Sample Category Title

Pound Under Pressure As US Bond Yields Rise

The British pound has posted small gains in the Wednesday session, erasing the gains seen on Tuesday. In North American trade, GBP/USD is trading at 1.3945, down 0.23% on the day. The sole event on the schedule is Crude Oil Inventories, which posted a gain of 2.2 million, easily beating the estimate of -1.6 million. Thursday will be much busier, as the US releases durable goods orders and unemployment claims.

The US dollar continues to climb against its rivals, and GBP/USD has slipped 2.1% since April 16. Much of the US streak can be attributed to rising yields on US bonds, which have hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The US currency has also benefited from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

One of the most thorny issues surrounding Brexit is the Northern Ireland border. Ireland is a member of the European Union, and would like to avoid a hard border with the north. However, once Britain leaves the UK, there will have to be some type of border controls between Ireland and Northern Ireland. So far, no satisfactory solution has been found. On Wednesday, Brexit Secretary David Davis said that a solution isn’t needed until the end of the transition period, which concludes in January 2021, since the UK will remain in the single market until that date. What happens after that? Davis would like to see the UK reach a comprehensive trade deal with the EU and a frictionless border, but Brussels may not be interested, with European leaders still smarting over Britain’s exit. Any scenario, called the “backstop plan”, envisions some time of “harmonization” of trade rules between Northern Ireland and the EU. However, the May government has continually expressed opposition to such a plan, so a solution will likely remain elusive until the clock forces the sides to show more flexibility.

Gold Slips To 5-Week Low As Bond Yields Boost Dollar

Gold prices have resumed a downward slide, as the base metal has recorded losses in four of the past five sessions. In Wednesday’s North American trade, the spot price for an ounce of gold is $1322.33, down 0.61% on the day. In the US, it was a quiet day, with no major releases. Thursday promises to be busier, as the US releases durable goods orders and unemployment claims.

The greenback rally has sent its rivals to lower ground, with gold also heading lower. Gold has fallen 2.1% since April 16, and earlier on Wednesday dropped to $1318 an ounce, its lowest level since March 19. Much of the dollar rally can be attributed to rising yields on US bonds, which have hit 4-year highs this week. On Wednesday, 10-year US Treasury notes climbed to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. Gold has also lost ground due to a recent reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

The trade battle between China and the US has become a geopolitical hotspot, dominating the headlines and shaken global markets. After a series of tit-for-tat tariffs between the economic giants, there has been widespread concern that these moves could lead to a trade war which would slow down Chinese growth and trigger a global recession. However, US Treasury Secretary Steven Mnuchin sought to lower the rhetoric on the weekend, saying that he was considering a trip to China, adding he was “cautiously optimistic” that the two sides could resolve the trade dispute. If relations between the US and China improve, gold prices could continue to head lower.

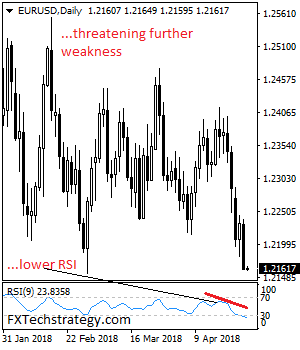

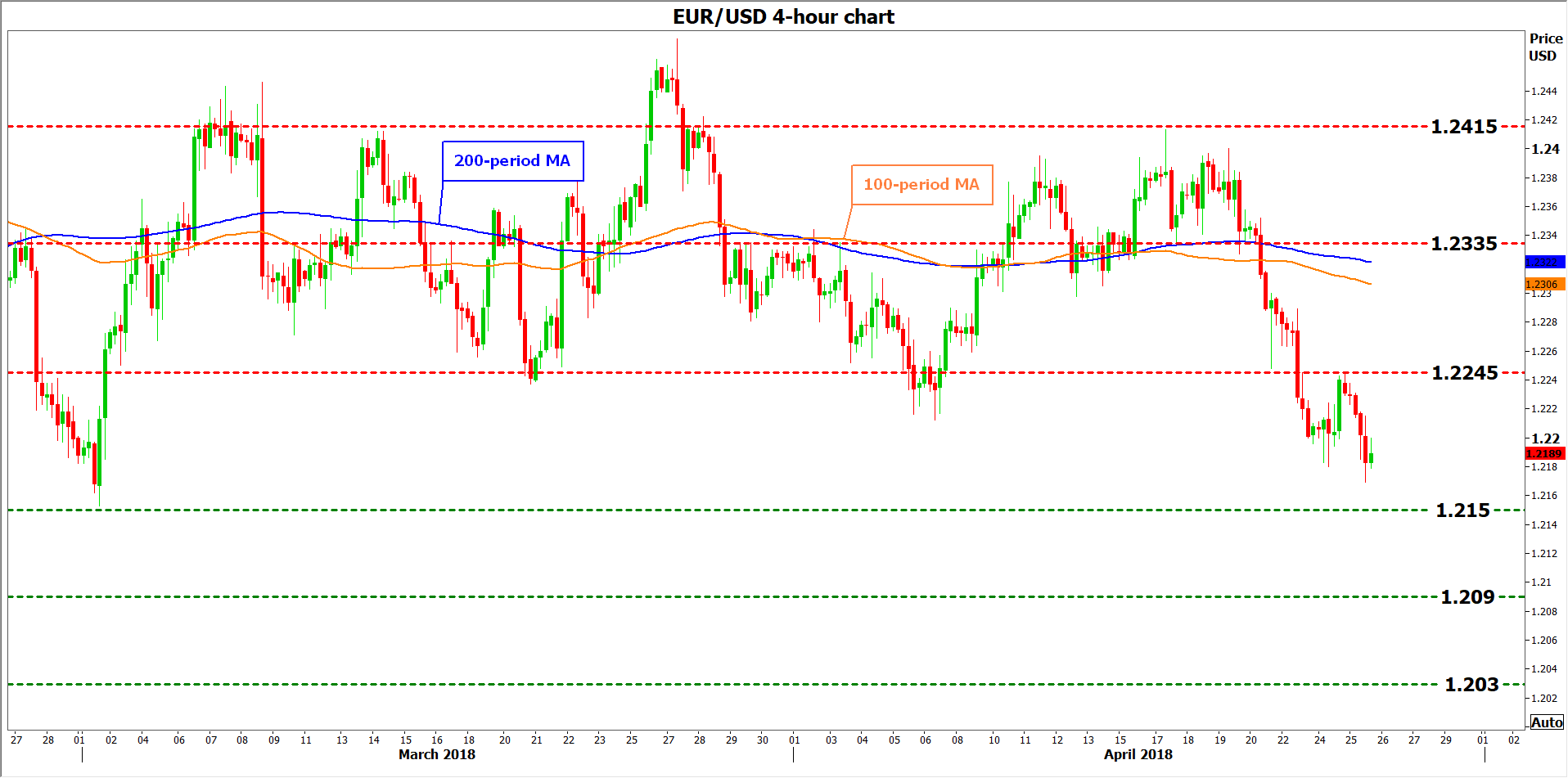

EURUSD – Bearish, Resumes Downside Pressure

EURUSD - The pair resumed its weakness on Wednesday leaving risk of more decline on the cards. On the upside, resistance comes in at 1.2200 level with a cut through here opening the door for more upside towards the 1.2250 level. Further up, resistance lies at the 1.2300 level where a break will expose the 1.2350 level. Conversely, support lies at the 1.2100 level where a violation will aim at the 1.2050 level. A break of here will aim at the 1.2000 level. Below here will open the door for more weakness towards the 1.19500. All in all, EURUSD faces further downside threats.

Gold Nearing Breakout

Most gold bulls have been holding on to long positions for months, if not years anticipating the next big breakout. It was almost one year ago when gold made a successful break above the six-year trendline resistance, extending from the $1921 high. But how long must we wait for a clear break above $1400?

What we already know

Gold attempted and failed to break above $1390-1400 in more than 6 occasions over the past five years. I have argued in favour of the fundamental case supporting further advances in gold in previous articles including; ‘Can Yields Stop Gold?’ and ‘Under The golden Hood’. The rationale remains valid.

The Technical case continues to be generally supported by a combination of multi-year inverted head and shoulder formation (currently we are alongside the neckline), double dosage of weekly golden crosses (100 week moving average crossing above the 200 week moving average and the 55-week moving average above the 100-week moving average) and 2 ½ years of uninterrupted higher lows.

Look for Sentiment Breakout

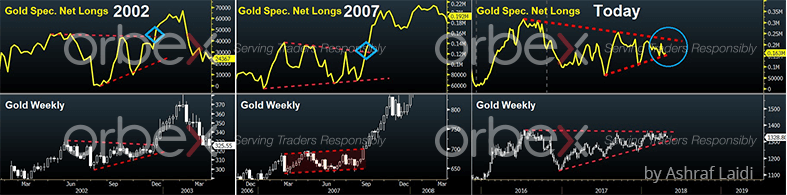

Looking at the commitments data of futures speculators at the Comex, net longs in gold can shed valuable light on future moves in the spot price of bullion. Specifically, triangle breakouts have proven effective (in the case of gold and EUR longs vs USD commitments) in signalling breakouts in the spot price. At times, the breakout in net longs occurred 3-4 weeks before in that of the spot price.

The charts below highlight two prominent cases when the breakout in gold speculative positioning offered a clearer signal than that shown in the spot price, as seen in December 2002 and September 2007. In both cases, the ascending price momentum served as a confirmation for the move in the futures market.

Today, the triangular wedge patterns are prominent in both of the net longs and the gold price. Specifically encouraging is that bullion is near 5-year highs while net speculative longs are well below the record high, suggesting there is more durable demand than speculative interest behind the gold rally.

Combining the structure of the ascending pattern in the spot price and ensuing neckline, $1520 remains a viable target for this year. Will the breakout in speculative interest trigger the signal? Stand by for the answer in late May – early June.

Eco Data 4/26/18

[php_everywhere instance="1"]

CHF and CAD showing some strength while USD dominates

USD is without a doubt the strongest one today as helped by another day of rally in yields. 10 year yield hit as high as 3.032, just shy of 2013 high, key resistance level, of 3.036. Up till now, it looks like TNX could close above 3.000 handle. But let's see.

D heatmap shows that GBP is so far very resilient today, staying above yesterday's low against USD and is trading as the second strongest. However, it's the strength of CHF and CAD in the current 4H bar that catches our attention.

On the one hand, CHF is helped as EUR/CHF is rejected by 1.2 again.

On the one hand, CHF is helped as EUR/CHF is rejected by 1.2 again.

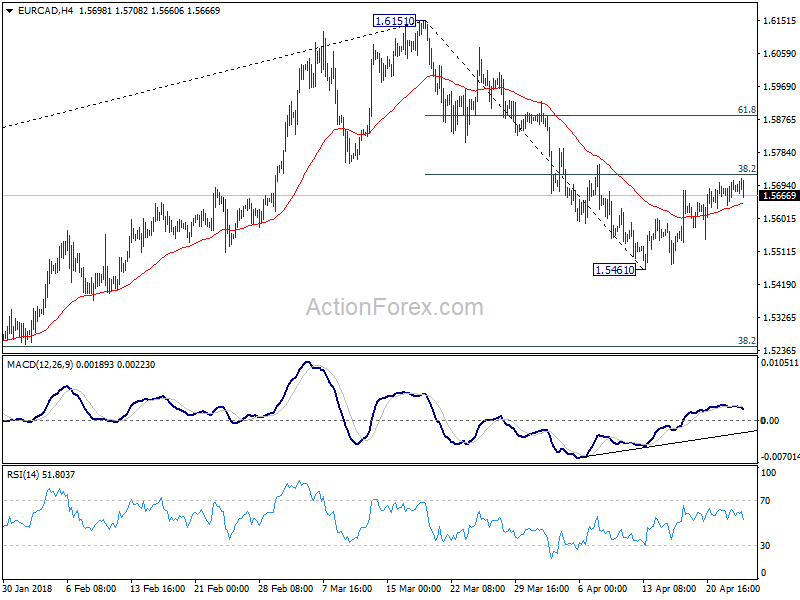

Meanwhile, CAD is helped by some cross buying. It's a bit early to say. But EUR/CAD could be starting to end (?) the corrective rebound from 1.5461, ahead of 38.2% retracement of 1.6151 to 1.5461 at 1.5724.

Meanwhile, CAD is helped by some cross buying. It's a bit early to say. But EUR/CAD could be starting to end (?) the corrective rebound from 1.5461, ahead of 38.2% retracement of 1.6151 to 1.5461 at 1.5724.

EUR/CAD's action bias chart is not giving any indication of that yet. We'll keep monitoring it too see if there will be red action bias bars in H and 6H chart ahead.

Dollar Punches Past 109 Yen as US Bond Yields Climb

The yen continues to lose ground against the robust US dollar. In the Wednesday session, USD/JPY is trading at 109.27, up 0.42% on the day. The pair has posted gains in 6 consecutive sessions, climbing 2.2% during that period. On the release front, Japanese All Industries Activity rebound with a gain of 0.4%, after a decline of 1.8% a month earlier. Still, this missed the estimate of 0.6%. There are no major US events on the schedule. Thursday will be much busier, with a host of key indicators. The US releases durable goods orders and unemployment claims. Japan will publish retail sales and CPI, and the BoJ will issue a policy statement.

The US dollar continues to climb against its rivals, buoyed by rising yields on US bonds, which have hit 4-year highs. On Wednesday, 10-year US Treasury notes have risen to 3.015%, and 2-year bonds have increased to 2.504 percent. With inflation appearing to be on the rise, there are stronger expectations that the Federal Reserve will raise rates four times in 2018, which is good news for the US dollar. With oil pushing above $70 a barrel, there are concerns that inflation will rise, which has pushed bond prices lower and yields upwards. The US currency has also benefited from a reduction in geopolitical risk, with an easing of tensions between North and South Korea, and a lull in the conflict in Syria.

The Japanese economy continues to expand, but inflation has lagged behind growth and remains well below the Bank of Japan’s target of around 2 percent. The markets have been speculating that stronger economic conditions might cause the BoJ to re-examine its ultra-accommodative monetary policy. However, on Monday, BoJ Governor Haruhiko Kuroda poured cold water over such sentiment, stating that in order to reach its inflation target, “the Bank of Japan must continue very strong accommodative monetary policy for some time”. The BoJ will issue an inflation forecast on Friday, with the bank expected to reiterate that the inflation target will be reached in fiscal year 2019. Kuroda’s dovish statement can be seen as an attempt to curb volatility in the yen following the release of the inflation forecast.

ECB Meeting: Staying “Cautious” for Now?

The European Central Bank (ECB) will announce its policy decision on Thursday, at 1145 GMT. No change in either policy or guidance is expected, so price action in the euro will likely be dictated by the signals from President Draghi and other policymakers at the subsequent press conference, at 1230 GMT. Considering the softness in recent economic data, worries around protectionism and a firm euro, the balance of risks seems to be tilted towards a cautious tone by Draghi and Co.

At its latest meeting in March, the ECB took another small step towards normalizing policy, by removing from its forward guidance the so-called QE easing bias, the commitment that it stood ready to increase the size and/or duration of its asset purchases if the outlook became less favorable. Although President Draghi downplayed the importance of that move at the subsequent press conference, triggering a sharp drop in the euro, the removal of this dovish sentence was seen as paving the way for the Bank to end its QE program altogether later this year.

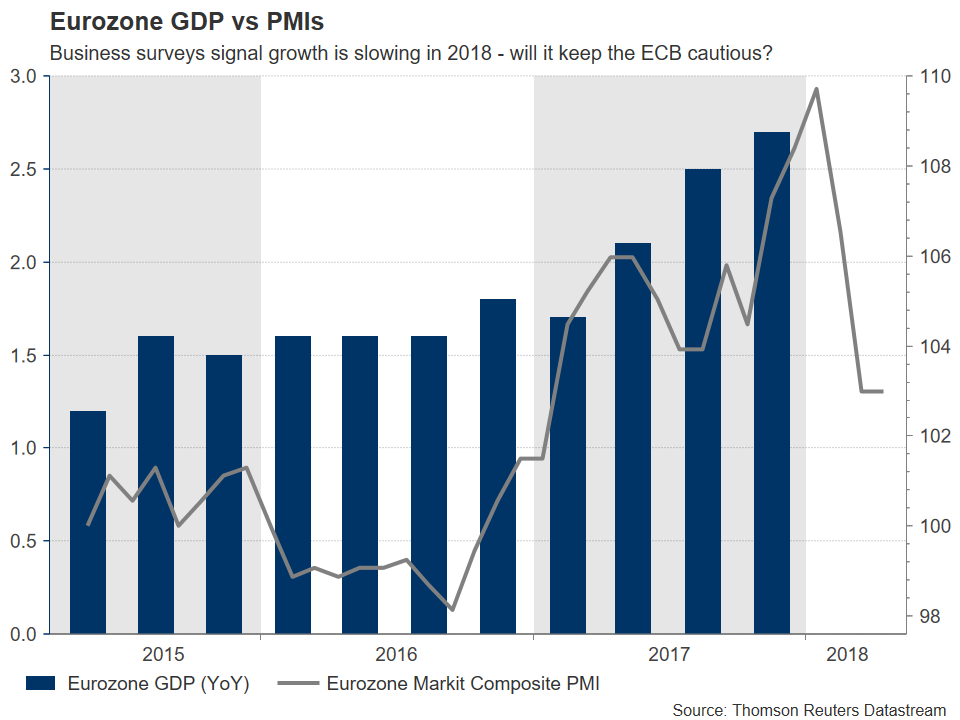

Alas, developments since then have been discouraging overall. In terms of economic data, inflation remains largely subdued, while economic growth appears to be slowing. The bloc’s core CPI rate has remained stuck at 1.0% since January, and while GDP data for Q1 have yet to be released, business surveys such as the PMIs suggest the economy is losing momentum, presenting downside risks to the ECB’s optimistic growth forecasts.

Moreover, the ECB appeared quite vigilant of global trade risks at its last meeting. The minutes showed concerns that protectionist measures could hinder growth, and that the risk of a full-blown trade conflict had risen. Considering that the latest US-China tariffs had not even been announced at that time, the ECB may view the risk of more trade frictions as having increased further, providing another reason to tread cautiously. Finally, the “strong” euro is likely to stay high on the Bank’s list of worries. While the currency traded mostly sideways this year, the Bank will likely remain watchful of any negative effects from the euro’s past appreciation, and will probably be keen to avoid fueling any further gains in the exchange rate.

All things considered, the Bank appears to have more incentives to strike a cautious tone, for now at least. President Draghi could adopt a conservative “wait-and-see” approach regarding further steps towards normalization, providing policymakers some time to monitor whether the latest economic slowdown is temporary, and how trade risks will evolve.

In case the ECB’s stance is seen as dovish overall, the euro could edge lower. Looking at euro/dollar, immediate support to declines could be found near the March 1 low of 1.2150, with steeper declines likely to bring the 1.2090 handle into play, the high of January 4. Further down, buy orders may be found near 1.2030, the September 20 peak.

On the other hand, if the Bank dismisses the recent economic slowdown as being owed to transitory factors, or if it downplays trade risks, the euro may soar. Resistance in euro/dollar may come around 1.2245, a level defined by the high of April 24. If the bulls overcome that hurdle, then sell orders may be found near 1.2335, the inside swing low of April 17, with even further advances likely to stall at 1.2415, the April 17 top.

In the big picture, even if the ECB does err on the side of caution at this meeting, that would still leave intact the broader narrative that the days of QE are drawing to an end. Policymakers still look set to begin scaling back their asset purchase program in the autumn, with some signaling of that likely to come in the summer meetings. For this narrative to be derailed, it would probably require a much sharper deterioration in economic data than what we have seen thus far, or for downside risks such as a trade war to materialize, both of which appear unlikely at this juncture.

Sunset Market Commentary

Markets

There were no important data in the EMU and the US today. Still, the test of key US yield levels continues and this move remains important for other markets (including equities and FX). The US 2-year yield is trying to clear the 2.5% hurdle. The US 10-y yield is holding north of 3.0%. The 3.05% 2014 top is within reach. The 30-y yield (3.19%) is also closing in on key 3.20/3.25% resistance. Markets have become more sensitive to potential upside inflation risks. The recent rise in oil prices was an important catalyst (even as prices eased slightly yesterday and today). At the same time, markets are preparing for a next batch of important US eco data starting with the Q1 US GDP release on Friday. Combined with next week’s US ISM’s, the payrolls and the statement of the May 2 Fed meeting, markets should have a clearer view on the Fed’s intentions for the June meeting (and maybe even for later this year) at the end of next week. The US yields are abound 1 bp higher currently. German bunds again outperform US Treasuries with yields rising less than 0.5 bp. European bond investors are cautious to join the repositioning in US yields ahead of tomorrow’s ECB policy meeting/press conference. Intra-EMU yield spreads versus Germany are little changed. Remarkable given the rise in core yields.

The same themes that drove FX trading yesterday are still at work today. Dollar strength prevails as markets ponder the consequences of US yields testing/breaking key resistance levels. In the recent past, interest rate differentials often played only a limited role as a driver for USD trading. However, to the extent that markets anticipate that upcoming US data might reinforce the case of three rather than two additional Fed rate hikes this year, the ever growing interest rate differential finally comes to support the dollar. At the same time, markets expect the ECB to maintain a soft tone at the April policy meeting. Tomorrow, we will know whether this assessment is correct. EUR/USD is trading in the 1.2180 area. The 1.2155 support is coming ever closer. The yen remains weak against the overall strong dollar. Contrary to what was the case yesterday, the rally in EUR/JPY shows tentative signs of fatigue. This might be due to euro softness. Or is it an indication that at least some safe have flows might return to the yen if global sentiment on risk were to deteriorate further?.

There were also no important eco data in the UK. Sterling was mostly driven by global market trends. Cable kept downward intraday bias as the dollar remained well bid across the board. EUR/GBP lost a few tick on a daily basis. EUR/USD declining below 1.22 probably caused some modest spill-over effects on EUR/GBP, too. The pair trades currently in the 0.8740 area. Cable is changing hands around 1.3935/40. In the UK, the debate whether the UK/UK government should retain the option of staying in a customs union with the EU continues. For now it is far from clear to what side this domino will fall. The day-to-day gyrations in this debate have little impact on sterling.

News Headlines

US equity markets find themselves between a rock and a hard place. US corporate results mostly came out better than expected. Today positive surprises of Twitter en Boeing did catch the eye. At the same time investors are worried about the impact of higher yields. US equity markets open little changed, but soon came again under pressure. Most European indices are losing between 1.0% and 1.75%.

German economy Minister Altmaier indicated that the German government cut the 2018 growth forecast from 2.4% to 2.3%. He also expects no significant contribution from foreign trade to growth. 2019 growth was set at 2.1%. The Minister said that the economic upturn is continuing. He is concerned about international trade developments but hopes that a trade war can be avoided.

Dollar Surges as 10 Year Yield is Having Another Take on 3%

Dollar jumps again today as 10 year yield is having another attempt at 3% handle today. The greenback is trading above yesterday's high against all major currencies except Sterling. And for now, Yen is actually not the weakest one. Instead, commodity currencies and Swiss Franc are the worst performers. EUR/CHF had another attempt on 1.2 handle earlier today, but thanks to Euro's weakness, this historical level is still intact. Developments in yield will be the main driver in the markets with a near empty economic calendar in the US session.

German Economic Ministry revised growth forecast down to 2.3% in 2018

The German Economy Ministry lowered growth forecast for this year today. For 2018, GDP is now projected to grow 2.3%, downgraded from January forecast of 2.4%. For 2019, growth is projected to be at 2.1%.

Economy Minister Peter Altmaier said that the German economy s in a "robust state", "remains buoyant and the upturn is continuing." Also, while recent economic data have been disappointing, Altmaier said they ""are in no way pointing to a downturn." He added that "any growth in the region of 2 percent or above is exceptionally good growth, if you compare it with the history of the last 10-15 years in Germany."

ECB Mersch noted increasing confidence, Vasiliauskas said it's time to transit from asset purchase

Articles by ECB Executive Board member Yves Mersch and Governing Council member Vitas Vasiliauskas were published Wednesday by Eurofi today. While Mersch's article was submitted back on March 21 and Vasiliauskas on March 15, they're worth a quick read.

Mersch's article was on the topic of "Monetary policy in the euro area: solid expansion with timid price pressure". He noted that "confidence has recently risen and convergence is being confirmed - partly because the temporary decline in the inflation rate has been weaker than our internal calculations had predicted." And still, emphasized that patience and persistence with respect to our monetary policy is required."

Vasiliauskas' article was on the topic of "The time is approaching to seriously consider a smooth transition from the APP". He noted that "we have witnessed the strengthening of broad-based growth and steadily declining unemployment, providing conditions for inflation convergence to our objective." And, "this has increased my confidence that it is time to transition from the asset purchase program". However, Vasiliauskas also emphasized that "the closure of the program should not be abrupt."

ECB meeting is not totally a non-event

Talking about ECB, there is little chance of any change in monetary policy nor language tomorrow. Despite expectations that the ECB would only announce adjustments on QE and interest rate in June the earliest, the upcoming meeting is not a non-event. Since the March meeting, Eurozone's economic data have surprised to the downside. It would be of great interest to see the policymakers' interpretation of the situation. All in all, we expect the members to view the first quarter slowdown as driven by temporary factors, e. g.: weather, which do not affect the monetary stance. More in ECB Preview: Caution over Recent Slowdown Won't Affect QE Schedule

And some suggested readings on ECB:

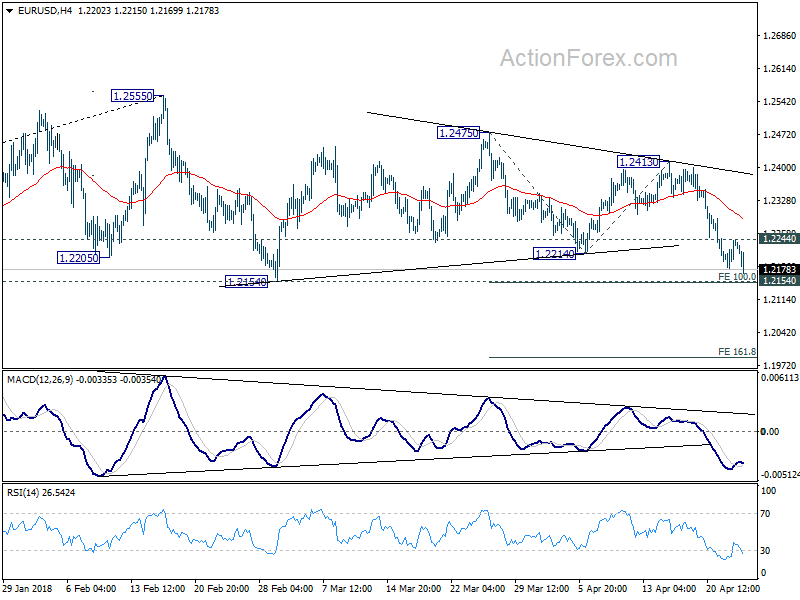

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2194; (P) 1.2220 (R1) 1.2258; More....

EUR/USD's fall resumes after brief consolidation and intraday bias is turned to the downside for 1.2154 key support. Decisive break there should confirm the bearish case of medium term reversal. And EUR/USD should then target 161.8% projection of 1.2475 to 1.2214 from 1.2413 at 1.1991. On the upside, though, break of 1.2244 minor resistance will indicate short term bottoming. And even though we'd still expect deeper decline in that case, lengthier consolidation would be seen first.

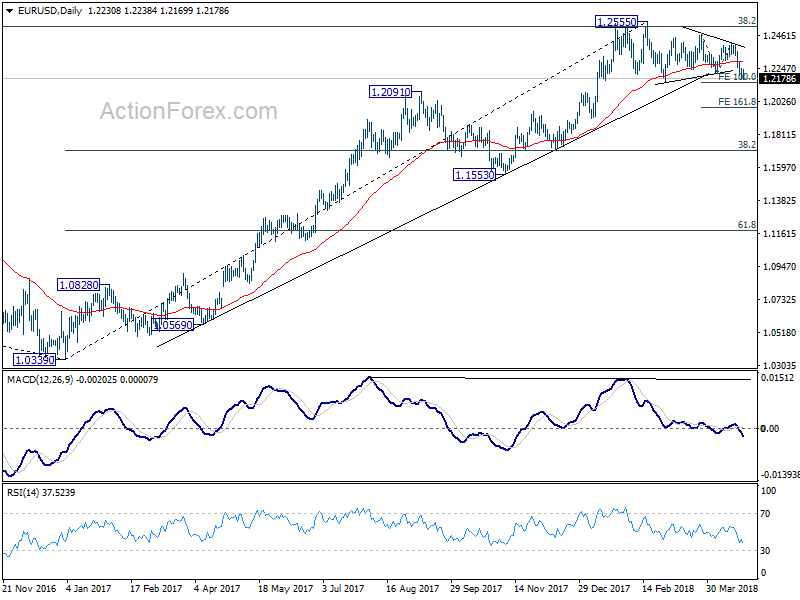

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Firm break of 1.2154 support will confirm rejection by this fibonacci level. And in that case, a medium term top is at least formed at 1.2555. EUR/USD should then head back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. We'll look at the structure and momentum of such decline before decision if it's an impulsive or corrective move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 4:30 | JPY | All Industry Activity Index M/M Feb | 0.40% | 0.50% | -1.80% | -1.10% |

| 14:30 | USD | Crude Oil Inventories | -1.1M |