Sample Category Title

Dollar Confined in Range, Loonie to Look into CPI

Outlook in the forex markets remain basically unchanged. Dollar is trading as the strongest major currency for the week. However, it remains bounded in recent range against others. Current rebound is viewed as a corrective move and there is no change in the bearish down trend yet. Yen and Sterling are following as the second and third strongest. Meanwhile, commodity currencies are trading broadly lower. In particular, Canadian Dollar is broadly pressured after yesterday's weak retail sales data. The loonie will turn to CPI release today for more guidance.

Fed Kaplan: Three hikes a reasonable base case

Dallas Fed Robert Kaplan said that the tax cut may deliver "too much of a good thing" as fiscal stimulus". And, it's "wise" to take back some of the monetary accommodation. He believed three rate hikes year is a "reasonable" base case. Nonetheless, that could change if employment and inflation developments exceed his expectations.

ECB Smets: FX volatility a point of attention

ECB Governing Council member Jan Smets said that the "volatility on the foreign exchange markets remains a point of attention" fro the central bank. Nonetheless, he emphasized that the strength of Euro is not as problem as long as it's supported by fundamentals. He added that "only if, as we said last time after our monetary policy meeting in Frankfurt, this volatility becomes excessive, when certain levels are breached because of overshooting, because of a devaluation policy to increase competitiveness, can problems occur."

Most Analysts saw USD/JPY best at 110-114

According to a Reuters poll between February 16-22, 22 out of 34 economists expected BoJ to keep interest rate at zero throughout 2018. Most expected BoJ to keep year yield target at zero this year. 28 out of 36 expected the central bank to keep ETF purchase at around JPY 6T while 8 expected the amount to be cut later this year or afterwards. Regarding the exchange rate, 20 of 34 saw USD/JPY at 110-114 as optimal for the economy. 8 saw 105-109 while 3 said 115-119. Another three said 120 or above.

On the data front

New Zealand retail sales rose more than expected by 1.7% qoq in Q4. Japan national CPI core was unchanged at 0.9% yoy in January, corporate service price rose 0.7% yoy. German GDP final and Eurozone CPI final will be the main feature in the European session. Canadian CPI will be the focus later in the day.

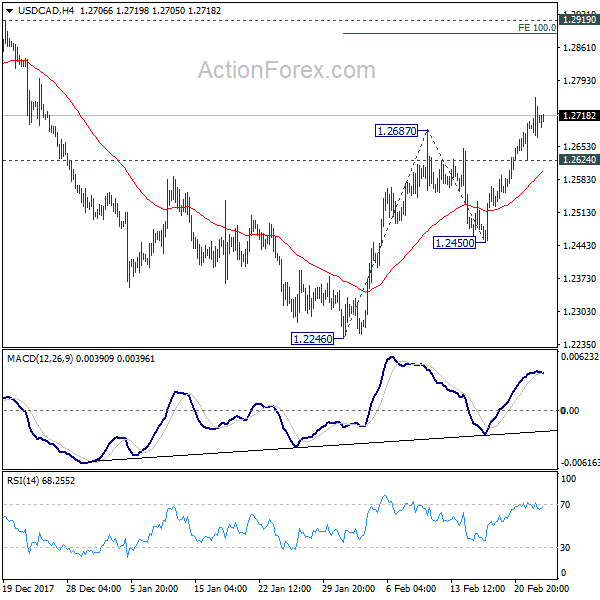

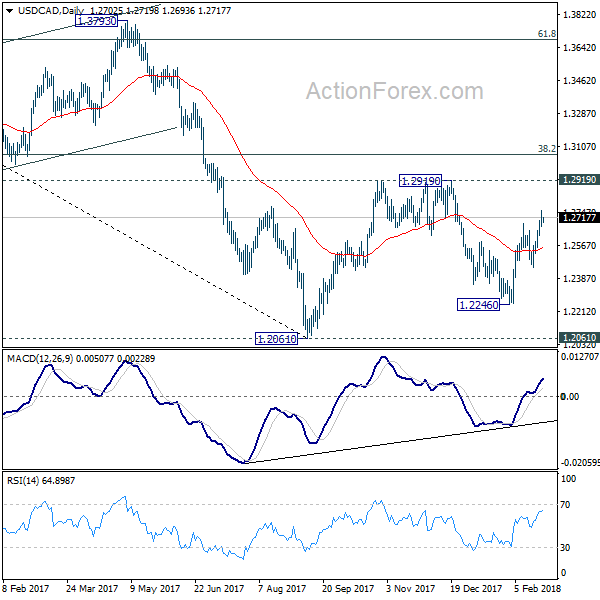

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2667; (P) 1.2709; (R1) 1.2748; More....

Intraday bias in USD/CAD remains on the upside as rebound from 1.2246 would target 100% projection of 1.2246 to 1.2687 from 1.2450 at 1.2891, which is close to 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2624 minor support will turn intraday bias neutral first. But further rally would be mildly in favor as long as 1.2450 support holds.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2776), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Ex Inflation Q/Q Q4 | 1.70% | 1.30% | 0.20% | 0.30% |

| 23:30 | JPY | National CPI Core Y/Y Jan | 0.90% | 0.80% | 0.90% | |

| 23:50 | JPY | Corporate Service Price Y/Y Jan | 0.70% | 0.80% | 0.80% | |

| 7:00 | EUR | German GDP Q/Q Q4 F | 0.60% | 0.60% | ||

| 10:00 | EUR | Eurozone CPI M/M Jan | -0.90% | 0.40% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Jan F | 1.30% | 1.40% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan F | 1.00% | 1.00% | ||

| 13:30 | CAD | CPI M/M Jan | 0.50% | -0.40% | ||

| 13:30 | CAD | CPI Y/Y Jan | 1.50% | 1.90% | ||

| 13:30 | CAD | CPI Core - Common Y/Y Jan | 1.60% | |||

| 13:30 | CAD | CPI Core - Median Y/Y Jan | 1.90% | |||

| 13:30 | CAD | CPI Core - Trim Y/Y Jan | 1.90% |

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2667; (P) 1.2709; (R1) 1.2748; More....

Intraday bias in USD/CAD remains on the upside as rebound from 1.2246 would target 100% projection of 1.2246 to 1.2687 from 1.2450 at 1.2891, which is close to 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2624 minor support will turn intraday bias neutral first. But further rally would be mildly in favor as long as 1.2450 support holds.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2776), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

USD/JPY Is Facing Tough Challenge On Upside

Key Highlights

- The US Dollar recovered recently, but it failed to move above the 107.90 resistance against the Japanese Yen.

- There is a major bearish trend line forming with current resistance at 107.40 on the 4-hours chart of USD/JPY.

- The pair is under bearish pressure and it may perhaps retest the 106.00 support.

- The US Initial Jobless Claims for the week ending Feb 17, 2018 declined from the last revised reading of 229K to 222K.

USDJPY Technical Analysis

Earlier this week, the US Dollar started a recovery and moved above 107.00 against the Japanese Yen. However, the USD/JPY pair could not break the 107.90-108.00 resistance and moved down.

Looking at the 4-hour chart, the pair failed to trade above a major bearish trend line with current resistance at 107.40. The pair traded as high as 107.94 and is currently moving lower.

It traded below the 23.6% Fib retracement level of the last wave from the 105.54 low to 107.94 high. It seems like the pair is under pressure and it could extend the current downside move.

It already tested the 50% Fib retracement level of the last wave from the 105.54 low to 107.94 high. Therefore, if it breaks the 106.70 support level, it could move back towards the 106.00 support.

On the upside, an initial resistance is around 107.20. However, the most important hurdle for buyers is near the bearish trend line with current resistance at 107.40. As long as the pair is below 107.40, it may remain in a negative zone.

Recently, the US Initial Jobless Claims for the week ending Feb 17, 2018 was released by the US Department of Labor. The market was looking for no change in the claims from 230K.

However, the actual result was better, as there was a decline in claims to 222K. Moreover, the last reading was revised down to 229K.

The report added:

The previous week’s level was revised down by 1,000 from 230,000 to 229,000. The 4-week moving average was 226,000, a decrease of 2,250 from the previous week’s revised average. The previous week’s average was revised down by 250 from 228,500 to 228,250.

Overall, the US Dollar seems to be struggling to gain upside momentum. USD/JPY must break the 107.40 level to start a fresh upside recovery.

Market Morning Briefing: The Euro-Yen Saw A Low Near 131.30

STOCKS

Dow (24962.48, +0.66%) moved up sharply about 166 points yesterday, contrary to our expectation of testing lower levels of 24500-24000. Overall trade within 25500-24500 region looks possible in the coming sessions.

Dax (12461.91, -0.07%) has dipped lower in line with our expectation. A test of 12300 is possible on the downside before the index again starts to inch upwards targeting 12600 in the medium term. Overall the index is likely to remain range bound.

Nikkei (21814.31, +0.36%) is trading higher contrary to our expectation of a test of support near 21200-21000. As mentioned earlier, the index now has some scope on the upside towards 22500 while above 21000. Near term looks bullish.

Shanghai (3279.52, +0.34%) breaks above 3260/70 levels mentioned yesterday and could now be headed towards 3300-3350 in the early sessions next week. Near term is likely to be bullish.

Stability around the support levels on both Nifty (10382.70, -0.14%) and Sensex (33819.50, -0.07%) is retained just now but the immediate supports re unable to produce a sharp bounce from current levels. Could this indicate an eventual break below current levels in the near to medium term? Maybe. An end in the current stable and range bound trade would lead to some sharp movement on either direction. While immediate supports lacks strength, our preference would be on the downside.

COMMODITIES

WTI (62.81) and Brent (66.34) have risen sharply and are trading higher today. A report from the EIA states that the crude oil inventories at 420.5mln barrels are in the lower half of the seasonal average and is likely to stimulate optimism. The prices could see a rise today followed by some dip in the next week.

As mentioned yesterday, 1320 is an important near term support for Gold (1329) and while that holds, Gold is likely to move back towards 1350-1360 levels in the near term. A break below 1320 if seen and sustains, could be vulnerable for the metal increasing chances of testing 1315-1310 by end of next week.

Copper (3.22) is likely to trade in the 3.15-3.30 region for the near term.

FOREX

The Dollar Index (89.836) after testing resistance on daily candles near 90.1-90.2 yesterday didn’t rise to test higher resistance on weekly candles near 90.3-90.4.The Dollar Index has ranged between the broad 88.,5-90.5 zone for the last 3 weeks and if the same ranging continues next week, downside target could be support on daily and weekly candles near 88.25-88.50. The EU CPI data release later today and the US Consumer Confidence and US GDP data release next week could be further market movers for the major currencies next week.

Euro (1.2318) saw a low near 1.226 yesterday and tested lower support near 1.2275-1.2265 on the daily candles (which was also seen as crucial support on weekly candles). We had written about chances of a false break of support on weekly candles towards 1.221-1.223, but that didn’t take place, and the Euro is now seeing a bounce. It has been ranging in the broad 1.22-1.255 zone for the last 3 weeks and if the ranging continues, we could again see a test of 1.25 sometime late next week.

The Dollar-Yen (106.89) has dipped from resistance near 107.9-108.0 on the daily candles and could again move down towards 105.5 – seen as support on weekly candles. Yesterday we wrote about the Dollar Yen having seen 4 continuous weeks of upmove on the last 2 occasions when it tested support on weekly candles. It is now looking less likely that the same will get repeated, as the Dollar Yen could continue to stay bearish over the next 1-2 weeks.

The Euro-Yen (131.68) saw a low near 131.30 yesterday and is now trading at levels near 131.6-131.8 indicating that a bounce might be underway. Strength in Euro towards 1.24 and in Yen towards 106 would mean that the Euro yen stays above support on daily candles near 131.30.

Pound (1.3953) saw a low of 1.3857 yesterday but now seems to be bouncing from support on daily candles near 1.39. There is still some possibility of it moving down again next week towards lower support near 1.38 – seen both on daily and 3 day candles.

Dollar-Rupee (65.045): The near-term outlook (one-three days) is unclear. Equal chances of rise towards 65.20 and of fall towards 64.90-80-70.

INTEREST RATES

US 10 Year Yield (2.9335), US 30 year Yield (3.2179), US 5 year yield (2.6687), US 2 year yield (2.254) : As the US bond auctions continue, all 4 yields continue to hover around their long term resistances. There has been a slight dip in the 10 Year yield from yesterday’s highs near 2.95%, which might indicate that there could be a further dip below 2.9% next week.

As mentioned yesterday as well, after this week’s volatility in yields, we might well see another few sessions of consolidation next week. A decisive breach of long term resistances towards 3% for the 10 Year yield still looks to be few weeks away.

(Long term resistance levels for the 4 yields earlier mentioned are as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively - we have been expecting these levels to hold in this month.)

Japan 10 year yield (0.05%) has come down towards 0.05% after seeing highs near 0.095% in late Jan, reflecting the fact that investors might be moving towards Japanese bonds in these times of volatility.

EURUSD – Remains Bearish, Extends Weakness

EURUSD - With the pair continuing to retain its downside pressure, more weakness is envisaged. On the upside, resistance comes in at 1.2350 level with a cut through here opening the door for more upside towards the 1.2400 level. Further up, resistance lies at the 1.2450 level where a break will expose the 1.2500 level. Conversely, support lies at the 1.2250 level where a violation will aim at the 1.2200 level. A break of here will aim at the 1.2150 level. Below here will open the door for more weakness towards the 1.2100. All in all, EURUSD faces further bear threats on correction.

Possible Inverse Head And Shoulders On The Kiwi

As shown on the daily chart below, the Kiwi / US pair is displaying a potential Inverse Head & Shoulders continuation pattern that has been developing over the past 6 months. Not only does this signify that the correction could be coming to end, but it presents a potential opportunity for significant upside gains.

A sustained break from the neckline resistance at approximately 0.7435 would confirm the breakout and potentially offer a trade with an upside target area of around 0.8000.

Generally speaking, there are a couple of ways a trader could play this setup – by buying a solid breakout of the neckline, or buying the potential re-test of the breakout area.

I’m keeping an eye on this and remain on the sidelines until I see confirmation of the Inverse H&S pattern on the Kiwi.

24 Hours Of Reconciliation

24 hours of reconciliation

It took all of 24 hours for the results of the rationality test to kick in after traders took time to the read the minutes from Wednesday. Not a heck of a lot has changed in the Feds view. The minutes were far more balanced than the equity market sell-off suggested. The discussions about their inflation target being symmetric indicate that the Feds are less concerned about the updraft from inflationary pressures than current market pricing. Overall there were few if any significant hawkish shift and traders have started to nimbly re-engage the US dollar downside not waiting until Powell’s key Humphrey Hawkins testimony which should clear up more than a few policy concerns.

The Feds will raise interest rates in March on the back of two strong inflation prints post-January meeting, but the market remains comfortably parked in the three rate hike camp for 2018.

This new Fed Chair will be as data dependent as his predecessor so, in reality, no one knows for sure what the Feds will do other than hike somewhere between two and four times in 2018.

Bond Markets

The bond markets continue to trade from a bear market bias, and this is unlikely to change anytime soon given the burdening supply issues which are compounded as the Feds delicately and gingerly pull back on QE largess.

Stock Markets

US equity market rebounded as concerns over rising US interest rates abate. If you were confused by Wednesday 50 pips downside adventure on the S&P post-FOMC minutes, you were not alone. However, until the dust is settled on the Fed policy debate, we should expect more back and forth ahead of Jerome Powells Humphrey Hawkins testimony.

Oil markets

Oil market bid was boosted by DoE inventories which saw a draw of -1.616 million barrels which far better than consensus and more profound than the -.9mn print by the API. While the market continues to communicate concern over rising levels of shale production, this bullish inventory data coupled with a slightly softer USD profile, it’s easy to see why oil prices are finding fresh session highs going into the NY close.

Gold Markets

Gold continues to act as less of a haven hedge and more as a proxy for USD sentiment. Given the greenback is trading within a restricted range as the stage is getting prepared for new Chair Jerome Powell, gold will remain supported by the $ 1324-25 levels given the markets ubiquitous bias to sell the USD. But the topside should also stay in check as most traders will opt to only aggressively re-engage in USD downside after Powell clears the policy airwaves in his Humphrey Hawkins testimony.

The Japanese Yen

No need to jump the gun, today’s CPI data will be a crucial driver in JPY sentiment. Post data comments to follow.

The Euro

Fact of fiction, the Euro remains a point of contention, but topside conviction remains low ahead of the Italian election compounded by softer EU economic data.

The Malaysian Ringgit

The USDMYR landscape is a bit muddled, and this air of uncertainty could extend, more so if opinion on the soft dollar narrative become less reliable. Rising US interest rates and the markets growing sensitivity to local economic data presents some near-term challenges for the Ringgit. Ultimately we believe that US rates are in the process of topping but until we get a definitive signal from the New Fed chair, hopefully, next week, we should expect offshore flows to remain light in the short run.

None the less the Ringgit is getting support from higher oil prices and given we are far removed from the USDJMYR 4.0 danger zone, longer-term investors should continue to look for opportunistic levels to re-engage long MYR posting

The Chinese Yaun

Markets in China return from a week-long holiday only to discover the US has initiated another anti-dumping probe.. This time for rubber bands. Certainly sounds more bark than the bit, but non the less trade war discussion is picking up.

Continue to favour a constructive view on the Yuan given the markets negative USD bias. But he RMB complex will most certainly benefit from expected bond inflows which should accelerate as we move through 2018.

Gold Gains Ground, Puts Brakes On Dollar Rally

Gold has posted gains in the Thursday session, erasing the losses seen on Wednesday. In North American trade, the spot price for an ounce of gold is $1331.17, up 0.50% on the day. On the release front, unemployment claims dropped to 222 thousand, well below the estimate of 230 thousand.

Gold prices remain continue to fluctuate. The base metal has lost 1.3% this week, erasing much of last week’s gains. Concerns that strong US numbers could stoke inflation and more rate hikes sparked the recent turbulence in global stock markets. This has triggered volatility in gold, as gold prices are sensitive to moves (or expected moves) in interest rates. The Fed is currently projecting three rate hikes this year, but if inflation continues to move upwards, many analysts are expecting that the Fed could press the rate trigger four, or even five times in 2018.

The Federal Reserve released the minutes of its January meeting, and as expected, the benchmark rate was left unchanged at a rate between 1.25% and 1.50%. The message from policymakers was that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers “anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further”. At the December meeting, the Fed penciled in three rate hikes in 2018, and there was no reference to a quicker pace of hikes in the January minutes. As for inflation, the minutes did not reveal any concern. Most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent.

GBP/USD – Pound Shrugs Off Soft GDP Report

The British pound has posted slight gains in the Thursday session. In North American trade, GBP/USD is trading at 1.3943, up 0.18% on the day. On the release front, British Second Estimate GDP for the fourth quarter remained unchanged at 0.4%, shy of the estimate of 0.5%. Preliminary Business Investment for Q4 dropped to 0.0%, missing the estimate of 0.5%. In the US, unemployment claims dropped to 222 thousand, well below the estimate of 230 thousand.

British GDP for Q4 was a disappointment, but the pound has managed to hold its own against the dollar. GDP was revised downwards to 0.4%, down from 0.5% in the initial estimate. Looking at growth for all of 2017, GDP was revised lower from 1.8% to 1.7%, its worst showing since 2012. The weak readings are being attributed to lower production and weaker consumer spending. Consumers are being squeezed by a weaker British pound as well as high inflation, which is running at a 3% clip, compared to the BoE target of 2%.

The Bank of England has been hinting that it could accelerate the pace of rate hikes, and this was further reinforced on Wednesday, as BoE Chief Economist Andy Haldane said that interest rates might need to climb faster than previously expected, in order to bring down inflation to the BoE’s target of 2 percent. The Bank has been reluctant to raise rates in order to lower inflation, but may be running out of options, as inflation hovers at 3 percent and continues to erode the purchasing power of consumers. The Bank has taken pains to be transparent with the markets, stating recently that the pace of rate hikes could be accelerated and larger hikes than previously forecast could be on the way.

USD/JPY – Dollar Falls To 107 Yen, Japanese Inflation Reports Next

The Japanese yen has recorded considerable gains in the Thursday session. In North American trade, USD/JPY is trading at 107.03, down 0.68% on the day. On the release front, US unemployment claims dropped to 222 thousand, easily beating the estimate of 230 thousand. In Japan, the focus will be on inflation indicators, with the release of National Core CPI and the Services Services Producer Price Index. Both indicators are expected to post gains of 0.8%.

The Federal Reserve released the minutes of its January meeting, and as expected, the benchmark rate was left unchanged at a rate between 1.25% and 1.50%. The message from policymakers was that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers “anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further”. At the December meeting, the Fed penciled in three rate hikes in 2018, and there was no reference to a quicker pace of hikes in the January minutes. As for inflation, the minutes did not reveal any concern. Most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent.

The Bank of Japan has been holding a steady course with monetary policy, and we can expect more of the same with the re-election of Governor Harohiko Kuroda to a second 5-year term. The move is also a clear message from the BoJ that it is no rush to make any change to the massive stimulus program, a key component of Abenomics. Kuroda has made it a priority to raise inflation, but this has proven a daunting task, as inflation is still below of the BoJ’s inflation target of 2%. In this period of strong volatility in the currency markets, Kuroda’s re-election may have a calming effect on the markets. The yen has jumped 5.0% in 2018, and if the rise continues, policymakers will have to consider further easing in order to curb the yen’s value and protect the export sector, which has improved due to stronger global demand.