Sample Category Title

ECB Rate Decsion Expected On Thursday

A report on German consumer confidence courtesy of GfK will kick off the European session at 07:00 GMT. The consumer confidence index for the month of May is expected to come in at 10.8 after hitting 10.9 the previous month.

Reports on Spanish unemployment and British mortgage approvals will also make the rounds on Thursday.

The ECB decision is scheduled for 11:45 GMT. Investors can expect the main interest rate to be left at zero and the deposit rate at -0.4%.

Shifting gears to North America, the US government will report on initial jobless claims at 12:30 GMT. The number of Americans filing for first-time unemployment benefits is projected to fall by 2,000 to a seasonally adjusted 230,000 in the week ended 20 April.

The Department of Commerce is scheduled to report on durable goods orders and the overall trade balance at 12:30 GMT. Orders for manufactured goods meant to last three years or more is expected to rise 1.6% in March after surging 3.1% the month before. Meanwhile, Washington’s trade deficit with the rest of the world is forecast to slip to $74.8 billion in March from $75.35 billion in February.

The Federal Reserve Bank of Kansas is scheduled to report its monthly manufacturing survey at 15:00 GMT. An expected reading of +17 for April will undershoot the March tally of +20.

EUR/USD

A sliding euro broke below 1.2200 US on Wednesday for the first time since early March. EUR/USD is currently hovering around 1.2170, with immediate support located at 1.2150. The common currency could face an active trading session on Thursday as the ECB votes on monetary policy.

GBP/USD

Cable continues to struggle in the face of a rising US dollar. GBP/USD attempted a shallow recovery on Wednesday before swinging back down to the low 1.3900 region. The pair was last seen trading at 1.3936. Rising US yields could determine the short-term outlook for cable, which has given back sizable gains over the past week.

USD/JPY

The US dollar continues to surge against its Japanese counterpart, with prices climbing above 109.00 for the first time since February. At the time of writing, USD/JPY was trading at 109.41, where it was little changed compared with the previous close. The pair is looking to break out of a defined trading range between 105-110. However, that could depend on the Bank of Japan’s rhetoric on Friday when it delivers the next interest rate verdict.

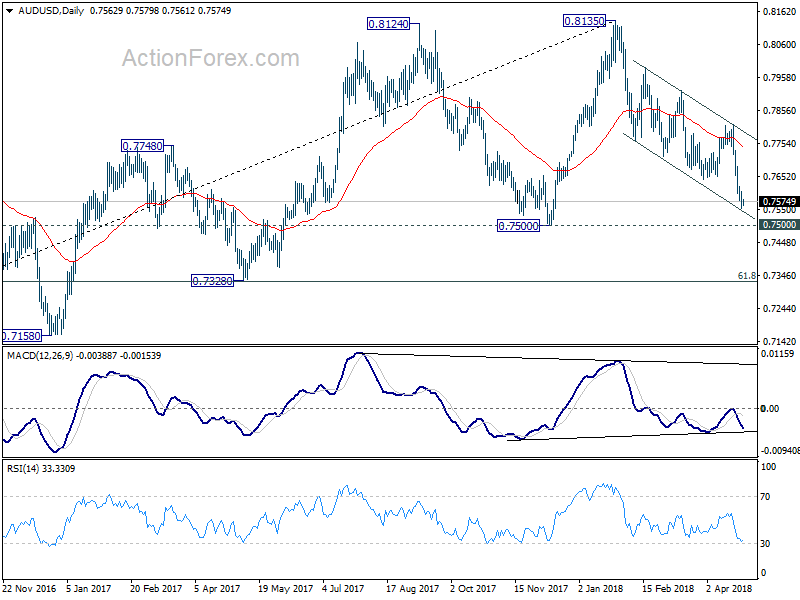

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7542; (P) 0.7573; (R1) 0.7596; More...

With 0.7620 minor resistance intact, intraday bias in AUD/USD remains on the downside for 0.7500 key support level. Decisive break there will indicate medium term reversal and target 0.7328 support next. On the upside, above 0.7620 minor resistance will turn intraday bias neutral and bring consolidations. But recovery should be limited below 0.7812 resistance to bring fall resumption.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term..

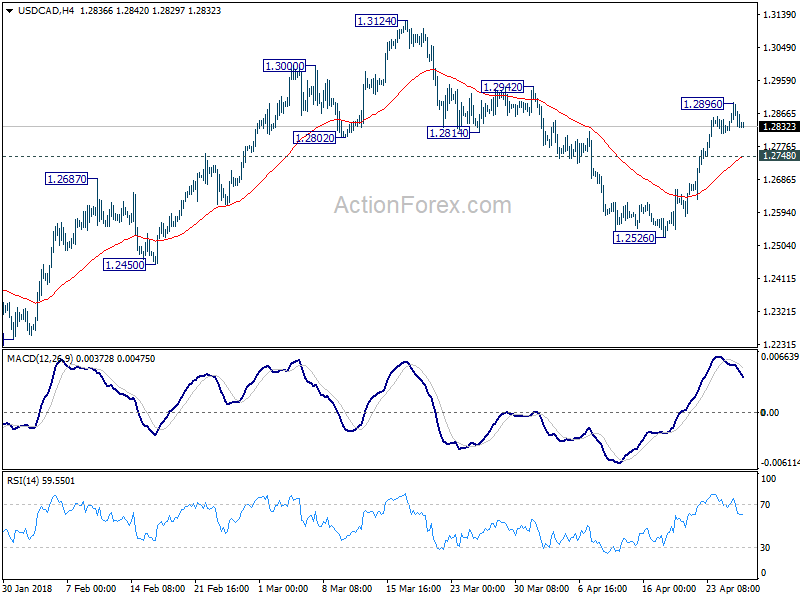

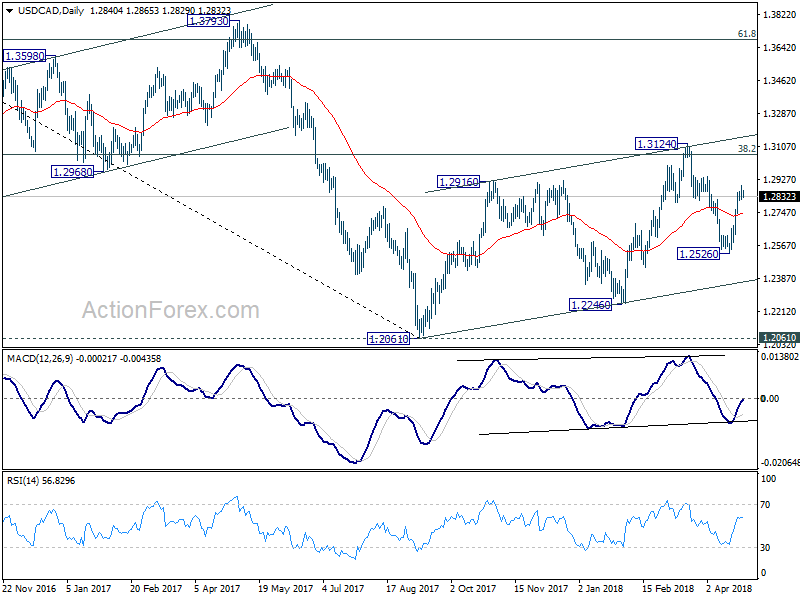

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2811; (P) 1.2854; (R1) 1.2889; More....

A temporary top is in place at 1.2896 with 4 hour MACD staying below signal line. Intraday bias in USD/CAD is turned neutral first. Downside of retreat should be contained by 1.2748 minor support to bring another rise. Above 1.2896 will turn bias back to the upside for 1.3124 resistance next. However, firm break of 1.2748 will turn focus back to 1.2526 support instead.

In the bigger picture, current development suggests that rebound from 1.2061 has not completed yet. Focus is back on 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Sustained trading above there will confirm medium term bullish reversal. That is, down trend from 1.4689 has completed at 1.2061 already. In that case, next target will be 61.8% retracement at 1.3685.

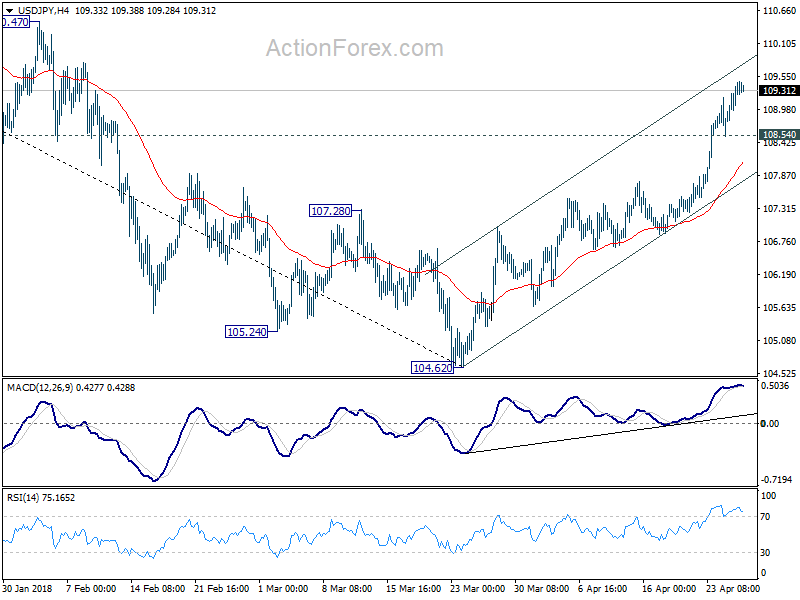

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.97; (P) 109.21; (R1) 109.66; More...

With 108.54 minor support intact, intraday bias in USD/JPY remains on the upside. Rise from 104.62 is in progress and should target 61.8% retracement of 114.73 to 104.62 at 108.48 9 110.86 next. On the downside, below 108.54 minor support will turn bias neutral and bring consolidation first, before staging another rise.

In the bigger picture, break of 108.12 support turned resistance now suggests that corrective fall from 118.65 (2016 high) has completed with three waves down to 104.62. And, rise from 98.97 (2016 low) could be resuming. Focus is back on 114.73 resistance and break there will pave the way to 118.65 and above. This will now be the preferred case as long as USD/JPY stays above 55 day EMA (now at 107.47).

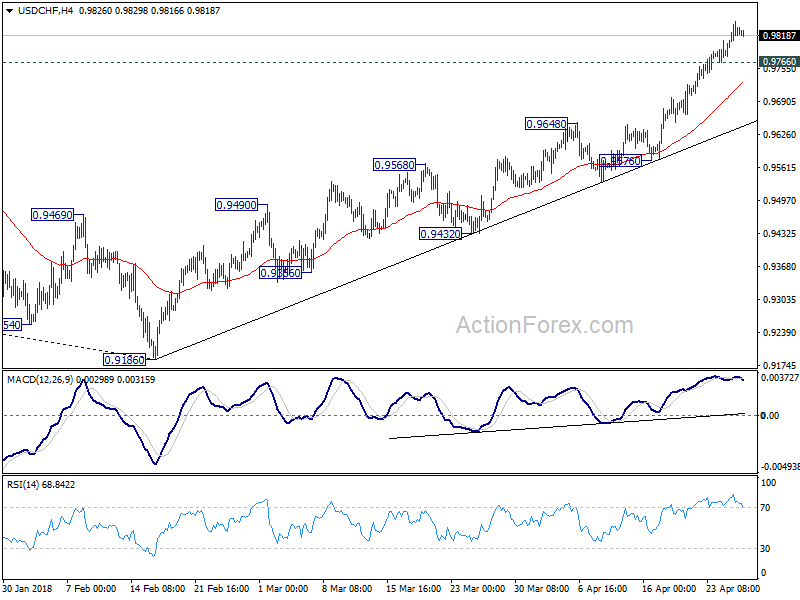

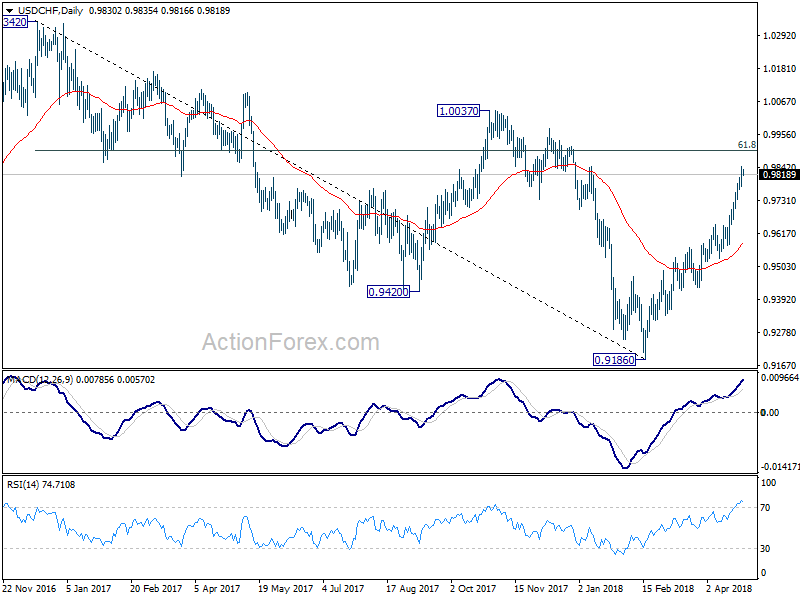

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9792; (P) 0.9819; (R1) 0.9859; More...

USD/CHF is losing some upside momentum as seen in 4 hour MACD. But intraday bias remains on the upside with 0.9766 minor support intact. Current rise from 0.9186 is still in progress for 0.9900 fibonacci level first. Break will target 1.0037 resistance next. On the downside, below 0.9766 minor support will turn bias neutral and bring consolidations. But outlook will stay bullish as long as 0.9576 support holds.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. The break of 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626 suggests that it's likely completed at 0.9186 already. Further rally would be seen back to 61.8% retracement at 0.9900 and above. Sustained break there would pave the way to retest 1.0342 key resistance next. This will now be the preferred case as long as 0.9576 support holds.

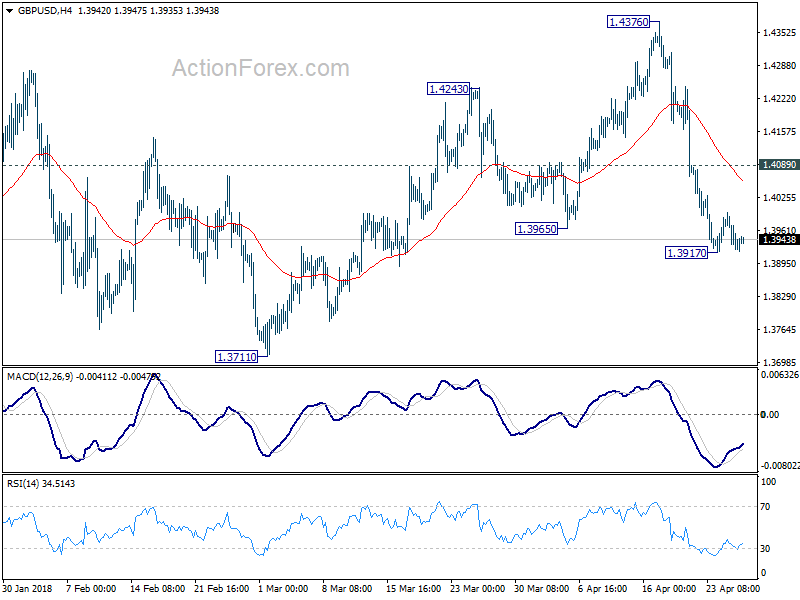

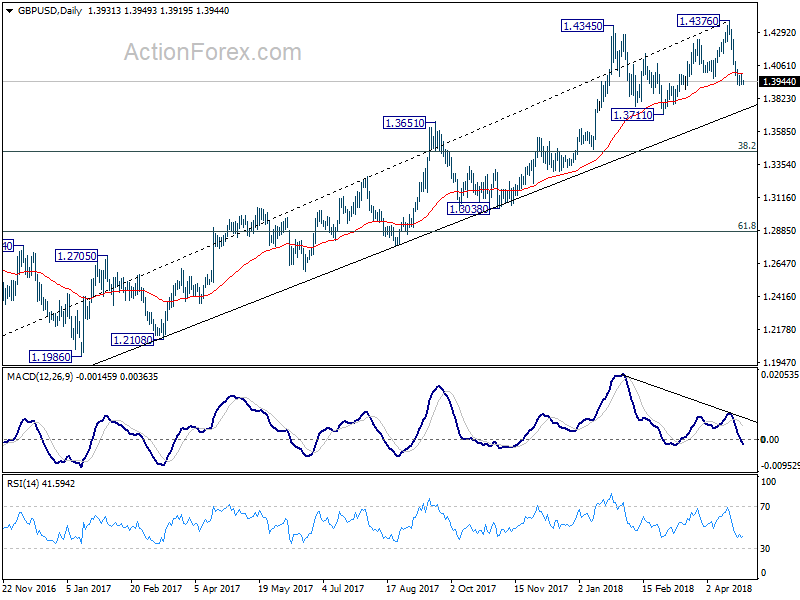

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3899; (P) 1.3965; (R1) 1.4004; More...

Intraday bias in GBP/USD remains neutral as consolidation from 1.3917 temporary low is still unfolding. Another recovery cannot be ruled out. But upside should be limited by 1.4089 minor resistance to bring fall resumption. Below 1.3917 will target 1.3711 key support next. However, firm break of 1.4089 will turn focus back to 1.4376 high instead.

In the bigger picture, bearish divergence condition in daily MACD is raising the chance of medium term reversal. Also, note that GBP/USD has just failed to sustain above 55 month EMA (now at 1.4257). Focus is back on 1.3711 support. Firm break there will confirm medium term reversal and target 38.2% retracement of 1.1936 (2016 low) to 1.4376 at 1.3448 first. Break will target 61.8% retracement at 1.2874 and below. For now, sustained break of 55 month EMA is needed to confirm medium term upside momentum. Otherwise, we won't turn bullish even in case of strong rebound.

Markets Focused On ECB Interest Rate Decision, No Change Expected

At 11:45 GMT, the ECB Deposit Rate Decision will be announced and is expected to remain unchanged at -0.4%. The ECB Interest Rate Decision will also be released at this time and is expected to be unchanged at 0%. This data could see volatility increase in EUR markets on the approach to the ECB Press Conference and Monetary Policy Statement at 12:30. Comments from ECB President Mario Draghi will be assessed for hints on future monetary policy, with hawkish comments adding strength to the Euro. However, any change in guidance is not expected to occur until June.

At 12:30 GMT, US Durable Goods Orders Ex-Transportation (Mar) is expected to come in at 0.5% from 1.0% previously, which was revised down from 1.2%. Durable Goods Orders (Mar) is expected at 1.6% against 3.0% previously, which was revised down from 3.1%. This data series beat expectations last time out but revisions have lowered expectations somewhat. US Initial Jobless Claims (Apr 20) is expected to be 230K from 232K previously. Continuing Jobless Claims (Apr 13) is expected to be 1.850M from 1.863M previously. Jobless Claims data has beat expectations on the last three readings, but numbers have been decreasing from the 242K high three weeks ago. USD crosses may be moved by this data.

In Sweden It Is Time For The Riksbank’s Policy Announcement

Market movers today

The main focus today will be the ECB- and Riksbank meetings and overnight tonight these meetings will be followed by Bank of Japan.

In the case of ECB, we do not expect any announcements with regards to policy changes from the governing council at this meeting. However, as presented earlier today in our ECB preview, we have changed our call on the ECB's hiking path. We expect ECB to come with its first rate hike in December 2019, but with a 20bp size on the deposit rate hike instead of a 10bp hike in Q2 19. Recent data on inflation has disappointed compared to ECB projections, and the declining activity indicators should further lead the ECB to revise its GDP forecast downwards at the June meeting. Taken together, we believe the ECB is likely to postpone the first hike, as its current projections seem overly optimistic given recent developments.

In Sweden it is time for the Riksbank's policy announcement. In our minds, now is the time for the Riksbank to make another shift to the rate path by pushing hikes further out in the future, presumably to the first quarter of 2019.

Early Friday morning, the Bank of Japan (BOJ) will announce its policy decisions. We expect the BoJ to keep its 'QQE with yield curve control' policy unchanged, which is the first under the new leadership. With the arrival of two new deputy governors, we expect the board to have turned slightly more dovish. Considering how the economy has lost some momentum recently and inflation has still not really picked up, we see the probability of further easing as at least as likely as any tightening measures.

Selected market news

After the break of the pivotal 3% mark yesterday, the 10 year US government bond yield have taken a firm hold above 3% trading at 3.03% this morning. While we continue to hold the view that it is too early to call for a major fixed income sell-off given the business cycle outlook and still dovish central banks, the break of the 3% in the 10 year US yield has created room for higher US yields supporting the case for further widening of the 10 year government bond yield spread between the US and Germany, which is currently at the widest level since the inception of the European Monetary Union just below 240bp.

US equities ended the day slightly higher yesterday and the S&P500 index gained 0.18% after swinging between gains and losses during the US session as investors continue to consider global equity markets' ability to cope with higher interest rates. Asian markets trade mixed this morning with Japanese equity indices in the green while Chinese markets trade lower.

Yesterday's NOK session was dominated by news that the opposition had voted against the March change of the Norges Bank's inflation mandate from 2.5% to 2.0%. However, shortly after the news hit the wire, the Christian Democratic Party's spokesperson stated that in the end it is the government that decides. In other words, we should not expect a re-change of the inflation mandate back to 2.5%. The noise did however contribute to weakening the NOK in yesterday's session.

Markets Consolidate This Morning After Recent Volatility

Markets were choppy yesterday as 10-year US notes went above 3%, but after creating new lows for the week, stock markets rallied with much of this move extending into the Asian session. The USD strengthened further, with USDJPY reaching the key 109.500 level and GBPUSD consolidated under 1.40000. The EUR settled into a tighter range as we await the ECB Rate Decision and Press Conference later today. This meeting is expected to be a preamble to the serious business on future policy is done at the June meeting. Today’s meeting should largely address recent economic data weakness but the risk is that any comments will create a volatile move in the EUR.

Swiss ZEW Survey – Expectations (Apr) were 7.2 against a prior reading of 16.7. This data has been weakening since a reading of 52.0 was recorded in December 2017. A reading under 16.7 had not been recorded since December 2016. This illustrates the drop in Economic expectations in Switzerland. GBPCHF fell from 1.37100 to 1.36924 after the data release.

US EIA Crude Oil Stocks (Apr) data was released, coming in with a build of 2.170M against an expectation for a draw of -2.043M barrels, from a previous reading of -1.071M barrels. Oil prices sank on Tuesday, from a high of $69.30 to $67.49, as the private inventories data suggested a surprise build of 1.099M against a consensus of -2.250M and the French and US Presidents discussed a new Iran deal. This build was borne out in this release and prices fell to the $67.05 support, where buyers stepped in and have carried the price back to $68.40. A drop under $67.00 may force downward pressure on prices, but, for now, it marks the bottom of the range up to $69.50.

Bank of Canada Governor Poloz testified along with Senior Deputy Governor Carolyn Wilkins before the Standing Senate Committee on Banking, Trade and Commerce, in Ottawa. They said that people needed to be prepared for higher interest rates and that they needed to get the timing right to counter inflation. The comment was also made that fiscal stimulus had helped avoid a lower path for rates. USDCAD fell during this event from 1.28657 to a low of 1.28308 as a result.

EURUSD is up 0.16% overnight, trading around 1.21796.

USDJPY is down -0.10% in early session trading at around 109.310.

GBPUSD is up 0.13% this morning, trading around 1.39456.

Gold is up 0.07% in early morning trading at around $1,323.99.

WTI is up 0.40% this morning, trading around $68.32.

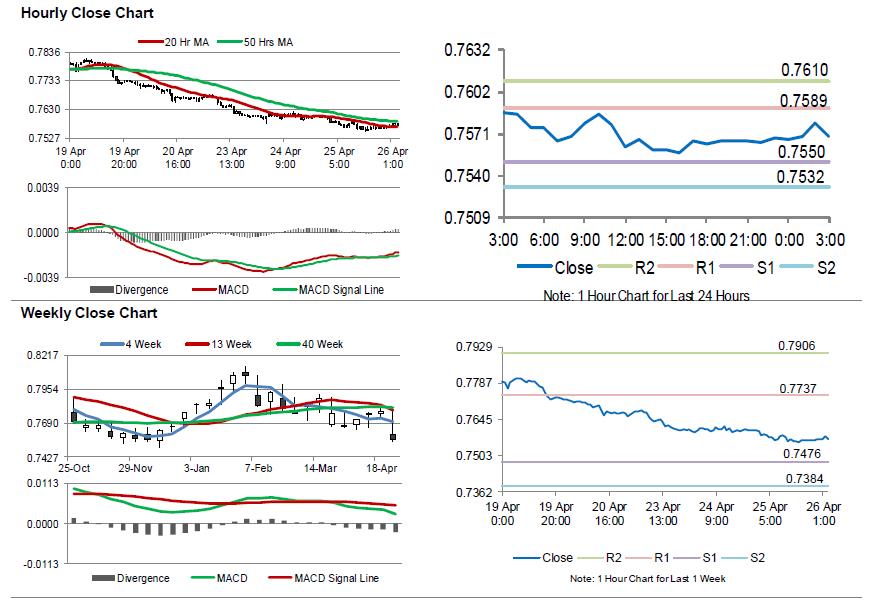

Aussie Trading A Tad Higher This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.46% against the USD and closed at 0.7568.

LME Copper prices declined 0.38% or $26.5/MT to $6960.5/MT. Aluminium prices rose 1.17% or $26.0/MT to $2248.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7569, with the AUD trading marginally higher against the USD from yesterday's close.

In economic news, Australia's export price index grew 4.9% QoQ in the first quarter of 2018, topping market expectations for a rise of 4.1%. In the prior quarter, the index had risen 2.8%. Moreover, the nation's import price index advanced more-than-anticipated by 2.1% on a quarterly basis in the first three months of 2018, compared to market consensus for a rise of 1.2%. In the prior quarter, the index had climbed 2.0%.

The pair is expected to find support at 0.755, and a fall through could take it to the next support level of 0.7532. The pair is expected to find its first resistance at 0.7589, and a rise through could take it to the next resistance level of 0.7610.

Going ahead, traders would focus on Australia's producer price index for Q1, due to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.