Sample Category Title

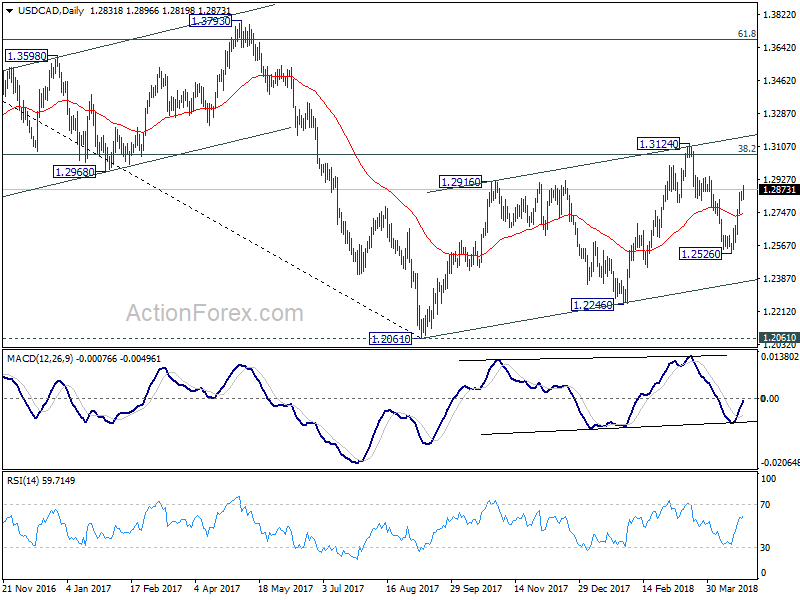

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2808; (P) 1.2834; (R1) 1.2857; More....

USD/CAD surges to as high as 1.2896 so far and intraday bias remains on the upside. Break of 1.2942 resistance will extend the rally from 1.2526 towards 1.3124 next. On the downside, below 1.2811 minor support will turn intraday bias neutral first. But for now, further rise will be expected as long as 4 hour 55 EMA (now at 1.2735) holds.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685.

Trump Holding Fire as Negotiations with China Begin

- US-China trade tensions ease as the US is set to send a delegation to Beijing for negotiations next week.

- Details are still awaited from Trump on an additional USD100bn worth of Chinese imports subject to tariffs, but Trump is likely to hold fire for now while negotiations go on.

- While the risk of a trade war is easing, the risk of a longer-lasting US-China tech war is on the rise.

As we wrote in Flash Comment: Is Trump preparing for a round of trade escalation - again?, 13 April 2018, the pendulum keeps swinging in the US-China trade conflict. Just 10 days ago it looked like Trump was going to escalate things further by announcing details on an extra USD100bn worth of US Chinese imports subject to tariffs, which would have triggered immediate China retaliation. However, it now seems increasingly likely that Trump is holding fire and has decided to move down the negotiation path, as he is sending a team of officials and top advisers to China for negotiations next week. According to media reports (see New York Times), the team will include Treasury Secretary Steven Mnuchin, US Trade Representative Robert Lightlizer and Director of the White House's National Economic Council, Larry Kudlow. Trade adviser Peter Navarro, probably the biggest China hawk on trade, may also join the group.

It is clearly a positive development that more serious negotiations are likely to take place now. It raises the prospect that we may have seen the worse and that a dangerous tit-for-tat path of retaliation can be avoided. It shows clearly that neither the US nor China is aiming for a trade war, and that the domestic pressure on Trump from American businesses may have convinced him it was time to start serious talks. At the same time, on China's part there have been some concessions as Xi Jinping among other things has promised lower tariffs on cars and other goods while opening up more for investments (see box). Protection of intellectual property rights will also be improved. The concessions must have been big enough for Trump to see scope for a deal. We continue to regard the end game as a deal that avoids a harmful trade war. As we have said before, however, we should continue to expect ebbs and flows in the negotiations as both sides will aim to get the best deal possible and scaring the other side is typically part of the negotiation tactics.

One effect of the rising uncertainty of US tariffs is that more companies are considering moving production away from China to other Asian countries. The FT today reported that German sportswear maker Puma is preparing to relocate production from China to other Asian markets if Trump puts tariffs on shows and apparel. Hence, the future risk of tariffs is already harming China's ability to attract investments for production.

The beginning of a US-China tech war?

Another US-China battle field, the tech area, has seen rising tensions over the past week. The US stirred things up by banning sales by US companies to one of China's big tech companies, telecom equipment maker ZTE. The ban is set to be in place for seven years and is due to the lack of compliance with US sanctions on Iran some years back that it subsequently tried to cover up. The ban is a big blow for ZTE, which relies on supplies of microchips from US suppliers. It also raises the risk of a continued 'tech war' between the US and China. China is currently blocking an USD44bn acquisition by US tech company Qualcomm and Dutch semi-conductor maker NPX due to supposed anti-trust reasons. While these specific matters may be resolved, in our view it is likely to mark the beginning of a long-lasting era of technological rivalry between the US and China, and high US protectionism towards China in the tech area.

The ZTE case has only worked to reinforce China's aim to become less reliant on foreign technology and sharpen its focus on developing high-tech sectors. It also raises the probability that tech companies will be subsidised in order to allow for potential negative bottom lines while they develop their technologies. In a speech over the weekend, Chinese President Xi Jinping said that 'core technology is an important tool for the nation', and called on various parties to persevere, focus and accelerate breakthroughs in technology. Xi Jinping held the speech at a national conference on network security and information. Chinese business leaders are also calling for more companies to play a role in technology. Alibaba founder Jack Ma said on Sunday that 'it is the compelling obligation for big companies to compete in core technology…a real company is not determined by its market value or market share, but how much responsibility it takes and whether it has mastered core and key technologies'.

Next month, the US Treasury Department is expected to release a plan to further restrict Chinese investment in US companies, which will most likely emphasise a need to protect national security in the tech area against Chinese companies.

Recent Chinese signals on opening up and IPR protection

Financial institutions:

- Raise foreign equity caps in banking, securities and insurance industries.

- Accelerate opening-up of insurance industry.

- Ease restrictions on the establishment of foreign financial institutions.

Manufacturing and service sector

- Open up as soon as possible in remaining areas of manufacturing still having limits: automobiles, ships and aircraft.

- Widen access in telecoms, healthcare, education and old age care. Improve role for markets

- Encourage competition and oppose monopolies. Setting up State Administration for Market (in March) Regulation to remove systematic and institutional obstacles that prevent the market from playing a decisive role.

Property rights and technology

- Strengthening of intellectual property rights by re-instituting the State Intellectual Property Office to step up law enforcement and raise the cost for offenders

- Encourage normal technological exchanges and cooperation between Chinese and foreign enterprises, and protect the lawful IPR owned by foreign enterprises in China.

Strengthen imports

- Work hard to import more products that are competitive and needed by Chinese people.

- First International Import Expo to be held in Shanghai this November to strengthen commitment to opening up market.

Source: People's Daily, Xinhua, Xi Jinping speech at Boao Forum, April 2018

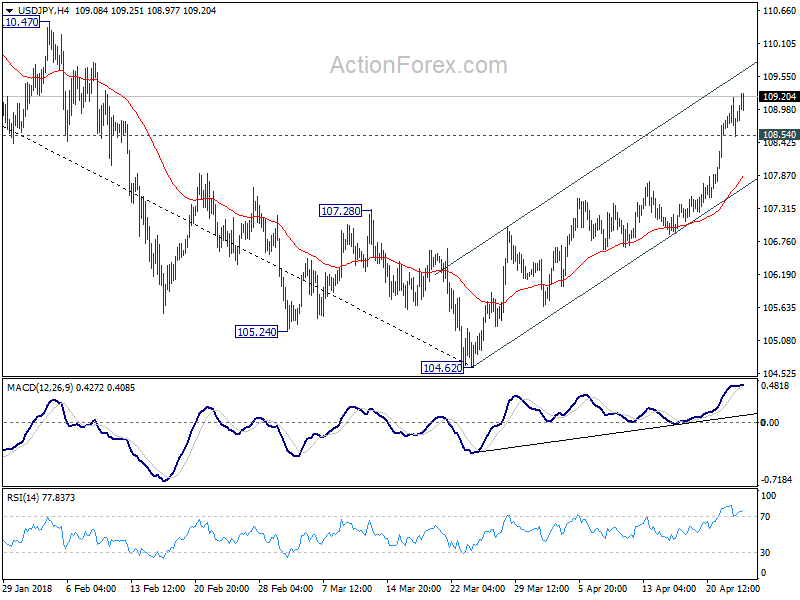

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.50; (P) 108.85; (R1) 109.15; More...

USD/JPY's rally is still in progress and intraday bias stays on the upside. Current rise from 104.62 should extend to 61.8% retracement of 114.73 to 104.62 at 108.48 9 110.86 next. On the downside, below 108.54 minor support will turn bias neutral and bring consolidation first, before staging another rise.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.47).

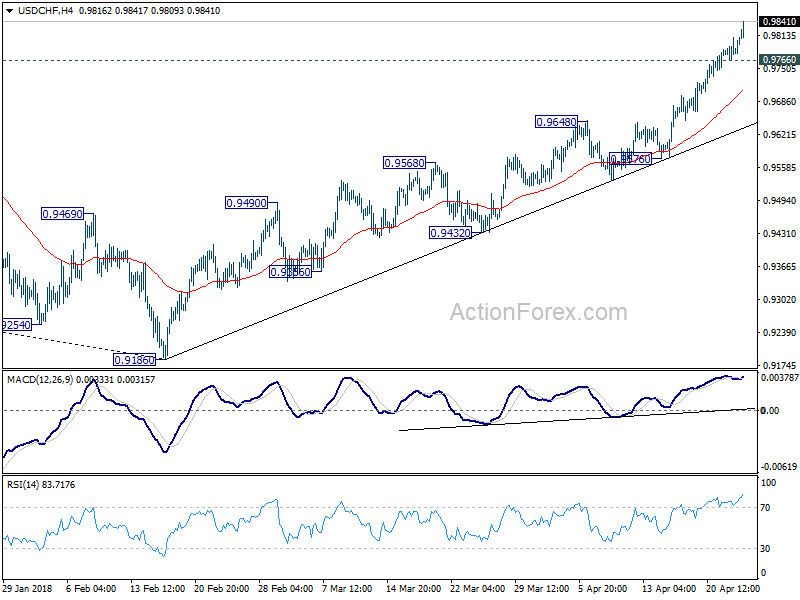

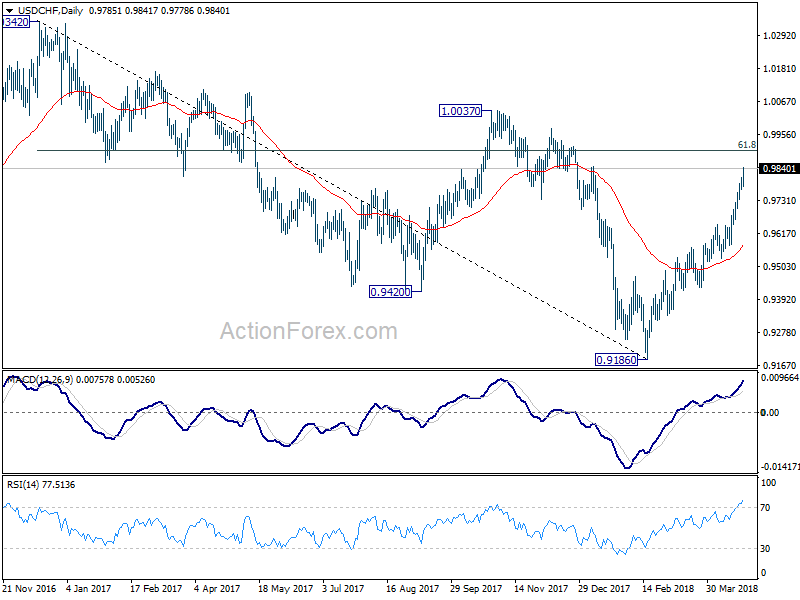

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9749; (P) 0.9768; (R1) 0.9801; More...

USD/CHF's rally continues to as high as 0.9841 so far and intraday bias remains on the upside. Current rally from 0.9186 should target 0.9900 fibonacci level first. Break will target 1.0037 resistance next. On the downside, below 0.9766 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.9576 support holds.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next. This will now be the preferred case as long as 0.9576 support holds.

SNB Unlikely to Act Despite Recent EURCHF Strength

EURCHF remains in consolidation after briefly breaching 1.2 last Friday. We see policy divergence, US sanctions against Russia and the upcoming referendum on SNB’s power are key reasons for the recent weakness in Swiss franc. Despite the symbolic meaning – SNB set 1.2 as the floor of EURCHF in September 2011 before abruptly abandoning is in January 2015, we do not believe the central bank would consider tightening its monetary policy just because the 1.2 level is breached. Indeed, Chairman Thomas Jordan has affirmed that the FX market is “fragile” and there is no plan to change to monetary policy for the time being. We do not feel surprised to see further downside on Swiss franc.

Policy Divergence

SNB has been maintaining negative interest rates for years. In December 2017, it again kept the sight deposit rate unchanged at -0.75%, while the target range for the three-month Libor stayed at between –1.25% and –0.25%. The central bank reiterated that it would “remain active in the foreign exchange market as necessary”, while “taking the overall currency situation into consideration”. The pledge to keep the monetary policy accommodative is contrasted with the major central banks. For instance, the Fed has raised the policy rate for 6 times since 2015. The market expects two or three more hikes this year. Although the ECB has continued with asset purchases, the scaled has been reduced for a few times. The market expects it to announce further scale down, or even an end, of the current program in coming months. Policy divergence, reflected in the yield spreads between Switzerland and other economies, has been a key reason for funds to leave Switzerland for higher yields elsewhere.

Sanctions against Russia

US sanctions against Russia in response to the latter’s support for Syria have not only caused massive selloff in Russian equities and currency – ruble, but also triggered investors to repatriate capital sheltered in Switzerland, top destination of Russian capital outflow. Statistics show that about 14% of Russia’s cross-border outflow went to Switzerland last year, tripling that to the US.

SNB Referendum

On June 10, a referendum would be held for Swiss citizens to vote on whether only the central bank is allowed to create money. The SNB, the Federal Council and the Swiss parliament have released statements to oppose the initiative – the Vollgeld Initiative or the sovereign money initiative. According to SNB, “acceptance of the initiative would have serious consequences for the structure and the stability of the financial system, as well as the monetary policy of the SNB, and plunge the Swiss economy into a period of extreme uncertainty”. While it is expected that the chance of a success for the pro- Vollgeld camp is low, this might cause some sorts of volatility in Swiss franc as the referendum is getting close.

Although franc’s weakness might persist for weeks, or even months, it is unlikely that SNB would adjust its monetary policy. At an interview last week, SNB chairman Thomas Jordan indicated that Swiss franc is moving in the “right direction” after significant overvaluation for years, though he cautioned that the current FX movement is in a “relatively fragile situation”. As such, the central bank would remain “very prudent at this point”. He added that “it’s not the time today to talk about changing monetary policy” and he is “convinced that the current monetary policy is still necessary”.

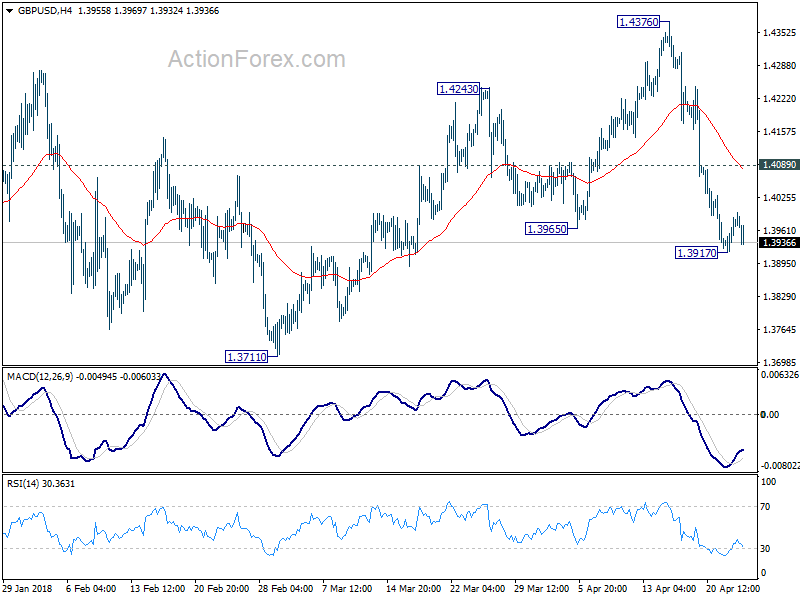

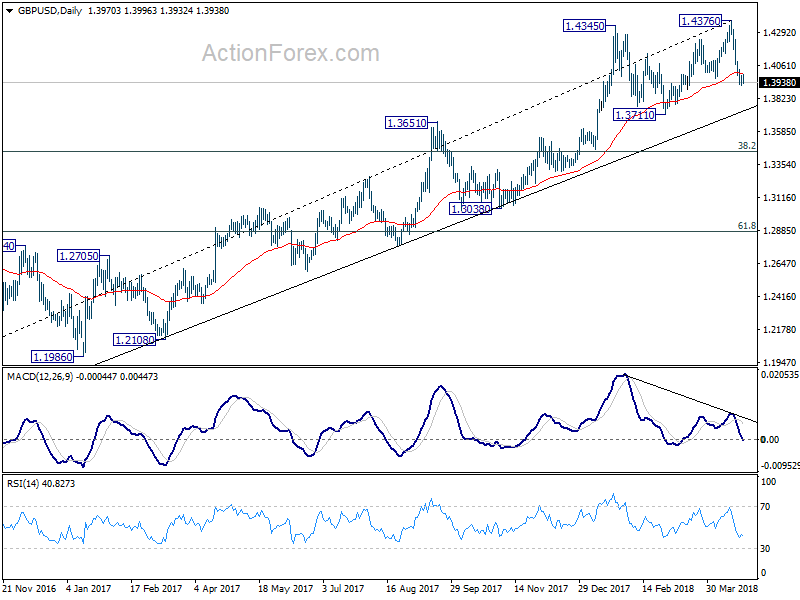

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3899; (P) 1.3965; (R1) 1.4004; More...

GBP/USD is staying in consolidation above 1.3917 temporary low and intraday bias remains neutral for the moment. Another recovery could be seen. But upside should be limited by 1.4089 minor resistance to bring fall resumption. Below 1.3917 will target 1.3711 key support next. However, firm break of 1.4089 will turn focus back to 1.4376 high instead.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4257). Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

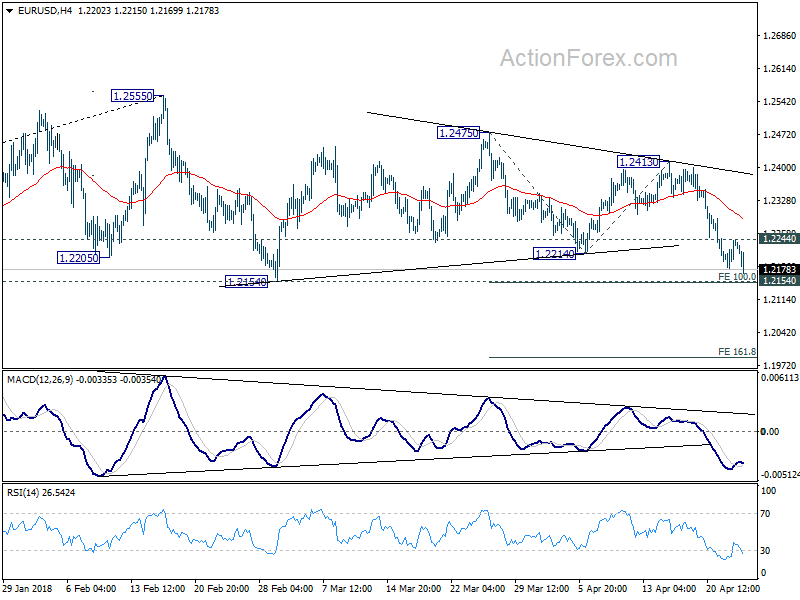

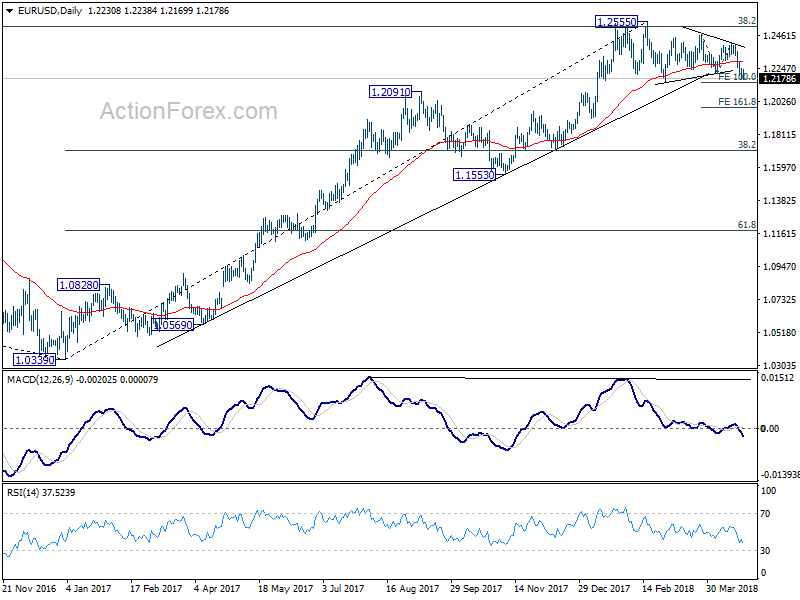

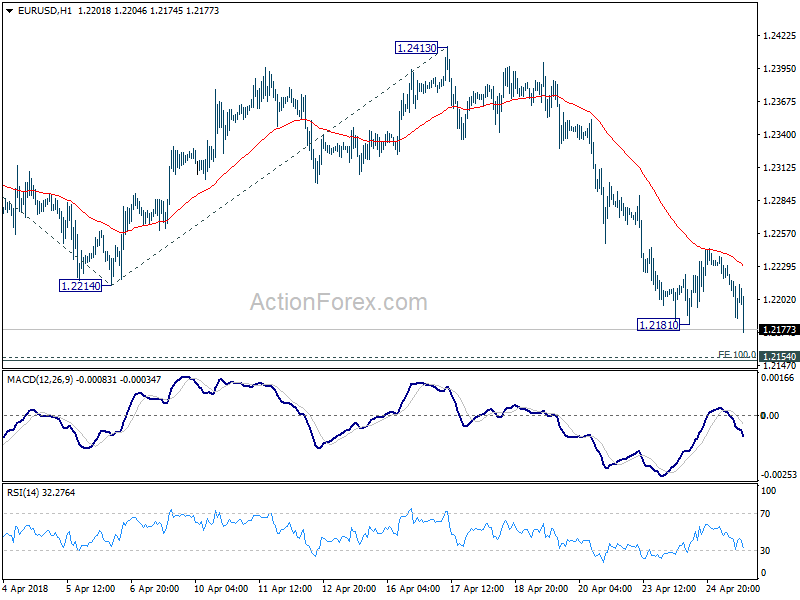

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2194; (P) 1.2220 (R1) 1.2258; More....

EUR/USD's fall resumes after brief consolidation and intraday bias is turned to the downside for 1.2154 key support. Decisive break there should confirm the bearish case of medium term reversal. And EUR/USD should then target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. On the upside, though, break of 1.2244 minor resistance will indicate short term bottoming. And even though we'd still expect deeper decline in that case, lengthier consolidation would be seen first.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Global Stocks Under Pressure While Gold Dips

Global equity markets were under pressure on Wednesday as rising U.S Treasury bond yields and speculation of higher U.S interest rates dented appetite for stocks.

Most Asian shares fell during early trade, following a heavy selloff on Wall Street overnight. The negative momentum from Asian markets and growing caution have already punished European stocks this morning. With investors likely to maintain some distance from equities as U.S bond yields climb, Wall Street could extend losses this afternoon.

Sterling depressed below 1.4000

Sterling struggled to push back above the 1.4000 pivotal level this morning as investors continued to question the likelihood of a BOE interest rate hike in May.

An aggressively appreciating Dollar has punished the GBPUSD further, with prices trading around 1.3957 as of writing. Slowing UK inflation and a cautious Mark Carney have forced investors to scale back expectations of a May rate hike. The Pound, which remains extremely sensitive to monetary policy speculation, could depreciate further based on these factors.

Taking a look at the technical picture, the GBPUSD is bearish on the daily charts. The decisive breakdown below the pivotal 1.4000 support level could encourage a decline towards 1.3920 and 1.3800, respectively. For bulls to jump back into the game, prices need to secure a daily close back above 1.4000.

Currency spotlight – USDJPY

The Yen slipped to a fresh two-month low at 109.25 during Wednesday’s trading session, as higher U.S yields boosted the Dollar.

With the Dollar finding amble support from rising bond yields and expectations of higher U.S interest rates, the USDJPY has scope to venture higher. From a technical standpoint, the USDJPY is bullish on the daily timeframe as there have been consistently higher highs and higher lows. A daily close above 109.00 could encourage an incline higher towards 109.70. Alternatively, if bulls fail to maintain control above 109.00, the next levels of interest will be at 108.40 and 107.80, respectively.

Commodity spotlight – Gold

Gold has edged lower with prices sinking towards $1324, despite global equity markets suffering heavy losses.

An aggressively appreciating Dollar, expectations of higher U.S interest rates and easing geopolitical tensions are the most likely culprits for the yellow metal’s depreciation. With the Dollar expected to remain supported by rising bond yields and Fed hike speculation, zero-yielding Gold could feel the heat. If U.S GDP data release dishes out an upside surprise on Friday, bears may be injected with enough inspiration to send prices towards $1300. All in all, it must be kept in mind that Gold still remains in a wide $60 range with support at $1300 and resistance at $1360. Prices are likely to remain confined within these regions, until a fresh catalyst is brought into the picture.

Canadian Dollar Slide Continues as US T-Bills Shine

The Canadian dollar has continued its losing ways in the Wednesday session. Currently, USD/CAD is trading at 1.2889, up 0.44% on the day. The Canadian dollar has slipped 1.0%.percent this week, as USD/CAD has the 1.29 level in its sights. In economic news, BoC Governor Stephen Poloz will testify before the Standing Senate Committee on Banking. There are no key events in the US. On Thursday, the US releases durable goods orders and unemployment claims.

The US dollar continues to climb this week, buoyed by rising yields on US bonds, which have hit 4-year highs. On Wednesday, 10-year US Treasury notes have risen to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The US currency has also benefitted from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

The trade battle between China and the US has become a geopolitical hotspot, dominating the headlines and shaking global markets. After a series of tit-for-tat tariffs between the economic giants, there has been widespread concern that these moves could lead to a trade war which would slow down Chinese growth and trigger a global recession. However, the bellicose rhetoric between the sides has eased and US Treasury Secretary Steven Mnuchin is scheduled to lead a delegation to Beijing. On Tuesday, President Trump said that "we've got a very good chance at making a deal."

USD jumps ahead of US session, EUR/USD breaks yesterday’s low

Dollar rally picks up momentum again in enter into US session. In particular EUR/USD has now taken out yesterday's low at 1.2181 to resume recent fall to 1.2154 support.

As seen in the D heat map, only GBP/USD's is holding above yesterday's low for now. NZD, AUD, CHF and CAD are trading as the weakest ones.

As seen in the D heat map, only GBP/USD's is holding above yesterday's low for now. NZD, AUD, CHF and CAD are trading as the weakest ones.

Action bias table also shows overwhelming momentum.

Action bias table also shows overwhelming momentum.

Let's see how far USD can go in a day with no important economic data featured.

Let's see how far USD can go in a day with no important economic data featured.