Sample Category Title

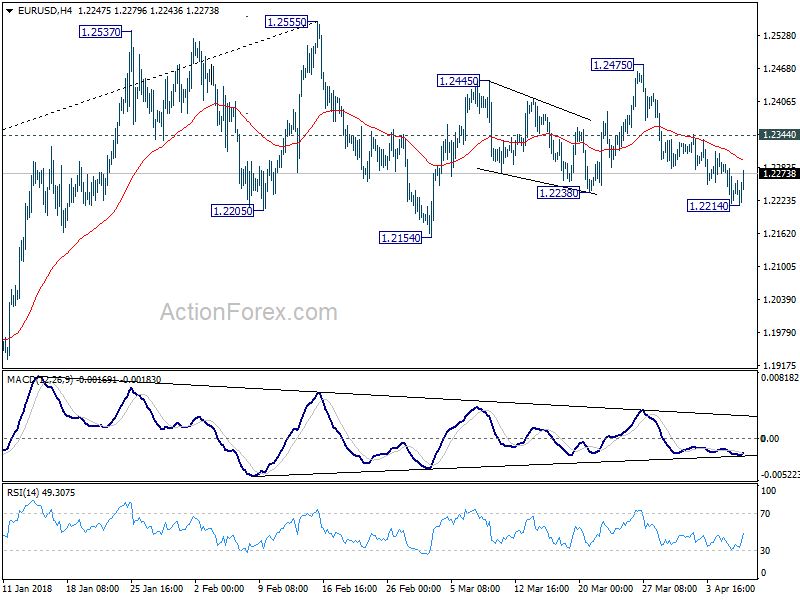

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2207; (P) 1.2249 (R1) 1.2279; More....

Intraday bias in EUR/USD is turned neutral with current recovery. For now, another decline is expected as long as 1.2344 minor resistance holds. Below 1.2214 will target 1.2154 first. Firm break there should confirm rejection by 1.2516 key fibonacci resistance. In that case, whole decline from 1.2555 should target 38.2% retracement of 1.0339 to 1.2555 at 1.1708 next. However, break of 1.2344 will turn bias back to the upside for 1.2475 and above to extend recent range trading.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

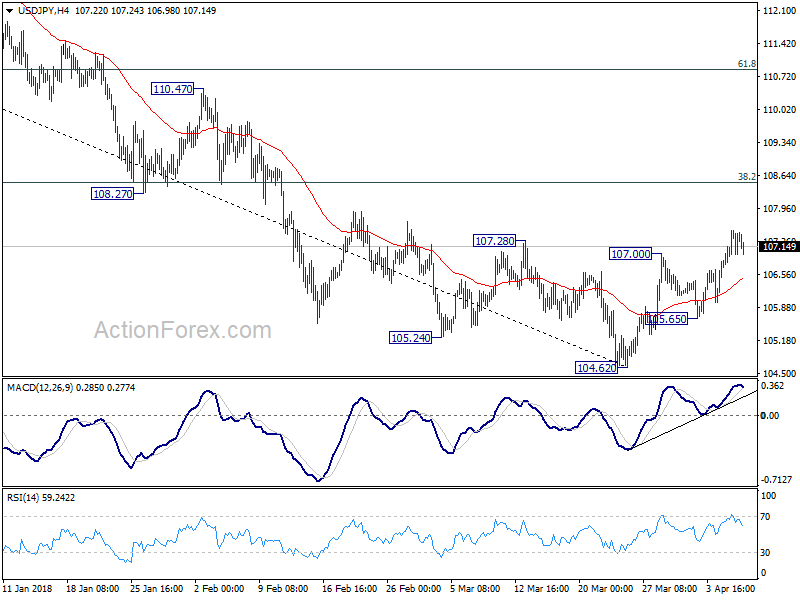

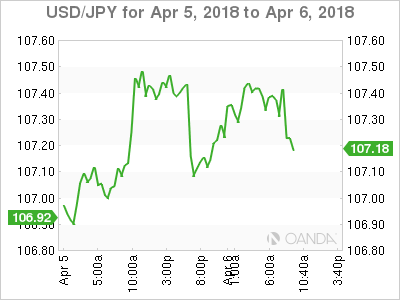

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.89; (P) 107.19; (R1) 107.68; More...

No change in USD/JPY's outlook. Even though rebound from 104.62 might extend, the reaction from 38.2% retracement of 114.73 to 104.62 at 108.48 is crucial to determine the outlook. Firm break of 108.48 will add some credence to the case of trend reversal. And USD/JPY should target 61.8% retracement at 110.86 next. Nonetheless, rejection from 108.48 (which is close to 108.12 key resistance too), will retain bearishness. Break of 105.65 support will indicate that the rebound is completed and turn bias back to the downside for 104.62 and below.

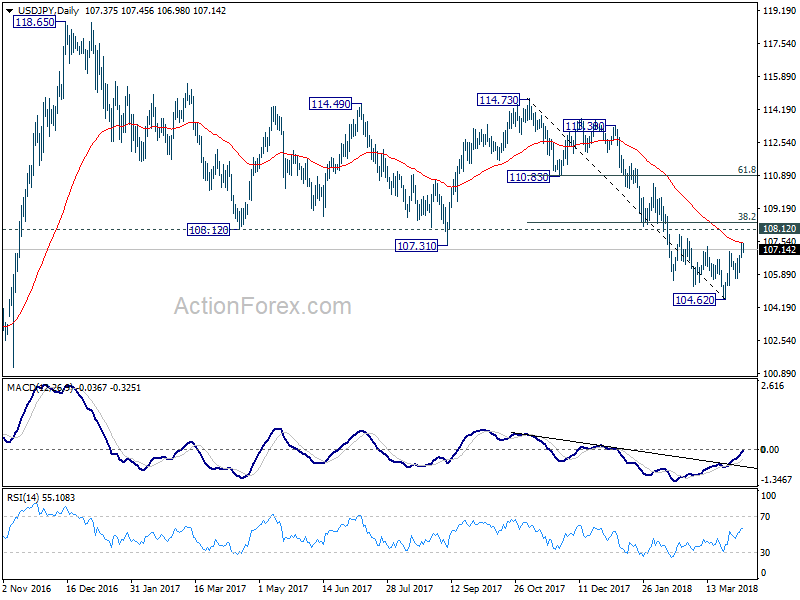

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

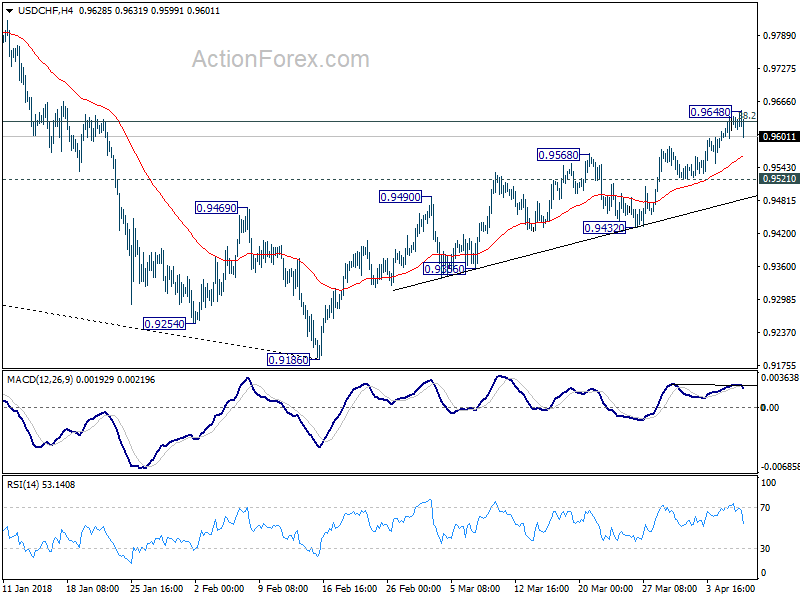

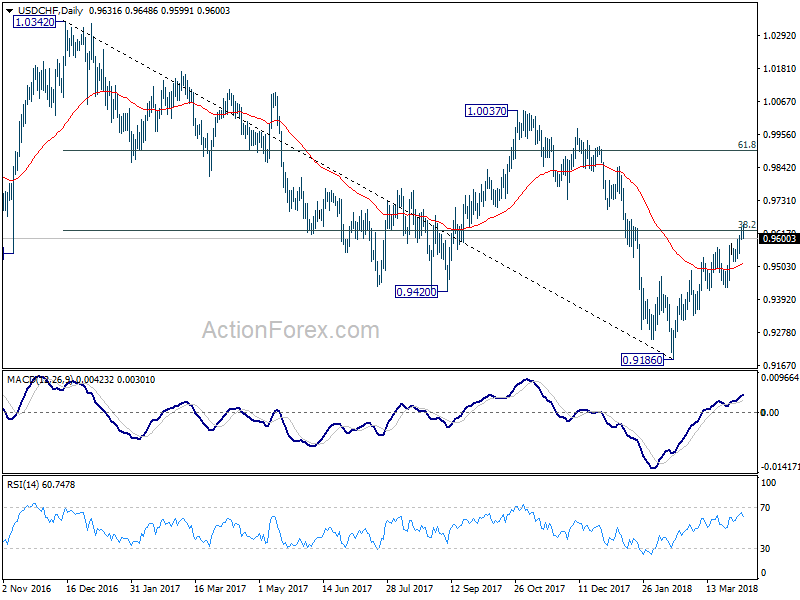

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9607; (P) 0.9623; (R1) 0.9649; More...

Despite edging higher to 0.9648, USD/CHF failed to sustain above 0.9626 key fibonacci level. With 4 hour MACD turned below signal line, intraday bias is turned neutral first. Rejection from 0.9626, followed by by break of 0.9521 support, will turn bias back to the downside for 0.9432 support. Break there will indicate near term reversal and completion of rebound from 0.9186. Meanwhile, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above. However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

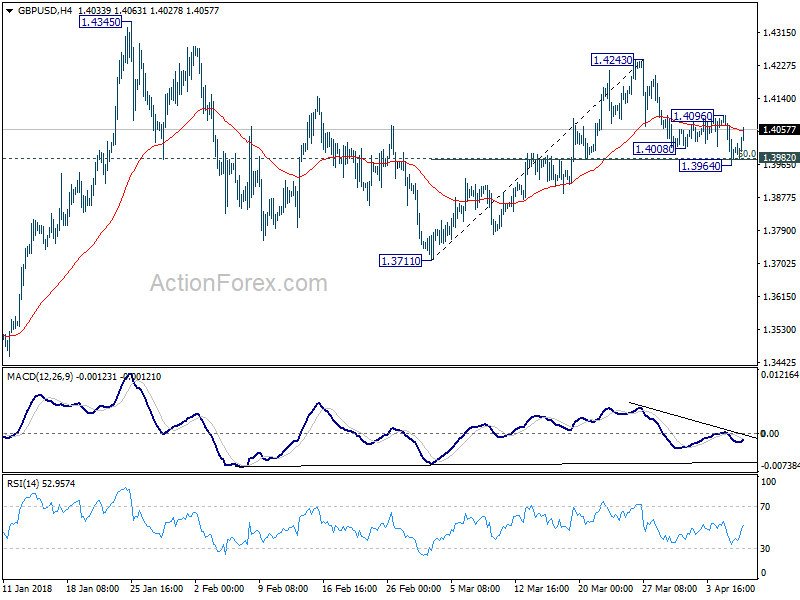

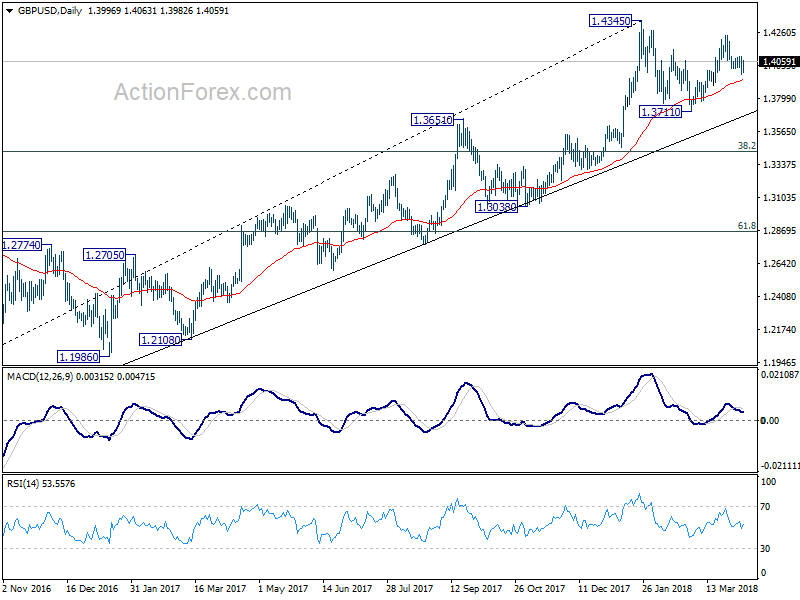

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3947; (P) 1.4022; (R1) 1.4078; More....

Despite dipping to 1.3964, GBP/USD failed to sustain below 1.3982 support so far and recovered strongly. Intraday bias remain neutral first. Strong rebound from 1.3982, followed by break of 1.4096 minor resistance will retain near term bullish and turn bias to the upside for 1.4243. Break will resume the rally from 1.3711 for 1.4345 high first. Nonetheless, decisive break of 1.3982 will indicate completion of the rise from 1.3711. In that case, deeper decline should be seen back to retest 1.3711.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

US: Job Growth Takes a Breather in March

U.S. payrolls took a breather in March, up just 103k. That modest hiring, however, follows a 326k surge in February. Over the first quarter, hiring has averaged a healthy 202k jobs per month.

Both goods and services sector hiring slowed in March. Notably, the construction sector lost 15k jobs, after a sizeable 65k gain the prior month, evidence of how the warm weather in February likely pulled forward hiring in the sector. The retail sector also lost jobs (-4k) after an outsized gain the prior month. Hiring slowed across most sectors after very healthy gains in February.

The unemployment rate remained unchanged at 4.1% as job gains matched growth in the labor force. The labor force participation rate was down a tick to 62.9%. Overall, participation in the labor force has been fairly steady since early 2016, but that hides an encouraging upward trend for core-age workers (25-54 yrs.), which is being offset by the large cohort of baby boomers entering retirement.

Wage growth accelerated in March, up 0.3% on the month. That left average hourly earnings up 2.7% year-on-year. Over the past three months, wages have advanced at a 3.2% annualized pace.

Key Implications

After red-hot hiring in February, a slowdown in March does not come as a surprise. It is also worth noting that typically payrolls in March disappoint on average by -48K, the most next to May. Smoothing the hiring trend over a few months shows a healthy pace of job gains. The fact that the unemployment rate remained at its low 4.1% level, and wage growth accelerated, are better indicators of the health of the U.S. labor market.

Tax cuts and increased government spending are expected to add fuel to this fiery labor market over the coming months. The economy is expected to run at roughly 3% over the next few quarters, and the resulting demand for labor should drive the unemployment rate below 4% by the end of the year.

While some might be a bit disappointed by the modest headline hiring tally, we are inclined to discount it. Continued progress in wage growth should give the FOMC the green light to continue to raise rates at a gradual pace. We expect two more 25 basis point hikes in 2018, but if inflation starts surprising to the upside there is certainly an upside risk to this view.

March Marks Another Month of Canadian Job Gains

Canada added 32.3k jobs on net in March, an improvement over February's 15.4k pace. A roughly equal climb in the size of the labour force (+30.1k) left the unemployment rate unchanged at 5.8%.

It was full-time employment that led the way in March, with 68.3k net positions added, more than offsetting a 35.9k decline in part-time employment.

Public sector employment added 19.6k positions as the private sector shed 7k. With this resulting in just a 12.5k net gain in employees, it was self-employment that rounded out the gain, up 19.8k in March.

The report presented a mixed bag in terms of industries: notable gains were seen in construction (+18.3k), public administration (+11.9), and educational services (+8.4k). On the other side, notable net declines were recorded for information services (-8.7k) and manufacturing (-8.3k).

Regionally, the majority of the action was seen in Quebec (+16k), Ontario (+10.6k), and Alberta (+8.3). While provincial unemployment rates were little changed in general, Alberta stood out as its rate dropped from 6.7% to 6.3%.

Despite the bulk of the gains being recorded in full-time work, aggregate hours were roughly unchanged in March, bringing the year-on-year pace to 2.2%. On the wage front, there was little change as wages among permanent employees matched February's 3.1% gain in March.

Key Implications

On its face, today's report is something of a mixed bag. The main roulette wheel may have landed on an above-expectations 32.3k net positions, but the details were decidedly mixed. All of the gains were in full-time employment, but the bulk of the net change was in self-employment. Moreover, hours worked – a helpful measure of overall economic activity – turned in a soft performance.

Of course, with a report as volatile as this, caution should be the watchword. Trends are much more informative, and they remain fairly solid. On a 6 month moving average basis, both headline (22.2k) and full-time (36.9k) job gains remain in healthy territory, while part-time employment continues to trend lower.

Identifying a trend in wages is more challenging. After a rapid ascent over the back half of last year, there are signs of stabilization around the 3% mark. While this pace of wage gains is fairly robust by the standards of the inflation targeting era, the Bank of Canada has indicated that this pace is nevertheless below what they would expect in an economy with tight labour markets. As such, we doubt that today's report will do much to move the needle in terms of bringing rate hikes forward.

Weak Jobs Growth Barely Shakes USD

- Wages More Important to Traders Than Job Creation;

- China Prepared for New Counter-Tariffs.

It’s not often that the see a miss of around 88,000 in the US job creation figures and markets shrug it off but that’s exactly what we’ve seen today.

The US jobs report was somewhat overshadowed this week by the ongoing back and forth between the world’s two largest economies which has threatened to disrupt the period of strong growth the global economy is seeing. Despite that, traders as ever were paying very close attention to the data release and were clearly unmoved by what they saw, despite the NFP number being well below expectations.

Was this a sign that traders are only interested in trade wars right now as opposed to the economic data? I don’t think so. I think this is a sign that the component of the report that traders are focused on has changed, with average hourly earnings now being of far more interest. Unemployment is very low and whether that’s 4.1% or 4% doesn’t make a huge amount of difference, the economy is on a very good trajectory and with the passing of tax reforms, it will get there some time soon.

Inflation on the other hand is certainly not guaranteed and traders are looking for clues that, given the apparent tightness of the labour market, inflationary pressures are building. The average hourly earnings component of the report offers some insight into this as higher earnings are typically associated with higher inflation. They were in line with expectations on an annual basis at 2.7% and slightly ahead on a monthly basis at 0.3%, which may explain why the dollar slightly weakened after the release before returning to pre-report levels shortly after.

With the jobs report out of the way and holding no surprises of substance, focus will now shift back to trade wars, with the Chinese Commerce Ministry shortly after the jobs data claiming that they have a fully prepared response to Trump’s proposed tariffs. They also claimed negotiations can’t be conducted under these conditions and none have taken place recently. This is more significant than today’s jobs data and is likely to have a greater impact on the markets going forward.

Canadian Jobs Boost CAD, NFP Miss Hurts Dollar

Strong Canadian Payrolls

The Canadian economy added a net +32.3k jobs in March on a seasonally adjusted basis, all of which were in the full-time category. Market expectations were for a net gain of +20k.

- Full Time Employment Change: +68.3k vs. -39.3k prior

- Part Time Employment Change: -35.9k vs. +54.7k prior

- Participation Rate: 65.5% v 65.5% prior

Canada’s unemployment rate was unchanged at +5.8%% last month as the labor force expanded and full-time hiring surged, partially retracing steep job losses that took place in January.

The loonie has caught a bid on the strong report, currently up +0.15% at CAD$1.2751

U.S Job Growth Slows in March; Unemployment Rate Holds at +4.1%

U.S Job Growth Slows in March; Unemployment Rate Holds at +4.1%

The pace of hiring stateside slowed in March and the unemployment rate held at a 17-year low.

U.S nonfarm payrolls rose a seasonally adjusted +103k, a sharp slowdown from February’s gain of +323k (revised).

The unemployment rate was a seasonally adjusted +4.1% for the sixth consecutive month.

Figures for January and February were revised down, subtracting -50k jobs from the first two months of the year. The U.S added +326k in February and +176k in January.

Note: In Q1, employers have added an average of +202k workers to payrolls, outpacing last year’s average growth of +182k per report.

A tighter labor market should also produce better wage growth, but so far that’s failed to materialize. Average hourly earnings for all private-sector workers increased +8c to +$26.82. Wages rose +2.7% y/y in March.

Stock futures have edged slightly lower after the release, while the U.S 10-year Treasury yield has edged lower, down -2 bps to +2.8%, while the USD has slipped -0.2% against G7 currency pairs.

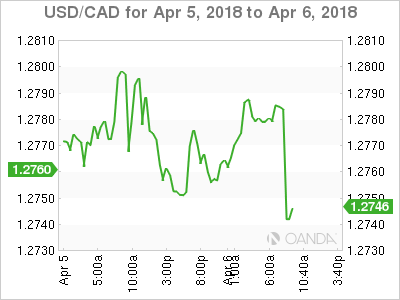

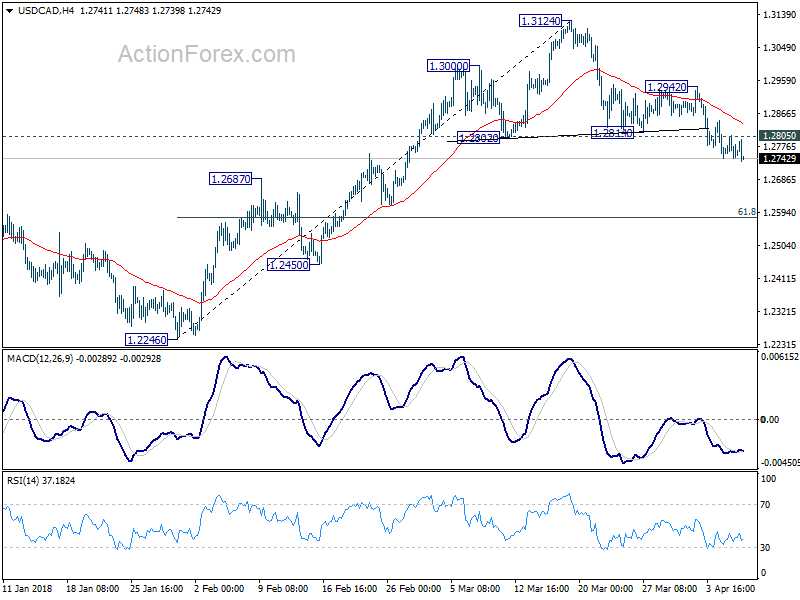

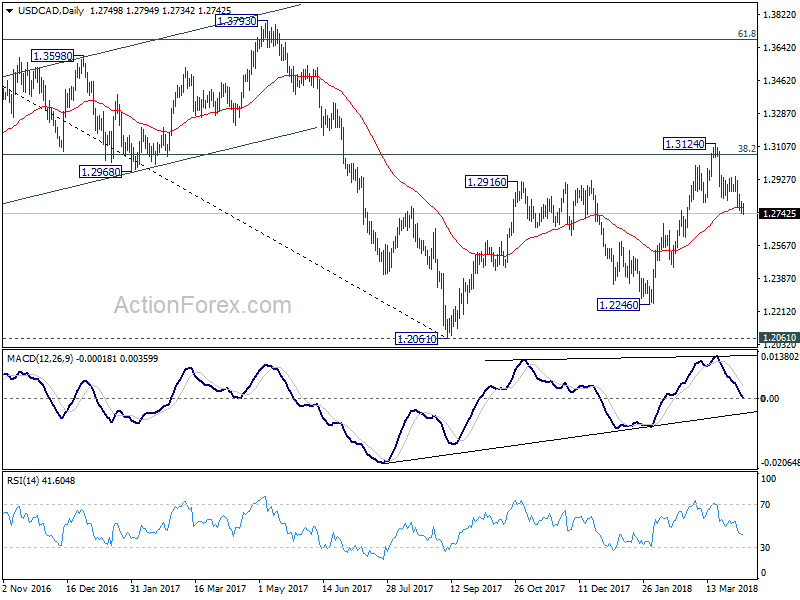

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2728; (P) 1.2767; (R1) 1.2790; More....

USD/CAD's decline continues today and hit as low as 1.2734 so far. Intraday bias remains on the downside. As noted before, near term trend should have reversed with head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942). Decline from 1.3124 should target 61.8% retracement of 1.2246 to 1.3124 at 1.2581 next. Also, noted that current development suggest rejection by 1.3065 fibonacci level. And deeper decline could be seen back to 1.2246 and below eventually. On the upside, above 1.2805 minor resistance will turn bias neutral first. But break of 1.2942 is needed to confirm completion of the decline. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, outlooks is turned a bit mixed again. Strong support was seen from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. But there was no follow through buying above 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Dollar Supported by Wage Growth Despite NFP Miss, No Drama from China’s Brief Press Briefing

Reactions in the financial markets to the escalation in US-China trade tensions remain rather mild. Nikkei closed down just -0.36% today. European indices are in red at the time of writing. But DAX is down -0.5%, CAC down -0.3% and FTSE is nearly flat. US futures point to triple digit loss in DOW at open but it's already they've already recovered much from early day selloff. The press briefing of Chinese Ministry of Commerce is highly anticipated but it's briefer than a usual briefing. Nothing special is revealed there except the pledge to retaliate. It certainly lack the intensity of the Wednesday one.

After all, as we mentioned before, US will have to go through the process of public input till May 22 before finalizing that Section 301 tariff on USD 50b in Chinese imports. There is no implementation date for the this set of tariffs yet. And there is no list of products for the USD 100b of products yet. Even so, it's just Trump's proposal right now. There's still a rather long way to go before US and China hit fire.

Briefer than brief press briefing of China MOFCOM

China Ministry of Commerce Spokesman Gao Feng delivered a rather unimpressive briefing, in response to US President Donald Trump's proposal of tariffs on additional USD 100b of products. Gao just said that US action is extremely wrong, and with misjudgment in the situation. He pledged that China is ready and won't hesitate to retaliate. And there will be immediately action is the US releases the USD 100b tariff list. Gao claimed that China has very detailed retaliatory measures.

Basically, Gao just said that we're ready to hit the ball back hard. But it's now still in your court.

War of words between Trump and China

Earlier today, the Chinese Ministry of Commerce issued a quick response to Trump's intention to add tariffs to additional USD 100b of Chinese imports. It noted in a statement that China pledged to fight US unilateralism and protectionism "to the end, and at any cost". And China will "firmly attack, using new comprehensive countermeasures, to firmly defend the interest of the nation and its people." The MOFCOM also blamed that the the US "singlehandedly started the trade conflicts". And it added that it's "provocation of unilateralism of the US to global free trade".

In a surprised move, Trump announced after yesterday's market close he has just ordered the Trade Representative to consider tariffs on additional USD 100b in Chinese imports, in addition to the USD 50b list of 1300 product lines. In his own statement, Trump condemned China's retaliation as "unfair" to "harm our farmers and manufacturers". He also ordered the Secretary of Agriculture to "implement a plan to protect our farmers and agricultural interests". USTR Robert Lighthizer supported Trump's proposal and said it's an "appropriate response" to China's recent threat of new tariffs.

Dollar supported by wage growth despite headline NFP miss

Dollar attempts to dip lower lower as initial reaction to the big miss in headline non-farm payroll number. But selloff is limited as the greenback is also supported by solid wage growth. The more notable move is seen in USD/CAD with Canada positing its own solid employment data. Otherwise, Dollar is held in familiar range.

US non farm payrolls come in much weaker than expected, showing 103k growth in March only, versus expectation of 189k. Prior month's figure was revised up from 313k to 326k. Unemployment rate was unchanged at 4.1% versus expectation of 4.0%. Nonetheless, average hourly earnings rose 0.3% mom, meeting expectation.

Canada employment grew 32.3k in March, way above expectation of 20k. Unemployment rate was unchanged at 5.8%, meeting consensus.

ECB Cœuré: "Winding back globalization is the wrong solution"

ECB Executive Board member Benoît Cœuré warned of "consequence of protectionism" in a speech at a workshop today. He pointed out that greater global economic integration "has boosted living standards worldwide and lifted millions out of poverty." And, while there are some associated problems, winding back is the "wrong solution. And, a retreat from openness will "only fuel more inequality" as import prices rise, goods become dearer and real incomes fall. The effect of globalization should be addressed by "targeted policies that achieve fairer outcomes."

He also pointed to EU's experience. He noted that "by allowing Member States to recover some of the state functions that have been eroded by globalization, the European Union is a vehicle that brings the benefits of economic openness to the greatest number of its citizens while protecting them against untrammelled global forces." And, "it represents the most progressive model we have for taking back control of globalization by addressing people's concerns over open markets and fair competition - doubts that individual countries on their own cannot dispel."

Elsewhere

Eurozone retail PMI dropped to 50.1 in March. German industrial production dropped 1.6% mom in February. Swiss foreign currency reserves rose to CHF 738b in March. Japan leading indicators rose to 105.8 in February. Japan overall household spending rose 0.1% yoy in February, below expectation of 0.3% yoy. Labor cash earnings rose 1.3% yoy in February, well above expectation of 0.50% yoy.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2728; (P) 1.2767; (R1) 1.2790; More....

USD/CAD's decline continues today and hit as low as 1.2734 so far. Intraday bias remains on the downside. As noted before, near term trend should have reversed with head and shoulder top pattern (ls: 1.3000; h: 1.3124; rs: 1.2942). Decline from 1.3124 should target 61.8% retracement of 1.2246 to 1.3124 at 1.2581 next. Also, noted that current development suggest rejection by 1.3065 fibonacci level. And deeper decline could be seen back to 1.2246 and below eventually. On the upside, above 1.2805 minor resistance will turn bias neutral first. But break of 1.2942 is needed to confirm completion of the decline. Otherwise, outlook will stay cautiously bearish in case of recovery.

In the bigger picture, outlooks is turned a bit mixed again. Strong support was seen from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. But there was no follow through buying above 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Feb | 0.10% | 0.30% | 2.00% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Feb | 1.30% | 0.50% | 0.70% | 1.20% |

| 05:00 | JPY | Leading Index Feb P | 105.8 | 105.5 | 105.6 | |

| 06:00 | EUR | German Industrial Production M/M Feb | -1.60% | 0.20% | -0.10% | 0.10% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Mar | 738B | 734.5B | 732.8B | |

| 08:10 | EUR | Eurozone Retail PMI Mar | 50.1 | 52.3 | ||

| 12:30 | USD | Change in Non-farm Payrolls Mar | 103K | 189K | 313K | 326K |

| 12:30 | USD | Unemployment Rate Mar | 4.10% | 4.00% | 4.10% | |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.30% | 0.30% | 0.10% | |

| 12:30 | CAD | Net Change in Employment Mar | 32.3K | 20.0k | 15.4k | |

| 12:30 | CAD | Unemployment Rate Mar | 5.80% | 5.80% | 5.80% | |

| 14:00 | CAD | Ivey PMI Mar | 60.2 | 59.6 |