Sample Category Title

‘Coalition of the Willing’ Boosts Euro and European Stock Futures

The meeting between US President Trump and Ukrainian President Zelensky didn’t go as planned—no mineral deal was signed, and the talks ended in a clash. In contrast, Zelensky’s meeting with UK Prime Minister Starmer was more productive. Starmer urged European companies to form a ‘coalition of the willing’ to support Ukraine with military aid and security guarantees. Later, Macron announced plans to pursue a one-month truce.

Overall, tensions between the two continents have worsened. Oil prices initially rose in early Asian trading amid concerns that the Trump-Zelensky conflict could delay any path to lasting peace. However, selling pressure outweighed geopolitical risk perception, as last Friday’s US economic data fueled concerns about slowing growth—Atlanta Fed's GDPNow tanked to -1.5%!

The EURUSD started the week on a positive note after slipping below its 50-day moving average on Friday.

The European will to stand with Ukraine means more military spending. Increased defense spending from the ‘coalition of the willing’ should provide a short-term economic boost but also accelerate technological advancements in the medium to long run. The whole situation is a wake-up alarm for the sleeping European beauty.

On the budget side, higher spending also means increased borrowing, which could push European yields higher. The latter doesn't impact optimistic mood among investors this monday morning with DAX futures leading gains. Appetite for the European defense stocks will certainly remain solid. Gold has given back early session gains, while the US dollar is broadly softer even against the Loonie although the US is supposed to go ahead with 25% tariffs on Mexican and Canadian imports, while levies on Chinese products would be doubled to 20%.

Speaking of China, the CSI and HSI kicked off the week on a negative note despite a stronger-than-expected Caixin data that suggested the manufacturing activity in China grew faster than expected in February. Chinese bubble tea giant Mixue made a strong debut in Hong Kong trading—something to take your mind off geopolitics for a moment.

On the data front

Friday’s economic data was bitter-sweet. The core PCE index, the Federal Reserve’s (Fed) favourite gauge of inflation, came in line with expectations. But the combination of higher-than-expected personal income but lower-than-expected – and unexpectedly negative - spending growth in January raised worries regarding US growth prospects. On top, Atlanta Fed’s GDPNow forecast tanked to -1.5% from above 2% printed previously. As such, the US growth expectations are deteriorating – and they are deteriorating fast. The latter could boost the dovish Fed expectations – which could be an encouraging development for risk appetite – but for the Fed to go ahead with further support to the economy, inflation should remain under control. And with tariffs due to materialize starting from this month, controlling inflation won’t be a walk in the park.

Anyway, this week, the market will focus on January employment numbers. A consensus of analyst expectations on the latest Bloomberg survey suggests that the US economy may have added 156K nonfarm jobs in January and slightly slower wages growth. Investors will also be looking at the impact of mass firings at the federal government offices in the coming months. Soft data is good for boosting Fed doves, pushing the yields lower and improving sentiment in risk assets, but if inflation doesn’t allow, the ‘bad news is good news’ trade could be limited.

In Europe

The geopolitical developments are perceived with optimism among investors on hope that the clash with the US will finally awaken the sleeping European economies, shift focus from financial control to more spending without asking too many questions on whether the extra spending is justified – because it is. In the past, war and military spending have accelerated technology advances and served to the broader economy.

On the trade front, the next step in Trump’s tariff threats is the actual implementation, with levies set to increase. The latter will certainly have a negative impact on growth prospects and call for a decent support from the European Central Bank (ECB) to the underlying economies. Here, as well, the inflation’s trajectory is important to assess the extent to which the ECB could ease financial conditions to boost growth. The CPI updates for February released last week pointed at a mixed picture across the major eurozone countries. But the aggregate CPI update due this morning is expected to print a softening headline and core inflation in February. If that’s the case, the impact on the euro is not certain. In one hand, soft inflation numbers back the expectation of a more dovish ECB stance and could weigh on the euro, but on the other hand, the geopolitical tensions boost growth prospects and the idea that monetary and fiscal support would lead to a stronger growth across Europe – and that’s positive for the euro outlook. The combination of deteriorating growth prospects for the US and improved growth prospects for Europe could help the EURUSD regain confidence and appreciate sustainably beyond the 1.06 mark, the major 38.2% Fibonacci retracement on September to January Trump selloff, and reverse the Trump-led bearish trend.

All Eyes on Russia and Ukraine Peace Plan

In focus today

In the euro area, focus turns to the inflation data for February. As hinted by the national releases (see our what happened over the weekend section), we forecast euro area headline inflation to decline to 2.3% y/y from 2.5% y/y. Most importantly, underlying inflation continued to ease in all countries, with muted monthly price increases and a decline in the yearly growth rates. Services inflation is finally starting to decline due to base effects and lower momentum, and we thus expect euro area core inflation to fall to 2.4 % y/y from 2.7% y/y. We also look out for the final release of the manufacturing PMI for February, which rose more than expected to 47.3 in the flash print.

In the US, focus turns to the ISM Manufacturing index for February released at 16.00 CET. Consensus points to a modest downtick to 50.5 from 50.9 in January. This is in contrast to the flash S&P Manufacturing PMI, which showed an improvement in February. Note that the final release of the S&P-measure will be released at 15:45.

In Sweden, PMI for the manufacturing sector has been in solid territory over the past year with an average of 52.0, and the last print for January was 52.9. While our base case is for a number around that level, we look for any impact of recent jitters around tariffs and the increasing geopolitical tensions. Given the rather weak state of the labour market, we will also look more closely at how the employment sub-index evolved. We will also get the Riksbank Business Survey, which will be an important input for the board ahead of the upcoming March meeting and has been highlighted by Aino Bunge as especially important.

The focus this week will most likely be on geopolitical news - in particular any progress in the Russia-Ukraine peace talks and whether the Trump administration's tariffs imposed on Mexico, Canada and China will be implemented Tuesday. Furthermore, the ECB will convene on Thursday, where we expect them to cut rates by 25bp, while the week is concluded with the US February Jobs Report scheduled for release on Friday.

Economic and market news

What happened over the weekend

In the US, Core PCE was close to expectations at +0.3% m/m (SA), while core services inflation moderated. While this is not exactly a surprise, it is still positive for the Fed to see that the upside surprise in CPI was not repeated in PCE data.

And while spending data for January is subject to residual seasonality, at first glance it is noteworthy that savings rate ticks quite sharply higher to 4.6% (from 3.5%). This causes real household spending volume to decline by 0.5% m/m (SA). It will be interesting to see if weaker consumer sentiment in February translates into further cautiousness in spending.

In the euro area, there were several inflation releases on Friday. German CPI inflation was unchanged at 2.3% y/y in February (consensus 2.3% y/y), but higher than indicated by regional data. In France, HICP inflation fell to 0.9% y/y from 1.8% y/y (consensus 1.1% y/y). Italian HICP rose 1.7% y/y, which was below expectations of a rise to 1.8% y/y (prior 1.7%). Hence, Italian inflation also came in lower like France and Germany.

In Norway, NAV registered labour market report showed an unemployment rate of 2.0% (SA) which is slightly below Norges Bank's forecast of 2.1%. The number of full-time employees fell by 327 people s.a. in February which is clearly considerably better than what other indicators would suggest. Retail sales showed a monthly rise of 1.1% m/m which paints a picture of a slight pick-up in goods consumption towards the end of last year and the beginning of 2025.

The Norges Bank's Q1 expectations survey showed that price and wage expectations are on the decline. Thus, the range for expected wage growth in 2025 is in the range 3.9-4.2%, compared with Norges Bank's estimate of 4.2% from the December monetary policy report.

In Sweden, GDP numbers came in better than expected at 0.8% q/q and 2.4% y/y. The domestic economy also performed better than expected, and consumption ticked up by 0.7% q/q. Thus, we expect consumption to show a more modest increase in Q1 than in Q4.

In China, manufacturing and non-manufacturing activities showed growth in February, with the PMI (NBS) rising to 50.2 and 50.4 respectively, suggesting improved domestic demand. Composite PMI increased to 51.1 in February. Like NBS, Caixin manufacturing PMI increased to 50.8 from 50.3.

Turning to politics, China plans to counter the upcoming US tariffs by targeting American agricultural exports, according to China's state-backed Global Times. The US agricultural sector, with China as its largest market, has historically been prone to being leveraged during trade conflicts.

On the geopolitical front, the UK and France announced they would lead the so-called Coalition of the Willing and work on a ceasefire proposal for Ukraine after the emergency meeting convened by the UK Prime Minister Starmer in London yesterday. They emphasize that for any peace deal to be sustainable, the US needs to be involved and say that signing of the minerals deal is a key priority next. Late in the evening, French PM Macron also proposed a partial one-month ceasefire that would not cover ground fighting. This morning we published a piece about the most recent talks in the Russia-Ukraine war, see Research Global: Arming Ukraine is the cheap option for Europe, 3 March. After the heated Trump-Zelensky exchange in the Oval Office on Friday, it is ever more clear that Europe urgently needs a plan to ensure undisrupted support for Ukraine. We argue that arming Ukraine is by far the cheapest option for Europe, even if it requires that Europe would cover the costs on behalf of the US. We also think the easiest way forward is to work with the so-called Coalition of the Willing instead of pursuing a unanimous EU-wide decision on the matter of confiscating the frozen Russian assets.

In the Middle East, the ceasefire between Hamas and Israel lapsed on Sunday morning after Hamas rejected an updated proposal by Israel regarding the extension of the ceasefire under phase two. As a result, Israeli PM Netanyahu announced that all aid deliveries to Gaza would stop.

Equities: Equities rose on Friday as US markets rallied, closing at their highest point after a late surge in trading. However, this does not alter the fact that equities were lower over the week on a global scale, led by declines in the US and within the tech growth sector. It is also worth remembering that Japan and other Asian markets experienced sharp declines on Friday morning.

Before jumping to conclusions, it is essential to thoroughly review the performance of cross-equities and cross-asset classes. One notable observation is that European equities rose last week, driven by banks, which saw gains of more than 4%. Thus, the initial conclusion is that we are not witnessing a global growth scare. Also, value stocks outperformed growth stocks by 3% last week, which does not align with the message from the bond market, where yields continued to fall, including on Friday.

It is tempting to point to a growth scare in the bond market, drawing parallels to previous episodes. However, the still relatively new US administration plays a significant role here. Again, look at Europe, where the 10-year yield is down "only" 25 basis points from its peak in January compared to the US, where the decline is about 60 basis points. Hence, we are not really seeing a global growth scare.

A final noteworthy observation is the performance of assets such as Bitcoin and Tesla, which surged right after the election but are currently under pressure. This indicates that we are not dealing with a classic growth scare sell-off but rather a policy fear and uncertainty-driven readjustment. US equities on Friday: Dow +1.4%, S&P 500 +1.6%, Nasdaq +1.6%, and Russell 2000 +1.1%. Markets in Asia are playing catch-up this morning despite the looming tariff deadline tomorrow. European futures are also reflecting the strong late-hour performance in the US on Friday, rising by half a percent this morning. US futures are green as well, although not rising as strongly as in Europe.

FI: The decline in US yields continued through Friday's session as US consumer spending weakened significantly in January. The bulk of the move came from the front end of the curve with the 2Y US Treasury yield breaking below the 4% mark. In Europe, rates were relatively flat throughout the session despite a new batch of soft figures on core inflation from Germany and France. The recent string of soft US data has lowered the implied terminal Fed Funds rate from 4% by mid-February to 3.50% as of today. We think the downward correction can proceed a bit longer, as we target a terminal rate of 3-3.25%. However, the rapid repricing seen recently has left US yields more sensitive in the near term to upside data surprises (e.g. on this Friday's NFP) and the ongoing process of delivering an expansionary tax reform.

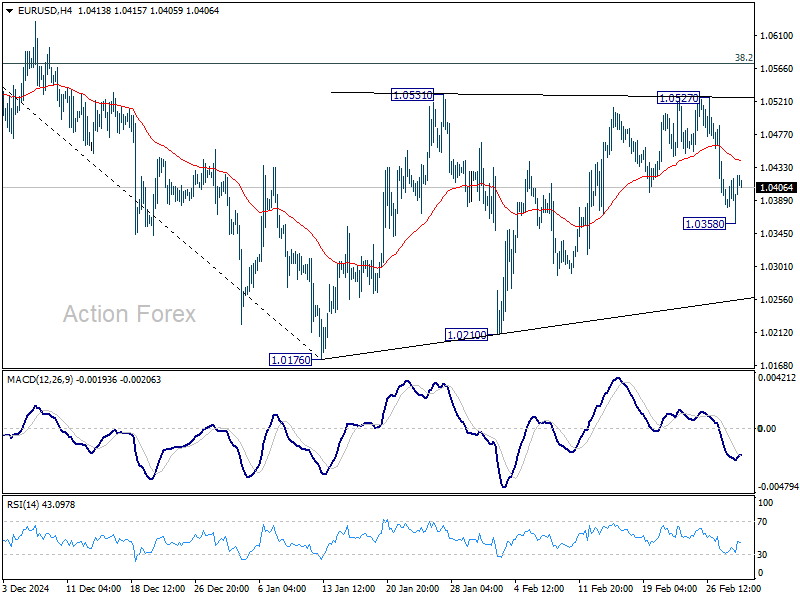

FX: EUR/USD dropped below 1.04 after Trump's tariff tweet last Thursday, which triggered a typical risk-off reaction and a broadly stronger USD - its first weekly gain in a month, also supported by general risk off sentiment. CEE currencies ended the US-session on Friday on a weak footing after Zelensky's visit to the White House took a turn for the worse, halting further immediate progress between the two nations. Closer to home, the market continued to press EUR/DKK FX forwards higher on Friday in anticipation of tighter liquidity conditions at the end of March.

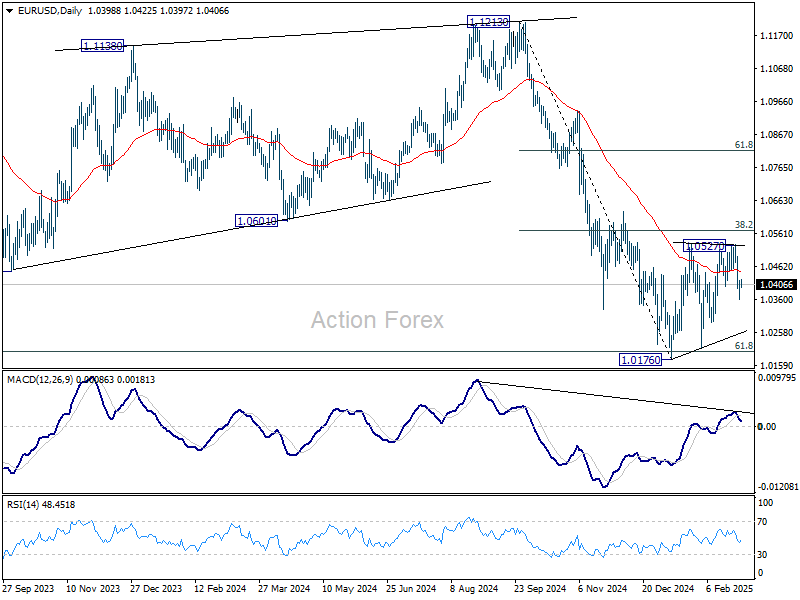

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0350; (P) 1.0385; (R1) 1.0410; More...

Intraday bias in EURUSD is turned neutral first with current recovery. But outlook is unchanged that consolidation from 1.0176 should have completed at 1.0527. Below 1.0358 will target 1.0176/0210 support zone first. Firm break there will resume whole fall from 1.1213, and carry larger bearish implications. Overall outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

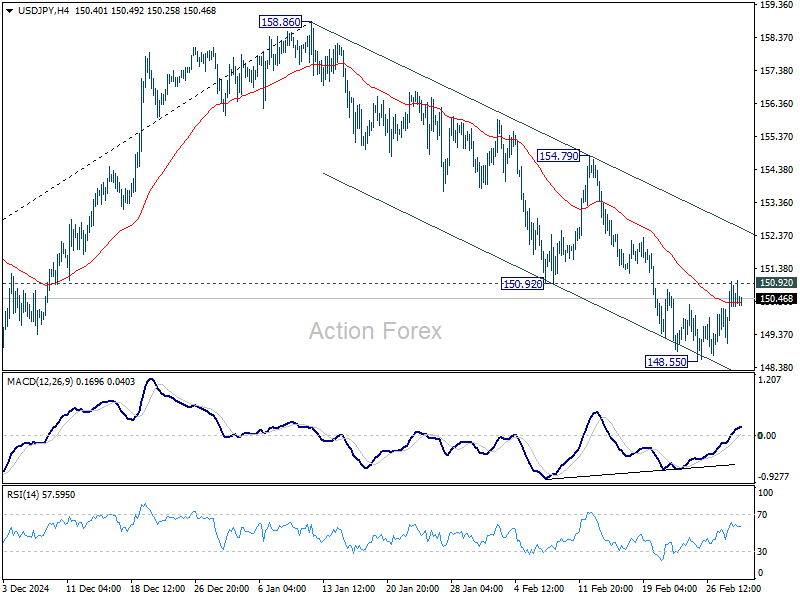

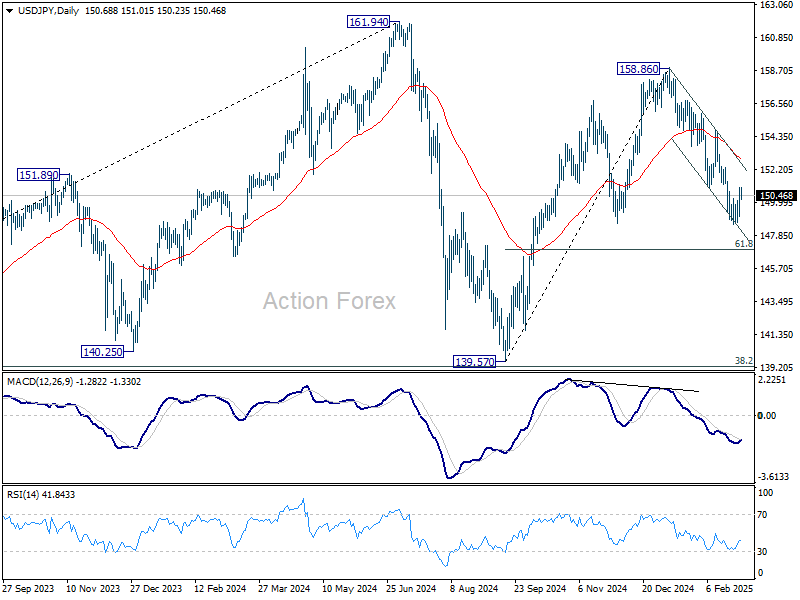

USD/JPY Daily Outlook

Daily Pivots: (S1) 149.49; (P) 150.24; (R1) 151.38; More...

Intraday bias in USD/JPY remains neutral for the moment. Fall from 158.86 is seen as the third leg of the corrective pattern from 161.94 high. Break of 148.55 will target 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, however, break of 150.92 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

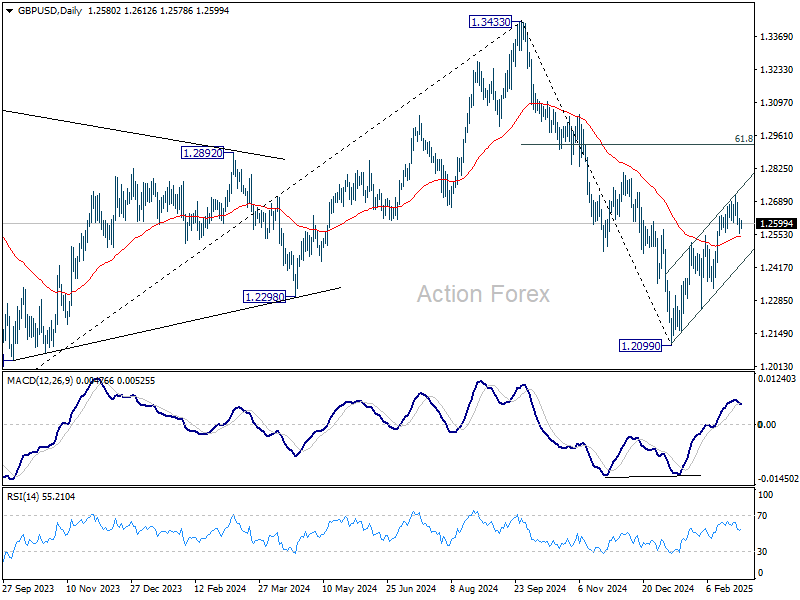

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2549; (P) 1.2585; (R1) 1.2612; More...

Intraday bias in GBP/USD stays mildly on the downside at this point. Fall from 1.2715 short term top would extend to near term rising channel support (now at 1.2439). Sustained break there will indicate that corrective rebound from 1.2099 has already completed. Nevertheless, above 1.2715 will resume the rebound to 1.2810 resistance next.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

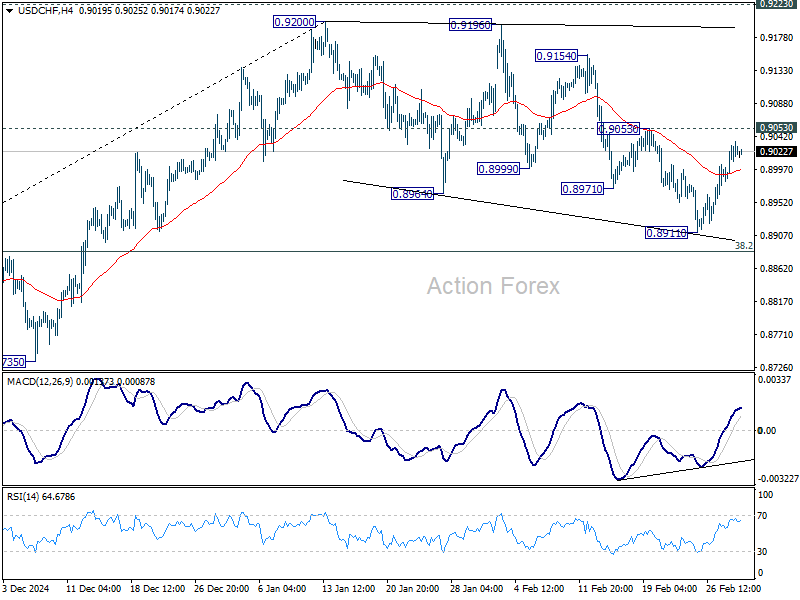

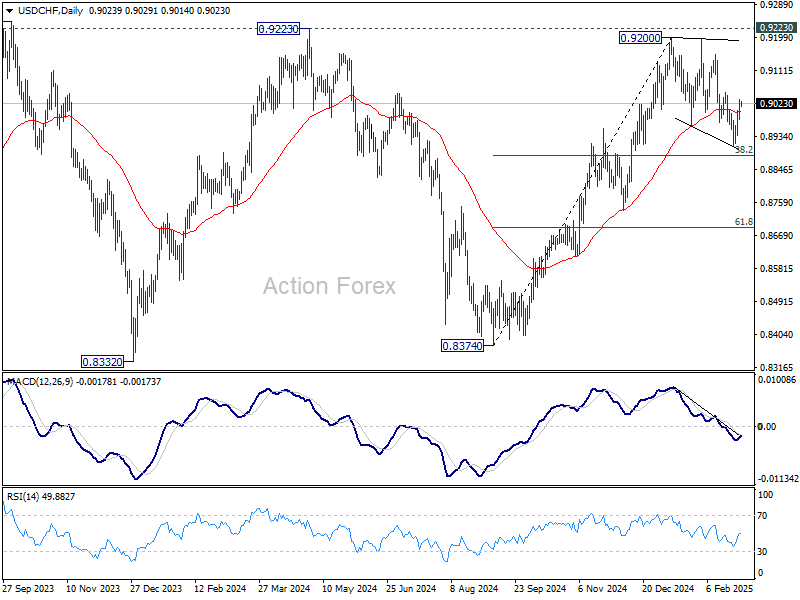

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8996; (P) 0.9017; (R1) 0.9050; More…

Intraday bias in USD/CHF remains neutral for the moment. On the upside, firm break of 0.9053 will suggest that corrective pattern from 0.9200 has already completed at 0.8911. Further rally should then be seen to retest 0.9200 resistance. In case of another fall, downside should be contained by 38.2% retracement of 0.8374 to 0.9200 at 0.8884 to bring rebound.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

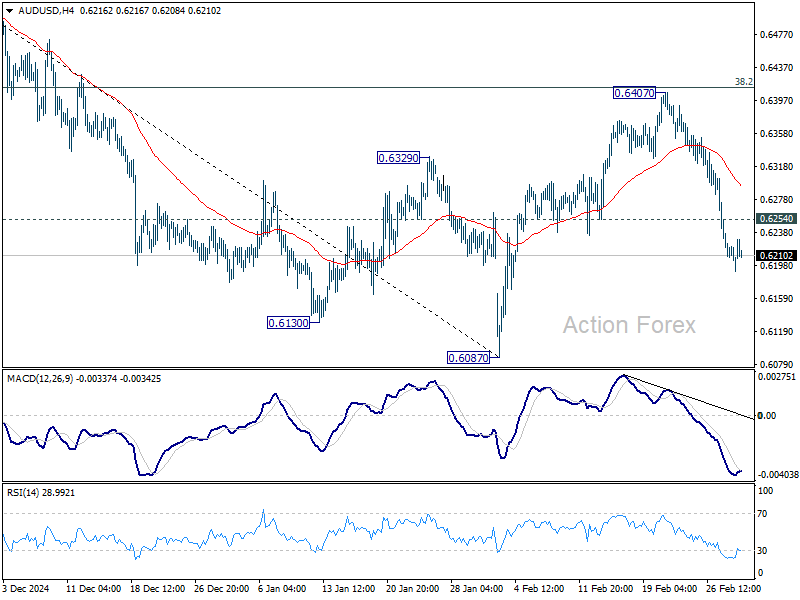

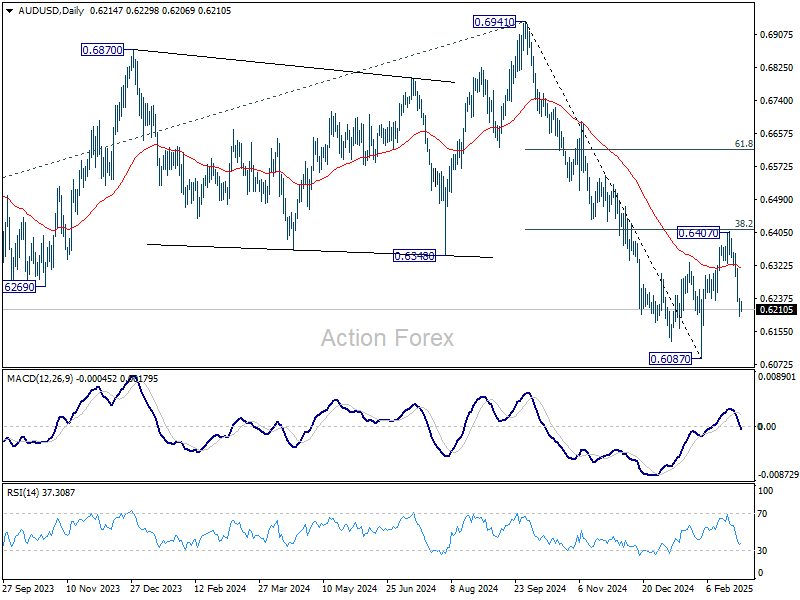

AUD/USD Daily Report

Daily Pivots: (S1) 0.6207; (P) 0.6261; (R1) 0.6291; More...

Intraday bias in AUD/USD stays on the downside at this point. Corrective rebound from 0.6087 should have completed at 0.6407, ahead of 38.2% retracement of 0.6941 to 0.6087 at 0.6413. Deeper fall should be seen for retesting 0.6087 low. Firm break there will resume whole decline from 0.6941. On the upside, above 0.6254 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6494) holds.

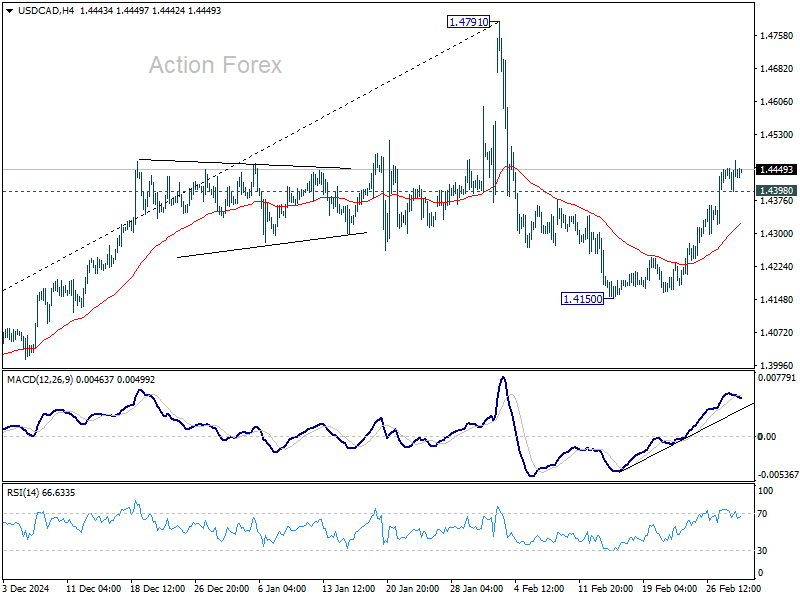

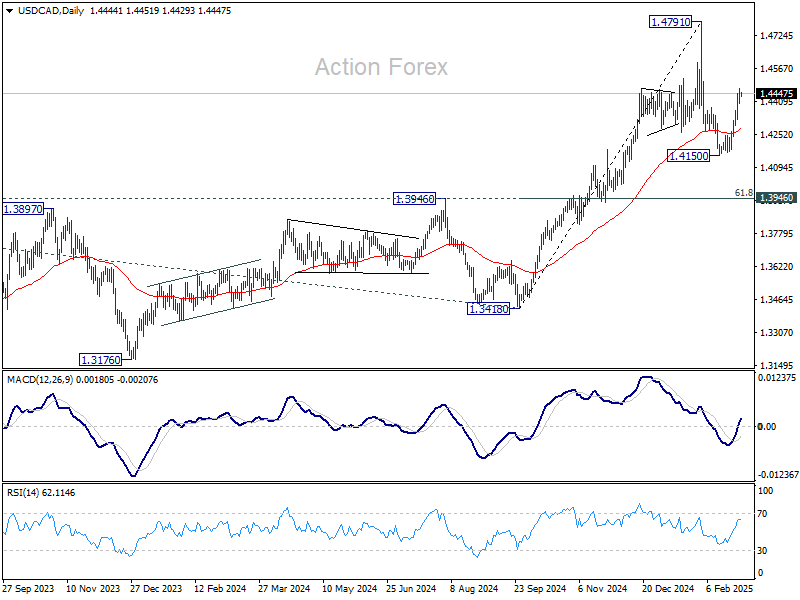

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4420; (P) 1.4446; (R1) 1.4492; More...

Intraday bias in USD/CAD remains on the upside at this point. Corrective pull back from 1.4791 should have completed at 1.4150 already. Further rise should be seen to retest 14791 high. Strong resistance might be seen there to limit upside on first attempt. But decisive break there will confirm resumption of larger up trend. On the downside, below 1.4398 minor support will turn intraday bias neutral again first.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

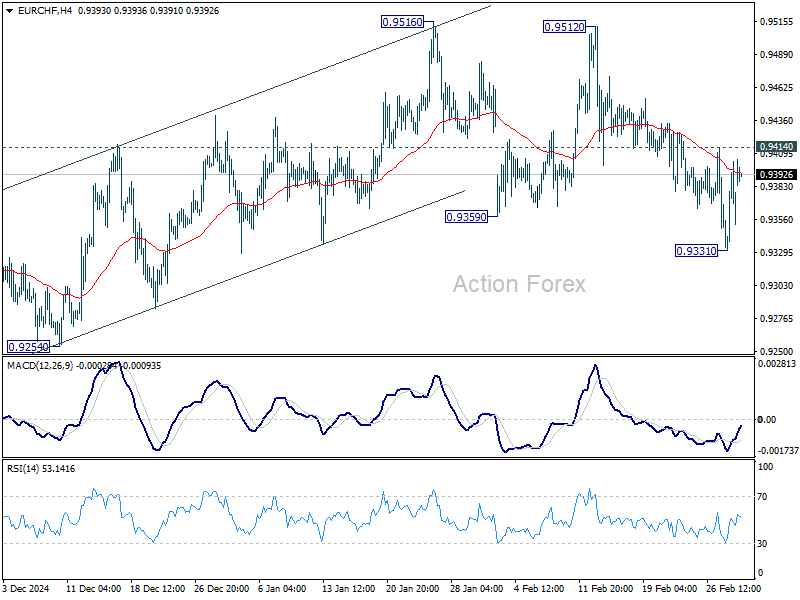

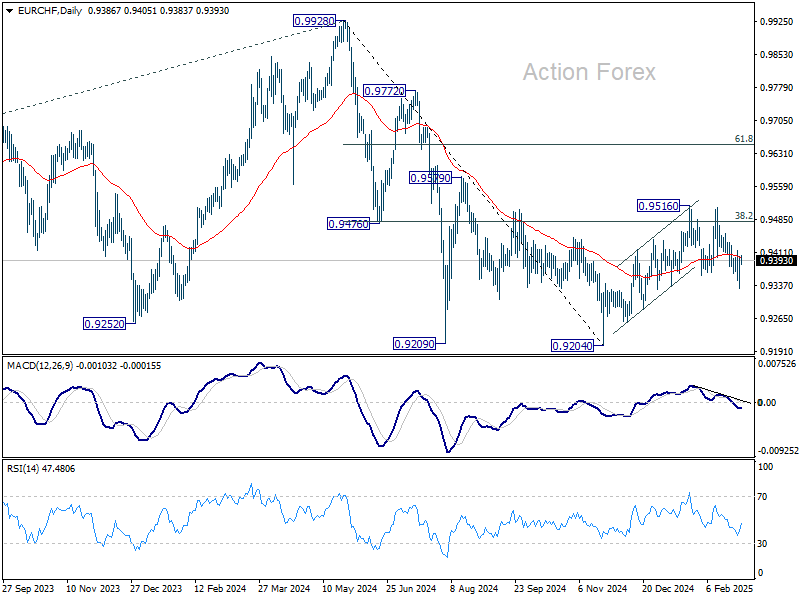

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9333; (P) 0.9369; (R1) 0.9404; More....

Intraday bias in EUR/CHF remains neutral for the moment, but further decline is expected with 0.9414 resistance intact. Corrective rise from 0.9204 could have completed at 0.9516 already. Below 0.9331 will target a retest on this low. However, break of 0.9414 resistance will mix up the near term outlook again.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204 at a later stage.

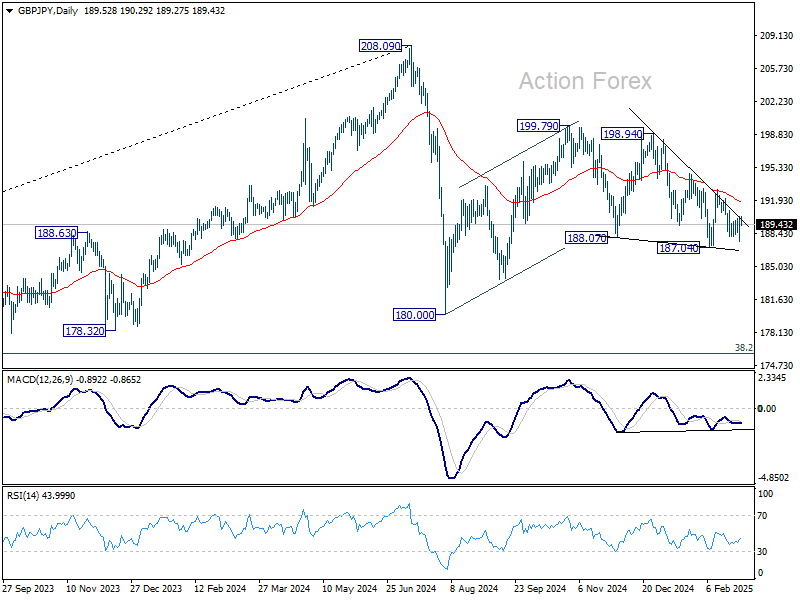

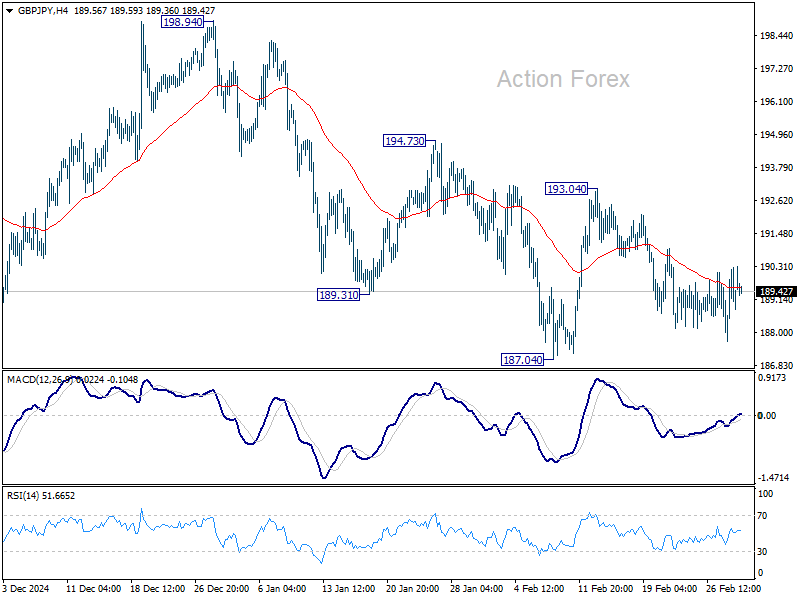

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.00; (P) 189.16; (R1) 190.62; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. Further decline is in favor as long as 193.04 resistance holds. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support. That will also raise the chance that correction from 208.09 is resuming downward.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.