Sample Category Title

EUR/USD Wave Patterns Depend On Breakout Direction

The EUR/USD remains a difficult currency pair to analyse as price is moving sideways for a lengthy period of time. The bullish breakout could be limited as price challenges potential Fibonacci levels of wave B (brown). A bearish break below the support (blue) could create a larger ABC (brown) whereas a bullish continuation could indicate a larger correction might not take place.

The EUR/USD is building a potential bull flag chart pattern but price will need to break the pattern before a larger bullish continuation is likely. Price could have completed 5 bullish waves which could be part of a wave A (red) within wave B (brown). A break below the support line (blue) could create bearish downside within wave B.

USD/JPY

The USD/JPY bounced at the support trend line (blue) which could indicate a bullish push if price breaks resistance (red). Price is also challenging the Fibonacci levels of a potential wave 4 correction (blue). A break above the shallow Fib levels such as the 38.2-50% Fibs makes such a wave 4 unlikely and that would change the wave perspective to bullish.

The USD/JPY respected the Fibonacci support levels. One more push higher could take price to the 50% Fib whereas a bearish break below the support trend lines could indicate a trend reversal.

Chinese President Xi Soothes Market Worries

With US Producer Prices data on the way this afternoon, and predicted to be largely as expected, the morning session will be dominated by central bankers, as FOMC Member Kaplan and MPC Member Haldane are due to make separate speeches. The US/China Trade War has been dominating headlines, with Chinese President Xi speaking overnight and soothing market worries. He said that China is an open, reforming country that promotes free trade and will stick to this policy in order to succeed. He said that cold war mentality is out of place and dialogue is the way to resolve disputes. He added that China will sharply widen access to the market, will expand imports and lower auto import taxes. He also said that they will strengthen intellectual property protection. The market went risk-on after the speech, USDJPY rising from 106.614 to 107.240. US equity markets regained their losses from the end of the US session and gold fell from 1337.00 to 1330.00

UK Halifax House Price Index (MoM) (Mar) was 1.5% v an expected 0.2%, against 0.4% previously, which was revised up to 0.5%. UK Halifax House Price Index (3m/YoY) (Mar) was 2.7% v an expected 2.1%, against 1.8% previously. This data has been declining since hitting a high of 3.9% in June 2014. This latest release puts the month-on-month reading at a 14-month high, with a strong pick up in the numbers. GBPUSD rose from 1.41020 to 1.41165 following this data release.

The Bank of Canada Business Outlook Survey was published. The capacity pressure indicator has moderated but firms see capacity pressures intensifying over the coming 12 months. Labor constraints continue to be the most prevalent obstacle to firms scaling up operations. Economic slack appears to be mostly concentrated in energy-producing regions. Inflation expectations over the next two years picked up, with over half of the firms expecting inflation to be in the upper half of the 1-3% range. Investment intentions edge down but continue to point to an increase in the next 12 months. The share of firms anticipating strong economic growth in the United States in the next 12 months is near record-high levels. 20.9% of firms said US changes have had an unfavourable impact vs 19.8% prior. USDCAD fell from 1.27535 to 1.27140, moved by this data release.

The ECB's Praet made a speech, giving the following comments on the economy: Inflation developments remain subdued. Monetary policy will evolve in a data-dependent way. There appears to be a disconnect between growth and inflation. An ample degree of monetary policy stimulus remains necessary.

New Zealand NZIER Business Confidence (QoQ) (Q1) data was released at -11%, with a previous reading of -12%. This is the second reading in a row with a negative headline number, something that hasn't happened since 2009.

EURUSD is down -0.10% overnight, trading around 1.23084.

USDJPY is up 0.38% in early session trading at around 107.140.

GBPUSD is up 0.03% this morning, trading around 1.41324.

USDCAD is unchanged in early trade at around 1.26947.

Gold is down -0.30% in early morning trading at around $1,332.39.

WTI is up 0.84% this morning, trading around $63.85.

US Producer Prices Predicted To Be In Line With Expectations

At 08:30 GMT, FOMC Member Kaplan will deliver a speech, and USD crosses may be affected by the comments made.

At 09:30 GMT, MPC Member Haldane is due to speak about the role of central banks and societal inequality at the David Finch Public Lecture, in Melbourne. Audience questions are expected and comments may result in movement in GBP crosses.

At 12:15 GMT, Canadian Housing Starts s.a (YoY) (Mar) will be released, with a previous reading of 229.7K. This data is performing strongly, despite indications that the headline number will decline this month. CAD pairs may see an increase in price movement from this data.

At 12:30 GMT, US Producer Price Index Ex-Food and Energy (YoY) (Mar) is expected to be 2.6% against a previous reading of 2.5%. Producer Price Index (MoM) Mar) is expected to be 0.1% from 0.2% previously. Producer Price Index Ex-Food and Energy (MoM) (Mar) is expected to be unchanged at 0.2%. Producer Price Index (YoY) Mar) is expected to be 2.9% from 2.8% previously. This data is expected to come in largely as expected, with the monthly numbers predicted to be slightly soft. USD crosses may be affected by this data release.

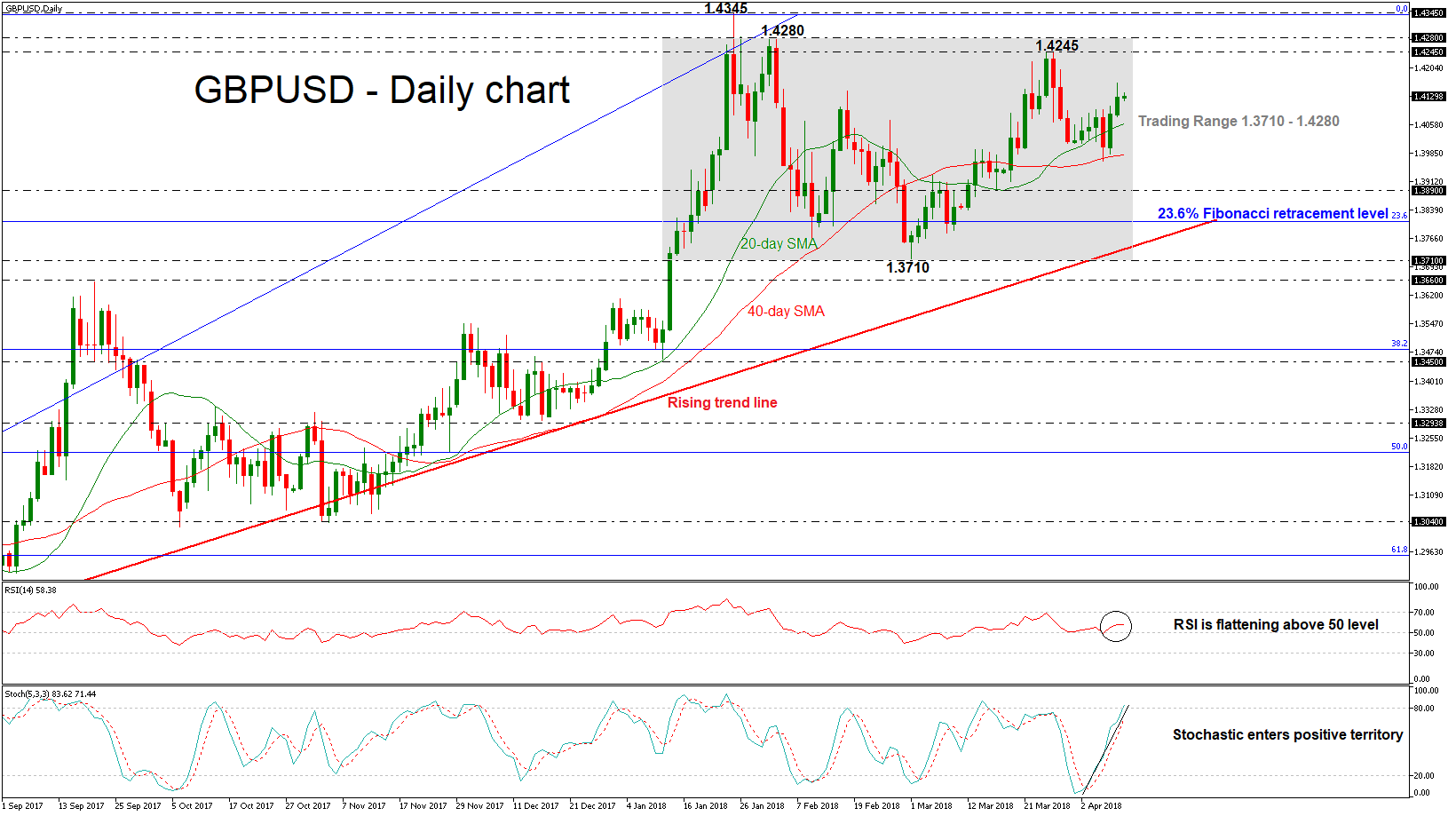

GBPUSD Holds In Trading Range, Bullish Bias Is Expected In Short Term

GBPUSD has been consolidating since January 12 with upper boundary the 1.4280 resistance level and lower boundary the 1.3710 support barrier. The neutral to bullish picture in the short-term looks to last a while longer as prices are still trading in the middle of the trading range. During a previous couple of sessions, the pair rebounded on the 40-day simple moving average and is trying to extend its gains to the upside.

Support was met around the 1.3980 region, forcing the cable to reverse higher. The positive bias in the near-term is supported by the deterioration in the momentum indicators. The %K line of the stochastic oscillator has risen sharply into overbought levels and the %D line is following it. However, the RSI indicator is flattening in the bullish territory, suggesting a continuation of the sideways channel.

If prices continue to head higher, resistance should come from the 1.4245 – 1.4280 area. A jump above this zone would reinforce the medium-term bullish view and open the way towards 1.4345, which has been a major resistance area in the past.

On the flip side, should a downside reversal take form, immediate support could likely come from the 20 and 40 SMAs, near 1.4060 and 1.3980 respectively. A break below the latter level could shift the short-term bias to a bearish one, with the next support coming from 1.3890. Further losses, could drive the pair towards the 23.6% Fibonacci retracement level around 1.3810 of the upleg from 1.2100 to 1.4345.

As a side note, the aforementioned obstacle stands near the ascending trend line, which has been holding since March 2017 and in case of a break below it, could shift the medium-term bullish outlook to negative.

Xi Jinping Provided Equity Bulls A Much-Needed Boost

Appetite for risk bolstered Tuesday morning, as Chinese President Xi Jinping offered plans to further open up the second largest economy. Xi's public speech at the Boao Forum came days after the U.S. and China exchanged tit-for-tat tariffs threats, which had kept investors on edge for several weeks. He promised to lower import tariffs for autos, as well as on some other products, open up the financial and insurance sectors, and most importantly, to increase protection to intellectual property.

Xi's speech calmed markets by responding to all of Donald Trump's concerns, without even mentioning him. Now it's time for China to provide specific figures and a timeline on how these reforms will be implemented. I think what was achieved today is likely to reduce trade tensions and buy some extra time. Whether the U.S. will wave back with an olive branch to China remains to be seen, but certainly, the probability of a full-blown trade war is now much lower than a week ago.

Asian equities were all in the green this morning with the Hang Seng Index and Nikkei 225 climbing more than 1%. Futures are also indicating a positive start to Europe and U.S. – the S&P 500 futures are up 1.3% at the time of writing.

However, the new geopolitical risks over the increased conflict in Syria cannot be ignored. This came after the U.S. imposed a wide range of financial sanctions on Russian assets, causing stocks to suffer their worst performance in four years and the ruble falling as much as 4.1%. Russia warned the U.S. that any military reprisal to Saturdays' chemical attack in Syria could have “grave repercussions”. Will U.S. and Russia go into a confrontation in Syria? This likely depends on Trump's decision over the next 24 hours, but the risks are high.

Although oil prices may have risen on hopes that trade tensions will ease, investors may start pricing in a much higher risk premium. So far, it seems the conflict in Syria has no impact on the supply from the Middle East, but if the battle spills outside the Syrian border, I expect another $10 risk premium to be added to the current price.

The economic calendar is light today, so expect currency traders to continue taking the cue from equity markets.

Currencies: US Holds Mixed Picture As Trade Tensions Ease

Rates: Chinese President reaches out to US to unlock trade conflict

Risk sentiment improved overnight after Chinese President XI Jinping called in favour of a more open Chinese economy and lowering import tariffs on eg vehicles. We hold a negative intraday bias for core bonds with heavy European & US supply also playing in their disadvantage. The consensus bar for US PPI doesn’t seem that high (0.1% M/M).

Currencies: US holds mixed picture as trade tensions ease

FX trading was driven by global risk sentiment yesterday. This factor is still in play this morning after a constructive speech of Chinese President Xi Jinping. However, the impact on the dollar is modest and mixed. USD/JPY tries to regain the 107 barrier. EUR/USD is holding in the 1.23 area. Will US price data be strong enough to support more broad-based USD gains?

The Sunrise Headlines

- US stock markets failed to hang on to positive intraday momentum, but still closed up to 0.5% higher (Nasdaq). Asian stock markets recovered initial weakness after Chinese president Xi Jinping’s speech (>0.5%).

- Chinese President Xi Jinping promised to open the country's economy further and lower import tariffs on products including cars, in a speech seen as conciliatory amid rising trade tensions between China and the US. (Reuters)

- “While risks to growth can be assessed as being broadly balanced, the international trade environment may have added to the downside. Financial conditions have recently tightened, but remain very supportive,” ECB Praet said.

- Dallas Fed Kaplan warned of potential damage to the US economy if the US/Chinese trade conflict won’t get resolved soon even if it’s too early to judge at this stage. He remains in favour of 2 more rate hikes this year.

- FBI agents searched the office, home and hotel room of President Trump’s longtime lawyer Cohen as part of a probe by the US attorney’s office which is coordinated with the office of special counsel Mueller. (WSJ)

- The CBO said that it expected the US budget deficit to swell to $804bn this year, some $242bn more than it projected last summer. The gap would expand to just over $1tn by 2020 (nearly 100% of GDP) (FT).

- Today’s eco calendar contains US NFIB small business optimism and PPI data. ECB Nouy, Nowotny, Visco and Fed Kaplan are scheduled to speak. Austria, the Netherlands, Germany and the US tap the bond market

Currencies: US Holds Mixed Picture As Trade Tensions Ease

US shows mixed picture as trade tensions ease

The (often diffuse) narrative on the US China-trade conflict continued driving FX yesterday. USD swings were modest initially. Later, (US) equities rebounded as markets anticipated a constructive speech of Chinese President Xi Jinping. The risk-on sentiment supported USD/JPY, EUR/JPY and EUR/USD. Cautiously positive comments from ECB members were also euro supportive. Risk sentiment deteriorated later on as the FBI started an investigation against president Trump’s personal lawyer, Michael Cohen. US equities returned most intraday gains and the issue weighed on the dollar. USD/JPY closed the session at 106.77. EUR/USD ended the day near the session top at 1.2321.

Chinese president Xi Jinping kept a positive, open tone on trade in a keynote speech at the Boao forum overnight. Asian equities and US equity futures rebounded and so did USD/JPY. The pair tries again to regain the 107 barrier. The gain of the dollar against the euro remains very limited. EUR/USD is holding north of 1.23.

Markets will today look out for the reaction of the US to the speech of Xi Jinping. US NFIB small business confidence and PPI price data will be published. Headline PPI is expected to rise 0.1% M/M and 2.9% Y/Y. Of late, the trade war overshadowed US data as driver for FX trading. Still, the data might resurface as a driver for trading. The bar of the consensus for the PPI (0.1% M/M) is not that high. We are keen to see the USD reaction in case of a positive surprise. Of late, we had the impression that USD/JPY became a bit more sensitive to good news (both data and risk-on). The picture for EUR/USD remains more diffuse. Last week, EUR/USD drifted gradually lower in the 1.2476/1.2155 ST consolidation pattern. A sustained break of this range bottom will probably remain difficult as long as Fed rate hike expectations are clouded uncertainty on trade.

Sterling trading was still driven by technical considerations yesterday. EUR/GBP held a tight range close to, but mostly slightly north of 0.87. BRC retail sales were OK overnight. Combined with a positive risk-sentiment, this might be slightly sterling positive in a daily perspective. Sterling sentiment wasn’t too bad of late. We maintain the working hypothesis though that really high profile news on Brexit or from the data is needed for EUR/GBP to break the 0.8650 support area.

USD (trade-weighted) holding within ST consolidation pattern. Will easing trade tensions support US currency?

Currencies And Equities Higher After Comments

General Trend:

- Equity markets rise as China President Xi strikes conciliatory tone; makes no reference to possible countermeasures on trade

- China President Xi pledges to open up auto sector and reduce auto-related import tariffs; follows reported request by Trump Administration officials.

- Regional auto names higher after China President Xi noted he would open up auto sector to allow increased % of foreign ownership and lower auto import tariffs; Chinese auto makers lower

- Nasdaq Futures rise over 1.5%

- Aluminum producers rise as prices increase amid US sanctions on Russian elites

- Aussie outperforms on comments from China’s Xi

- Australia March NAB business confidence declines for 2nd straight month

- Fed’s Kaplan sees ‘little bit’ flatter interest rate path likely in 2019; watching yield curve very carefully

- China March CPI and PPI expected on Wednesday's session

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.4%; closed +0.5%

- TOPIX Iron & Steel index +1.8%, Electric Appliances +1.3%

- Japanese automakers gain after comments by China President Xi; Honda up over 2%

- (JP) BOJ Gov Kuroda: Will continue to implement powerful easing - inauguration press conference (overnight)

- (JP) Japan Fin Min Aso: will work to restore trust in finance ministry, was a mistake to ask school officials to lie about Moritomo

Korea

- Kospi opened -0.2%

- (KR) Concerns are growing over the negative impact of the strengthening won on Korea’s exports - Korean press

- (KR) South Korea Fin Min Kim Dong-Yeon: Seeking cooperation from smaller firms to create quality jobs to reduce the country's high youth unemployment rate

China/Hong Kong

- Hang Seng opened -0.1%, Shanghai Composite +0.2%

- Hang Seng Materials index +2.8%, Info Tech +1.6%, Property/Construction +1.5%, Energy +1.1%, Financials +1.1%, Services +1.1%

- Shanghai Composite Property sub-index rises over 1%

- (CN) China President Xi: China GDP has grown on avg 9.5% over last 40-yrs; China reform and opening will definitely succeed; Cold war mentality is out of place, its a zero sum game, isolationism will hit walls; China to lower auto import tariff later this year - remarks at Boao conference

- (CN) Unigroup plans to invest $100B on chip making in 10 years - Chinese Press

- (CN) China PBoC Open Market Operation (OMO): Skips v injects CNY10B in 7-day reserve repos prior; Net: CNY30B drain v CNY30B drain prior

- (CN) China PBoC sets yuan reference rate at 6.3071 v 6.3114 prior

- (CN) China Agricultural Ministry: Expects imports of soybeans to be 'basically normal' in the short-term

- (CN) China Vice Commerce Min Qian Keming: Still hopes to negotiate with US on trade issues; won't back down should a trade war break out

Australia/New Zealand

- ASX 200 opened -0.2%

- ASX 200 Resources index +1.4%, Telecom +1.3%, Financials +1.1%, Energy +0.8%

- (NZ) NEW ZEALAND Q1 NZIER BUSINESS CONFIDENCE: -11 V -12 PRIOR; ADJ BUSINESS CONFIDENCE: -9 V -11 PRIOR

- ResApp, [-6%], RAP.AU Reports positive preliminary results from clinical proof-of-concept studies in obstructive sleep apnea

- (AU) Australia sells A$150M v A$150M indicated in Nov 21 2027 index bonds, avg yield 0.7075%, bid to cover 2.73x

- (AU) Australia Mar NAB Business Confidence: 7 v 9 prior; Conditions: 14 v 20 prior

- Godfreys, [+43%], GFY.AU Co-founder launches takeover bid at A$0.32/shr

- (AU) Banks in Australia said to be noting the need to raise mortgage rates to offset rise in wholesale funding costs – Australian Press

Other Asia

- (MY) Malaysia: Sets May 9th as date for general election

North America

- US equity markets ended higher: Dow +0.2%, S&P500 +0.3%, Nasdaq +0.5%, Russell 2000 +0.1%

- S&P500 Health Care +1%, Technology +0.8%

- (US) FBI raids office of Trump's longtime personal lawyer Michael Cohen; search doesn't appear to be directly related to Mr. Mueller’s investigation - New York Times

- (MX) Mexico to review all forms of cooperation with the United States, including efforts to combat powerful drug cartels - financial press

- (US) Fed’s Kaplan: China and US might be well served ‘to lower heat on trade rhetoric’

- Monsanto [MON]: Dept of Justice reportedly will approve Bayer/Monsanto deal in exchange for additional concessions - press

Europe

- (EU) ECB's Coeure: growth outlook doesn't warrant change in monetary policy stance - radio interview

- (EU) ECB's Praet: inflation developments have stayed subdued

- (UK) Mar BRC Sales LFL y/y: +1.4% v -0.3%e; Retail Spending y/y: 2.0% v 3.8% prior (smallest increase since April 2016); Total Retail Sales y/y: 2.3% v 1.6% prior (highest since April 2017)

- LVMH [MC.FR]: Reports Q1 Rev €10.9B v €10.6Be

- De La Rue [DLAR.UK]: Reportedly activist investor Crystal Amber Fund is building a stake - Sky News

Levels as of 02:00ET

- Hang Seng +1.5%; Shanghai Composite +0.6%; Kospi +0.3%; ASX +0.8%

- Equity Futures: S&P500 +1.2%; Nasdaq100 +1.6%, Dax +1.0%; FTSE100 +0.6%

- EUR 1.2328-1.2307; JPY 107.24-106.62; AUD 0.7738-0.7693;NZD 0.7332-0.7304

- Jun Gold -0.3% at $1,335/oz; May Crude Oil +0.6% at $63.81/brl; May Copper +0.9% at $3.10/lb

EURO Buyers In Control Above 1.2300 Level

The euro continues to push higher against the greenback, with price-action earlier hitting 1.2329, on broad-based weakness in the U.S dollar index. The EURUSD pair is currently intraday bullish while trading above 1.2300 level, although the pair needs to move clearly above the 1.2382 resistance level to regain its medium-term bullish bias. With a lack of eurozone macroeconomic data, traders will look towards the 89.83 support level on the U.S dollar index and release of U.S PPI inflation numbers.

The EURUSD pair is intraday bullish bias while trading above the 1.2300 level, key intraday resistance is found at the 1.2344 and 1.2382 levels.

Should the EURUSD pair decline below the 1.2300 level, key intraday support is found at the 1.2275 and 1.2252 levels.

USDJPY Pair Supported By Dip Buying

The U.S dollar continues to hold firm above the 107.00 handle against the Japanese yen, with traders using any pullbacks in price-action as an opportunity to buy the pair. The USDJPY pair has also diverged from Monday’s theme of U.S dollar weakness, with the pair continuing to create bullish higher price-highs. The USDJPY pair remains intraday bullish while trading above the 106.77 level, and currently retains a high correlation with U.S and Japanese equity markets.

The USDJPY pair remains intraday bullish while trading above the 106.77 level, further upside towards the 107.49 and 108.00 levels appears possible.

Should the USDJPY pair fall below the 106.77 level, a deeper price-correction towards the 106.60 and 106.30 levels seems likely.

US Data Headlines Tuesday Trading

The economic calendar picks up on Tuesday after a slow start to the week with US figures set to drive headlines in North American trade.

The European data session begins at 06:45 GMT with a report on French industrial output. February industrial output is projected to rise 1.5% after sinking 2% the previous month.

Italy will report a similar data set later in the session. The Italian figures are projected to show industrial output growth of 4.8% for February.

Monetary policy is also on the agenda Tuesday. US Federal Open Market Committee (FOMC) member Robert Kaplan will deliver a speech at 08:30 GMT. One hour later, the Bank of England's Andrew Haldane will deliver remarks.

Shifting gears to North America, the Canadian government will report on housing at 12:15 GMT. Ground-breaking for Canadian homes is projected to fall to a seasonally adjusted annual rate of 219,000 in March, compared with 229,700 in February.

The Canadian government will also report on February building permits at 12:30 GMT. Permits likely rose 1.3% for February, based on the latest consensus forecasts.

At 12:30 GMT, the US Department of Labor will report on producer inflation. The March data set is projected to show growth of 2.9% annually, compared with 2.8% for February.

Core producer inflation, which strips away food and energy costs, is forecast to grow 2.6% annually.

The Commerce Department will report on wholesale inventories at 14:00 GMT. Inventories, which are used to calculate gross domestic product (GDP), are forecast to grow 0.9% month-on-month in February.

Energy traders will also be keeping a close eye on weekly crude inventory figures courtesy of the American Petroleum Institute (API) at 20:30 GMT. The official inventory results will be presented the following morning by the US Energy Information Administration (EIA).

EUR/USD

Europe's common currency rode a tailwind higher on Monday, with the EUR/USD climbing back above the critical 1.2300 level. At the time of writing, EUR/USD was trading at 1.2314. The up-move was largely a result of weakness in the US dollar. Immediate support for the uptrend is located at 1.2260.

GBP/USD

The Cable extended its upside on Monday to a high of 1.4156. GBP/USD would later consolidate in the 1.4120 range, where it was trading at the time of writing. The pair faces strong resistance at 1.4200. A break above this level would extend the rally back to the 26 March high of around 1.4240.

USD/CAD

The greenback fell sharply against its northern rival at the beginning of the week, with USD/CAD plunging 120 pips to break below 1.2700 for the first time since February. The pair will likely be driven by economic data from both sides of the border on Tuesday.