Sample Category Title

Briefer than brief press briefing of China MOFCOM

China Ministry of Commerce Spokesman Gao Feng delivered a rather unimpressive briefing, in response to US President Donald Trump's proposal of tariffs on additional USD 100b of products. Gao just said that US action is extremely wrong, and with misjudgment in the situation. He pledged that China is ready and won't hesitate to retaliate. And there will be immediately action is the US releases the USD 100b tariff list. Gao claimed that China has very detailed retaliatory measures.

Basically, Gao just said that we're ready to hit the ball back hard. But it's now still in your court.

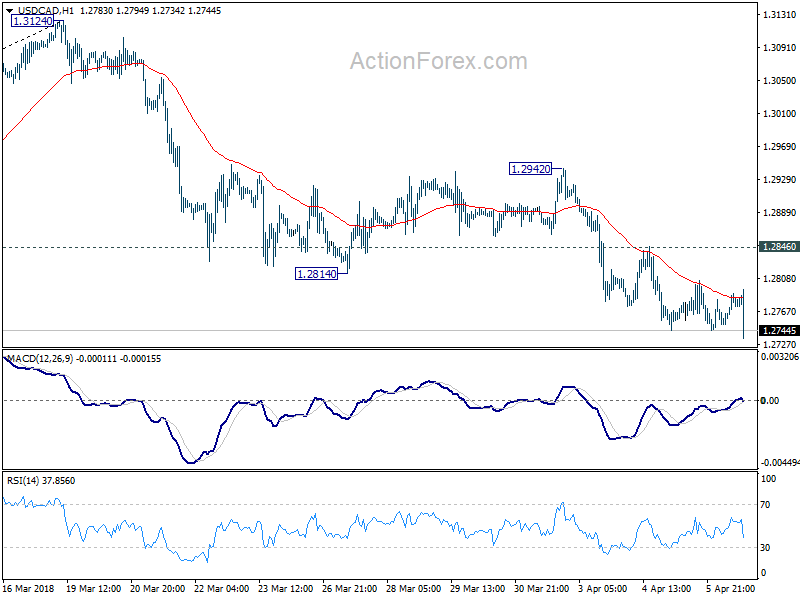

Big miss for headline NFP, but wage growth solid. USD/CAD dives

US non farm payrolls come in much weaker than expected, showing 103k growth in March only, versus expectation of 189k. Prior month's figure was revised up from 313k to 326k. Unemployment rate was unchanged at 4.1% versus expectation of 4.0%. Nonetheless, average hourly earnings rose 0.3% mom, meeting expectation.

Canada employment grew 32.3k in March, way above expectation of 20k. Unemployment rate was unchanged at 5.8%, meeting consensus.

Dollar is trading lower against most major currencies on the head line NFP number. It remains to be seen if the solid wage growth number could give it enough support.

USD/CAD is at the center of attention regarding the batch data in early US session. Apparently, market are responding with a selloff in the pair after the releases.

Uncertainty Goes Up as Trump Chooses Escalation Over Negotiation

Key points

- Trump has chosen to escalate the trade dispute with China further, which adds to the uncertainty and risk of a trade war.

- We still believe the US and China will ultimately strike a deal - but it may take longer than expected.

- It is increasingly likely that the rising uncertainty will weaken the global business cycle in 2018.

- It may also soon start to affect central banks and could possibly delay or soften their tightening paths.

Yesterday we argued that we were entering a more unpredictable phase of the US and China trade dispute and outlined two scenarios: one in which negotiations start and we end up with a kind of a grand bargain between US and China, see Research - Two scenarios for the US-China trade conflict, 4 April 2018. And one in which we escalate further and enter a real trade war. We also argued the first scenario was most likely.

However, for now we were mostly right about the unpredictability as Trump last night chose the path of escalation by ordering his administration to 'consider whether USD100bn of additional tariffs would be appropriate… and, if so, identify the products upon which to impose such tariffs'. He also instructed his agriculture secretary to 'implement a plan to protect our farmers and agricultural interests' from Chinese retaliation. Not surprisingly, China responded by saying it was prepared to strike back and adopt 'new comprehensive countermeasures'. It also repeated that 'China doesn't want a trade war, but we're not afraid to fight a trade war'.

We still believe that the ultimate outcome will be one of a negotiated solution and do not expect Trump to go all the way and enter an all-out trade war. However, it seems things could get worse before they get better. The longer the uncertainty drags out, the higher the probability that we will see this uncertainty feed into lower economic sentiment among businesses and impact real investments negatively for some time while companies await the outcome of the current dispute.

It points to a risk that the current weakening of the global business cycle could be reinforced while the uncertainty prevails. This would normally entail lower bond yields and continued high volatility in equity markets. It could also lead to a delay or soften central bank tightening in both the US and the euro area.

Why we still believe in a solution ultimately

With Trump's clear message of a further escalation and signs that we are entering a tit-fortat trade war, why do we still believe a solution is ultimately found?

First, we know that Trump's negotiation style is to scare his opponent as much as possible and seem irrational enough to do things that could have a very high cost. We saw this in the North Korean crisis, where he warned of 'fire and fury like the world has never seen', although an attack on North Korea would likely have a very high cost in terms of lives in South Korea. Tripling the amount of goods from USD50bn to USD150bn seems like a response out of proportion and designed to scare China (US tariffs would then comprise 30% of total US imports from China and 1.3% of Chinese GDP) . Trump wants the strongest possible hand going into negotiations with China and his hand is strongest if he seems unpredictable and possibly irrational.

Second, while Trump is now escalating the conflict most of his advisors have done the opposite over the past 24 hours. His new economic advisor Larry Kudlow has said there would be negotiation and it was possible there would not be any tariffs at all. The same message has come from Trump's commerce secretary, Wilbur Ross, while US Trade Representative Robert Lighthizer was quick to say that any additional tariffs would not go into effect immediately but would be subject to a 60-day public comment period, as would the penalties announced earlier in the week.

Third, Trump will now come under significant pressure from American businesses that fear for their future sales in China. As we mentioned in our piece yesterday, General Motors now sells more cars in China than in the US and a consumer boycott of US goods could hurt them significantly. The same thing goes for a lot of other brands like Coca-Cola, Nike and Apple. Similarly the agricultural sector will be hurt - even if Trump aims to compensate them short term. They would still lose competitive edge in one of the world's fastest growing markets for the next 10-15 years and lose out on major opportunities here as European and other countries stand ready to take over market shares from US exporters.

Fourth, a trade war with China cannot be won. China's hand is too strong and they can do too much damage to the US economy both short term and long term. China will not flinch from retaliating if measures are implemented away from the negotiating table or are based on a decision outside of the WTO system. If China does not respond to measures taken outside of the global trade system of WTO it would open a Pandora's box of other potential tariffs from other countries. China wants a rules-based system, but will likely respect a decision against them within that system. They are aware of the issue with technological transfer related to joint ventures and Chinese Premier Li Keqiang recently pledged they would take action in this area, see Bloomberg, China Pledges Action on Tech Transfer as Trump Plans Tariffs, 20 March 2018.

What now? Always darkest before dawn

Uncertainty prevails currently and we do not know exactly how far Trump is willing to take this before making a deal with China. However, we still believe a deal will be made. With so much at stake, though, for the US and China, both countries may be willing to push each other very hard before striking a deal. Hence, it seems that uncertainty will be with us for some time and that it will have to get even darker before dawn. With that, it is increasingly likely it will have an effect on global activity in the coming quarters. Nevertheless, this effect should prove temporary and be replaced by a rebound when postponed investments come out of the drawer again.

NFP To Give The Dollar Direction

There are perhaps more arguments in favor of a weaker U.S non-farm payroll this morning (08:30 am EDT), but given the recent strength of the dollar this week, the market seems to have been positioning itself for stronger labor-market numbers. If so, this would suggest that there should be a big reaction depending on the direction of the surprise.

Consensus is looking for an NFP headline print of +175k for March compared with a +313k rise in February that led to a massive equity selloff. The unemployment rate is seen falling to +4.0% from +4.1%. If the U.S labor markets report surprises positively today, something that is quite possible considering this weeks strong ADP report (+241k vs. +206k), will fuel investor concerns about the U.S economy overheating, rate expectations could rise, supporting the dollar even further.

If payrolls exceed +200k, wage-growth rises by +0.3% and the unemployment rate falls as expected, USD/JPY should have the strength and momentum to break ¥108. However, if wages rise by only +0.2%, the unemployment rate holds steady and payrolls are less than +200k, the market will surely consider pushing USD/JPY below ¥106.80 again.

To ease off global risk sentiment, the U.S. non-farm payrolls should show limited signs of wage inflation and a resilient jobs activity, and Fed Chair Jerome Powell should sound “fairly neutral” during his speech later this afternoon.

Elsewhere, heading into the NFP release, European shares are under pressure along with U.S futures after President Trump’s latest threat to target Chinese imports for another $100B in tariffs. U.S Treasury prices are climbing while commodities fall.

On tap: Fed Chair Powell will deliver a speech on the economic outlook during a visit to Chicago at 01:30 pm EDT. San Francisco Fed. President John Williams will speak later. Canadian job numbers are released at 08:30 am EDT.

1. Stocks down on further tariff threats

In Japan, equities fell overnight after U.S President Trump proposed fresh tariffs on +$100B of imports from China in an escalating trade dispute, but the benchmark Nikkei index managed to post a gain for the week. The Nikkei share average ended down -0.4%, while the broader Topix fell -0.31%.

Down-under, Aussie shares ended effectively flat on Friday with investors awaiting China’s response to Trump’s newly proposed tariff plan. The S&P/ASX 200 index closed -10 bps lower, and logged a weekly gain of +0.5%, ending a three-week run of losses. In S. Korea, the Kospi lost -0.33%.

In Hong Kong, shares rallied, catching up to global market gains in the previous session, but the threat of fresh U.S. tariffs quickly pulled stocks off their early highs. The blue-chip Hang Seng index and the Hang Seng China Enterprises index showed a similar gain of +0.8%.

Note: Markets in mainland China, Taiwan and Thailand were closed on Friday.

In Europe, regional indices trade modestly lower across the board on Sino/U.S trade fears. U.S futures have traded sharply lower on the news before making back over half the losses before consolidating ahead of March’s NFP release.

U.S stocks are set to open in the ‘red’ (-0.8%).

Indices: Stoxx600 -0.5% at 374.2, FTSE -0.2% at 7183, DAX -0.7% at 12222, CAC-40 -0.5% at 5250, IBEX-35 -0.4% at 9700, FTSE MIB -0.2% at 22933, SMI -0.7% at 8677, S&P 500 Futures -0.8%

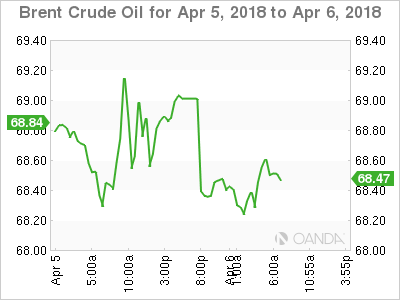

2. Oil moves lower on Trump Threats, gold heavy

Oil prices are again under pressure after U.S President Trump’s threat of new tariffs on China reignited fears of a trade war between the world’s two biggest economies.

Brent crude for June delivery is down -36c, or -0.53%, at +$67.97 per barrel, while U.S West Texas Intermediate crude for May delivery is down -35c, or -0.55%, at +63.19 a barrel.

Note: Both contracts are heading for their biggest weekly fall since early March.

Providing some support to prices this week was the midweek EIA report that reported a +4.6m barrel draw in U.S crude inventories last week, compared with market expectations for an increase of +246k barrels.

The ‘big’ dollars direction after this morning’s NFP release will dictate crude prices next move.

Note: Shanghai crude futures trading will resume on Monday after public holidays in China.

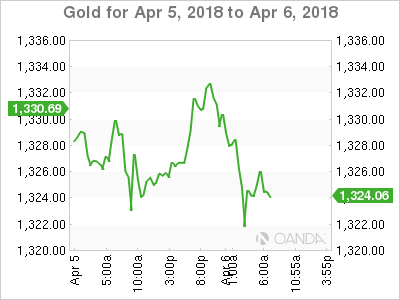

Ahead of the U.S open and payroll numbers, gold prices have hit over two-week lows, weighed down by a firmer dollar even as President Trump re-ignited trade war fears. Spot gold is down -0.2% at +$1,324.01 per ounce, after hitting +$1,321.16 earlier in the session, its lowest since March 21.

3. Sovereign yields range bound

Sovereign yields appear to continue their range trading; reflecting twists and turns in the continuing U.S/China trade conflict.

The yield on 10-year Treasuries declined -1 bps to +2.82%, the largest fall in more than a week. In the U.K, the 10-year Gilt yield declined -2 bps to +1.418%, the biggest drop in more than a week, while in Germany, the 10-year Bund yield declined -1 bps to +0.51%, the largest decrease in more than a week.

In Japan, longer-dated JGB’s prices continue to find support on steady investor demand for debt at the start of the new domestic fiscal year. Super-long (30-years+) JGB yields fell to a new 16-month low amid demand from life insurers and pension funds who were purchasing product to balance their portfolios at the start of the fiscal year, which began April 1. The 30-year yield fell -0.5%.

Fed Chair Jerome Powell will hold a speech on economic outlook at the Economic Club of Chicago (01:30 pm EDT).

4. Dollar maintains firm tone

Despite trade war rhetoric, the U.S dollar is maintaining its firm tone heading into this mornings U.S payrolls release. The FX market has done a good job shrugging off the latest Trump trade rhetoric of more U.S tariffs as a means of getting China to negotiate on trade practices. The USD is poised to register a second consecutive week of gains against G10 currency pairs.

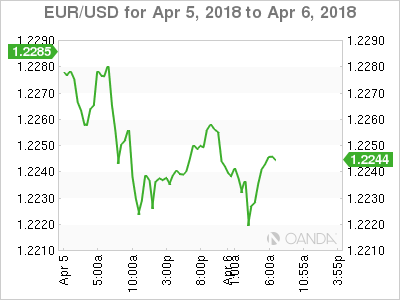

EUR/USD (€1.2241) is probing the lower end of its €1.22 range as Euro data continues to disappoint – Germany’s Feb. Industrial Production missed expectations (see below). GBP/USD (£1.4007) continues to trade atop of £1.4000. Pound ‘bears’ believe the positive Brexit news has largely been priced in, while the Northern Ireland border concerns remain unresolved. USD/JPY (¥107.34) remains little changed, waiting for NFP for guidance.

Elsewhere, TRY has plunged to a fresh record low against the dollar after President Erdogan’s criticism of monetary policy and economic management. USD/TRY now trades up +0.4% at $4.0635 after the pair hit a record high of $4.0665.

NAFTA – The Mexican negotiator is in D.C and the Canadian will be there today. There is a strong possibility of a weekend meeting and a possible situation update. If so, MXN and CAD to trade accordingly on Asians open next week.

5. German industrial production disappoints

Data this morning showed that German industrial output fell in February, more than erasing a modest increase in the previous month.

Industrial output in adjusted terms fell -1.6% in February m/m after a +0.1% increase in January. Market expectations were looking for a +0.3% increase on the month. Y/Y, Industrial output was up +2.6% from February 2017.

The German economy ministry said in a statement “industrial production has lost momentum, however, the good order situation and the positive mood among companies suggest that the industry will remain on an upward trend.”

USDJPY Bullish Heading Into Payrolls

The greenback continues to gain ground against the Japanese yen currency, with price-action surging towards the 107.49 level, on broad-based U.S dollar strength. The USDJPY pair currently trades around the 107.30 level, with bullish momentum largely in place while price trades above the 107.00 level. Traders now look towards the release of the U.S Nonfarm payrolls job report, with analysts expecting 193,000 new jobs to be created and monthly U.S Wage Earnings to tick higher by 0.2 percent.

The USDJPY pair remains intraday bullish while trading above the 107.00 level, key resistance is found at the 107.69 and 108.01 levels.

The USDJPY pair will likely correct lower once clearly below the 107.00 level, key technical support is then found at the 106.60 and 106.00 levels.

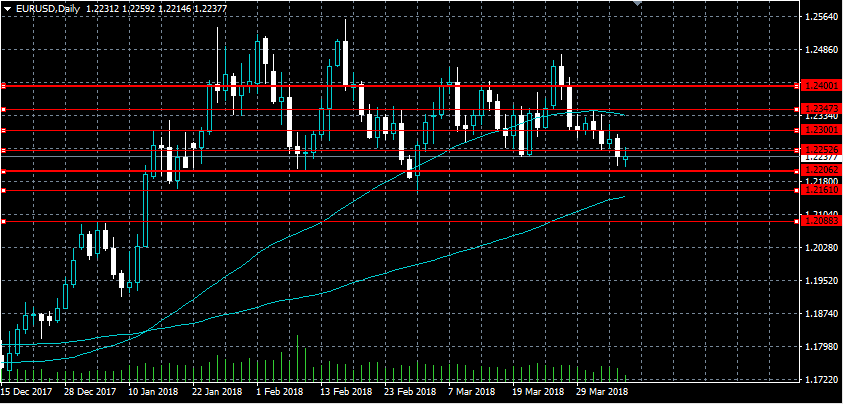

Key Euro Levels Ahead Of U.S. Jobs Report

The euro continues to trade to the downside against the U.S dollar, ahead of today’s key March Nonfarm Payrolls job report from the United States economy. The EURUSD pair is currently trading around the 1.2240 level, with medium-term selling pressures building on the pair while price-holds below the 1.2252 level. A clear breach of the 1.2161 support level should accelerate further euro selling, with the 1.2130 and 1.2088 levels then coming into focus.

The EURUSD pair remains under bearish pressure while trading below the 1.2252 level, key medium-term support is then found at the 1.2206 and 1.2160 levels.

A sustained move above the 1.2300 resistance level, may support further buying towards the 1.2347 and 1.2400 levels.

Forex Analysis: Gold And USDJPY

The U.S. Dollar strengthened on Friday in response to an escalation in trade tensions and ahead of non-farm payrolls (NFP) and wage data. President Donald Trump issued a statement that he was considering $100 billion in extra tariffs, with China quickly responding that it “will take them on until the end at any cost”. However, all eyes will be on the NFP report later today. The expectation is for 188k new jobs to have been created in March, down from the 313k in February. The wage growth number will get the most attention as it is a leading indicator of domestic price pressure and is important to the Federal Reserve inflation forecast and interest rates. If the NFP report surprises positively, which is possible given the strong ADP report, it could cause more Dollar strength.

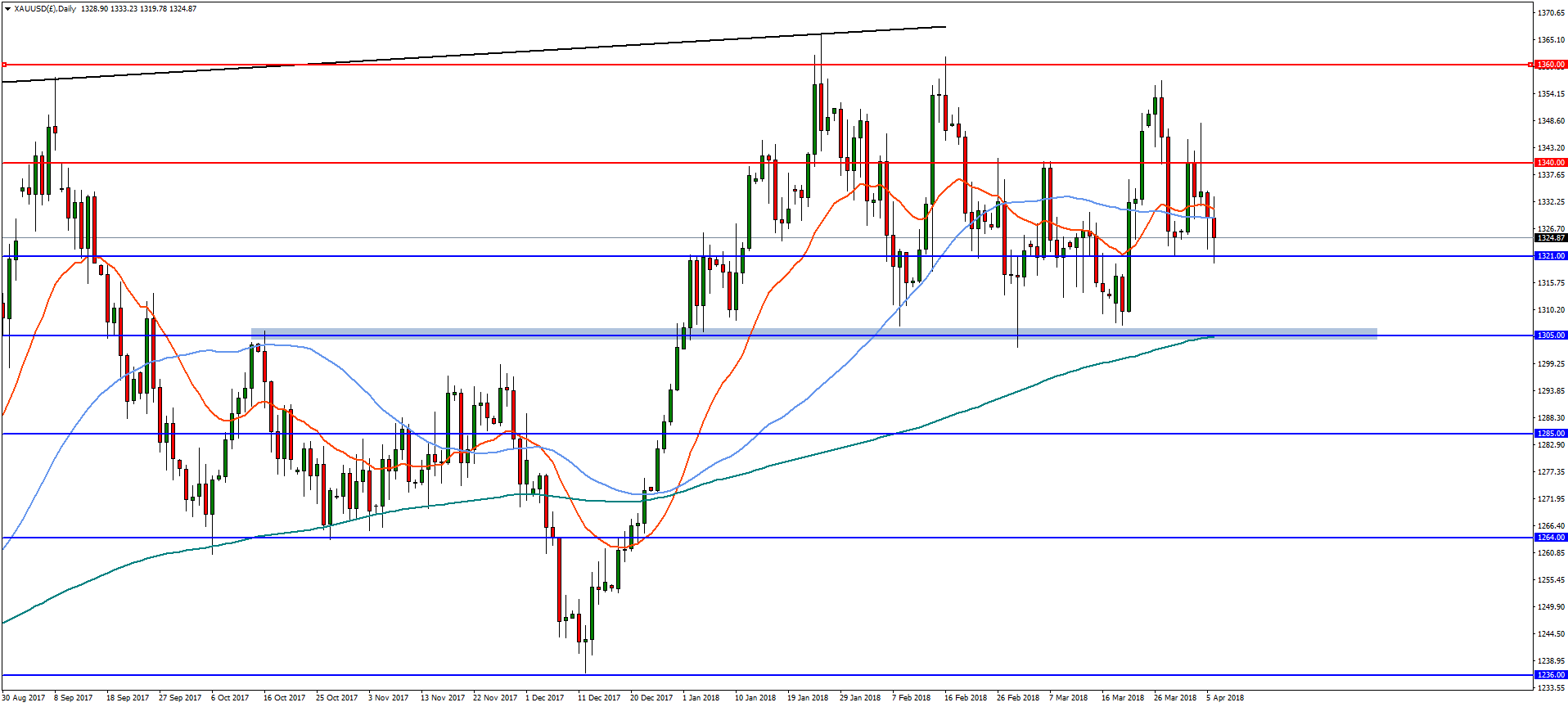

GOLD

Gold is denominated in U.S. dollars so it is likely to react to the NFP report later today. Higher interest rates usually result in a strong dollar and can reduce the appeal of non-yielding precious metals. On the daily chart, Gold is trading above 1321 and a break of this area will open the way for a test of major support at 1305. A decisive break of 1305 is needed to open the way to the 61.8% Fibonacci retracement at 1285. On the flip side, a bullish reversal above 1330 will find resistance at the highs near 1360.

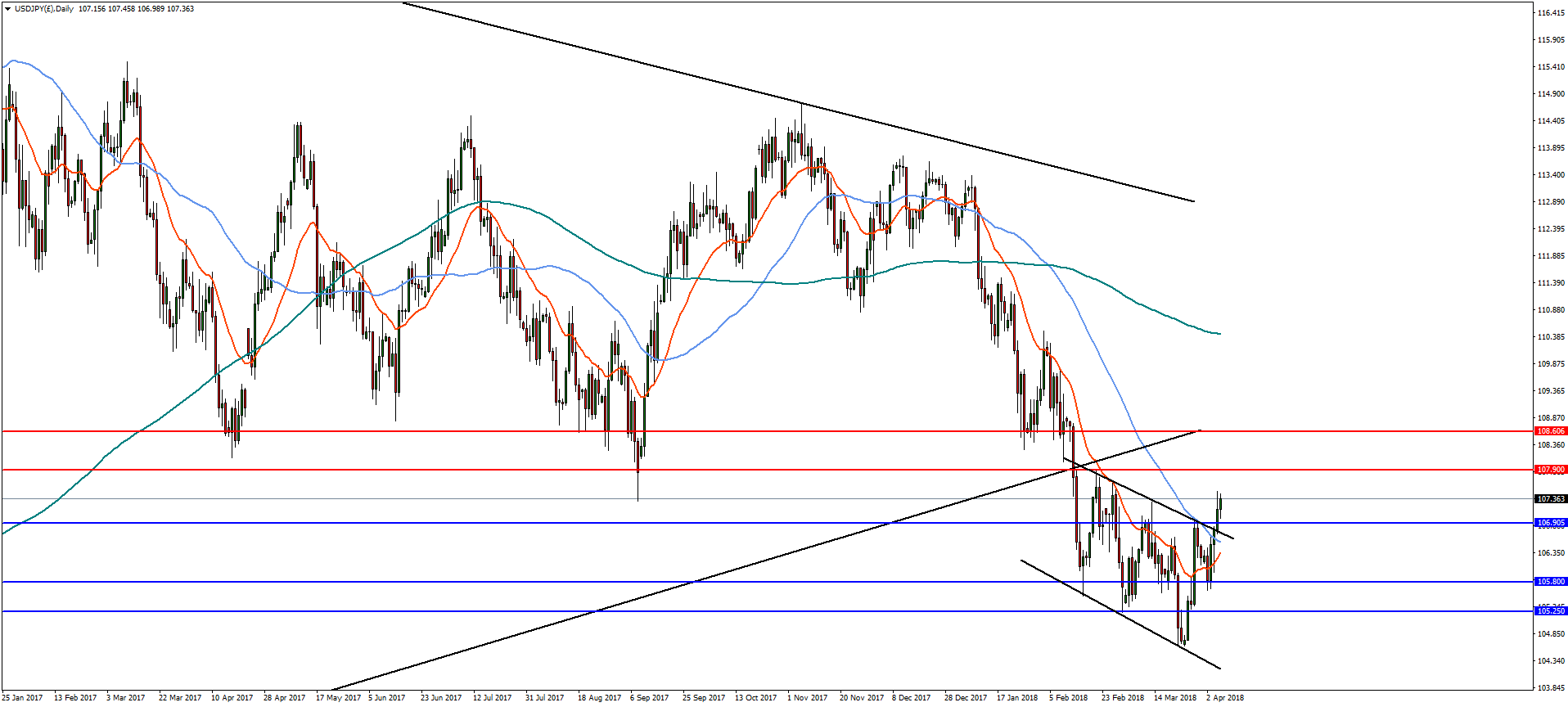

USDJPY

On the daily chart, USDJPY is trading above 107.0 ahead of the NFP report. The recent uptick in USDJPY due to USD strength is being capped due to the Japanese Yen’s safe-haven appeal. Continued upside momentum will find resistance at the 38.2% retracement and horizontal resistance level of 107.90 before attempting a test of the trend line at 108.60. A reversal below the support at 106.90 could open the way to further declines to support at 105.80 and 105.25.

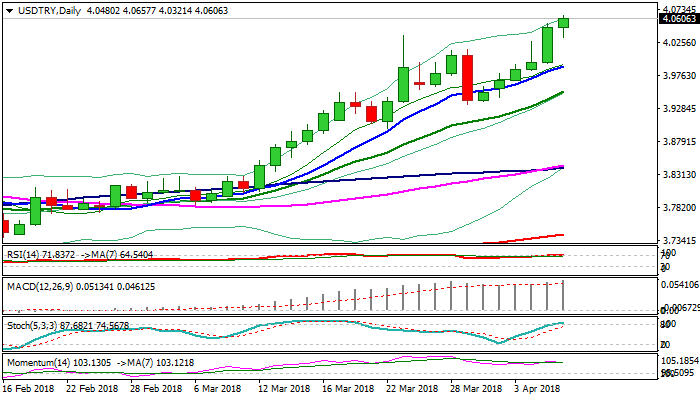

USDTRY Hits New Record Highs On News That CB Is Preparing Plan To Lower Interest R

The Turkish lira hit new record high at 4.0657 on Friday, in extension of previous day's strong fall, with signals that lira could weaken further. Fears among investors rose after news that Turkish government works on measures to lower interest rates, with tax cuts also being in the agenda. Turkish central bank's monetary does not follow the situation in the Turkish economy and current signs that interest rates could be lowered despite double-digit inflation, sets scope for further negative scenario for lira. The USDTRY pair is holding in uncharted area and fresh extension higher approaches initial target at 4.0830 (Fibo 138.2% projection of the upleg from 3.7143 trough) and eyes psychological 4.10 barrier. Upbeat US jobs data could further accelerate dollar for test of initial targets. The pair is also on track for strong bullish weekly close which would be positive signal for further advance, as CBRT policy meeting (due on 25 Apr) comes in focus. Today's low at 4.0321 marks initial support, but more significant point lies at psychological 4.00 support, reinforced by rising daily Tenkan-sen.

Res: 4.0657, 4.0830, 4.1000, 4.1458

Sup: 4.0422, 4.0321, 4.0150, 4.0000

Markets Slip As Trump Proposes New Tariffs

- Trump Tariffs Overshadow US Jobs Day;

- Kudlow Comments Limit Indices Downside For Now;

- Higher Earnings and Inflation May Be Key to 10-Year Treasuries Breaking 3%.

It's jobs report day in the US and yet, as has been the case for most of the week, attention is firmly on the latest wrangling between the US and China, with Donald Trump proposing another $100 billion in tariffs.

'Perhaps Kudlow's comments have indeed reassured investors that those behind the scenes do not have the desire to engage in a trade war as much as Trump does which is limiting the downside'

We saw a remarkable rebound early in the session on Wednesday after China unveiled $50 billion of tariffs of their own in retaliation to those announced by the White House earlier in the week. Dow futures were more than 500 points in the red ahead of the open but it appears some reassuring words from White House economic advisor Larry Kudlow were enough to ease investors' concerns, triggering a rapid rebound with markets ending the day in positive territory and posting further gains on Thursday.

Kudlow reiterated the point that no tariffs will be put in place for at least two months and claimed he believed Beijing will back down. This gave the impression that a trade war is not what Washington is looking for, despite Trump's previous claim that they are easy to win, and that negotiations will take place to avert one if possible. With neither side giving the impression that they're willing to back down though, there's still a very real chance that these could be imposed, along with any others that are announced in the meantime.

The declaration by Trump that he has instructed the US Trade Representative to consider another $100 billion of tariffs under section 301 has once again sent markets lower, although not as much as previous tariff announcements have. Perhaps Kudlow's comments have indeed reassured investors that those behind the scenes do not have the desire to engage in a trade war as much as Trump does which is limiting the downside.

'With midterm elections in November not far away, there's likely to be a lot of nervous Republicans worried about what impact this could have if it's allowed to escalate further'

With midterm elections in November not far away, there's likely to be a lot of nervous Republicans worried about what impact this could have if it's allowed to escalate further. China is quite clearly targeting big swing states and those whose support Trump relied on to get elected. If these tariffs are imposed, they will feel let down and that will show at the polls, potentially causing critical harm to Republicans in the Senate and the House. It's no wonder China feels in a position of power given that Trump has quite a clear weakness.

While the tariffs story will likely continue to be the main mover of financial markets, we can't ignore the data that's about to be released. The US jobs report is arguably the most important economic report we get each month and offers valuable insight into how the labour market is performing and, more importantly right now, whether wages are growing.

'An upside surprise in average hourly earnings today may not be enough to trigger a move above 3% but it will certainly get people thinking about the possibility that higher inflation is coming'

Higher wages typically means higher inflation which, in turn, means more interest rate hikes. So far, the Federal Reserve has been raising interest rates in anticipation of higher inflation but that hasn't really materialised. Should that continue, they may be convinced to take the foot off the gas a little, while signs of inflationary pressures building could encourage them to push for a fourth hike this year, which they weren't far from forecasting last month.

There's a number of reasons the yield on 10-year Treasuries has failed to make the break above 3%, despite coming close on a few occasions recently and one of those, I believe is the lack of inflation. An upside surprise in average hourly earnings today may not be enough to trigger a move above 3% but it will certainly get people thinking about the possibility that higher inflation is coming, given the recent changes to tax rates, and start a chain of events that triggers a big psychological move.

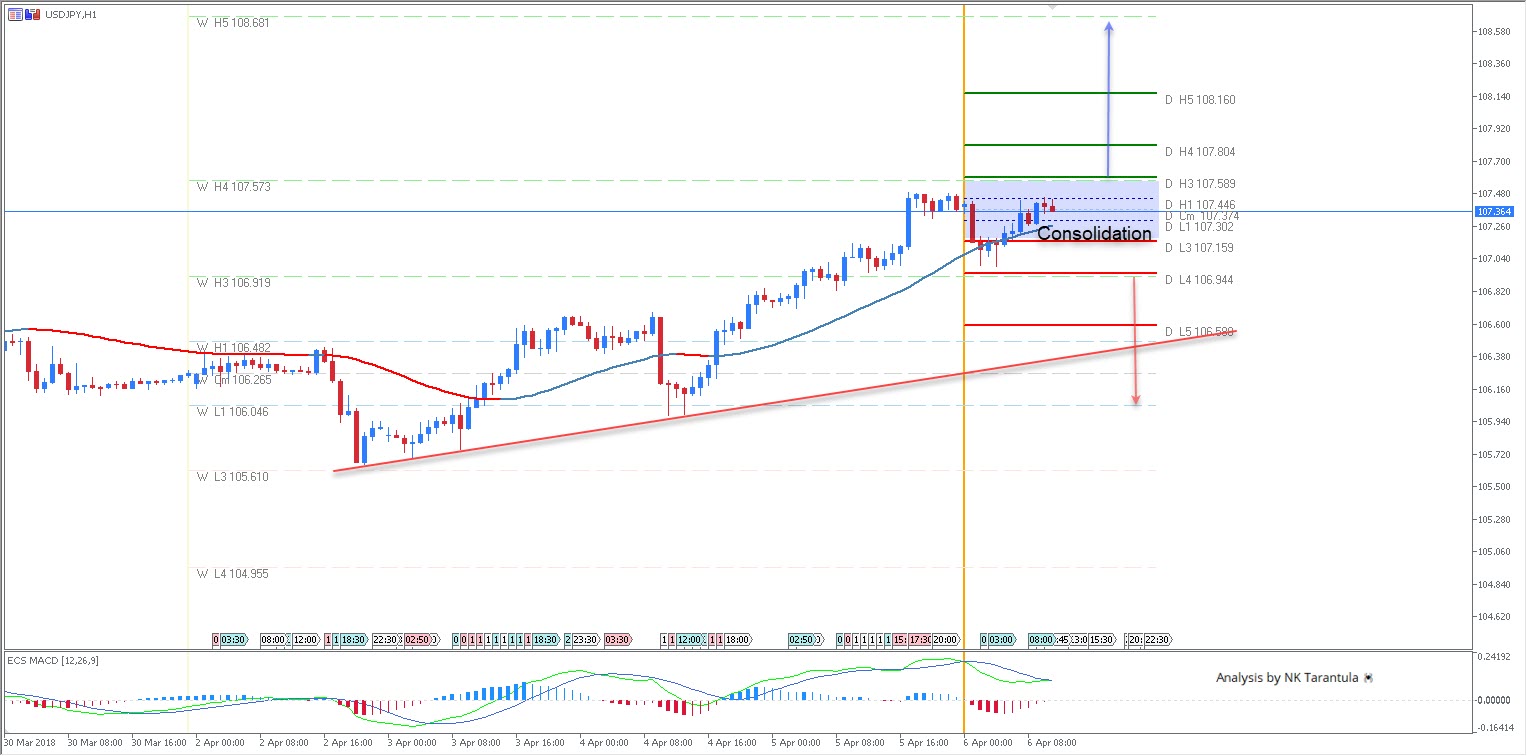

USD/JPY Consolidation Prior To NFP

The price went exactly as planned after yesterday's analysis. The USD/JPY made a continuation move and currently it is consolidating between 107.15-107.60 (blue area). The NFP with all related data (Average Hourly Earnings, Unemployment rate) should decide where the next move will be. Above 107.58 targets are 107.80 and 108.16. Better than expected results could initiate additional momentum. Strong momentum above 108.16 targets 108.68. However a drop below 106.94 should initiate a sell off towards 106.60 and 106.25. Worse than expected results could provide additional bearish momentum below 106.25 for 106.00 retest. Watch for volatility today and possible 2-way price action.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)