Sample Category Title

German Inflation, US Consumer Sentiment On The Agenda

A steady stream of economic data will flow through the financial markets on Friday, with headline reports from Europe and the United States. In particular, currency traders will be eyeing final inflation numbers from Germany and a closely-watched sentiment indicator from the United States.

The German data set will be released at 06:00 GMT. The final consumer price index (CPI) for March is expected to rise 1.6% year-over-year, based on the consensus forecast. Germany's harmonised index of consumer prices (HICP), which calculates inflation using a method consistent throughout the EU, likely rose 1.5%.

The Spanish government will also release its final inflation data set for March. Spain's HICP is forecast to rise 1.3% annually during the month.

At 09:00 GMT, the European Commission's statistical agency will report on the February trade balance. Brussels is expected to post a trade surplus of €20.2 billion in February, up from €19.9 billion the month before. Trade is a hotly contested topic in geopolitical circles after the Trump administration announced a tariff hit-list targeting commodities and Chinese goods.

Federal Reserve policymaker James Bullard kicks off the North American session with a speech scheduled for 13:00 GMT. Bullard serves as the President of the St. Louis Fed and is not currently a member of the Federal Open Market Committee (FOMC).

Later in the day, FOMC member Robert Kaplan will deliver a speech that could have important implications for monetary policy.

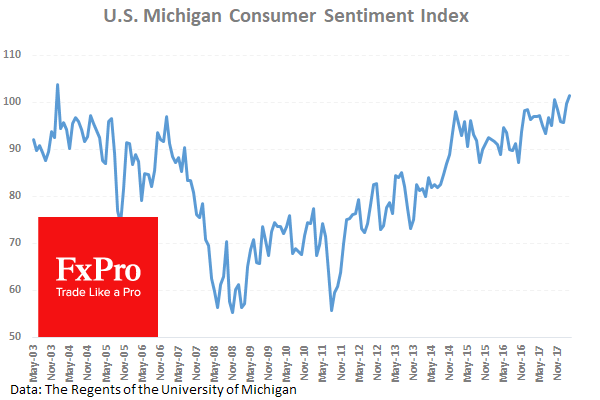

In terms of US economic data, the University of Michigan will release its monthly consumer sentiment index for April. The preliminary reading is likely to show a decline to 100.5 from 101.4 the previous month.

Meanwhile, energy traders will be keeping a close watch for the latest rig-count data courtesy of Baker Hughes Inc. The report is due for release at 17:00 GMT.

EUR/USD

Europe's common currency came under selling pressure on Thursday, with prices falling to a low of 1.2306. EUR/USD would later recover near 1.2330, although the short-term trend suggests further declines are afoot.

GBP/USD

Cable returned to positive territory on Thursday, with prices climbing back above 1.4200. GBP/USD was last seen trading at 1.4243, putting it on track for its highest settlement since early February. The pair faces immediate support around 1.4180. On the opposite side of the spectrum, the 1.4300 region could be the next major resistance.

USD/JPY

Declining risk aversion has undermined the Japanese yen recently, helping the USD/JPY exchange rate climb to one-and-a-half month highs. At the time of writing, the pair was trading at 107.35, where it was little changed from the previous close. Recent price trends suggest the pair could struggle to extend its rally past the 107.50 area.

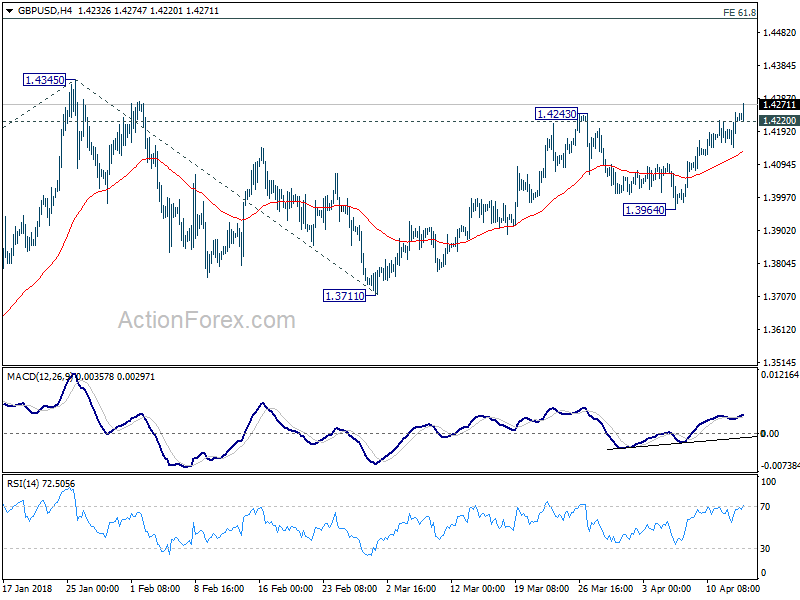

GBPUSD Strongly Bullish Above 1.4200

The British pound has moved to its highest trading level since February 2nd against the U.S dollar, as positive comments from Brexit secretary David Davis boosted sterling higher. The GBPUSD pair currently trades around the 1.4230 level, after earlier breaking above the March monthly price-high, at 1.4243. Traders now look towards the key 1.4200 level for direction, and a raft of top-tier macroeconomic data from the United States economy.

The GBPUSD pair is strongly bullish while trading above the 1.4200 level, key technical resistance is now found at the 1.4243 and 1.4278 levels.

Should the GBPUSD pair decline below the 1.4200 level, key intraday support is found at the 1.4146 and 1.4116 levels.

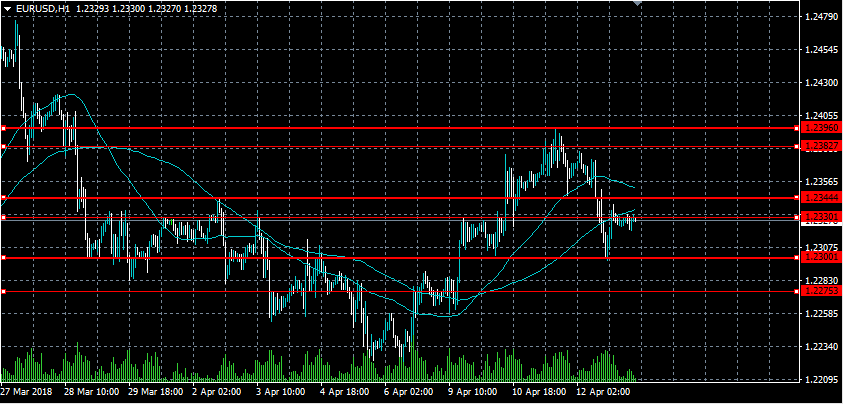

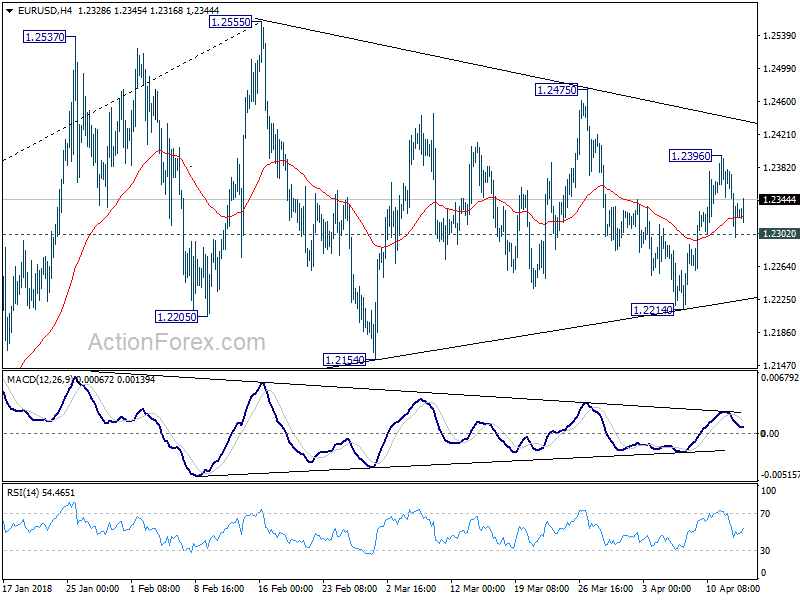

EURUSD Only Intraday Bullish Above 1.2333 Level

The euro has started recover upside momentum against the U.S dollar, after the single currency declined sharply lower, following the release of the ECB Meeting Minutes. The EURUSD pair currently trades around the 1.2330 level, after finding strong dip-buying demand from the key 1.2300 support level on Thursday. Traders now look towards CPI inflation figures from the German economy, with the 1.2333 level the pivotal intraday level to watch.

The EURUSD pair is only bullish while trading above the 1.2333 level, key intraday resistance is currently located at the 1.2382 and 1.2396 levels.

If the EURUSD pair trades below 1.2333 level, sellers may start to target the 1.2300 and 1.2275 support levels.

US Michigan Consumer Sentiment Index Close To Higher Than Pre-Crisis Levels

At 12:00 GMT, US Fed Boston President Rosengren is due to deliver the keynote speech on the economic outlook, at the Greater Boston Chamber’s Economic Outlook Breakfast. Comments made may result in movement in USD crosses.

At 13:00 GMT, the US Fed’s Bullard is due to make a scheduled speech on “Living Standards across US Cities” in a lecture at Washington University. Comments could cause moves in USD pairs.

At 14:00 GMT, US Michigan Consumer Sentiment Index (Apr) is expected to come in at 100.5 against a previous 101.4. The previous reading was a record high for the index and a slight slip back lower is expected this time around.

At 17:00 GMT, FOMC Member Kaplan is due to make a scheduled speech at an Odessa Chamber of Commerce Member Luncheon. Comments may affect USD pairs.

At 17:00 GMT, Baker Hughes US Oil Rig Counts is due to be released, with a headline number from last week of 808. This was the highest level reached in some time. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

AUD Helped By Stronger Than Expected Chinese Import Data

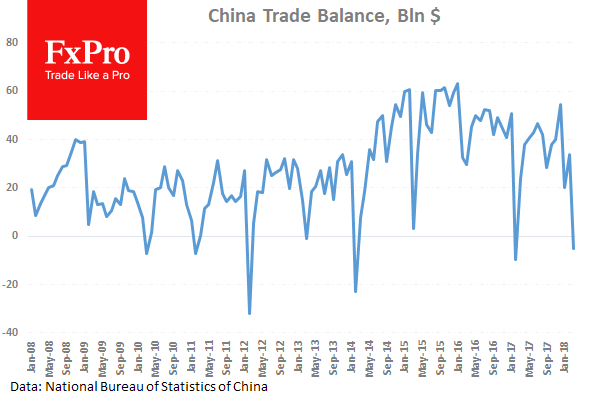

The AUD is the strongest currency today, as Chinese Imports (YoY) (Mar) came in at 14.4%, much stronger than the expected 10.0%, from a prior reading of 6.3%. This boosted the AUD, which was already higher due to positive risk sentiment, with AUDUSD up 0.28% to 0.77736 overnight. This pair was down at a low of 0.76516 on Monday.

The USDJPY has also moved higher, as the market sees a lack of any move against Syria as positive for risk and a relief rally is taking place. The pair is back to the high from a week ago, at 107.500, after dipping as low as 106.610 during the week. US WTI Oil rose on the back of the tensions in Syria and is currently trading around the $67.00 level, as traders saw a risk to supply developing from any potential conflict in the region. The USDTRY hit a high of 4.19287 during the week but is now trading at 4.11044. Stock markets have moved higher as tensions have eased, with the US500 setting a weekly high in yesterday’s session of 2674.30. Gold is down from a high of $1365.30 to $1338.91. Traders will watch for developments over the weekend and the scope and damage caused by any strike on Syria will be a main focus in the coming week.

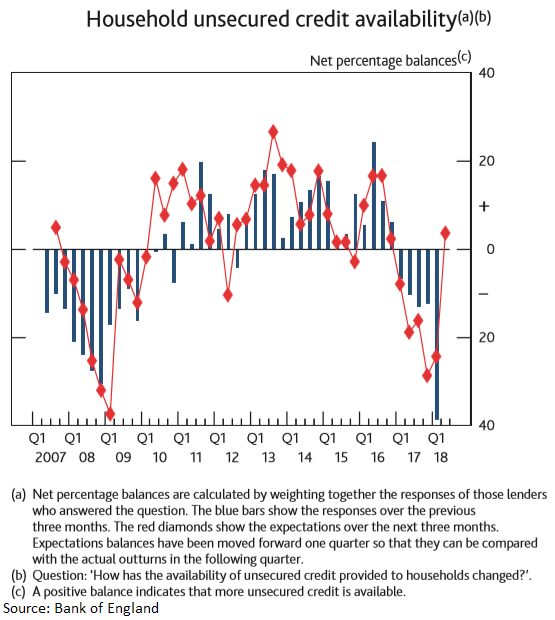

The BOE Credit Conditions Survey was published. This is a survey of lenders which asks respondents to rate the level of credit conditions, including secured and unsecured loans to households, small businesses, non- financial corporations and non- bank firms. The report showed a large drop in the availability of unsecured loans to consumers during Q1. This is the largest drop since records began. Lenders expect broadly unchanged availability over the next 3 months. They see a rebound in demand for mortgage lending for the next 3 months, with supply to remain steady. GBPUSD was down after the data from 1.41766 to 1.41446.

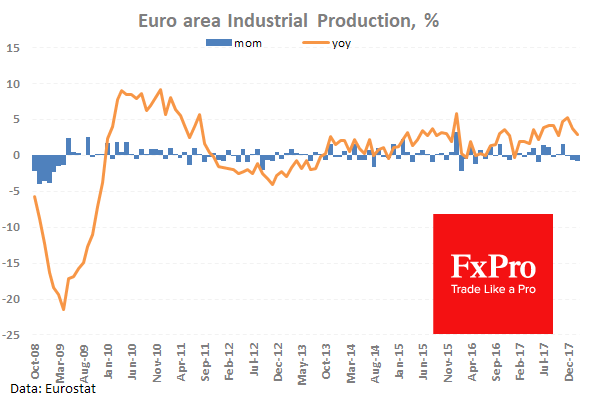

Eurozone Industrial Production w.d.a. (YoY) (Feb) was released, coming in at 2.9% v an expected 3.8%, from a prior of 2.7%. Industrial Production s.a. (MoM) (Feb) was -0.8% v an expected 0.1%, from -1.0% previously, which was revised down to -0.6%. This data was compiled during the cold snap that gripped the continent so there is still hope for a rebound in the coming months. EURUSD fell from 1.23458 to 1.23340 following the release of this data.

The ECB Monetary Policy Meeting Accounts were released. This is a detailed record of the ECB Governing Board’s most recent meeting, providing in-depth insights into the economic conditions that influenced their decision on where to set interest rates. The minutes showed the ECB broadly agreed that there is not enough evidence that inflation is sustained. The removal of easing bias should not be misunderstood and past EUR appreciation has not had a significant impact on demand. Despite the global upturn, underlying price pressures had remained subdued. Annual consumer price inflation in the OECD countries had ticked down slightly in January, to 2.2%, from 2.3% in December. The core inflation had remained steady, with inflation excluding food and energy standing at 1.8% in January. The ECB had widespread concerns over the risk of a trade conflict. EURUSD moved higher from a low of 1.23272 up to 1.23513 after this release.

The ECB’s Coeure delivered a scheduled speech from Paris. He said that the ECB’s current monetary policy stance was appropriate. Potential growth has not fallen by as much as we thought, it may imply that neutral rate of interest might be higher than is commonly estimated. EURGBP arrested its decline at 0.86908 and moved up to 0.86979 before turning lower again.

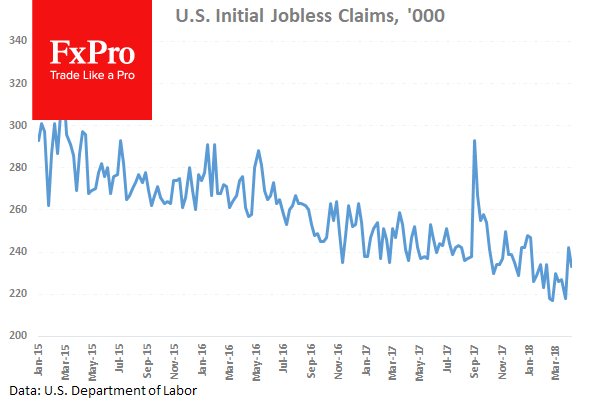

US Continuing Jobless Claims (Mar 30) came in at 1.871M v an expected 1.848M, against a previous 1.808M, which was revised up to 1.818M. Initial Jobless Claims (Apr 6) was 233K v an expected 230K, from 242K previously. The Initial Claims ticked up again after last week, with this week’s data staying below the high but exceeding expectations. The expected rise in continuing claims comes after a decade low number was recorded last week despite its revision higher.

FOMC Member Kaskari made a scheduled speech with the following comments: The US must avoid a trade war with China. He says he is sympathetic on the need to push China to open more markets to US businesses. It is very hard to game out where the US trade dispute with China will end. Immigration has benefitted the US tremendously. We have not seen wage growth nationally and there is likely still some slack in labour market. He also said he thinks the tax cuts and stimulus from government spending may help push inflation to 2%.

Business NZ PMI (Mar) was released and came in at 52.2, with a previous reading of 53.4, which was revised down to 53.3. This data has been declining since its December reading of 57.7. A reading above 50.0 indicates growth. NZD USD moved up from 0.73749 to 0.73794 following this data release.

EURUSD is up 0.03% overnight, trading around 1.23292.

USDJPY is up 0.16% in early session trading at around 107.482.

GBPUSD is up 0.03% this morning, trading around 1.42309.

Gold is up 0.31% in early morning trading at around $1,338.91.

WTI is down -0.34% this morning, trading around $66.88.

Risk Sentiment Improved Yesterday

Markets

Risk sentiment improved yesterday after US President Trump changed tack on the necessity of a quick missile attack against Syria, easing geopolitical concerns. Russia threatened earlier to shoot down all US missiles. European and US equity markets eventually gained 0.75% to 1.25% with US stocks outperforming. Improved risk sentiment weighed on global core bonds, even if the Bund sell-off was hampered by dovish interpreted ECB Minutes. US yields eventually ended 4 bps (2-yr) to 5.8 bps (5-yr) higher, the belly of the curve outperforming. The German yield curve steepened with yield changes ranging between -0.6 bps (2-yr) and +3.2 bps (30-yr). Asian risk sentiment is positive overnight with China underperforming. Disappointing Chinese trade data delivered the final blow, but the intraday slide was already ongoing. Developments on the geopolitical scene are mixed (China, Iran; see headlines below). We question whether stock markets will be able to add significantly to yesterday’s gains given the weekend ahead. Investors might prefer to build in somewhat more safety given uncertainty surrounding China and Syria. We continue arguing in favour of consolidation both in the Bund and the US Note future.

The combination of improved risk sentiment and a dovish ECB sent EUR/USD lower. The pair approached the 1.23 mark intraday, but eventually closed at 1.2327. USD/JPY mainly profited from the risk component of yesterday’s story line, rising from 106.79 to 107.33 after testing 107.48 resistance. Second tier eco data (weak EMU IP, softer US import prices and near consensus claims) had no impact. Today’s eco calendar only contains Michigan consumer confidence (April) and speeches by non-voting Fed-governors Rosengren, Bullard and Kaplan. Dollar sentiment improved for the better yesterday. The data and risk sentiment suggest no strong directional move today.

Sterling outperformed. The split between the dovish ECB and tightening BoE (May rate hike?!) was definitely at play. EUR/GBP dropped from 0.8724 to 0.8643, closing below 62% retracement from the EUR/GBP rally between April and August last year (0.8693) and below this year’s low (0.8668). It would be technically very relevant if the break is confirmed in this week’s close. GBP/USD rose from 1.4177 to 1.4247 and closes in on this year’s high (1.4345). The UK eco calendar is empty today, but EU officials suggested overnight that the EU and UK will next week for the first time look into the post-brexit trade relationship. The sessions will also cover the still unresolved issue of the Irish border and other parts of the divorce agreement that remain to be settled. It could break sterling’s momentum given that both parties’ official views remain wide apart.

News Headlines

US President Trump seems to want to extend his hardline strategy against China. First, he instructed senior officials to look at whether the US should rejoin the Trans-Pacific Partnership of which China isn’t part. Mr. Trump withdrew the US from the Obama-era TPP in one of his first acts in office. Next, he ordered the White House, according to officials, to ratchet up the pressure on China by focusing on new tariffs. At the same time, the US administration is crafting sharp prohibitions on Chinese investment in advanced US technology. (WSJ)

China's March exports unexpected fell 2.7% Y/Y in USD terms, the first drop since February last year, while imports grew 14.4% Y/Y, more than expected. The combination left the country with a rare $4.98 bn trade deficit for the month, the first since February 2017. (Reuters)

US and European officials said they’ve made progress on revisions to the Iran nuclear accord to address ballistic missiles and sunset provisions, raising optimism among American allies that President Trump can be persuaded not to scrap the deal. (BB)

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2290; (P) 1.2334 (R1) 1.2370; More....

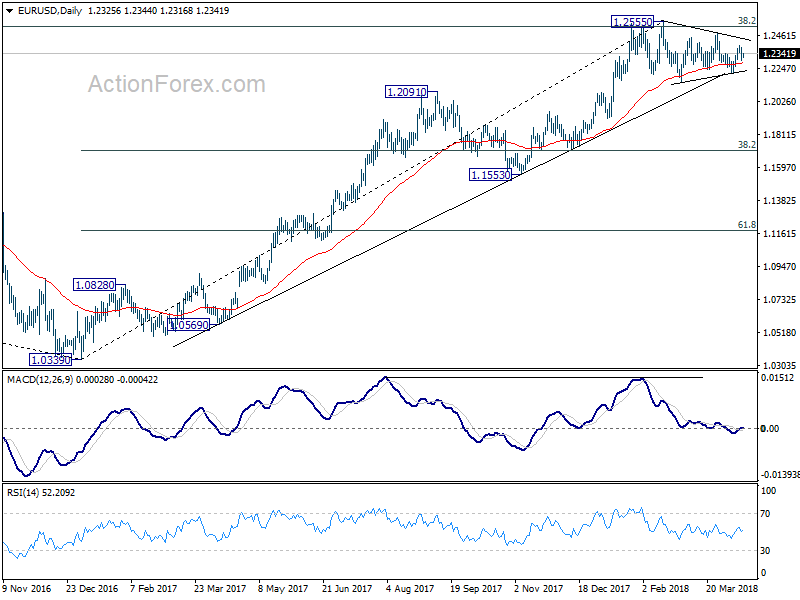

Intraday bias in EUR/USD remains neutral as this point, as it drew support from 1.2302 and recovered. On the upside, above 1.2396 will extend the rise from 1.2214 to 1.2475 and then 1.2555. 1.2516/55 is the key resistance zone to determine larger outlook. On the downside, below 1.2302 will turn bias to the downside for 1.2214 support first. And firm break there will revive the case of rejection by 1.2516 key fibonacci level and turn outlook bearish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

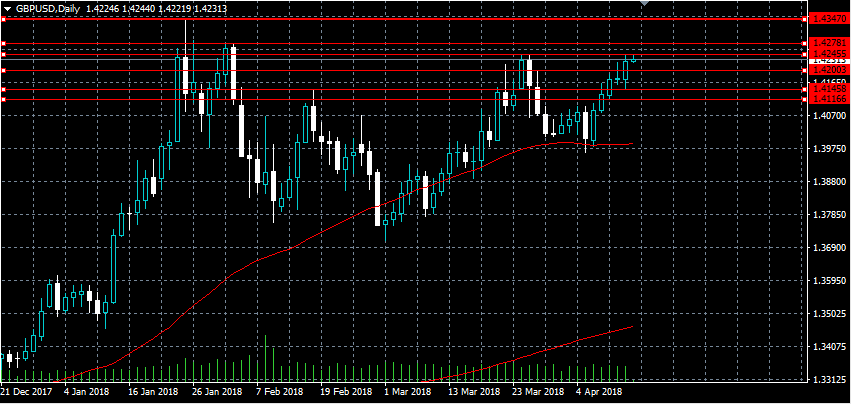

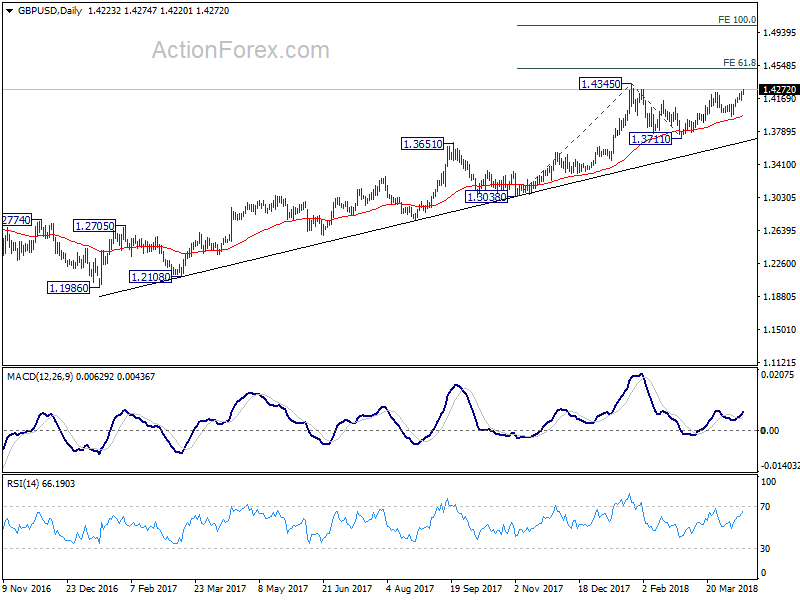

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4165; (P) 1.4206; (R1) 1.4266; More....

GBP/USD's rally resume after brief consolidation an reaches as high as 1.4274 so far. Intraday bias is back on the upside for 1.4345 high next. Firm break there will resume medium term rally and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, below 1.4220 minor support will turn intraday bias neutral again. But retreat should be contained well above 1.3964 support to bring another rally.

In the bigger picture, as long as 1.3651 resistance turned support holds, medium term outlook in GBP/USD will remain bullish. Rise from 1.1946 is at least correcting the long term down trend from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4267) so far. Break of 1.3651 will be the first sign of medium term reversal and turn focus to 1.3038 support for confirmation.

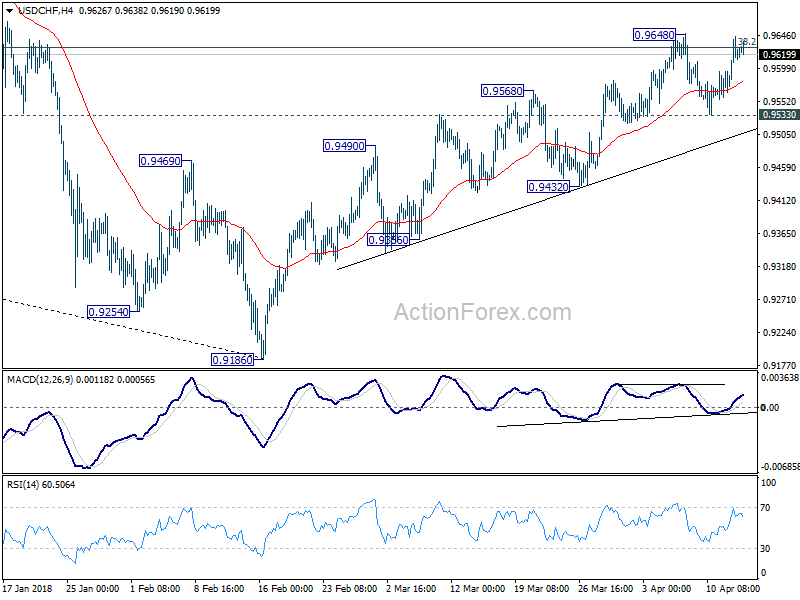

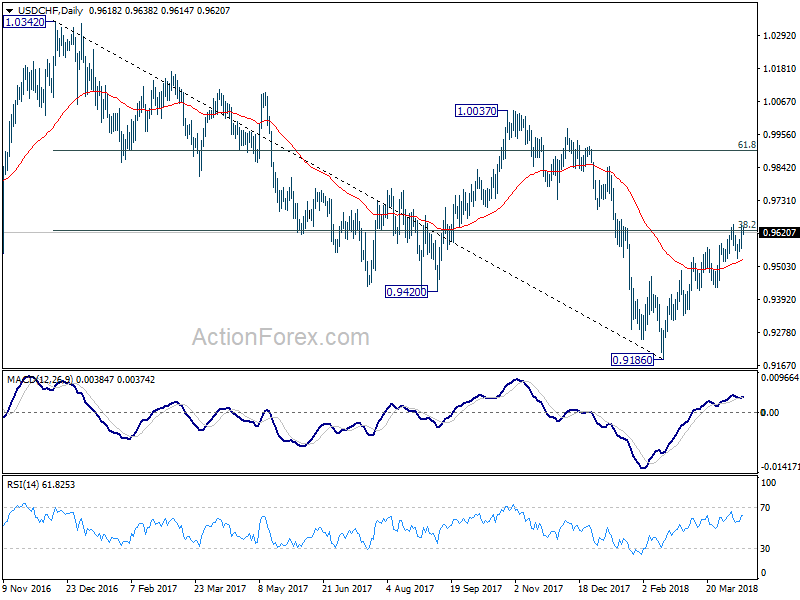

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9575; (P) 0.9610; (R1) 0.9659; More...

Intraday bias in USD/CHF remains neutral with focus on 0.9626 key fibonacci resistance. Sustained trading above this level will be another evidence of larger reversal. In that case, further rally should be seen back to next fibonacci level at 0.9900. On the downside, though, break of 0.9533 minor support should indicate rejection by 0.9626. Further break of 0.9432 will turn near term outlook bearish for retesting 0.9186 low.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

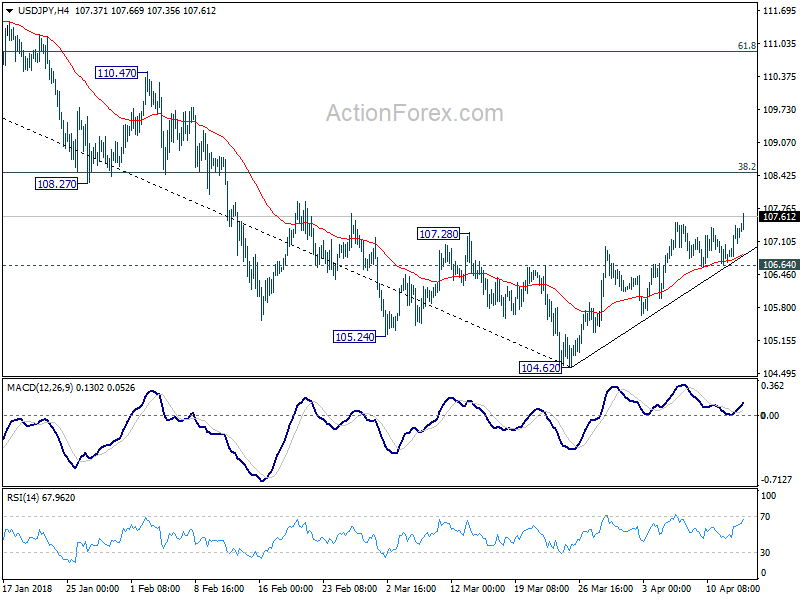

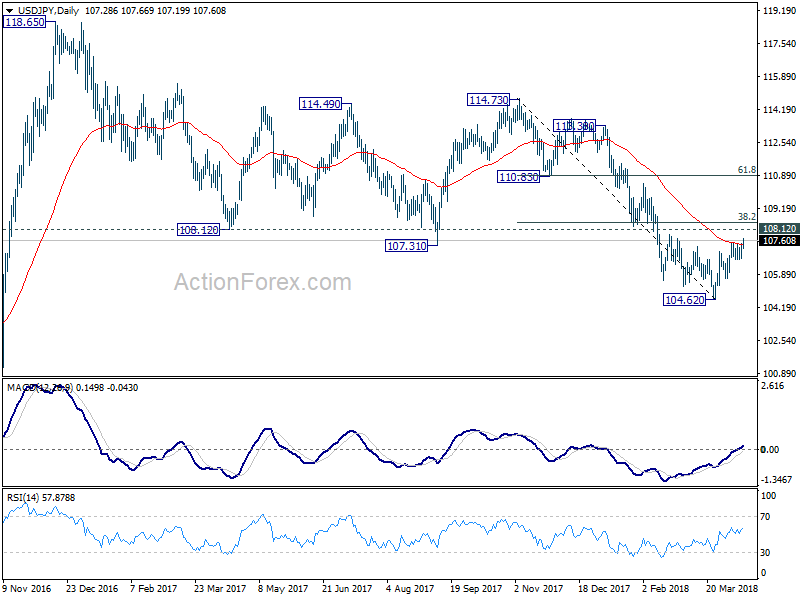

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.88; (P) 107.15; (R1) 107.61; More...

USD/JPY's rebound from 106.42 finally resumed by taking out 107.48 and reaches as high as 107.66 so far. Intraday bias is back on the upside for 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12. This resistance zone will be crucial in determining the medium outlook. On the downside, break of 106.64 minor support is needed to indicate completion of the rebound. Otherwise, further rise will remain in favor even in case of retreat.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.