Sample Category Title

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2774; (P) 1.2841; (R1) 1.2876; More....

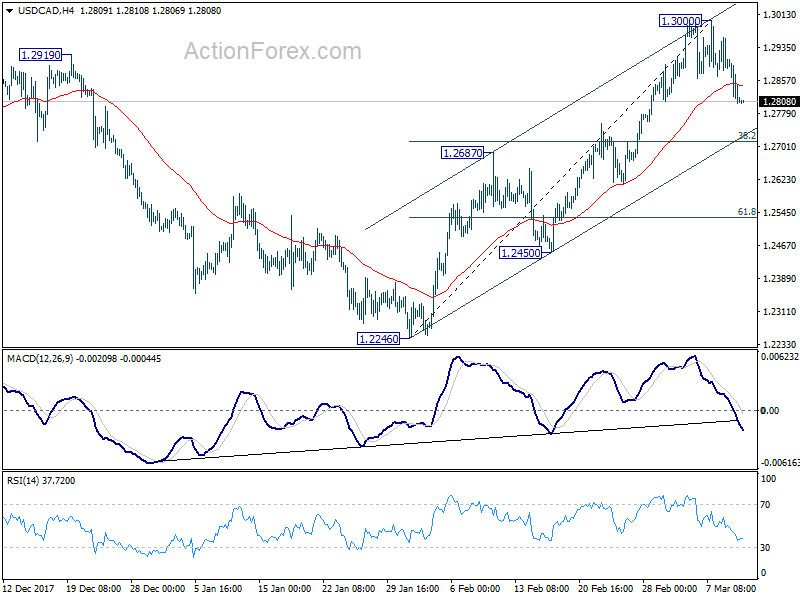

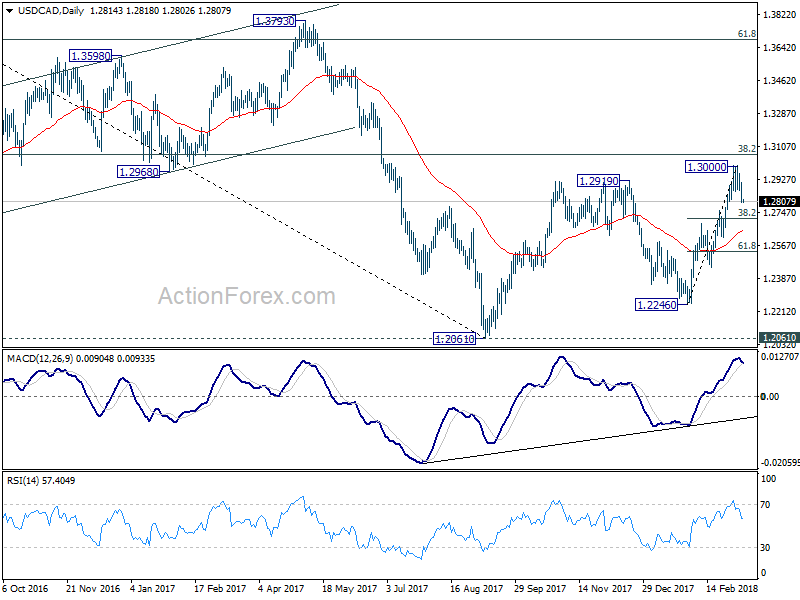

Intraday bias in USD/CAD remains on the downside for the moment. The pull back from 1.3000 might extend to near term channel support (now at 1.2720). At this point, we'd expect strong support from 38.2% retracement of 1.2246 to 1.3000 at 1.2712 to contain downside and bring rise resumption. On the upside, break of 1.3000 will resume the medium term rally to 1.3065 medium term fibonacci level

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Further rally should be seen back to 38.2% retracement of 1.4689 to 1.2061 at 1.3065 first. Break will target 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2687 support holds.

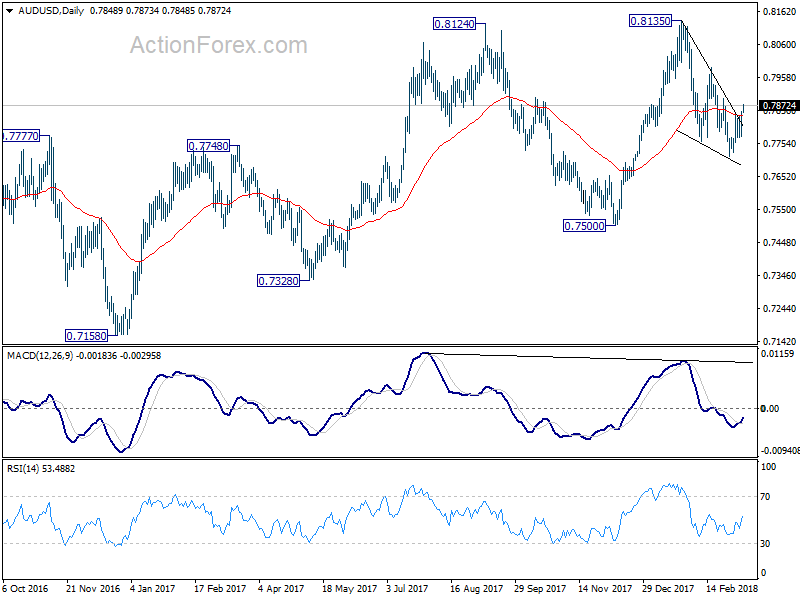

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7797; (P) 0.7825; (R1) 0.7874; More...

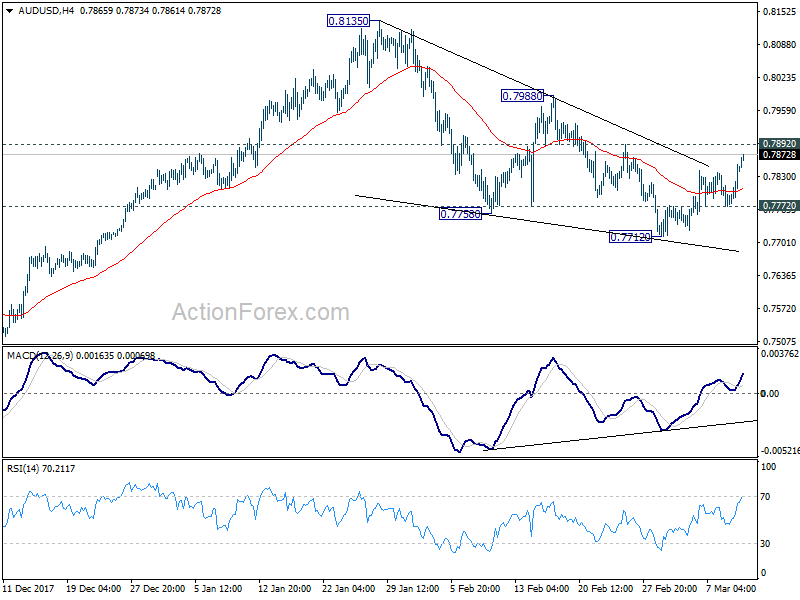

AUD/USD's rebound from 0.7712 extends to as high as 0.7866 so far today. As noted before, the break of f near term trend line resistance is taken as first sign of reversal. Intraday bias remains on the upside for 0.7892 minor resistance first. Break will affirm this bullish case and target 0.7988 and above. On the downside, below 0.7772 will turn bias to the downside for 0.7712. Break there will resume whole fall from 0.8135.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Australian Dollar Lifted by Risk Appetite and Steel Tariff Exemption

Australian Dollar and New Zealand Dollar jump broadly as another week starts in full risk-on mode. Japanese Nikkei opened sharply higher and is trading up 1.4% at the time of writing. Hong Kong HSI is also up close to 1.5%. That followed the strong 1.77% rise in DOW on Friday on the job report that's "perfect for stocks". Aussie is additional supported as the country is exempted from US President Donald Turmp's steel and aluminum tariff. Meanwhile, sentiments are not so positive for the greenback as it's under broad based selling pressure. The markets might be a bit quiet today but a key focus will remain on 1.2268 minor support support in EUR/USD, which will determine the next near term move.

EU sought clarity on steel tariffs, but Trump warned "we TAX CARS"

European Commissioner for Trade Cecilia Malmström met U.S. Trade Representative Robert Lighthizer over the weekend to seek clarity on the steel and aluminum tariffs of the US. However, Malmström expressed her frustrations afterwards complaining that the meeting delivered "no immediate clarity". She tweeted "As a close security and trade partner of the U.S., the EU must be excluded from the announced measures. No immediate clarity on the exact U.S. procedure for exemption however, so discussions will continue next week."

German Economy Minister Brigitte Zypries also warned that "Trump's policies are putting the order of a free global economy at risk." And, "he does not want to understand its architecture, which is based on a rule-based system of open markets. Anyone, who is questioning this, is jeopardizing prosperity, growth and employment."

However, Trump stepped up his rhetoric again as he tweeted "the European Union, wonderful countries who treat the U.S. very badly on trade, are complaining about the tariffs on Steel & Aluminum." He added "if they drop their horrific barriers and tariffs on U.S. products going in, we will likewise drop ours. Big Deficit. If not, we Tax Cars etc. FAIR!"

AU PM Turnbull: We're exempted, why complain?

Following Canada and Mexico, Australia was exempted from the steel tariff of the US. Prime Minister Malcolm Turnbull said there were no strings attached to the exemption. He said that "I know exactly what was discussed and there is no, sort of, request for any change or addition to our security arrangements." He also said that Australia is not going to initiate any complain to the WTO regarding the tariffs. He added that "obviously as a country that will be exempt from those tariffs, we don't have a basis to bring a complaint," he said. Trump tweeted over the weekend that Turnbull is "committed to having a very fair and reciprocal military and trade relationship. Working very quickly on a security agreement so we don't have to impose steel or aluminum tariffs on our ally, the great nation of Australia!

North Korea quiet on meeting with US

North Korea leader Kim Jong-un is set to meet with Trump by the end on May on the topic of denuclearization. It's reported that Kim would want to have a peace treaty with the US. But other than that, the country is so far very quiet on the topic. South Korea's Ministry of Unification spokesman Baik Tae-hyun said today that "we have not seen nor received an official response from the North Korean regime regarding the North Korea-U.S. summit." And, "I feel they're approaching this matter with caution and they need time to organize their stance."

Japan BSI sentiments dropped broadly

Japan business sentiments weakened generally in Q1. Large all industry index dropped to 3.3, down from 6.2. Large manufacturing index dropped to 2.9, down from 9.7. Large non-manufacturing index dropped to 3.4, down from 4.5. Outlook for Q2 showed further deterioration. But large companies are expectation a rebound in Q3. Deteriorations are also seen in sentiments of small and mid sized companies for Q1.

The week ahead

The economic calendar is not particularly busy this week. Major focuses will firstly be on CPI and retail sales from US. SNB quarterly rate decision will also be featured but unlikely to be inspirational. BoJ will also release meeting minutes. Other than that, some China growth data and New Zealand GDP will also be watched. Here are some highlights:

- Tuesday: Australia NAB business confidence, home loans; Japan tertiary industry index; UK annual budget release; US CPI

- Wednesday: New Zealand current account; BoJ minutes; China industrial production, fixed asset investment, retail sales; Eurozone employment change, industrial production; US retail sales, PPI, business inventories

- Thursday: New Zealand GDP; SNB rate decision; US Empire state manufacturing index, Philly Fed survey, import prices, jobless claims, NAHB housing markets index

- Friday: New Zealand BusinessNZ manufacturing index; Eurozone CPI final; Canada manufacturing sales; US housing starts and building permits, industrial production, U of Michigan sentiments.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7797; (P) 0.7825; (R1) 0.7874; More...

AUD/USD's rebound from 0.7712 extends to as high as 0.7866 so far today. As noted before, the break of f near term trend line resistance is taken as first sign of reversal. Intraday bias remains on the upside for 0.7892 minor resistance first. Break will affirm this bullish case and target 0.7988 and above. On the downside, below 0.7772 will turn bias to the downside for 0.7712. Break there will resume whole fall from 0.8135.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q1 | 2.9 | 10.3 | 9.7 | |

| 6:00 | JPY | Machine Tool Orders Y/Y Feb P | 48.80% | |||

| 18:00 | USD | Federal Budget Balance Feb | -222.3B | 49.2B |

Japan BSI sentiments weakened broadly in Q1

Japan business sentiments weakened generally in Q1. Large all industry index dropped to 3.3, down from 6.2. Large manufacturing index dropped to 2.9, down from 9.7. Large non-manufacturing index dropped to 3.4, down from 4.5. Outlook for Q2 showed further deterioration. But large companies are expectation a rebound in Q3. Deteriorations are also seen in sentiments of small and mid sized companies for Q1.

North Korea quiet on meeting with US

North Korea leader Kim Jong-un is set to meet with Trump by the end on May on the topic of denuclearization. It's reported that Kim would want to have a peace treaty with the US. But other than that, the country is so far very quiet on the topic. South Korea's Ministry of Unification spokesman Baik Tae-hyun said today that "we have not seen nor received an official response from the North Korean regime regarding the North Korea-U.S. summit." And, "I feel they're approaching this matter with caution and they need time to organize their stance."

AU PM Turnbull: No ground to complain to WTO, as AU is exempted from steel tariffs

Following Canada and Mexico, Australia was exempted from the steel tariff of the US. Prime Minister Malcolm Turnbull said there were no strings attached to the exemption. He said that "I know exactly what was discussed and there is no, sort of, request for any change or addition to our security arrangements." He also said that Australia is not going to initiate any complain to the WTO regarding the tariffs. He added that "obviously as a country that will be exempt from those tariffs, we don't have a basis to bring a complaint," he said.

Trump tweeted over the weekend that Turnbull is "committed to having a very fair and reciprocal military and trade relationship. Working very quickly on a security agreement so we don't have to impose steel or aluminum tariffs on our ally, the great nation of Australia!

EU Malmström sought clarity, Trump warned “we TAX CARS”

European Commissioner for Trade Cecilia Malmström met U.S. Trade Representative Robert Lighthizer over the weekend to seek clarity on the steel and aluminum tariffs of the US. However, Malmström expressed her frustrations afterwards complaining that the meeting delivered "no immediate clarity". She tweeted "As a close security and trade partner of the U.S., the EU must be excluded from the announced measures. No immediate clarity on the exact U.S. procedure for exemption however, so discussions will continue next week."

German Economy Minister Brigitte Zypries also warned that "Trump's policies are putting the order of a free global economy at risk." And, "he does not want to understand its architecture, which is based on a rule-based system of open markets. Anyone, who is questioning this, is jeopardizing prosperity, growth and employment."

However, Trump stepped up his rhetoric again as he tweeted "the European Union, wonderful countries who treat the U.S. very badly on trade, are complaining about the tariffs on Steel & Aluminum." He added "if they drop their horrific barriers and tariffs on U.S. products going in, we will likewise drop ours. Big Deficit. If not, we Tax Cars etc. FAIR!"

Market Morning Briefing: Gold Bounced Back From Support Near 1310

STOCKS

Overall major stock indices are trading higher.

Dow (25335.74, +1.77%) moved up in line with our expectation and may test immediate resistance near 25500. If that holds, a short dip back towards 25000-24500 is possible else a break above 25500, if seen could be bullish for the index towards

26000 or higher in the medium term.

Dax (12346.68, -0.07%) is almost stable below 12400. While resistance near 12400/500 holds, a fall towards 12200 or lower is possible.

Nikkei (21803.93, +1.56%) is trading just near immediate resistance levels and in case that holds, a short dip is likely in the coming sessions towards 21400-21000. Else a rise above current levels, if seen could take the index higher towards 22600 in the coming sessions.

Shanghai (3326.72, +0.59%) has resistance near 3350 on the 3-day candles and is likely to test that in the next few sessions before coming off from there. Immediate view is bullish within a bearish outlook for the medium term.

While below 10380, Nifty (10226.85, -0.15%) may come off towards 10080-10020 as we have been mentioning for quite sometime. Thereafter a bounce back towards 10320-10380 levels is possible.

Sensex (33307.14, -0.13%) is likely to test 33750 in the near term before coming off from there back towards 33000. Overall range trade is likely to continue for some time.

COMMODITIES

Brent (65.61) and WTI (62.15) have risen well. But note immediate resistances near 66.0-66.5 and 62-63 may limit further upside just now. Trade is expected within 66.50-62 and 63-60 region for the near term.

Gold (1323.60) bounced back from support near 1310 and while that holds the price is likely to trade within 1310-1340 region in the coming sessions.

Copper (3.1345) rose sharply from levels just above 3.05 and while the rise sustains, the price could move up towards 3.17-3.20 in the next couple of sessions. Near term looks bullish.

FOREX

Euro (1.2320) : Draghi's dovish stance in the 8th March press conference and the downward revision of forecasted inflation in 2019 caused the Euro to weaken below 1.24 and it saw a low of 1.2273 on Friday. It is respecting support on weekly candles near 1.228-1.23, but there is some likelihood for it to see a further downmove towards support on daily candles near 1.225 and then bounce from there back towards 1.25-1.26.

The Dollar Index (90.023) saw a bounce from support near 89.5 on daily candles last week after the ECB chief's dovish stance in the press conference. We were expecting the Bank of Japan's meeting on Friday to impact the Dollar – however, the BOJ maintained status quo and the Dollar Index hasn't seen any significant movement since then. As mentioned previously, it has immediate resistance visible on the daily candles near 90.5. If breached, there is higher resistance near 91 on 3 day and weekly line charts. In case of a dip (less preferred) from current levels, the next downside target is 89.75 on daily candles.

Dollar-Yen (106.61) as mentioned on Friday, seems to be respecting immediate resistance near 107 on the daily line charts provided by 13 days and 21 days moving average lines. The Bank of Japan meeting on Friday maintained status quo and didn't cause any significant impact on Yen strength . Dollar Yen in this week could again move down towards 105.5, which is a crucial support and a break of which would lead to medium term bearishness.

The Euro-Yen (131.33) looks likely to move down towards support near 129.75-129.50 seen on daily and 3 day candles in this week. If the Dollar Yen and Euro indeed test supports near 105.5 and 1.225, the corresponding rate for Euro Yen would be 129.23, which would be consistent with the predicted downmove towards support on the Euro yen daily chart.

As per expectation, strong support for the Pound (1.3857) near 1.38 has held and it is now seeing an upmove towards 1.395 (seen as immediate resistance level on daily candles).

Dollar-Rupee (65.17): Dollar-Rupee remains in an overall uptrend. A rise past 65.20 can take the market up to 65.40+.

INTEREST RATES

The Bank of Japan maintained its policy stance unchanged in the Friday meeting, causing no impact to bond yields or forex rates. Infact the Japan 10 Yr yield (0.05%) had bounced from support near 0.038% on the short term chart prior to the BOJ meeting in anticipation of some hawkishness by the central bank. However, with no such development and the BOJ's commitment to maintain the yield rate around the 0% level, it might again move down towards 0.04% in the coming weeks.

The German 10 Yr – US 10 Yr is currently at support near -2.26% on the long term chart and might bounce in this week via a slight dip in US yields.

US 10 Year Yield (2.9011), US 30 year Yield (3.1647), US 5 year yield (2.6621), US 2 year yield (2.2661) : We have been saying that a rise in US yields beyond long term resistance levels is imminent in March. However, last week, we also said that there might just be some drop in US yields in this week, after which the week of the US Fed meeting might then see volatility return, taking yields higher in anticipation of a rate hike. We might be wrong since yields have gone up by 2-3 basis points on average since Friday. We will have to wait and watch to see how the next few days pan out. (Long term resistance levels for the 4 yields have been as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively – a decisive breach of these levels could happen in March 2nd half.)

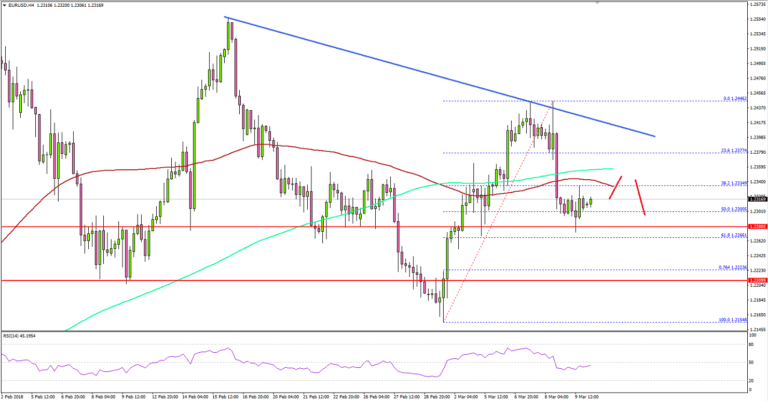

Can EUR/USD Recover Above 1.2370?

Key Highlights

- The Euro declined after trading towards the 1.2450 resistance against the US Dollar.

- There is a key connecting bearish trend line forming with resistance at 1.2400 on the 4-hours chart of EUR/USD.

- The US nonfarm payrolls figure posted a solid rise of 313K in Feb 2018, more than the forecast of 200K.

- Today, the US monthly budget for Feb 2018 will be released, which is forecasted to post $-222.6B.

EURUSD Technical Analysis

The Euro traded higher this past week above the 1.2400 level against the US Dollar. However, the EUR/USD pair could not move above 1.2450 and started a downside move.

The pair made a double top pattern near the 1.2445 level and declined. It moved below the 38.2% Fib retracement level of the last wave from the 1.2151 low to 1.2446 high.

More importantly, there was a close below the 1.2400 support and the 100 simple moving average (red, 4-hour). The pair remains under a bearish pressure and it could decline further towards 1.2250.

A major support is near the 61.8% Fib retracement level of the last wave from the 1.2151 low to 1.2446 high. Below 1.2260 and 1.2250, the pair may retest the 1.2200 support.

On the upside, there is a key connecting bearish trend line forming with resistance at 1.2400 on the 4-hours chart. A break above the trend line resistance is needed for the pair to move back towards 1.2450.

This past Friday, the US nonfarm payrolls report for Feb 2018 was released by the US Department of Labor. The market was looking for a rise of 200K, similar to the last reading.

However, the actual result was better as there was a rise of 313K. The last reading was also revised up from 200K to 239K. Moreover, the unemployment rate remained stable at 4.1%.

The report added:

Among the major worker groups, the unemployment rate for Blacks declined to 6.9 percent in February, while the jobless rates for adult men (3.7 percent), adult women (3.8 percent), teenagers (14.4percent), Whites (3.7 percent), Asians (2.9 percent), and Hispanics (4.9 percent) showed little change.

The overall sentiment is positive for the US Dollar, which is why the EUR/USD pair may remain in a bearish trend.

Economic Releases to Watch Today

US Monthly Budget for Feb 2018 – Forecast $-222.6B, versus $49.0B previous.

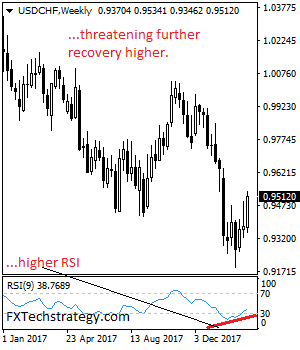

USDCHF – Looks To Strengthen Further On Correction

USDCHF - With the pair retaining its recovery pressure the past week, more gain is likely. On the downside, support lies at the 0.9450 level. A turn below here will open the door for more weakness towards the 0.9400 level and then the 0.9350 level. On the upside, resistance resides at the 0.9550 level where a break will clear the way for more strength to occur towards the 0.9600 level. Further out, resistance comes in at the 0.9650 level. Above here if seen will turn attention to 0.9700. All in all, USDCHF faces further downside pressure.