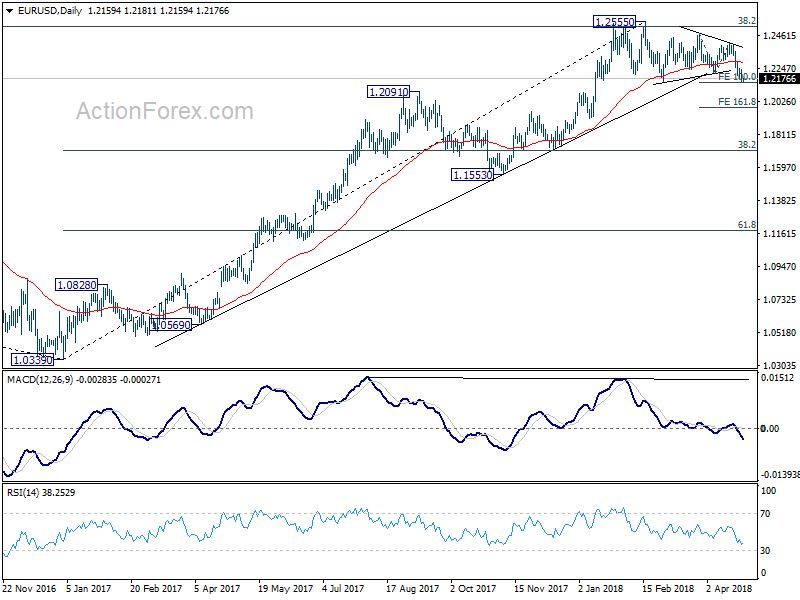

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2135; (P) 1.2186 (R1) 1.2213; More....

EUR/USD dropped to as low as 1.2159 so far and focus is now on 1.2154 key support. Decisive break there should confirm the bearish case of medium term reversal. In addition, the break of 100% projection of 1.2475 to 1.2214 from 1.2413 will indicate downside acceleration. In that case, EUR/USD should target 161.8% projection at 1.1991 next. In case of recovery, outlook will remain bearish as long as 1.2244 minor resistance holds. And further decline is still expected. However, break of 1.2244 will indicate strong support from 1.2154 and turn intraday bias back to the upside for 1.2413, to extend recent range trading.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | Import price index Q/Q Q1 | 2.10% | 1.20% | 2.00% | |

| 6:00 | EUR | German GfK Consumer Confidence May | 10.8 | 10.9 | ||

| 8:30 | GBP | BBA Loans for House Purchase Mar | 37.1K | 38.1K | ||

| 10:00 | GBP | CBI Reported Sales Apr | -2 | -8 | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 12:30 | USD | Initial Jobless Claims (APR 21) | 230K | 232K | ||

| 12:30 | USD | Advance Goods Trade Balance Mar | -74.8B | -75.9B | ||

| 12:30 | USD | Wholesale Inventories M/M Mar P | 0.60% | 1.00% | ||

| 12:30 | USD | Durable Goods Orders Mar P | 1.40% | 3.00% | ||

| 12:30 | USD | Durables Ex Transportation Mar P | 0.40% | 1.00% | ||

| 14:30 | USD | Natural Gas Storage | -36B |

South Korean Moon and North Korean Kim to plant the tree of “peace and prosperity” on Friday

South Korean President Moon Jae-in will meet with North Korean leader Kim Jong-un in a historical encounter tomorrow on Friday. That's the first highest level summit between the two countries for in more than a decade.

According South Korean chief of staff, the meeting will start at 10:30 a.m. (0130 GMT) at the Peace House in Panmunjom, a village just north of the de facto border between North and South Korea. Kim will then cross the border at 9:30 a.m. (0030 GMT). Moon and Kim will then have lunch separately before holding a tree-planting ceremony in the afternoon.

In the ceremony, a pine tree will be planted on the demarcation line, as a symbol of "peace and prosperity". Soil from Mount Paektu in North Korea and Mount Halla in South Korea will be used. Also, the tree with be watered with water brought from the Taedong River in the North and the Han River in the South.

A second round of talk will then be held after a walk in Panmunjom. A pact will then be signed by Kim and Moon, with an announcement. And the encounter will conclude with dinner on the South's side and watch a video clip themed 'Spring of One'.

Market Morning Briefing: Euro Is Again Testing The Lower End Of The Crucial 1.225-1.215 Zone

STOCKS

23250-23200 levels are still open for the Dow (24083.83, +0.25%) while the index trades below 24500. Dax (12422.30, -1.02%) is down sharply and may come off towards 12100 if it does not bounce back immediately from 12300. Near term looks bearish for both Dow and Dax.

Watch resistance near 22600 on the Nikkei (22333.91, +0.53%). Currently trading within narrow region, Nikkei may inch up towards 22600 before coming off from there sharply. Near term could be stable to bullish but overall the index looks bearish for the longer run.

Shanghai (3089.18, -0.92%) is likely to remain trapped in the 3050-3150 region for a few more sessions. Range trade could continue in the near term.

Nifty (10570.55, -0.41%) is stuck near the 10600 region and is unable to decide which direction to take up for the medium term. While some consolidation may continue this week, some fresh trigger could be seen in the early sessions of next week.

COMMODITIES

Brent (74.42) is trading above 74 just now but while the resistance near 76.0-76.5 holds, there could be some pause in Brent. A break above 76.50, if seen by next week could open up chances of testing 78 on the upside. Else some consolidation followed by a dip is possible by next week.

Nymex WTI (68.41) has important near term support at 67 which if holds could push the price to higher levels of 69.0-69.5. For now 69.50-67.0 could be the trade region for the coming sessions.

Gold (1325.20) dipped in line with our expectation and could test 1310 on the downside. Support near 1310 is likely to keep the price stable for the medium term. Need to watch price action at 1310. A break could open up chances of 1290-1280 in the longer term.

Copper (3.13) is stable since the last few sessions stuck within the 3.18-3.12 region. While the price could continue to remain so for the next few sessions, bias is on the downside towards 3.10 or lower.

FOREX

Dollar index (91.17) seems to have decisively breached the 90.5-91.0 zone, thereby breaking crucial resistances on all charts (daily, 3 day and weekly). This recent strengthening of the Dollar might have been aided by the upmove in US yields, which in turn, has happened due to positivity around US economic growth. Our Apr '18 Euro report's forecast of medium term Dollar bullishness after May/Jun seems to be happening earlier. The ECB meeting later today could be important. Any increase in hawkishness from the ECB could still pull the Dollar down. Let's wait and watch.

Euro (1.2172): Euro is again testing the lower end of the crucial 1.225-1.215 zone and seems to be turning bearish for the medium term. Crucial supports on 3 day and weekly candles seem to have been broken decisively. The ECB meeting later today could be the final decider of whether the Euro will bounce back from 1.215 or not. Right now, it seems increasingly unlikely that the Euro will gain any significant strength from here. Our Apr '18 Euro report's preference for bearishness in the Euro after May/Jun looks likely to happen earlier.

Dollar Yen (109.37) : Dollar Yen has risen past the 21 WMA (108.95) and looks like it could now target levels near 110. This rise has been in line with our Apr '18 Yen report. In the same report, we had expressed preference for Dollar Yen to turn bearish after testing 110 (max 110.5), which is seen as the previous high reached in Feb beginning.

Euro Yen (133.14) has continued to stay near 133 as our predicted moves in the Euro (towards 1.225) and Dollar Yen (towards 108.5) didn't happen. In the near term, Euro Yen could stay below 134 if the Dollar Yen dips from 110.5 and if the Euro moves below 1.215. Next month could see Euro Yen dipping to 131 or even lower.

As mentioned yesterday as well, Pound (1.3941) seems to be pausing in its downmove towards crucial long term support level near 1.385 on weekly line chart. We are however expecting it to test this level by next week possibly. If this support also breaks, Pound could turn very bearish in the medium term. However, our preference is for it to hold, in which case, we could see a rally towards long term resistance level of 1.46 in the weeks ahead.

Dollar Rupee (66.9050): Could see 66.70 today. Then 67.20. Then correction of 50-70 paise.

INTEREST RATES

The US 10 Year Yield and 30 Year yield are both breaking respective resistance levels near 3% and 3.2%. The ECB meeting today could be an important determinant for the course of US yields. As mentioned yesterday, any hint of hawkishness from Draghi could be negative for US yields. This recent upmove in US yields has happened on back of positive sentiment around the US economy's growth (reflected in various data releases of the last 2 weeks). In addition, Crude's rise towards 75 has also played its part in increasing inflation expectations and fuelling the rise in yields.

US 10 Yr Yield (3.03%), 30 Yr (3.21%), 5 Yr (2.84%), 2 Yr (2.48%):

The US 2 year yield (2.48) is pausing in its upmove towards 2.50% and could see a dip towards 2.40% soon. \

The US 5 Year yield could have its upside restricted by 2.9% in the coming month.

The 10 Year yield (3.03%) has not come off from 3% and is now looking likely to move towards 3.20% over the course of the next month and half.

As we have been saying, the 30 yr yield is breaking crucial resistance near 3.2% just when the 10 year yield broke the 3% level. It could now see an upmove towards 3.4%-3.5% in the coming month and half while the 10 Year yield moves towards 3.2%.

Fitch affirms Japan’s ‘A’ IDR rating with stable outlook. Trade protectionism poses a downside risk

Fitch Ratings affirmed Japan's Long-Term Foreign-Currency Issuer Default Rating (IDR) at 'A' with a Stable Outlook. Fitch noted Japan's "balance the strengths of an advanced and wealthy economy, with high governance standards and strong public institutions, against weak medium-term growth prospects and high public debt." And, "strong external finances marked by a persistent current account surplus and large net external credit and international investment positions relative to peers."

Fitch expected Japan GDP growth to slow to 1.3% in 2018 and 0.7% in 2019. However, "trade protectionism poses a downside risk to the outlook, exemplified by the imposition of a 25% tariff on US imports of steel and aluminium, including from Japan." Also, "spillovers from trade tensions between the US and China are also a risk, as are tensions on the Korean peninsula." Regarding inflation, Fitch projected headline inflation to reach only 1.2% at the end of 2018, and rise temporarily to 2.8% at the end of 2019 due to sales tax hike.

The monetary settings under BoJ's yield curve control framework will "remain broadly unchanged for the foreseeable future". Fitch noted recent slowdown in asset purchase has been sufficient to sustain the share of outstanding JGBs held by the central bank at around 40%-45%. And, "this level of BoJ ownership is within levels that would prevent the emergence of problems for JGB market liquidity, which the BoJ continues to monitor closely."

Moody’s affirms US Aaa rating, stable outlook. Economic strength couter balance lower fiscal strength

Moody's Investor Service affirmed US Aaa rating. Outlook was also maintained as stable. Moody's noted that "exceptional economic strength" of the US, very high strength of its institution, very low exposure to credit related-shocks. And that "counter balance" the lower fiscal strength.

The rating agency also noted that "diversity, dynamism, and competitiveness" of the US economy, Dollar's status as the "pre-eminent international reserve currency" and the "very large size and depth" of the treasury market. These advantages will "offset rising fiscal pressures" from "ageing-related entitlement spending, higher debt service payments", and recent policy actions that will likely lower revenues and increase expenditures.

For now, Moody's expected US and China to reach a trade deal eventually. However, Moody's Senior Credit Officer William Foster said that "if things ultimately progress in a way that is outside of the base case, that would be negative for both countries and for the global market place, but our expectation is this will be negotiated back from the headlines you're reading."

Canada Freeland: “Good” and “constructive” progress made in NAFTA talks

Canadian Foreign Minister Chrystia Freeland, Mexican Economy Minister Ildefonso Guajardo and US Trade Representative Robert Lighthizer are still carrying on with NAFTA renegotiation in Washington.

Freeland hailed yesterday that "there is a very strong, very committed, good-faith effort for all three parties to work 24/7 on this and to try and reach an agreement." And, some "good" and "constructive" progress was made. They are working on "a set of "proposals based on the creative ideas the U.S. came up with in March".

But there are still some major differences. For example, Canada is firm on it's stance that object the including of a "sunset clause" what would allow one of the three members to quit after five years. Freeland said that the withdrawal mechanism is "absolutely unnecessary".

Also Freeland reiterated Canada's opposition to US steel and aluminum tariffs, which is currently exempted until May 1. She said "Canada's position has been clear from the outset and that is that Canada expects to have a full and permanent exemption from any quotas or tariffs."

Crude Oil and Gasoline Inventories Surprisingly Increased

The report from the US Energy Information Administration (EIA) shows that total crude oil and petroleum products stocks gained +1.39 mmb to 1182.36 mmb in the week ended April 20. Crude oil inventory added +2.17 mmb to 429.74 mmb, amidst increases in 3 out of 5 PADDs. The market had anticipated a -2.04 mmb decline. Cushing stock gained +0.46 mmb to 35.37 mmb. Utilization rate decreased -1.6% to 90.8%. Meanwhile, crude production increased +0.44M bpd to 10.59M bpd for the week.

For refined oil products, gasoline inventory increased +0.84 mmb to 236.81 mmb as demand plunged -7.85% to 9.08M bpd. This was compared with consensus of a -0.63 mmb drop. Production dropped -3.12% to 9.89M bpd while imports soared +27.07% to 0.9M bpd during the week. Distillate inventory fell -2.61 mmb to 122.73 mmb although demand slumped -13.94% to 3.75M bpd. The market had anticipated a -0.86 mmb draw. Production slipped -2.3% to 4.98M bpd while imports soared +19.42% to 0.12M bpd during the week.

Released after market close on Tuesday, the industry- sponsored API estimated that crude oil inventory gained +1.1 mmb during the week. For refined oil products, gasoline distillate dropped -2.72 mmb while distillate fell -1.91 mmb.

EUR/JPY Downsides Remain Supported Above 132.60

Key Highlights

- The Euro remains in a crucial uptrend and is positioned well above 132.00 against the Japanese Yen.

- There is an important bullish trend line formed with support at 132.60 on the 4-hours chart of EUR/JPY.

- The pair may correct in the short term, but it remains supported around 132.75 and 132.60.

- Today, the ECB interest rate decision is lined up, and the central bank is likely to make no changes in April 2018.

EURJPY Technical Analysis

The Euro traded higher recently above 133.00 against the Japanese Yen. The EUR/JPY pair remains in a major uptrend, but there are chances of a short-term downside correction.

The pair traded as high as 133.49 this week before starting a downside correction. It declined below the 23.6% Fib retracement level of the last wave from the 132.04 low to 133.49 high.

However, there are many supports on the downside around the 132.50 level. There is also an important bullish trend line formed with support at 132.60 on the 4-hours chart of EUR/JPY. Above the trend line support, the 132.75 level is also a key support.

The stated 132.75 support is close to the 50% Fib retracement level of the last wave from the 132.04 low to 133.49 high. Therefore, if the pair continues to move down, it could find buyers around 132.75 and 132.60.

A break below 132.60 may perhaps open the doors for more declines towards 132.00 and the 100 simple moving average (red, 4-hours). On the upside, an initial resistance is at 133.25, followed by the recent high of 133.49.

Economic Releases to Watch Today

- Germany’s GfK Consumer Confidence for May 2018 – Forecast 10.8, versus 10.9 previous.

- ECB Interest Rate Decision April 2018 – Forecast 0%, versus 0% previous.

- US Initial Jobless Claims – Forecast 230K, versus 232K previous.

- US Durable Goods Orders for March 2018 – Forecast +1.6% versus +3.1% previous.

Currrency Markets Yield To Dollar Demand

G-10 and EM currencies yield to dollar demand

The recent rise in US yields is responsible for crystallising USD strength, and this appears to have been accentuated by comparatively strong data flow in the US. But next week’s US Trade Roadshow to China, which includes the President’s ” champions of trade” Steven Mnuchin, Robert Lighthizer and Larry Kudlow, has undoubtedly calmed investors nerves and triggered an unwind of USD risk premiums around tariff and trade.

The dollar has traded higher against most currencies since the recent uptick in Yields early in the month. Also, some thematic changes underway suggest we could be in the midst of a structural shift in the global currency market pecking order. With EURUSD below 1.22 in convincing fashion and USDJPY setting sights on 110, the USD appears poised to breakout across the board.

Equities were trading gingerly most of the NY session, and after a midday risk wobble which saw the USD and UST yields fall, the markets bounced right back. All this suggests in the view of the market unless there is a very unlikely massive meltdown in US equity markets, it is doubtful the Fed will waver on a June rate hike. So with equity market sentiment holding firm in the face of rising bond yields, the almighty dollar could move through G-10 currency market like a wrecking ball pulverising lingering shorts in its path.

Asia Open

While investors remain focused on Yields, it looks like the 3 % ten year UST doom, and gloom hand was overplayed. US equity investors are picking themselves up off the mat after taking a beating on Tuesday when U.S. 10-year Treasury yields breached the “psychological level” of three percent, on the back of corporate earnings. All of this should instil a definite sense of calm at the Asia open despite massive regional outflows this week

Oil Prices

A jumpy NY session on Oil markets a the DOE inventories data was was a tad bearish relative to market expectations and as traders continue to assess all the noise and implication around Iran’s nuclear program. But the closer we get to May 12, Iranian sanctions waiver deadline, the more deafening the rhetoric, so rest assures we will be in for a very choppy dynamic ride during the next few weeks.

However, besides the geopolitical risk, which has been dominating trader sentiment, global demand for oil has remained high and provided OPEC compliance remains solid; oil should remain firm throughout 2018.

Gold

The prospering US dollar has toppled Gold prices to a five-week low. And with the dollar possibly on the verge of a breakout, speculative demand will remain low, and we could see prices fall ahead of for Friday US GDP data. Bullish dollar sentiment will likely build ahead of the data given the US’ robust performance on the economic front. All this suggests gold investors will be sidelined looking for better levels to buy as a stronger dollar narrative unfolds.

Currency Markets

The Japanese Yen

Yesterday technical issues we resolved and outside of a midday risk wobble, the dollar continues to move higher in convincing fashion as investor confidence is returning in a big way.

The Euro

Despite the markets pressing against some massive technical levels around 1.2150, there appears little appetite to tweak the current positioning gauges ahead of the ECB.

The Malaysian Ringgit

The USD is stretching its wings getting set to soar suggesting there could be more pain ahead for regional currencies as ten year UST’s remain above 3 %. However, equity sentiment has fallen off as bad expected suggesting risk appetite remains guardedly optimistic, but regional outflows are expected to stay high on the back of higher US yields.

The MYR should continue to trade defensively on the combination of firmer US scrim and fixed income outflows.

President Najib took to the airwaves overnight sounding confident about an election win but was more guarded about a two-thirds majority.

Strong Yields Boost Dollar Awaiting ECB

The US dollar is higher across the board against major pairs. US 10-year treasury bonds are above the 3 percent level making dollar shorts more expensive. Higher yields are a reflection of interest rate hike expectations, which Fed members have stoked with their latest comments. Rising inflation and steady economic growth are behind those the policymakers comments. The European Central Bank (ECB) will headline the economic calendar on Thursday, but as European growth decelerates investors are expecting the rhetoric to be on the dovish side with little insights into the central bank’s plan.

- Despite a string of gains USD still vulnerable

- Fed could hike rates 3 more times in 2018

- ECB to be cautious on end of QE comments

Interest Rate Differentials Pushing US Dollar Higher

The EUR/USD lost 0.45 percent on Wednesday. The single currency is trading at 1.2176 ahead of the release of the European Central Bank (ECB) interest rate statement on Thursday, April 26 at 7:45 am EDT. The central bank is not expected to announce any major changes to its monetary policy or drop hints regarding what’s next after end of its quantitive easing program in September. The Fed by comparison has been hawkish and several members have talked up the possibility of a fourth rate hike in 2018. Th ECB is not expected to hike rates until 2019.

The US dollar continues to improve from its terrible start to the year. The rising yields in US bonds have pushed the currency to three month highs as they broke above the 3 percent level. The next stage will be to see if this is a sustainable move without strong sell offs in the stock market. The ECB can afford to be patient given the strong momentum built by the economy, but as that wanes with more disappointing releases it could delay even further its rate normalization schedule.

The CME FedWatch tool increased the probability of three more rate hikes this year to 47 percent upgrading it from 33 percent based on Fed fund rate futures. With the ECB expected to be dovish on Thursday as the economy is losing steam, the interest rate divergence favours the US currency specially since the fourth rate hike was not fully priced in at the beginning of the year.

The economic calendar heading into he end of the week will be focused on growth with the release of the US first estimate of GDP in the first quarter of 2018 on Friday, April 27 at 8:30 am EDT. The Bureau of Economic Analysis is forecasted to announced a 2.0 percent gain. This being the first version of the quarterly data it carries the most weight and it could validate the steady growth expectations that the Fed has on the US economy.

Yen Lower with the BoJ Not Expected to Change Easing Monetary Policy

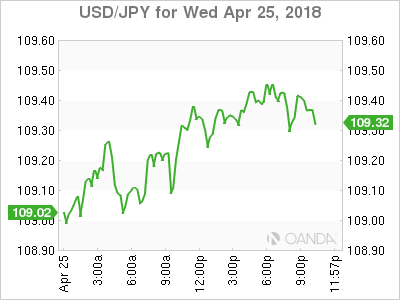

The USD/JPY gained 0.46 percent during the trading session. The currency pari is trading at 109.31 with the recovery of the US dollar and the subdued geopolitical frictions leading the yen lower. The Japanese currency had a strong start to the year despite the ever present concerns about low inflation but the Bank of Japan (BOJ) remains unconvinced that it needs to reduce its stimulus program which has pushed the JPY lower.

The central bank is not expected to tinker with its monetary policy, but the introduction of new deputy governor Masazumi Wakatabe thought to be in favour of adding even more stimulus to reach the 2 percent inflation target could prove more telling down the line if the Japanese economy struggles. Two days ago BOJ Governor Haruhiko Kuroda said that the inflation reach would reach the elusive 2 percent target within five years, and only then would stimulus would be reduced.

The Bank of Japan (BOJ) will release its monetary policy statement and its outlook report on Thursday at midnight and will follow up with a press conference on Friday, April 27.

Market events to watch this week:

Thursday, April 26

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

8:30am USD Core Durable Goods Orders m/m

10:00pm JPY BOJ Policy Rate

10:00pm Monetary Policy Statement

Midnight JPY BOJ Outlook Report

Friday, April 27

Tentative JPY BOJ Press Conference

4:30am GBP Prelim GDP q/q

8:30am USD Advance GDP q/q