Sample Category Title

DAX Slumps as US Bond Yields Continue to Rise

The DAX index has posted sharp losses in the Wednesday session. Currently, the DAX is trading at 12,335 points, down -1.70% on the day. On the release front, there are no German or eurozone events. On Thursday, the ECB releases a rate statement.

European stock markets have taken a thrashing on Wednesday, with the DAX falling close to 2 percent. On the DAX, banking stocks are sharply lower. Commerzbank has fallen 2.80% while Deutsche Bank has plunged 3.27%. The sharp losses reflect investor concerns over rising US bond yields, which have climbed to 4-year highs. On Wednesday, 10-year US Treasury notes have risen to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for bond yields and conversely, weighing on equities.

All eyes are on the ECB, which will release a rate statement, followed by a press conference with ECB President Mario Draghi. Eurozone indicators have softened in recent weeks, raising concerns that Draghi could sound dovish about the eurozone economy. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The ECB has said it intends to continue bond purchases until at least September, to keep interest rates at current levels until “well past” the end of the program. Traders shouldn’t expect any dramatic moves at the policy meeting, as the bank will likely continue to preach patience and prudence. However, a dovish message from Draghi could weigh on the European stock markets.

German Economic Ministry revised growth forecast down to 2.3% in 2018

The German Economy Ministry lowered growth forecast for this year today. For 2018, GDP is now projected to grow 2.3%, downgraded from January forecast of 2.4%. For 2019, growth is projected to be at 2.1%.

Economy Minister Peter Altmaier said that the German economy s in a "robust state", "remains buoyant and the upturn is continuing." Also, while recent economic data have been disappointing, Altmaier said they ""are in no way pointing to a downturn." He added that "any growth in the region of 2 percent or above is exceptionally good growth, if you compare it with the history of the last 10-15 years in Germany."

Dollar Receives Further Boost From US Treasury Yields

Here are the latest developments in global markets:

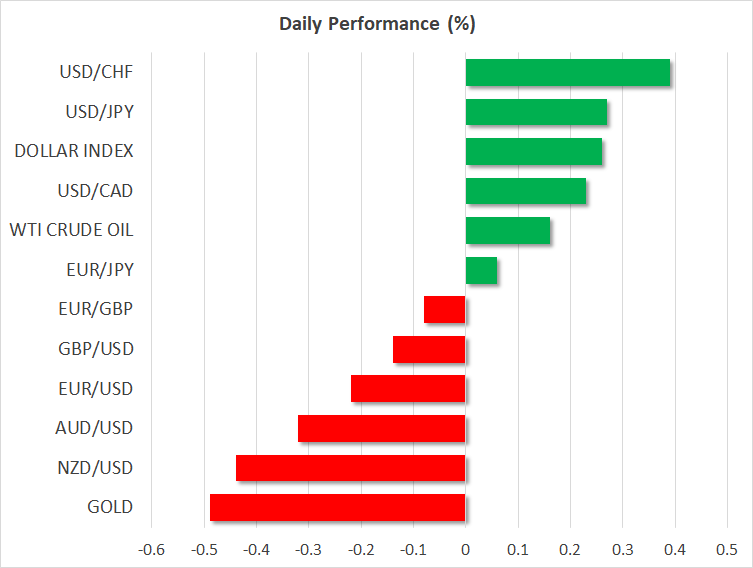

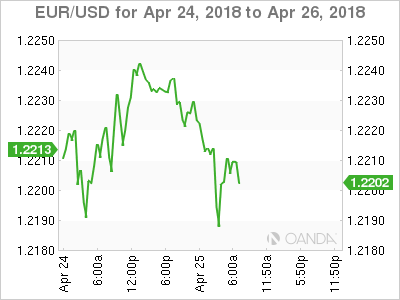

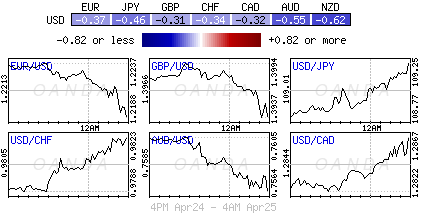

FOREX: The dollar continued to receive love from US Treasury yields, with the 10-year note spiking to a fresh 3-year high of 3.02% during the early European afternoon, underpinned by concerns of rising inflation and increasing debt supply. Easing trade tensions also lifted investors’ confidence in the currency after the US President admitted on Tuesday that China and the US “have got a very good chance at making a deal”. In the aftermath, the dollar index made a fresh 3 ½-month high at 91.11, while dollar/yen reached a new peak at 109.26, its highest since February 8. Meanwhile, euro/dollar remained under pressure, rising moderately from 1.2185 to 1.2221 (-0.16%), unable to gain much from hawkish comments delivered by ECB members, Yves Mersch and Vitas Vasiliauskas today as the spread between the US and German 10-year government bond yields turned the widest in 29 years. Note that ECB policymakers are meeting today to decide on monetary policy, with the announcement made tomorrow. Pound/dollar did not have a good day either so far, trading weak at 1.3962 (-0.09%). Political risks were weighing on the pair given the growing split in May’s inner cycle regarding the Brexit withdrawal bill which could interrupt progress in EU-UK negotiations. In antipodean currencies, aussie/dollar and kiwi dollar were the worst performers, changing hands lower at 0.7584 (-0.26%) and 0.7093 (-0.37%). Dollar/loonie was up at 1.2856 (+0.18%).

STOCKS: Stocks in Europe were all flashing red at 0800 GMT following their Asian and US counterparts as rising US Treasury yields continued to steal demand from equities. The pan-European STOXX 600 retreated further below its 10-week highs, losing 0.43%, on energy and basic materials. The blue-chip Euro STOXX 50 was also down by an equivalent percentage after peaking at an 8-week high yesterday. The German DAX 30 tumbled by 0.70%, Britain’s FTSE 100 fell by 0.32% and Spain’s IBEX 35 pulled back by 0.56%. Asian equities closed lower, while futures tracking US stock indices were hinting that losses may be in store for the US. In corporate news, Credit Swiss, Switzerland’s second biggest bank, and the luxury goods company Kering saw their shares surge after both companies posted an upbeat performance in the first quarter of 2018. However, the gains were not enough to offset losses in the European stock markets.

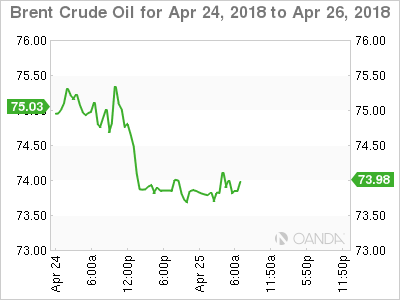

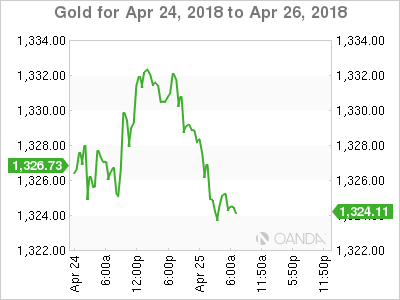

COMMODITIES: Oil prices gained some ground, recovering from the losses made after the API weekly oil report showed an unexpected increase in US crude inventories. OPEC-led supply cuts and rising speculation that the US will impose fresh sanctions on Iran were the main market drivers. Yesterday, Trump opposed the 2015 nuclear deal (signed by Iran, the United States, the United Kingdom, Russia, France, China, Germany and the European Union) despite the French President’s efforts to persuade him to maintain the agreement. WTI crude and Brent were trading at $67.74 (+0.10%) and $73.80 (-0.08%) per barrel. In precious metals, gold was hovering at $1,324 (-0.46%) per ounce, near three-week lows.

Day Ahead: Equities could dominate attention in absence of data

The calendar will be light of data for the remainder of the day, with investors turning their eyes on long-term US Treasury yields which managed to break above levels last seen back in 2014 over concerns on rising inflationary pressures and debt-issuance. It would be interesting to see whether US Treasury yields will maintain their positive momentum in the following days, affecting currency and equity markets as well.

The only release today in focus will be the EIA weekly report on US oil inventories, which could add further volatility to oil prices. According to forecasts, crude inventories are expected to drop by 2.043 million barrels in the week ending April 20 compared to a fall of 1.071 million in the previously tracked week.

Corporate earnings remain on the forefront on Wednesday, with AT&T, eBay, Facebook and Ford reporting results after the closing bell on Wall Street.

Turning to today’s public appearances, at 2015 GMT Bank of Canada Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins will be appearing before a Senate Standing Committee on Finance.

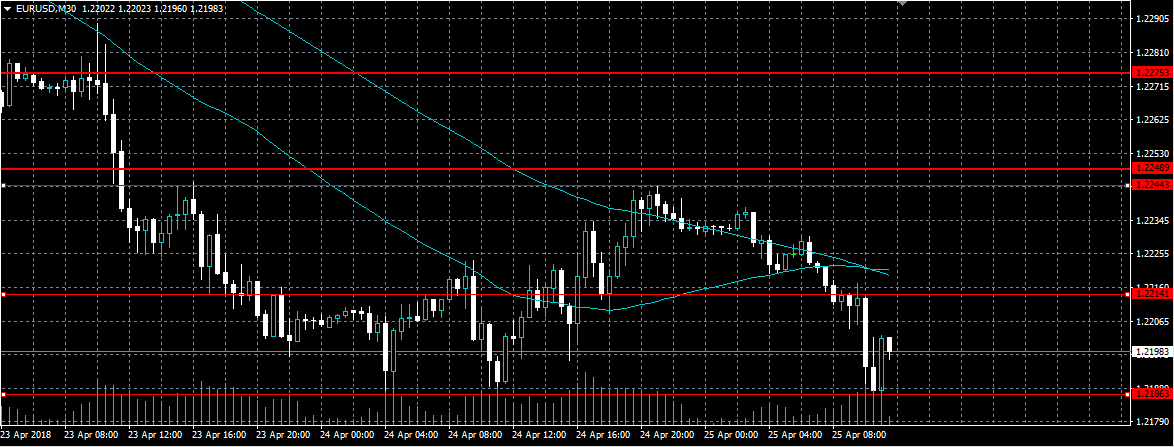

EURO Back Under Pressure Below 1.2214

The euro continues to trade to the downside against the U.S dollar, hitting 1.2186, during the European trading session as U.S Treasury-yields push the U.S dollar index sharply higher. The EURUSD pair currently trades around the 1.2198 level, after a strong technical rejection from the 1.2244 level on Tuesday. Traders now look towards the 91.00 level on the U.S dollar index for direction, and if the U.S 10-year treasury-yield can hold above the key three percent level.

The EURUSD pair remains bearish while trading below the 1.2214 level, further losses towards the 1.2184 and 1.2150 levels seems likely.

If the EURUSD pair starts to hold price-action above the 1.2214 resistance level, a further correction back towards 1.2248 and 1.2275 levels may occur.

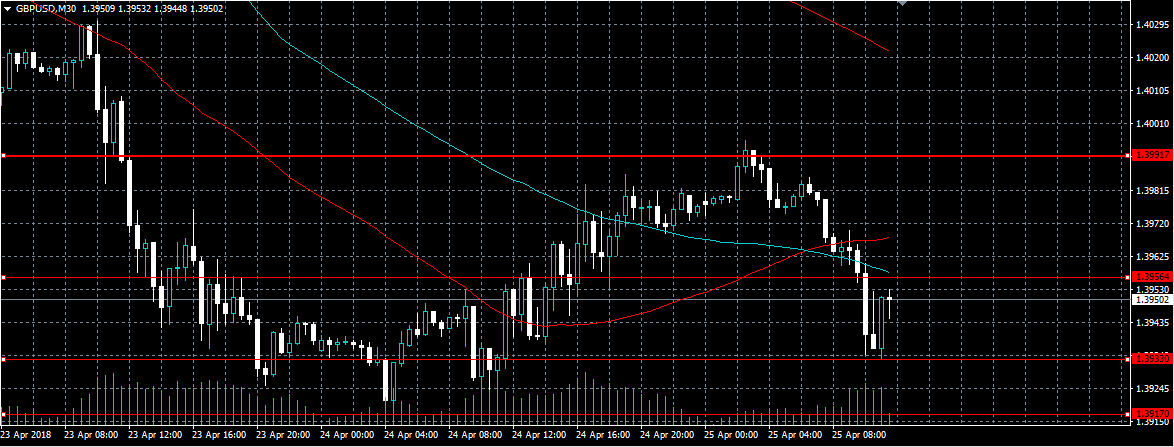

GBPUSD Now Bearish Below 1.3956 Pivot

The British pound has started to decline lower against the greenback, hitting 1.3933, as traders move back into the U.S dollar after the 10-year bond-yield breached the key three percent level. The GBPUSD pair currently trades around the 1.3950 level, with downside pressures likely to remain while price-action trades below the pivotal 1.3956 level. With a lack of macroeconomic data during the U.S trading session, intense focus is like to remain on the U.S dollar and U.S bond yields.

The GBPUSD pair is intraday bearish while trading below the 1.3956 level, losses may now extend towards the 1.3917 and 1.3880 levels.

If GBPUSD pair moves back above the 1.3956 level for an extended period, intraday buyers may again test towards the 1.3992 resistance level.

Dollar Yields To Higher Rates

Wednesday April 25: Five the markets are talking about

With U.S Treasury yields backing up, fixed income dealers are pricing in the possibility that there will be four Fed rate hikes this year and not the three they signaled in March.

Given U.S economic growth and signs that domestic inflation could be picking up, fed fund futures are pricing a +53% chance of four hikes, up from +48% on Monday and +33% a month ago.

Expectations for tomorrow's European Central Bank (ECB) meeting are for a ‘low key' event. The central bank's ongoing forward bias would suggest that there is no chance of any change in the overnight base rate.

Since last month's ECB's meeting, the eurozone real economy has show signs of cooling – industrial production has extended its monthly declines to three, while retail sales is expected to eat into Q1 GDP growth and even investor and business sentiment has fallen to new six-month lows.

At the obligatory press conference, expect Draghi to highlight some of the downside potential inherent in a strong EUR (€1.2200) and the increased threats of a trade war.

Elsewhere, the Bank of Japan's (BoJ) two-day policy meeting begins tomorrow; decision and forecasts are expected on Friday (April 27).

1. Stocks are on the back foot

In both Asia and Europe, equities have been tracking yesterday's Wall Street decline.

In Japan, the Nikkei ended -0.3% lower, pressured mostly by Takeda Pharmaceutical stock plummeting -7% as investors fretted about the company's ability to finance the Shire cash and stock deal. The broader Topix dropped -0.1%.

Down-under, Aussie shares rose overnight, driven by banks as benign inflation data backed expectations interest rates will remain accommodative for some time, but gains were capped by losses in materials on an extended slide in aluminum prices. The S&P/ASX 200 index ended up +0.6%, while in S. Korea, the Kospi fell for a fourth consecutive session.

In Hong Kong, equities followed the Asian market lower. The Hang Seng index fell -1.0%, while the China Enterprises Index lost -1.2%.

In China, stocks closed down on Wednesday as gains in healthcare firms were offset by losses in real estate and energy shares. Both the blue-chip CSI300 index and the Shanghai Composite Index fell -0.4%.

In Europe, regional indices trade lower across the board following on from a sharp drop on Wall Street and Asia.

U.S stocks are set to open in the ‘red' (-0.4%).

Indices: Stoxx600 -0.80% at 379.9, FTSE -0.5% at 7387, DAX -1.5% at 12353, CAC-40 -0.5 at 5419, IBEX-35 -0.7% at 9813, FTSE MIB -0.8% at 23854, SMI -0.6% at 8748, S&P 500 Futures -0.4%

2. Oil dips as rising U.S supply clouds bull-run, gold lower

Oil prices are under pressure ahead of the U.S open, falling back from their three-year highs reached Tuesday, as rising U.S fuel inventories and production weighed on market sentiment.

Brent crude oil futures are at +$73.71 per barrel, down -15c or -0.2%, from Tuesday's close and almost -$1.8 below the November-2014 high of +$75.47 a barrel reached on Monday. U.S West Texas Intermediate (WTI) futures are down -12c, or -0.2% at +$67.58 a barrel.

The oil market has been lifted by supply cuts led by OPEC and the possibility of renewed U.S sanctions against Iran.

Note: The U.S has until May 12 to decide whether it will leave the Iran nuclear deal and re-impose sanctions against OPEC's third-largest producer.

Market prices are being capped by U.S production – higher crude prices are bringing more U.S producers back “on line.”

Expect investors to take direction from this morning's weekly EIA report (10:30 am EDT).

Gold prices are under pressure as U.S bond yields trade above the psychological +3% level, which has lifted the dollar to its highest in more than three-months. Spot gold is down -0.5% at +$1,323.59 per ounce, while U.S. gold futures has lost -0.6% to trade at +$1,325 per ounce.

Note: The yellow metal rallied +0.5% yesterday to break a three-session losing streak.

3. Yields remain near four-year highs

The U.S 10-year Treasury yield trades atop of its four-year highs.

Ahead of the U.S open, the yield on the 10-year note has backed up +2 bps to +3.02%. Higher U.S yields are supporting other G7 sovereign yields.

In Germany, the 10-year Bund yield has also climbed +2 bps to +0.65%, the highest in seven-weeks, while in the U.K, the 10-year Gilt yield has gained +3 bps to +1.568%, the highest in two-months.

Note: The last time yields traded atop of current yield levels it hurt investor risk appetite and sent equities tumbling. It also came shortly before crude oil prices plummeted -75%.

The European Central Bank (ECB) guidance tomorrow (April 26), about the future of its stimulus programme, is the next thing that may cause some yield movement.

Last Friday, the ECB's Draghi said he was confident that the inflation outlook has picked up, but uncertainties “warrant patience, persistence and prudence.”

4. Dollar yields to higher rates

Withe the U.S 10-year yields trading above the psychological +3% is supporting the ‘big' dollar for now.

EUR/USD (€1.2210) is still holding support at €1.2150, as investors wait to hear from the ECB tomorrow before making their next move. The ‘single unit' could quickly fall to €1.2050 this week if the ECB disappoints tomorrow or if U.S GDP comes in on the firm side on Friday.

Note: Market participant have dialled back expectations that the ECB would wind up the QE program in September when the asset purchases currently are slated to end and no longer pricing in a summer 2019 rate rise, but rather looking toward the end of next year for the first hike.

GBP/USD (£1.3962) is little changed ahead of tomorrow's House of Commons debate on the E.U Withdrawal Bill. The pound has seen little movement despite reports that the E.U is prepared to offer the U.K a better trade deal if it decides to stay inside the customs union after Brexit.

USD/JPY (¥109.03) is a tad higher for a sixth consecutive session.

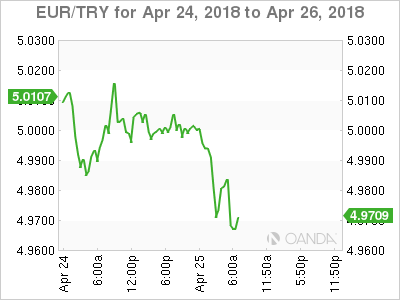

5. Turkey's Central Bank

The Turkish central bank is holding its monetary policy meeting this morning (07:00 am EDT) and the state lender is expected hike its top rate by +50 bps to +13.25%.

The techies believe that any inaction by the central bank could see the TRY ($4.0608) come under pressure again. USD/TRY is down by -0.65% at $4.0619 ahead of the announcement.

Euro Posts Small Losses, ECB Policy Statement Next

EUR/USD has posted slight losses in the Wednesday session, erasing the gains seen on Tuesday. Currently, the pair is trading at 1.2212, down 0.17% on the day. It’s a quiet day on the release front, as the sole event is Crude Oil Inventories. On Thursday, the ECB will set interest rates, while the US releases durable goods orders and unemployment claims.

What can we expect from the ECB policy statement on Thursday? Eurozone indicators have softened in recent weeks, raising concerns that ECB President Mario Draghi could sound dovish about the eurozone economy. This could weigh on the euro. At the March meeting, policymakers took a small step, dropping a pledge to increase stimulus if needed. Will we see additional ‘baby’ steps at the April meeting? The ECB has said it intends to continue bond purchases until at least September, to keep interest rates at current levels until “well past” the end of the program. Traders shouldn’t expect any dramatic moves at the policy meeting, as the bank will likely continue to preach patience and prudence.

Is the German locomotive in trouble? German business confidence took a hit in April, as Ifo Business Climate fell to 102.1 points, down from 114.7 points a month earlier. This marks the lowest level since November 2012. German key indicators have softened recently, pointing to a slowdown in economic conditions in the first quarter. We’ll get a look at the mood of consumers, with the release of German GfK Consumer Climate on Thursday.

The trade battle between China and the US has become a geopolitical hotspot, dominating the headlines and shaken global markets. After a series of tit-for-tat tariffs between the economic giants, there has been widespread concern that these moves could lead to a trade war which would slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute. The markets will be hoping for a truce between the sides, as any further tariffs could rattle the markets.

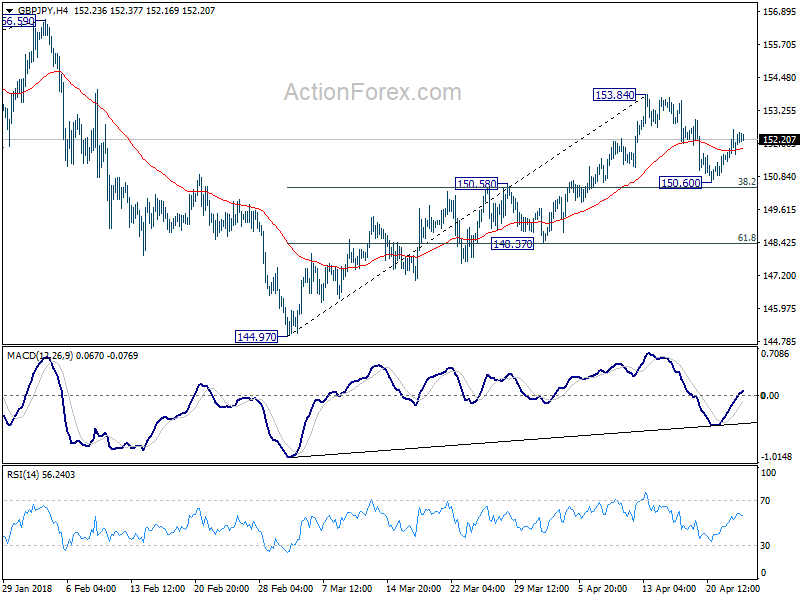

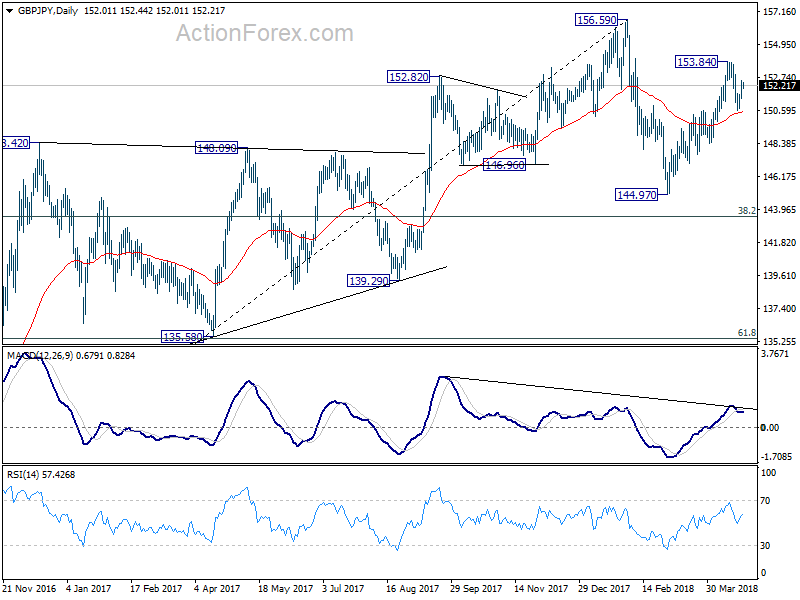

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.46; (P) 152.03; (R1) 152.65; More...

Intraday bias in GBP/JPY remains neutral at this point. We're holding on to the view that corrective rise from 144.97 should have completed at 153.84 already. Hence, another fall is expected in the cross. Break of 150.60 will target 148.37 support first. Break will bring retest of 144.97 low. However, firm break of 153.84 will invalidate our view and extend the rise from 144.97 towards 156.59 high.

In the bigger picture, price actions from 156.59 are viewed as a corrective pattern. For now, we'd expect at least one more fall for 38.2% retracement of 122.36 to 156.59 at 143.51 before the consolidation completed. Though, firm break of 156.59 will resume whole up trend from 122.36 (2016 low) to 50% retracement of 195.86 (2015high) to 122.36 at 159.11 next.

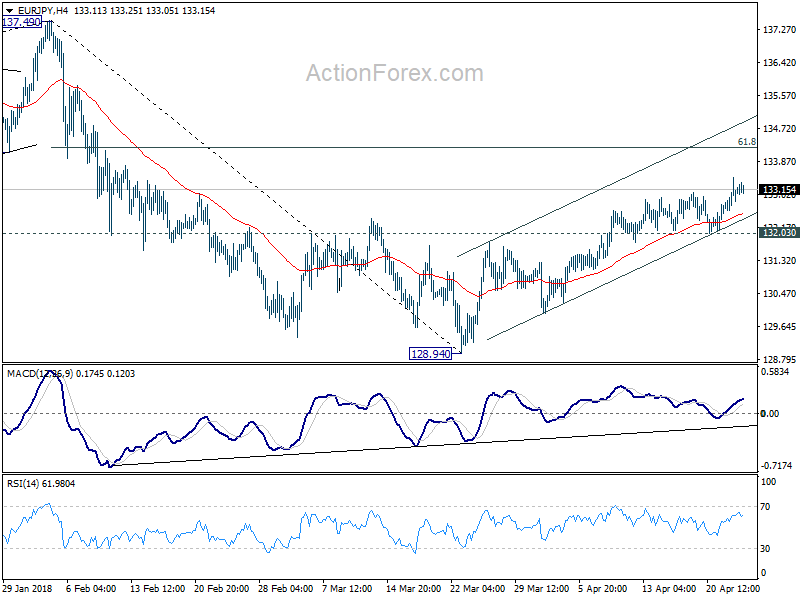

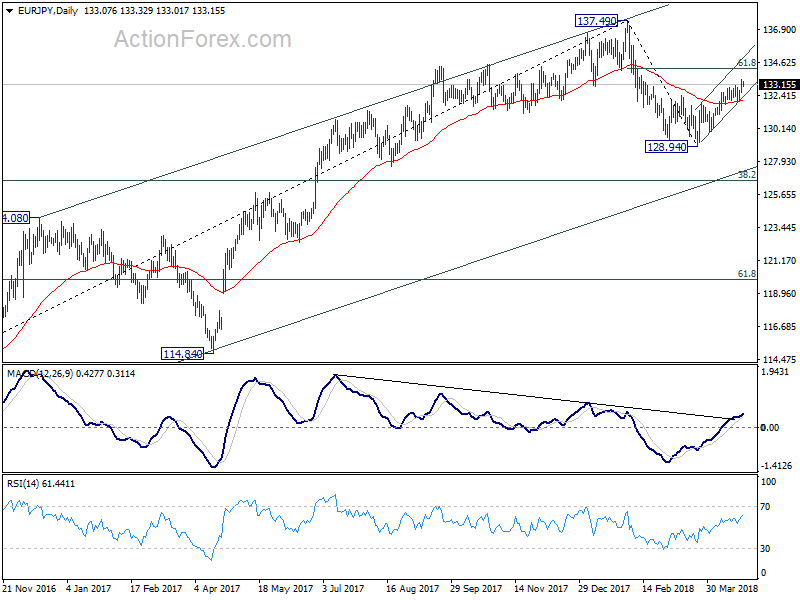

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.65; (P) 133.06; (R1) 133.52; More....

Intraday bias in EUR/JPY stays mildly on the upside at this point. Rebound from 128.94 should extend higher. However, it's after all seen as a corrective move. Therefore, expect strong resistance from 61.8% retracement of 137.49 to 128.94 at 134.22 to limit upside. Break of 132.03 will turn bias to the downside for retesting 128.94 low. However, sustained break of 134.22 will turn focus back to 137.49 high instead.

In the bigger picture, price action from 137.49 medium term top are developing into a corrective pattern. Strong support from 55 week EMA (now at 129.91) suggests that the first leg has completed at 128.94 already. Nonetheless, break of 137.49 is needed to confirm resumption of the rise from 109.03 (2016 low). Otherwise, we'd expect more corrective range trading, with risk of another fall to 38.2% retracement of 109.03 to 137.49 at 126.61 before completion.

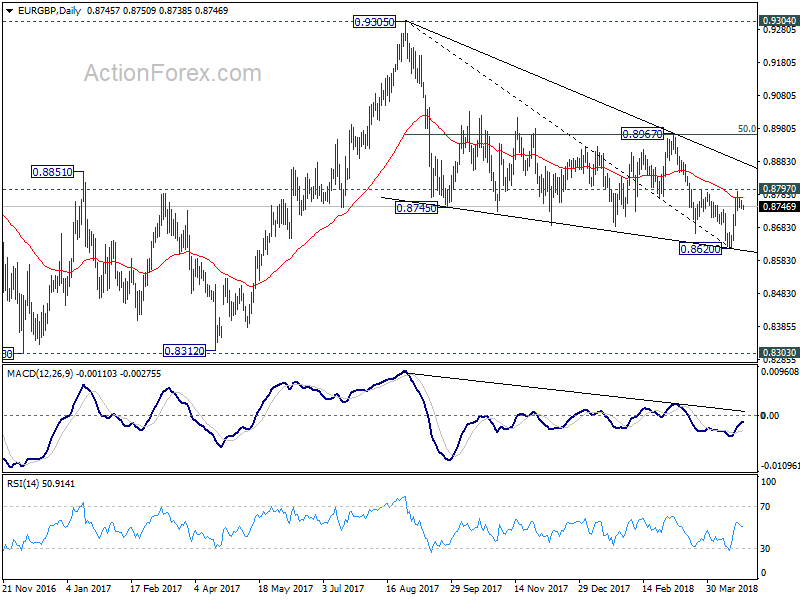

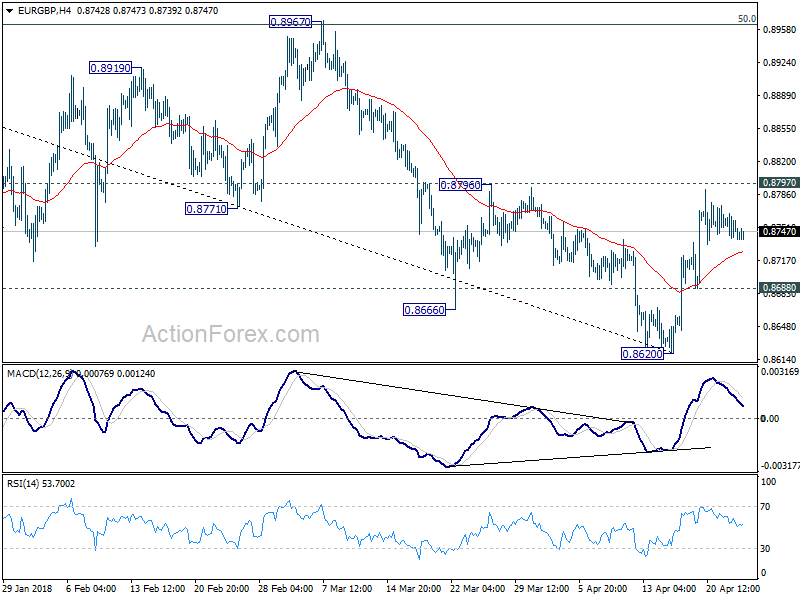

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8739; (P) 0.8752; (R1) 0.8765; More...

Intraday bias in EUR/GBP remains neutral for the moment. Further rise is expected as long as 0.8688 minor support holds. Break of 0.8797 will extend the rise from 0.8620 to key cluster resistance at 0.8967 (50% retracement of 0.9305 to 0.8620 at 0.8963) next. On the downside, break of 0.8688 minor support will dampen the bullish case and turn focus back to 0.8620 instead.

In the bigger picture, for now, the decline from 0.9305 is seen as a leg inside the long term consolidation pattern from 0.9304 (2016 high). Such consolidation pattern could extend further. Hence, in case of strong rally, we'd be cautious on strong resistance by 0.9304/5 to limit upside. Meanwhile, in another decline attempt, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.