Sample Category Title

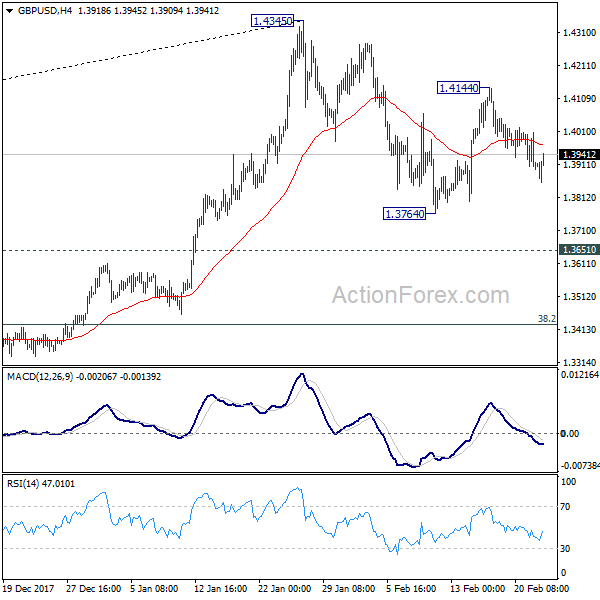

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3876; (P) 1.3942; (R1) 1.3981; More....

Intraday bias in GBP/USD remains neutral as it's bounded in range of 1.3764/4144. On the upside, break of 1.4144 will extend the rebound from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5105). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

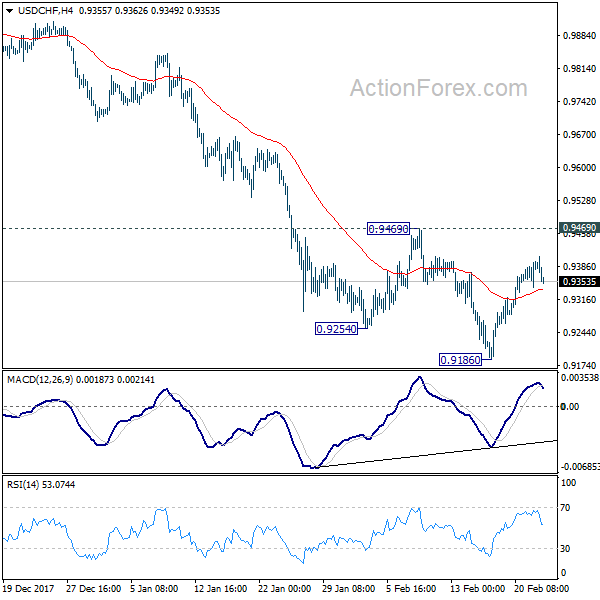

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9356; (P) 0.9376; (R1) 0.9410; More...

No change in USD/CHF's outlook. Rebound form 0.9186 is seen as a corrective move. Intraday bias remains neutral and outlook stays bearish for another decline. Break of 0.9186 will extend the larger down trend to 0.9115 medium term projection level next. However, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9541) and above.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 107.39; (P) 107.64; (R1) 108.03; More...

USD/JPY's recovery was limited well below 108.27 and struggled to sustain above 4 hour 55 EMA. Nonetheless, it's staying in range above 105.54. Intraday bias remains neutral first. As noted before, price action from 105.54 are seen as a corrective move and outlook stays bearish. Break of 105.54 will extend the larger fall from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 107.72 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48. now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

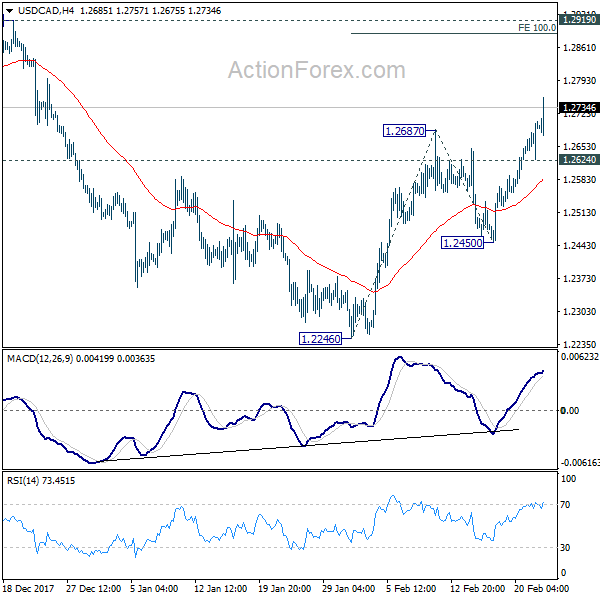

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2650; (P) 1.2676; (R1) 1.2728; More....

USD/CAD's rally continues to as high as 1.2757 so far today and intraday bias remains on the upside. Rebound from 1.2246 should be targeting 100% projection of 1.2246 to 1.2687 from 1.2450 at 1.2891, which is close to 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2624 minor support will turn intraday bias neutral first. But further rally would be mildly in favor as long as 1.2450 support holds.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2776), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Canadian Dollar Dives after Retail Sales, Dollar Struggles to Extend Gains Elsewhere

Canadian Dollar drops sharply in early US session after terrible weak retail sales data. Headline retail sales dropped -0.8% mom in December versus expectation of -0.1%. Ex-auto sales were even worse by dropping -1.8% mom, versus expectation of 0.0%. On the other hand, Dollar continues to struggle to extend post FOMC minutes gains despite solid job data. Initial jobless claims dropped -7k to 222k in the week ended February 17. Continuing claims dropped -73k to 1.88m in the week ended February 10. USD/CAD jumps after the releases and is on course towards 1.29 near term resistance zone. However, Dollar is staying below near term resistance against other major currencies, thus, maintaining bearish outlook.

Fed Bullard" A bunch of hikes will turn policy restrictive

St. Louis Fed president James Bullard tried to tame speculations of faster rate hike by Fed this year. He said in an interview that four rate hike this year would be "priced for perfection". And, "the idea that we need to go 100 basis points in 2018, that seems like a lot to me." He emphasized that for that to happen "everything would have to go just right". That is, "the economy would have to surprise on the upside a bunch of times during the year." And he's "not sure that's a good way to think about 2018." Bullard added that "a bunch of hikes this year Fed policy will turn restrictive" as "the neutral fed funds rates is pretty low."

On the other hand, Fed Governor Randal Quarles said in a speech that "after assessing the recent data, my take is that the current shortfall in inflation from target as most likely due to transitory factors that will fade through 2018, pushing inflation back up to target". And, "Against this economic backdrop, with a strong labor market and likely only temporary softness in inflation, I view it as appropriate that monetary policy should continue to be gradually normalized."

ECB minutes: Premature to change communication

Minutes of January ECB meeting showed that "changes in communication were generally seen to be premature at this juncture, as inflation developments remained subdued despite the robust pace of economic expansion." Nonetheless, ECB did acknowledge that Inflation expectations in the ECB Survey of Professional Forecasters (SPF) for the first quarter of 2018 showed average inflation expectations of 1.5 percent, 1.7 percent and 1.8 percent for 2018, 2019 and 2020 respectively. Compared with the previous survey round, this represented upward revisions of 0.1 percentage point for 2018 and 2019." Also, "longer-term market-based measures of inflation expectations had increased further, in line with the gradual upward trend observed since the middle of 2017."

German Ifo: Dipped but not change in underlying trend

German Ifo business climate dropped to 115.4 in February, down from 117.6, below expectation of 117.0. Expectation gauge dropped to 105.4, down from 108.3, missed consensus of 107.9. Current assessment gauge dropped to 126.3, down from 127.8, below consensus of 127.0. Ifo president Clemens Fuest said that "companies were less satisfied with their current business situation, but the indicator was at its second highest level since 1991." And, the data "signals economic growth of 0.7 percent in the first quarter." Ifo economist Klaus Wohlrabe said that "I would not yet speak of a change in the underlying trend, the German economy is still doing very well, but some of the steam has been let off."

Released from UK, Q4 GDP growth was revised lower to 0.4% qoq. Index of services rose 0.6% 3mo3m in December. CBI reported sales dropped to 8 in February.

Abe advisor urges BoJ to buy foreign bonds

In Japan, Prime Minister Shinzo Abe's Koichi Hamada urged BoJ Governor Haruhiko Kuroda to "consider having the BOJ buy foreign bonds." Hamada is an emeritus professor of economics at Yale University. The idea is pushed forward by academics. In particular, at this stage of the quantitative and qualitative easing program, BoJ could be running out of domestic assets to buy. Purchase of foreign bonds from financial institutions could give them Yen cash. Such funds could be loaned out to companies and households as cheap money, to spur growth and inflation.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2650; (P) 1.2676; (R1) 1.2728; More....

USD/CAD's rally continues to as high as 1.2757 so far today and intraday bias remains on the upside. Rebound from 1.2246 should be targeting 100% projection of 1.2246 to 1.2687 from 1.2450 at 1.2891, which is close to 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2624 minor support will turn intraday bias neutral first. But further rally would be mildly in favor as long as 1.2450 support holds.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2776), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 09:00 | EUR | German IFO Business Climate Feb | 115.4 | 117 | 117.6 | |

| 09:00 | EUR | German IFO Expectations Feb | 105.4 | 107.9 | 108.4 | 108.3 |

| 09:00 | EUR | German IFO Current Assessment Feb | 126.3 | 127 | 127.7 | 127.8 |

| 09:30 | GBP | GDP Q/Q Q4 P | 0.40% | 0.50% | 0.50% | |

| 09:30 | GBP | Index of Services 3M/3M Dec | 0.60% | 0.50% | 0.40% | |

| 11:00 | GBP | CBI Reported Sales Feb | 8 | 14 | 12 | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (17 FEB) | 222K | 231K | 230K | 229K |

| 13:30 | CAD | Retail Sales M/M Dec | -0.80% | -0.10% | 0.20% | 0.30% |

| 13:30 | CAD | Retail Sales Ex Auto M/M Dec | -1.80% | 0.00% | 1.60% | 1.70% |

| 15:00 | USD | Leading Index Jan | 0.70% | 0.60% | ||

| 15:30 | USD | Natural Gas Storage | -194B | |||

| 16:00 | USD | Crude Oil Inventories | 1.8M |

Futures Flat After Hawkish Fed Minutes

The rebound in equity markets appears to have lost some momentum, with European stocks trading in the red again on Thursday and US futures flat ahead of the open.

US stock markets have recovered quite well after falling more than 10% a couple of weeks ago but the recovery appears to have stalled in recent days. Around two thirds of the losses had been recovered by Tuesday but a couple of negative sessions has left indices more than 5% off their highs and with more work to do. Indices still appear vulnerable to further shocks and the prospect of more aggressive tightening by the Fed may trigger it.

The minutes from the January meeting, like the statement that accompanied it, were quite hawkish and pointed to at least three rate hikes this year. While this is now strongly priced in – more than 50% – there is potential for a fourth and more again next year, something that appears to be worrying investors and shaking confidence in equity markets.

Sterling Lower After Mixed GDP Data

There was some disappointing data from the UK this morning, as growth figures for the fourth quarter were revised down to 0.4% on a quarterly basis and 1.4% on an annual basis. The data triggered some volatility in the pound which is once again lower on the day against the dollar, euro and yen, despite the Bank of England's clear desire to continue raising interest rates.

The pound has performed very well in recent months as Brexit negotiations moved on to phase 2 and the central bank raised interest rates and signalled an intention to continue to do so gradually. Policy makers certainly struck a hawkish tone in yesterday's inflation report hearing, although that did little to support sterling which would suggest this has now been priced in. With negotiations over the transition period likely to dominate the next month, the pound could be vulnerable to downside shocks if talks risk breaking down, something that will likely play on the mind of traders.

Bitcoin Sell-Off May Not Be Over

Bitcoin continues to be a volatile as ever, having almost double in price in two weeks since bottoming around $6,000 on 6 February. It now finds itself testing $10,000 from above, a level that is providing some support in the near term. Sentiment remains extremely fragile in cryptocurrencies and I'm not convinced it's yet recovered from what was a nasty sell-off around the turn of the year.

A break back above $12,000 would suggest that confidence is returning to the space but I would expect any upside gains to be more gradual than we saw last year. The euphoria that accompanied last year's gains has subsided quite a bit and traders are likely to approach this a lot more cautiously, with many having been burned during the decline.

USD/CAD Ticks Lower, Canadian Retail Sales Next

The Canadian dollar has recorded small losses in the Thursday session. Currently, USD/CAD is trading at 1.2684, down 0.15% on the day. On the release front, Canada releases retail sales reports. The markets are expecting soft numbers, with an estimate of 0.1% for Core Retail Sales and 0.0% for Retail Sales. In the US, unemployment claims is expected to remain unchanged at 230 thousand. On Friday, Canada releases a host of CPI indicators, led by CPI.

The Federal Reserve released the minutes of its January meeting, and as expected, the benchmark rate was left unchanged at a rate between 1.25% and 1.50%. The message from policymakers was that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers "anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further". At the December meeting, the Fed penciled in three rate hikes in 2018, and there was no reference to a quicker pace of hikes in the January minutes. As for inflation, the minutes did not reveal any concern. Most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent.

The week started on a sour note for Canadian indicators, as Wholesales Sales declined 0.5%, short of the estimate of 0.4%. It marked the first decline in three months. The markets are expecting another soft release from Core Retail Sales, a key barometer of consumer spending. The indicator posted a strong gain of 1.6% in December, but is forecast to slow to just 0.1% in January. If the retail sales reports miss their estimates, the Canadian dollar could lose more ground. The Canadian dollar is under pressure, and has shed 1.0% so far this month.

Euro Edges Up ahead of ECB Meeting Minutes; European Stocks Ease

Here are the latest developments in global markets:

FOREX: The dollar index deviated below ten-day highs reached earlier in the day, but remained 0.12% up on the day, last seen at 90.07. Yesterday, the Fed meeting minutes spurred hopes that the Fed will hike rates four times this year, giving some lift to the dollar. Dollar/yen was struggling to gain ground, trading at 107.23 (-0.44%) as the weakness in stock markets continued to falter on the pair, with investors looking for safer assets. Pound/dollar extended losses towards 1.3817 following a downward revision in Q4 GDP growth initial estimates, while euro/dollar managed to rebound to 1.2288 (+0.07%) despite February's German Ifo business climate index dropping to the lowest level seen since September. Aussie/dollar and kiwi/dollar moved higher to 0.7825 (+0.25%) and to 0.7332 (+0.20%) respectively, while dollar/loonie inched down to 1.2682 (-0.13%).

STOCKS: The majority of the stocks traded in Europe opened lower on Thursday pressed by speculation that the Fed could raise interest rates faster than expected. Disappointing GDP growth revisions in the UK and weaker a German Ifo business confidence index added further pressure to the markets, while upbeat earnings releases failed to provide support. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.55% and 0.62% respectively at 1100 GMT, with all sectors being in the red except healthcare and utilities. The German DAX 30 dropped by 0.62%, the French CAC 40 declined by 0.29%, while the British FTSE 100 tumbled by 0.86%. The Spanish IBEX 35 was up by 0.22% driven by gains in Telecommunications after Spain's Telefonica expressed its optimism on revenues and profitability this year. US stock futures were mixed.

COMMODITIES: Oil prices held weak during early European trading as a surprise decline in US crude inventories was unable to lift the weigh arising from a rising dollar. WTI crude was down by 0.66% at 61.28/barrel and Brent slipped by 0.44% to $65.13/barrel. In precious metals, gold was flat at $1323.30/ounce.

Day ahead: ECB meeting minutes in focus; Canadian & New Zealand retail sales eyed; Japan reports on inflation

The calendar will be relatively busy in the remaining of the day with the US, Canada, New Zealand and Japan, reporting on economic figures, while the European Central Bank (ECB) is scheduled to release minutes regarding its latest policy meeting on January 25.

The ECB is expected to submit its accounts of its January's meeting at 1230 GMT, with investors looking for clues on whether central bankers have discussed any plans on the quantitative easing program after the asset purchase program expires in September 2018. Unless the ECB alters its policy language or uses strong statements on the exchange markets, the minutes are less likely to cause substantial moves on the euro in contrast to the December's accounts which lifted the common currency after the ECB signaled a hawkish shift to its communication stance in early 2018.

In the US, the Department of Labor will publish readings on initial jobless claims for the week ending February 16. The number of people applying for unemployment benefits for the first time is forecasted to rise by 230,000 as in the preceding week, holding below the threshold of 300,000 which is associated with a healthy labor market.

Staying in the US, the Energy Information Administration (EIA) will give its weekly updates on US oil inventories at 1600 GMT. Analysts believe that US crude oil inventories have grown at a slower pace of 1.795 million barrels in the week ending February 16 compared to 1.841 seen in the previous week. Refineries such as gasoline and distillates are said to decline.

Elsewhere, growth in Canadian retail sales might hold steady, with analysts projecting the measure to expand by November's pace of 0.2% month-on-month, whereas the core measure which excludes automobiles is seen weaker at 0.3%, far below the previous mark of 1.6%. New Zealand will also report on retail sales at 2135 GMT but forecasts, in this case, are more positive.

In Japan, figures on consumer prices will be available at 2330 GMT but the core CPI - the Bank of Japan's (BoJ) preferred inflation measure - could continue undershooting the BoJ's target of 2.0%.

Regarding today's public appearances, the New York Fed President William Dudley - a permanent FOMC voting member - will be participating in an economic briefing on the impact of hurricanes Irma and Maria in Puerto Rico and the Virgin Islands at 1500 GMT. Atlanta's Fed President Raphael Bostic - a voting FOMC member in 2018 - will be speaking on Banking at 1710 GMT, while the Dallas Fed President Robert Kaplan - a non-voting FOMC member in 2018 - will be participating in a Q&A session on NAFTA at 2030 GMT.

The British Prime Minister and the Cabinet will gather at Chequers today to discuss on Brexit and limit any differences between on the issue ahead of a May's crucial speech in front of EU ministers next week.

DAX Slips As German Ifo Business Climate Falters

The DAX index has posted strong losses in the Thursday session. Currently, the index is trading at 12,366.50 down 0.82% since the Wednesday close. On the release front, German Ifo Business Climate dipped to 115.4, short of the estimate of 117.1 points. This marked the lowest level since September. Later in the day, the ECB releases the minutes of its January policy meeting. On Friday, Germany releases Final GDP and the eurozone publishes Final CPI.

German and eurozone confidence and manufacturing indicators pointed downwards this week, and the euro has responded with a soft week, losing 1.0 percent. The well-respected ZEW economic sentiment reports dropped in February in Germany and the eurozone, although both indicators managed to beat their estimates. Eurozone consumer confidence remains weak, and the indicator dipped to zero, shy of the forecast of 1 point. On the manufacturing front, eurozone and German PMIs both fell in February and missed the forecasts. At the same time, both releases pointed to strong expansion, a reflection of strong global demand for European products.

With the recent stock market turmoil over fears of more rate hikes, the Federal Reserve minutes were highly anticipated. As expected, the benchmark rate was left unchanged at a rate between 1.25% and 1.50%. The message from policymakers was that further rate hikes could be in the cards, due to strong economic conditions in the US. In the words of the minutes, policymakers "anticipated that the rate of economic growth in 2018 would exceed their estimates of its sustainable longer-run pace and that labor market conditions would strengthen further". At the December meeting, the Fed penciled in three rate hikes in 2018, and there was no reference to a quicker pace of hikes in the January minutes. As for inflation, the minutes did not reveal any concern. Most Fed members were of the opinion that inflation would rise towards the Fed target of 2 percent.

UK GDP Disappoints, Dollar firms While Oil Remains Shaky

Sentiment towards the Pound was dealt a blow on Thursday, after Britain's Gross Domestic Product growth in the final quarter of 2017 was unexpectedly revised down.

The Office for National Statistics reported that the UK economy grew just 0.4% in Q4 of 2017; down from the 0.5% preliminarily estimate last month. Annual growth for 2017 was also revised down from 1.8% to 1.7%. While today's disappointing GDP report is unlikely to derail the Bank of England from its current hawkish path, it could raise fresh questions amongst investors over Britain's economic outlook this year. These questions may breed uncertainty, consequently leaving the Pound vulnerable to further losses.

Taking a look at the GBPUSD, a strengthening Dollar has instilled bears with enough inspiration to drag the currency pair below 1.3900. Repeated weakness below the 1.3900 level could encourage a decline towards 1.3850 and potentially lower.

Dollar climbs on hawkish FOMC minutes

Dollar bulls were in the building on Wednesday evening after January's hawkish FOMC meeting minutes reinforced market expectations over higher US interest rates this year.

The Federal meeting minutes showed optimism over the economic outlook with policymakers increasingly optimistic about inflation eventually reaching the 2% target. A key takeaway from January's meeting minutes was how a majority of Fed members agreed that recent "strengthening of the economy increased the likelihood of further gradual rate increases". Bullish investors warmly welcomed the hawkish remarks with the Dollar Index jumping towards 90.20 on Thursday morning. From a technical standpoint, the Dollar Index has the potential to challenge 90.55 following the daily close above 90.00.

Commodity spotlight - WTI Oil

It is interesting how oil prices edged lower on Thursday morning, despite the American Petroleum Institute on Wednesday reporting an unexpected drawdown in US Crude inventories.

There is a strong possibility that the primary culprit behind oil's recent decline could be a strengthening US Dollar amid prospects of higher US interest rates. While some may argue that WTI Crude remains supported by OPEC's commitment to tighten markets, price action seems to suggest otherwise as bears linger in the background. With fears mounting over surging production from US Shale potentially sabotaging efforts by OPEC to tackle the oversupply glut, oil prices remain exposed to downside risks.

Investors will direct their attention towards the Energy Information Administration's (EIA) inventory data this afternoon, to see whether US production continues to rise. A build in inventories has the ability to fuel the oversupply fears consequently punishing WTI Crude. Focusing on the technical picture, WTI could tumble towards $60 if bears are able to secure a solid daily close below $61. Alternatively, a breakout above $61.80 could invite an incline higher towards $62.50.

Currency spotlight - EURUSD

The Euro edged slightly lower against the Dollar on Thursday ahead of the anticipated ECB Monetary Policy Meeting Accounts, scheduled for release this afternoon.

Euro bulls could receive a welcome boost if the accounts offer fresh insight into the central bank's thoughts on quantitative easing and inflation. Focusing on the technical picture, the EURUSD is coming under noticeable pressure on the daily charts, thanks to a strengthening Dollar. Repeated weakness below the 1.2300 level could encourage a decline towards 1.2180. Alternatively, a breakout back above 1.2300 may invite an inline towards 1.2350 and 1.2440, respectively.