Sample Category Title

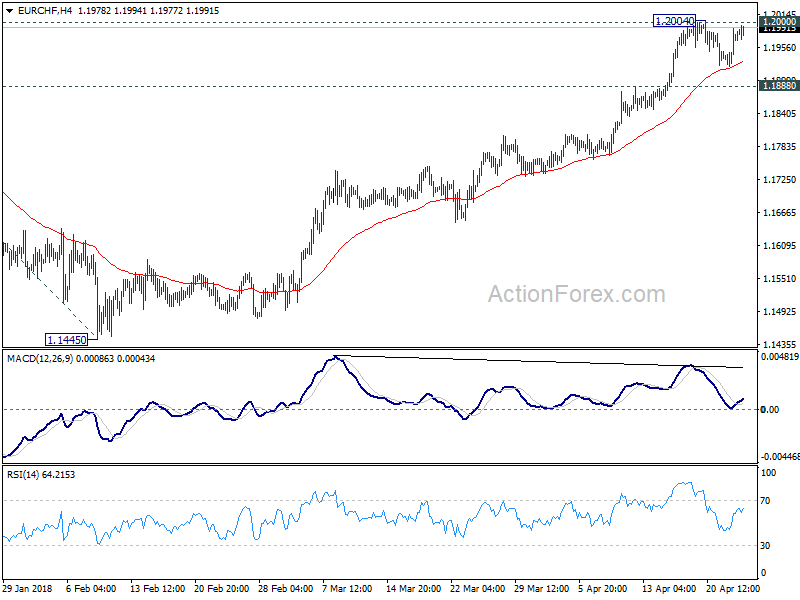

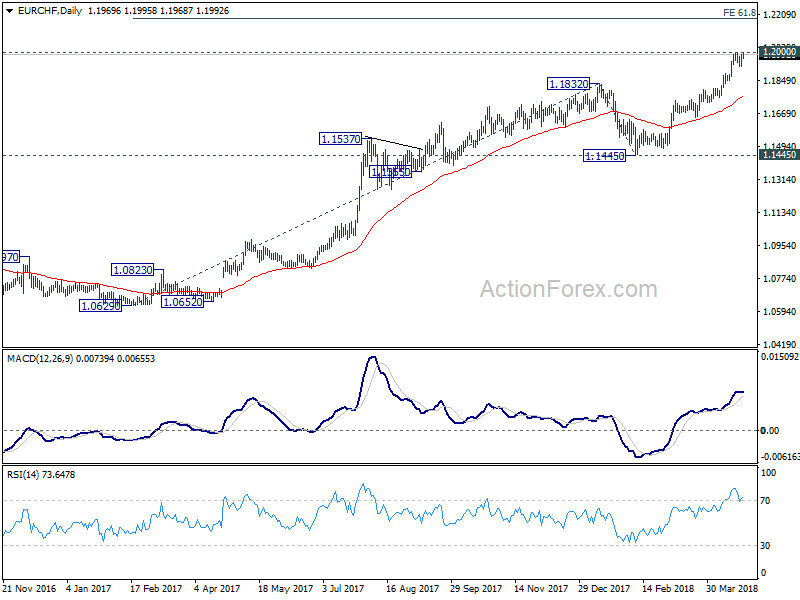

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1935; (P) 1.1963; (R1) 1.2001; More...

EUR/CHF recovered strongly, but it's still staying below 1.2004 temporary top. Intraday bias remains neutral first. Consolidation could extend but should be relatively brief as long as 1.1888 minor support holds. Decisive break of 1.2 will pave the way to 61.8% projection of 1.0629 to 1.1832 from 1.1445 at 1.2188. However, considering bearish divergence condition in 4 hour MACD, break of 1.1888 will indicate short term topping. In that case, deeper pull back would be seen back to 1.1445/1832 support zone.

In the bigger picture, long term up trend in EUR/CHF is still in progress. Prior SNB imposed floor at 1.2003 was already met but there is no sign of reversal yet. As long as 1.1445 support holds, we'd expect the up trend to extend to 2013 high at 1.2649 next.

USD Continues To Hold Onto Gains As Yields Rise

Notes/Observations

- Despite recent slowdown in EU growth and inflation; difficult to see a dovish Draghi on Thursday

Asia:

- Japan LDP Official: Dissolving lower house was an option if a motion of no confidence against the cabinet was submitted

- China officials said to be drafting guidelines on promoting imports as part of bid to balance foreign trade and would focus on certain consumer goods like food, clothing and medicine

- China PBOC: Previously announced RRR cut to be effective today (Wed) and would offset impact of maturity MLF loans

- China SOE official saw 'big room' for future RRR cut with 600-800 bps in such cuts in the coming 3 years. Believed the normal levels of banks’ reserve requirements should be 6-8% vs the current 14-16%. RRR cut did not mean a significant loosening of monetary policy

Europe:

- Italy 5-Star Party leader Di Maio: talks with the Northern League had ended; idea of a coalition govt with the center-right had passed. Saw the possibility for a coalition govt with PD (center-left). If talks with PD failed, then the only alternative would be a new election

- EU said to be prepared to offer Britain a better trade deal if the UK decides to stay inside the customs union after Brexit

- France President Macron: had frank discussions with Trump about Iran; want to work on a new nuclear deal with Iran. New deal should ban nuclear activities by Iran beyond 2025 (the current end date in the JCPOA). Did not know how President. Trump will decide on Iran Nuclear Deal; Nuclear issue is not the only issue with Iran as ballistic missiles also pose a problem

Americas:

- President Trump confirmed that Treasury Sec Mnuchin to visit China

- Canada Foreign Min Freeland: NAFTA negotiations to continue tomorrow (Wed, Apr 25th); prepared to respond to new proposals. US had presented some creative ideas on auto rules that have been helpful in moving talks forward

Energy:

- Weekly API Oil Inventories: Crude: +1.1M v -1.0M prior

Economic Data:

- (FR) France Apr Consumer Confidence: 101 v 100e

- (ES) Spain Mar PPI M/M: -0.9% v +0.1% prior; Y/Y: No est v 1.3% prior

- (AT) Austria Feb Industrial Production M/M: +0.3% v -0.7% prior; Y/Y: 5.1% v 7.3% prior

- (CH) Swiss Apr Credit Suisse Expectations Survey: 7.2 v 16.7 prior

- (PL) Poland Mar Unemployment Rate: 6.6% v 6.5%e

- (ZA) South Africa Q1 BER Consumer Confidence: +26 v -8 prior

Fixed Income Issuance:

- (IN) India sold total INR150B vs. INR150B indicated in 3-month, 6-month and 12-month bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -0.80% at 379.9, FTSE -0.5% at 7387, DAX -1.5% at 12353, CAC-40 -0.5 at 5419, IBEX-35 -0.7% at 9813, FTSE MIB -0.8% at 23854, SMI -0.6% at 8748, S&P 500 Futures -0.4%]

Market Focal Points/Key Themes:

- European Indices trade lower across the board following on from a sharp drop on Wallstreet and Asia and weaker futures this morning.

- Earnings remained the dominent theme with positive earnings from Credit Suisse, St Micro, Kering and Boohoo helping the shares buck the overall trend. Notable decliners include Osram Licht which trades lower after cutting guidance, while Tullow Oil and Antofagasta trade lower after production updates.

- Shire shares trade little changed after Takeda raised their offer again to £49/shr from £47 prior.

- Looking ahead notable earners include Anthem, Comcast, Twitter and Dow component Boeing.

Movers

- Consumer Discretionary [Kering [KER.FR] +6.4% (Earnings), Boohoo [BOO.UK] +13% (Earnings)]

- Financial [ Credit Suisse [CSGN.CH] +3.8% (Earnings)]

- Industrials [Bonava [BONAV.SE] -11% (Earnings), Antofagasta [ANTO.UK] -4.3% Production update), Kloeckner [KCO.DE] -9% (Earnings)]

- Technology [STMicro [STM.FR] +3.7% (Earnings), Osram Licht [OSR.DE] -10.4% (Prelim results, cuts outlook) ]

- Energy [ Statoil [STL.NO] -2.2% (Earnings), Tullow Oil [TKW.UK] -3.7% (Trading update)]

- Real Estate [Persimmon [PSN.UK] +0.8% (Trading update)]

Speakers

- ECB's Mersch (Luxembourg): Confidence on inflation has recently risen

- ECB's Vasiliauskas (Lithuania): More confident that it was time to transition from QE; closure of bond buying should not be abrupt

- Brexit Min Davis: Motion on Brexit agreement will be amendable. If Parliament rejected the deal then negotiation would fall. Bare-bones agreement was more likely than no deal

- China Ministry official welcomed the US to visit the country to negotiate trade issues and also urged the US to provide evidence of WTO rule violations

- China said to have raised the amount domestic funds could invest overseas

- China PBoC reiterated its prudent, neutral policy stance; recent RRR cut was to improve liquidity structure

Currencies

- The US 10-year yield moved above the 3% level and continued to help support the USD currency

- EUR/USD remained below the 1.22 level with dealers noting of key resistance at the 1.20/1.21 area. Focus turning the Thursday’s ECB meeting. Analyst saw no changed in policy this time around but the recent deterioration in Euro Zone economic growth and inflation indicators pondered whether the General Council would dare change its language. Market participant have dialed back expectations that the ECB would wind up the QE program in September when the asset purchases currently are slated to end and no longer pricing in a summer 2019 rate rise, but rather looking toward the end of next year for the first hike.

- GBP/USD was dealing in the mid-1.39 area ahead of Thursday House of Commons debate on the EU Withdrawal Bill. The Pound Sterling had little reaction of reports that EU was prepared to offer Britain a better trade deal if the UK decided to stay inside the customs union after Brexit.

- USD/JPY was higher for the 6th day to 2 ½ month high and was firmly established above the 109 level.

Fixed Income

- Bund Futures trade 22 ticks lower at 157.68 as European markets eye Thursday’s ECB meeting. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 120.95 lower by 26 ticks, tentatively breaking below the 121 handle. Support continues stands at 120.85 then 120.25, with upside resistance at 123.35 then 123.85.

- Wednesday’s liquidity report showed Tuesday's excess liquidity rose to €1.850T from €1.846T prior. Use of the marginal lending facility fell from €85M to €40M.

- Corporate issuance saw 10 issuers raise $13B in the primary market

Looking Ahead

- (DE) Germany govt updates its economic forecasts

- 06:00 (IL) Israel Mar Trade Balance: No est v -$2.3B prior

- 06:00 (FR) France Q1 jobseeekers Report

- 06:00 (CZ) Czech Republic to sell Bonds

- 06:45 (US) Daily Libor Fixing

- 07:00 (RU) Russia to sell combined RUB30.1B in OFZ bonds (2 tranches)

- 07:00 (US) MBA Mortgage Applications w/e Apr 20th: No est v +4.9% prior

- 07:00 (TR) Turkey Central Bank (CBRT) Interest Rate Decision: Expected to leave Benchmark Repurchase Rate unchanged at 8.00% (expected to hike the Late Liquidity rate 50 bps to 13.25% with range between 25-100)

- 07:00 (BR) Brazil Apr FGV Construction Costs M/M: 0.4%e v 0.2% prior

- 08:15 (UK) Baltic Dry Bulk Index

- 09:00 (MX) Mexico Feb Retail Sales M/M: +0.4%e v -0.2% prior; Y/Y: 0.4%e v 0.5% prior

- 09:30 (BR) Brazil Mar Current Account Balance: -$0.1Be v +$0.3B prior; Foreign Direct Investment(FDI): $4.5Be v $4.7B prior

- 10:30 (US) Weekly DOE Crude Oil Inventories

- 11:30 (US) Treasury to sell $17B in 2-Year Floating Rate Notes

- 13:00 (US) Treasury to sell $35B in 5-Year Notes .

- 13:30 (BR) Brazil Mar Central Govt Budget Balance (BRL): -16.2Be v -19.3B prior

- (BR) Brazil Apr CNI Consumer Confidence: No est v 101.9 prior

- (CO) Colombia Mar Retail Confidence: No est v 20.5 prior; Industrial Confidence: No est v 1.9 prior

ECB Mersch noted increasing confidence, Vasiliauskas said it’s time to transit from asset purchase

Articles by ECB Executive Board member Yves Mersch and Governing Council member Vitas Vasiliauskas were published Wednesday by Eurofi today. While Mersch's article was submitted back on March 21 and Vasiliauskas on March 15, there're worth a quick read.

Mersch's article was on the topic of "Monetary policy in the euro area: solid expansion with timid price pressure". He noted that:

- "Confidence has recently risen and convergence is being confirmed -- partly because the temporary decline in the inflation rate has been weaker than our internal calculations had predicted,"

- "More resilience will follow eventually. Still, patience and persistence with respect to our monetary policy is required."

Vasiliauskas article was on the topic of "The time is approaching to seriously consider a smooth transition from the APP". He noted:

- "We have witnessed the strengthening of broad-based growth and steadily declining unemployment, providing conditions for inflation convergence to our objective."

- "This has increased my confidence that it is time to transition from the asset purchase program. However, the closure of the program should not be abrupt."

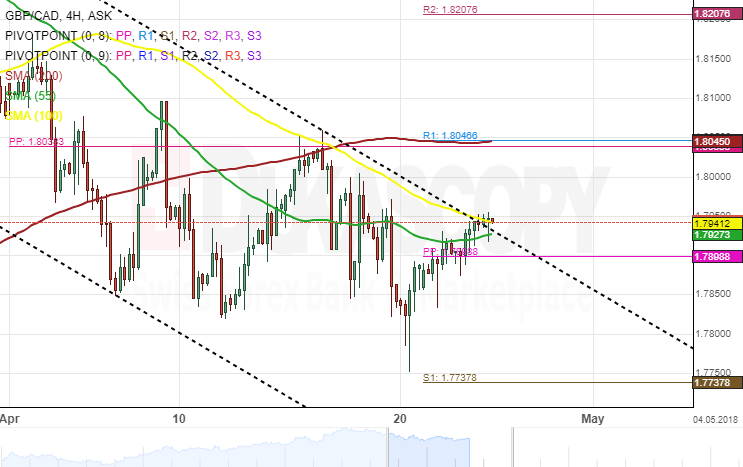

GBP/CAD 4H Chart: Breakout From SMAs

The British Pound has been trading in a dominant ascending channel against the Canadian Dollar since September. The exchange rate neat movement in this channel was interrupted in mid-March when a reverse south occurred after reaching a resistance set by the monthly pivot point near the 1.8457 area.

The GBP/CAD currency pair has since been moving in a junior descending pattern. Meanwhile, the pair has breached both the 55– and the 100– hour SMAs and the upper boundary of the junior channel.

Everything being equal, the currency exchange rate likely to continue moving in the channel down until it reaches the lower boundary of the dominant channel.

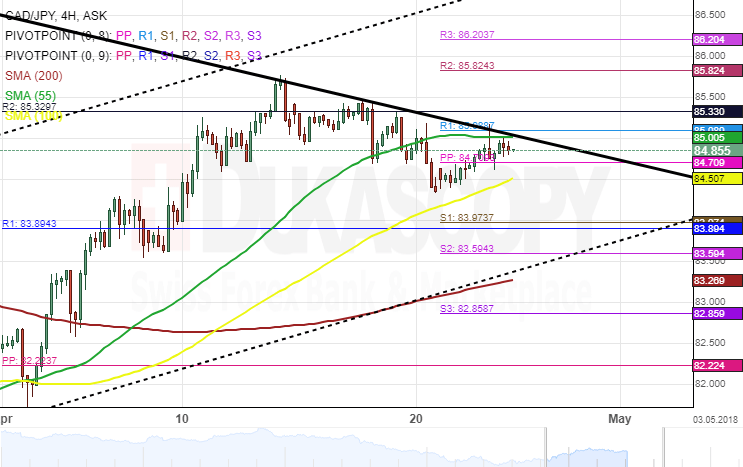

CAD/JPY 4H Chart: Stranded Between SMAs

The Canadian Dollar has been moving in a junior ascending channel against the Japanese Yen. The currency pair bounced off the lower boundary on March 19 and has since surged.

The exchange rate has tested the upper border of a dominant descending channel and could be set for a breakout. The CAD/JPY currency pair was stranded between SMAs at the time of this analysis. The 55– hour simple moving average was restricting the pair from making further movement north. While the 100– hour SMA was providing support.

As for near future, if the aforementioned breakout occurs, the currency exchange rate is likely to reach a potential target at 87.00 set by the monthly pivot point.

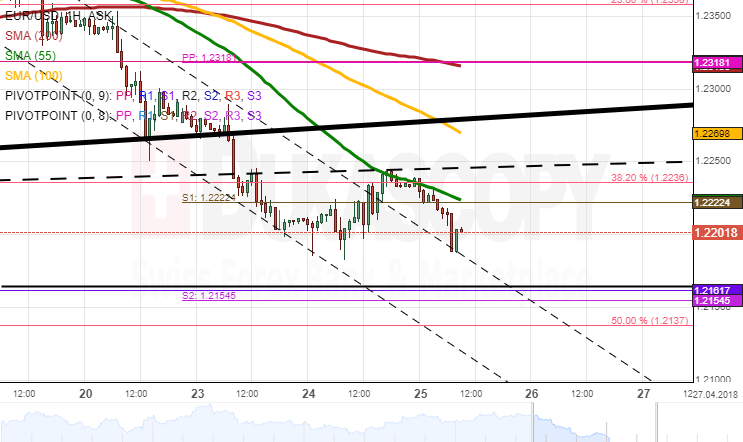

EUR/USD Analysis: Fails To Overcome 55-Hour SMA

The common European currency failed to move below the 1.22 mark due to the strong support of the 100-day SMA. This was followed by a slight move upwards, but a steep advance was restricted by the 55-hour moving average, a breached trend-line and the 38.20% Fibonacci retracement. This cluster remained an unbreakable barrier during the Asian session, as well.

The general tendency of the pair is likely to remain northwards this week, as it should target the 200-hour SMA and the 23.60% Fibo retracement circa 1.2350.

Meanwhile, this session might mark a brief period of consolidation in the 1.2200/60 during the first part of the day in response to pressures from the aforementioned barriers. The latter, however, should be surpassed, and a test of the 100-hour SMA should follow near 1.23.

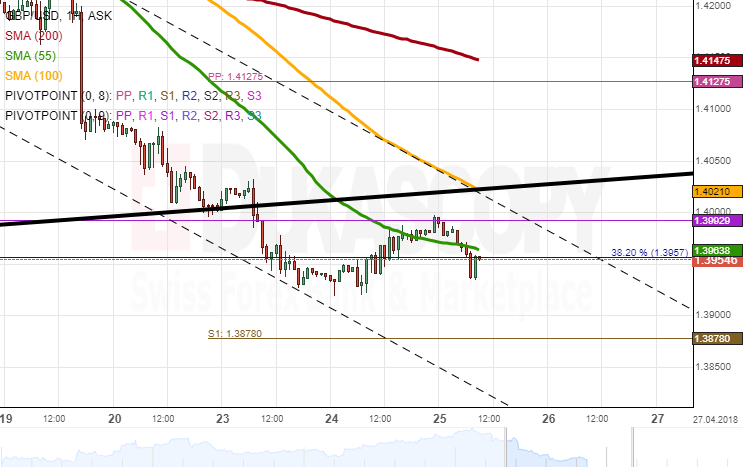

GBP/USD Analysis: Strong Resistance Ahead

Following a four-day decline against the US Dollar, the Sterling managed to recover some of its lost positions on Tuesday. As a result, it breached the 55-hour SMA, but was nevertheless limited by the monthly PP at the psychological 1.40 mark.

An upside breakout of the 55-hour moving average sends bullish signals, thus suggesting that this recovery is likely to continue during the remaining part of the week, as well.

This session, however, should not produce large gains due to a strong resistance cluster located at 1.4050. Apart from the 100-hour SMA and a breached senior channel, the 55-day SMA is likewise located in this area.

This might either set the Pound for a movement sideways or another fall down to the weekly or monthly S1s at 1.3875 and 1.3740, respectively.

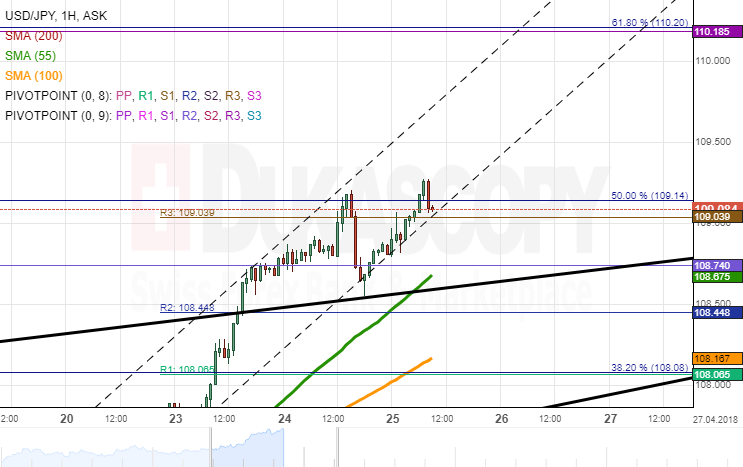

USDJPY Analysis: Allays Near 109.00

USD/JPY managed to remain steady during the previous session, thus showing that the strong upside momentum that prevailed earlier this week has allayed.

The US Dollar peaked at the weekly R3 and the 50.0% Fibonacci retracement near 109.00, went for a minor decline but nevertheless returned near this mark on Wednesday morning.

It is expected that this session is dominated by bears that should send the pair closer to the 55-hour SMA and the monthly R2 at 108.60. Despite lack of fundamental releases, this are should surrender, thus paving the way for the Greenback to approach the 38.20% Fibo retracement, the 100-hour SMA and the weekly R1 at 108.00.

In case the 55-hour SMA holds strong, the rate should not surpass the 109.50 mark.

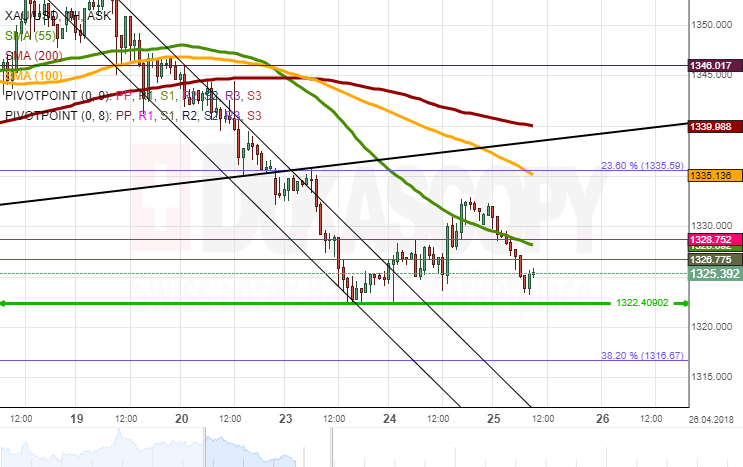

Gold Analysis: Lingers Near 1,330.00 On Wednesday Morning

The yellow metal has been strengthening steadily against the Greenback following a reversal from the 1,322.00 mark late on Monday.

The pair breached the combined resistance of the 55-hour SMA and the monthly PP near 1,330.00 on Tuesday evening but has since failed to accelerate. This might be explained by the fact that bulls have not still gathered enough momentum to dash through this mark which is additionally reinforced by the 55-day SMA and the 200-period SMA on the 4-hour time-frame.

If this area is breached, Gold should pick up speed and reach the 1,340.00 level by the end of this session. Meanwhile, a failure to do so, should send the rate back to its April support at 1,322.00.

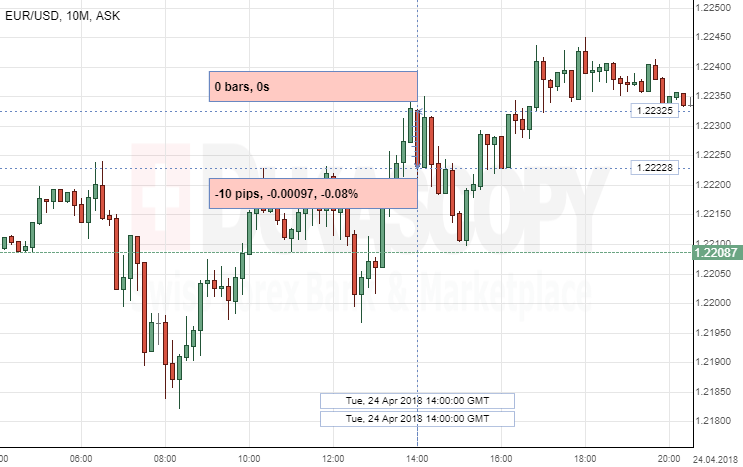

EUR/USD: CB Consumer Confidence

The Greenback strengthened against the Eurozone's single currency, following the US CB Consumer Confidence data release on Tuesday. The EUR/USD currency pair lost 10 pips, or 0.08%, to continue fluctuating in the 1.2226 area.

The Conference Board Inc. released better-than-expected Consumer Confidence, surpassing the forecasts of 126.0 with the number of 128.7 in April.

EUR/USD currency pair remained under pressure. One of the main reasons for Greenback to rally was high 10-year United States treasury bills, which showed notable gains during the start of the week.