Sample Category Title

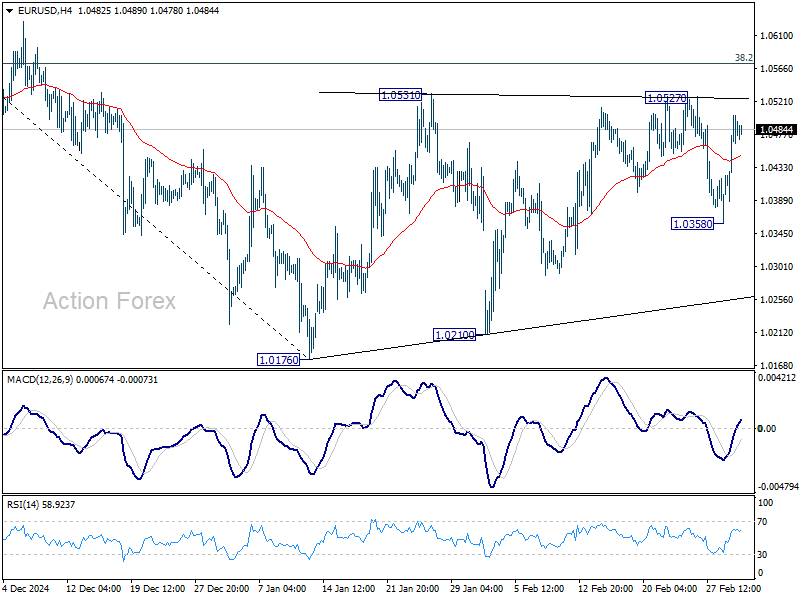

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0417; (P) 1.0461; (R1) 1.0532; More...

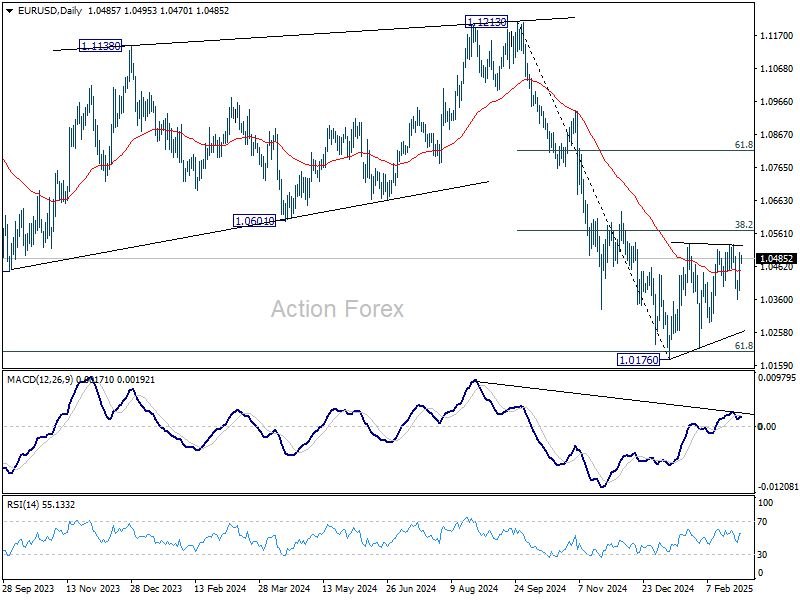

Intraday bias in EUR/USD stays neutral, and outlook remains bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. Below 1.0358 will target 1.0176/0210 support zone first. Firm break there will resume whole fall from 1.1213, and carry larger bearish implications. However, sustained trading above 1.0572 will pave the way to 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

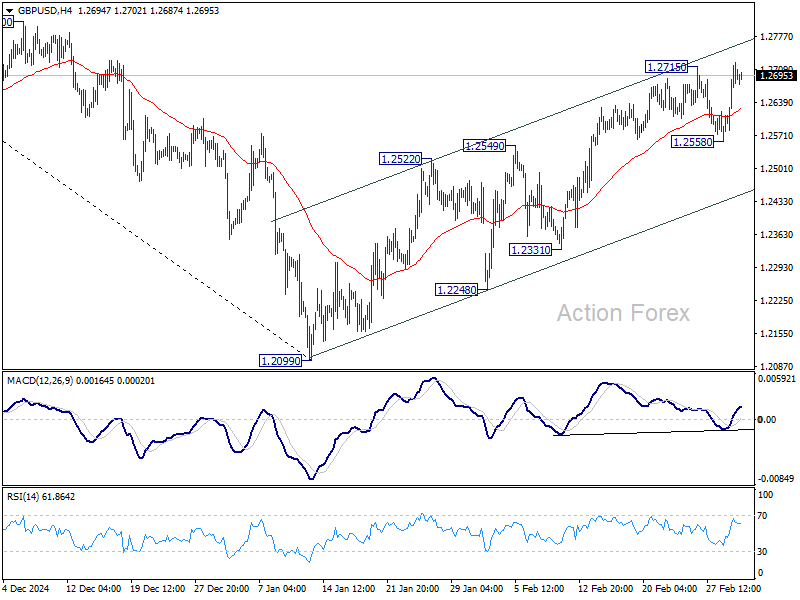

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2614; (P) 1.2669; (R1) 1.2757; More...

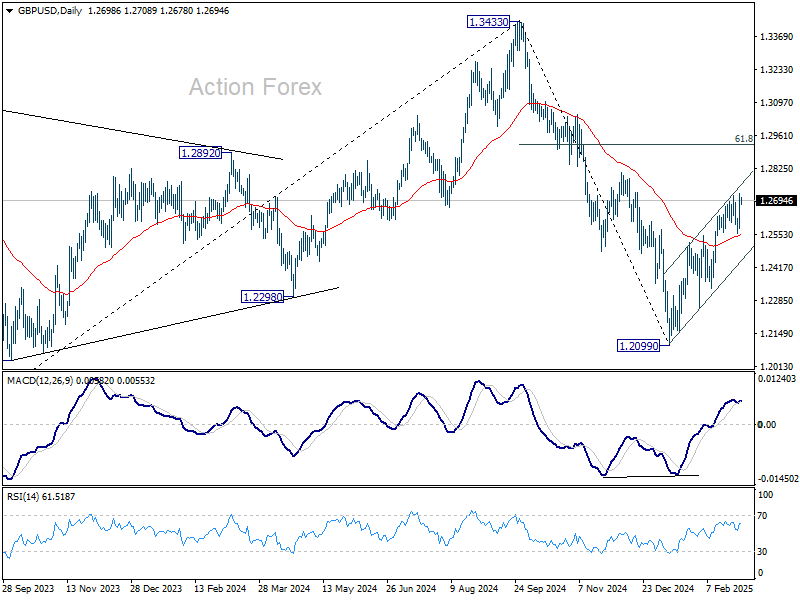

Intraday bias in GBP/USD is back on the upside with breach of 1.2715. Rise from 1.2099 is resuming for 1.2810 resistance. Firm break there will target 61.8% retracement of 1.3433 to 1.2099 at 1.2923. On the downside, break of 1.2558 will turn bias back to the downside for near term rising channel support (now at 1.2453).

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

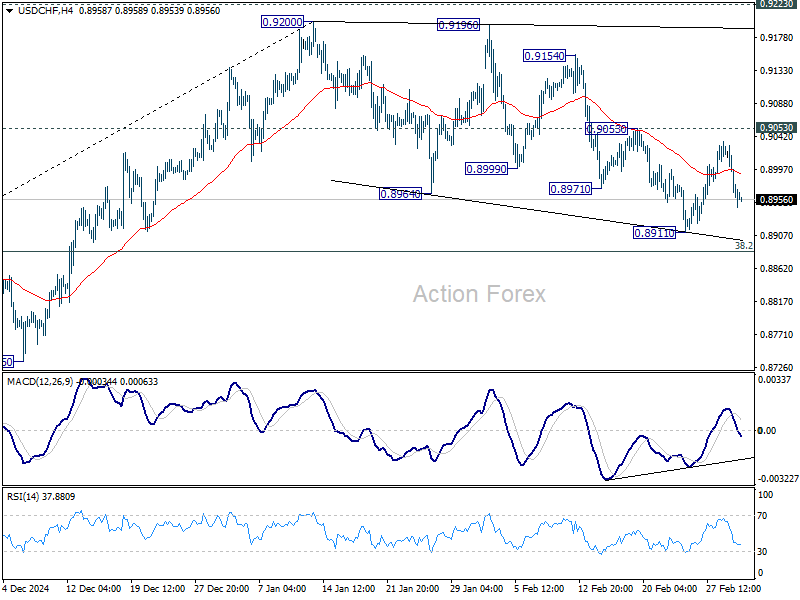

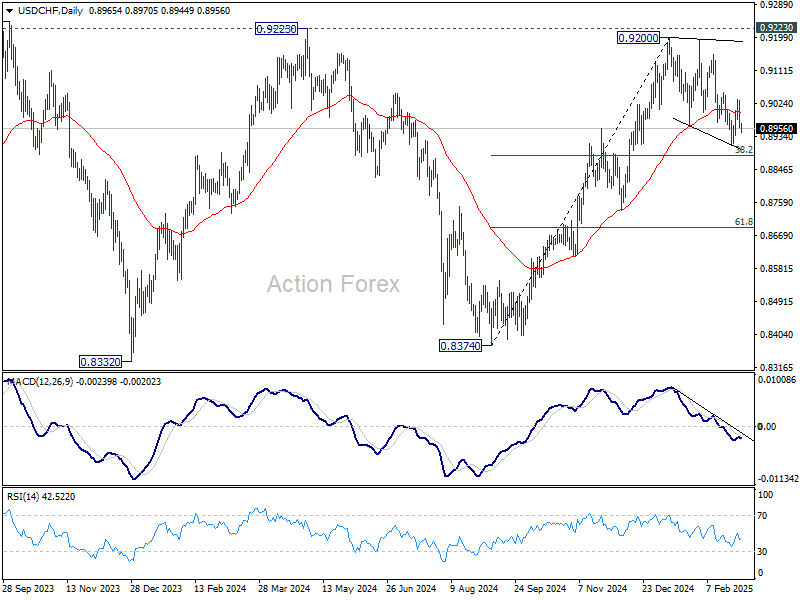

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8941; (P) 0.8987; (R1) 0.9013; More…

Intraday bias in USD/CHF remains neutral and outlook is unchanged. On the upside, firm break of 0.9053 resistance will suggest that corrective pattern from 0.9200 has already completed at 0.8911. Further rally should then be seen to retest 0.9200 resistance. In case of another fall, downside should be contained by 38.2% retracement of 0.8374 to 0.9200 at 0.8884 to bring rebound.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

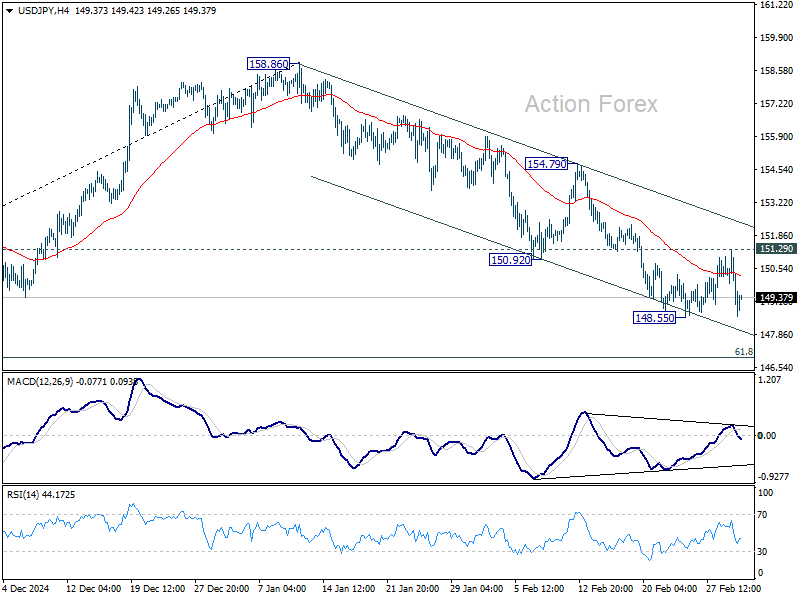

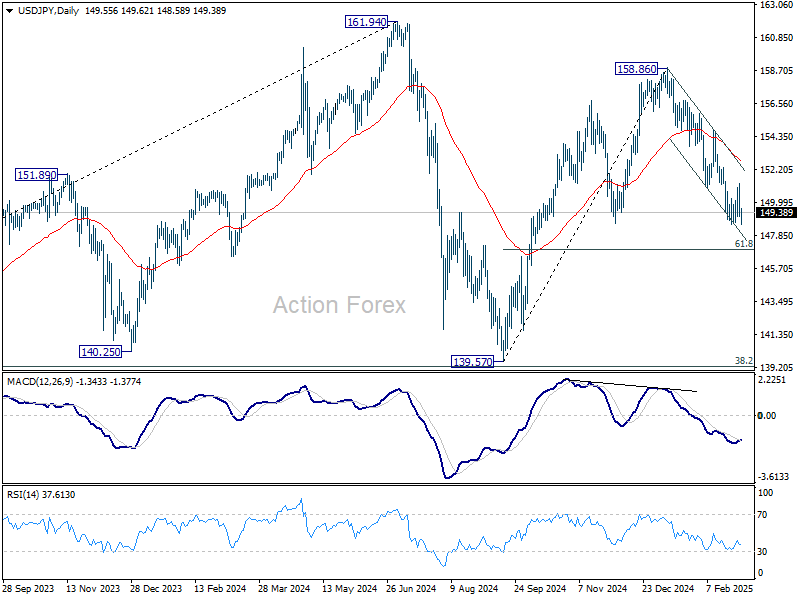

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.63; (P) 149.97; (R1) 150.83; More...

Intraday bias in USD/JPY is turned neutral again as it quickly reversed after recovering to 151.29. Overall outlook is unchanged that the decline from 158.86 is seen as the third leg of the corrective pattern from 161.94 high. On the downside, below 148.55 will resume the fall and target 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, break of 151.29 will delay the bearish case, and bring more consolidations.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Strengthens as Trade War 2.0 Formally Begins, Lifted Further by Trump’s Currency Warning

The latest round of US tariffs on Canada, Mexico, and China officially took effect today, marking the formal start of what many are calling "Trade War 2.0" under US President Donald Trump. Markets had been bracing for impact, and the steep selloff in US stocks overnight confirmed that investors are deeply concerned about the economic fallout. Treasury yields also tumbled, reflecting strong safe-haven flows as traders rushed into bonds amid rising uncertainty.

Despite the sharp risk-off move in the US, the reaction in Asian markets has been uneven. Japan's Nikkei is the only major index experiencing a significant selloff, while other regional markets remain relatively calm. This suggests that investors are still assessing the broader implications of the tariffs before making further adjustments to their positions.

In the currency markets, Yen is currently the strongest performer for the day, benefiting from both risk aversion and falling yields in the US and Europe. Yen's is facing additional upward pressure Trump directly accused Japan of currency manipulation. The US President stated that he had personally called Japanese leader to warn them against devaluing Yen, adding that if such actions continued, tariffs could be the next step to level the playing field for American manufacturers.

Japan wasted no time in responding, with Finance Minister Katsunobu Kato firmly rejecting the accusations. "We are not adopting a policy to weaken the Japanese currency. If you recall our foreign exchange market interventions in recent years, you can understand what I mean," Kato stated in a press conference. This exchange sets the stage for further tensions between Washington and Tokyo, as Japan seeks to defend its monetary policy while avoiding trade tensions with the US.

Elsewhere in the forex markets, the Australian Dollar is the worst performer of the day at this point. While RBA's minutes confirmed that there is no commitment to further rate cuts following last month’s policy reduction, Aussie has been dragged lower by broad risk aversion. Kiwi followed closely behind, and then Loonie.

On the other hand, the Swiss Franc is benefiting from the risk-off sentiment, positioning itself as the second-strongest currency after Yen. Dollar remains resilient, supported by safe-haven demand despite falling treasury yields. Meanwhile, the Euro and Sterling are mixed, still partially bolstered by optimism surrounding the European-led "Coalition of the Willing" and the region’s commitment to increased defense spending.

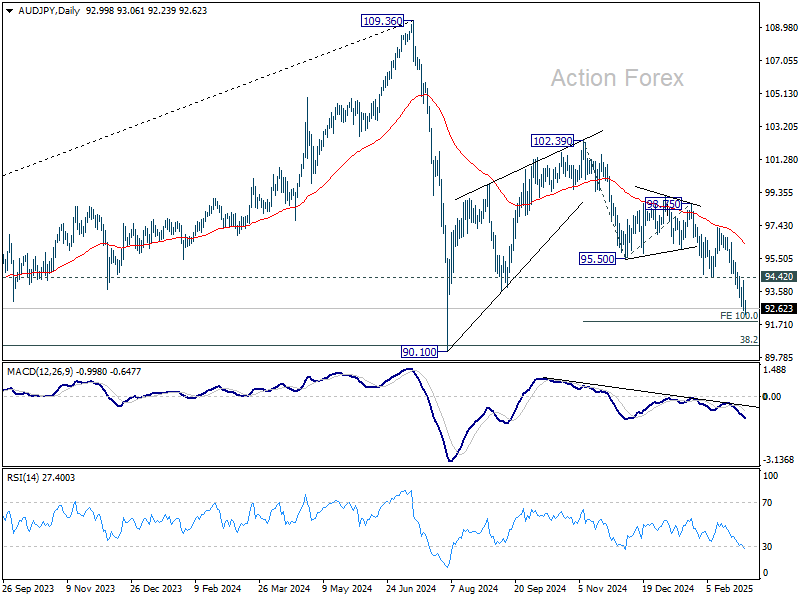

Technically, AUD/JPY's decline from 120.39 is in progress for 100% projection of 102.39 to 95.50 from 98.75 at 91.86, Such decline is currently seen as the second leg of the corrective pattern from 90.10 (2024 low). Hence, momentum should start to diminish below 91.86 while downside should be contained by 90.10 to bring reversal. Break of 94.42 support resistance will be the first sign of short term bottoming. However, sustained break of 90.10 will suggest that fall from 102.39 is indeed resuming the whole down trend from 109.36 (2024 high) as the third leg.

In Asia, at the time of writing, Nikkei is down -1.26%. Hong Kong HSI is down -0.26%. China Shanghai SSE is up 0.15%. Singapore Strait Times is down -0.33%. Japan 10-year JGB yield is up 0.010 at 1.419. Overnight, DOW fell -1.48%. S&P 500 fell -1.76%. NASDAQ fell -2.64%. 10-year yield fell -0.051 to 4.180.

S&P 500 sinks as US tariffs on Canada, Mexico, and China set to begin

US equities tumbled sharply on Monday, kicking off March with the biggest single-day decline in months, and the markets were rattled by the formal commencement of a US-led trade war.

The selloff started in the afternoon after US President Donald Trump reaffirmed that 25% tariffs on imports from Mexico and Canada would go into effect as scheduled on Tuesday. Hopes for a last-minute deal to avert the full imposition of tariffs were dashed. The Federal Register confirmed that the new duties would be officially imposed at 05:01 GMT.

Similarly, the additional 10% duty on Chinese goods was also slated to take effect at the same time, effectively raising the total tariff on thousands of Chinese products to 20%.

In quick response, Canada announced retaliatory measures, with Prime Minister Justin Trudeau confirming that CAD 155B worth of US goods would be hit with 25% tariffs if Trump's levies proceed as planned. China will impose an additional 15% tariff on US imports of chicken, wheat, corn, and cotton. Additionally, a 10% tariff will be applied to sorghum, soybeans, pork, beef, seafood, fruits, vegetables, and dairy. These measures are set to take effect on March 10.

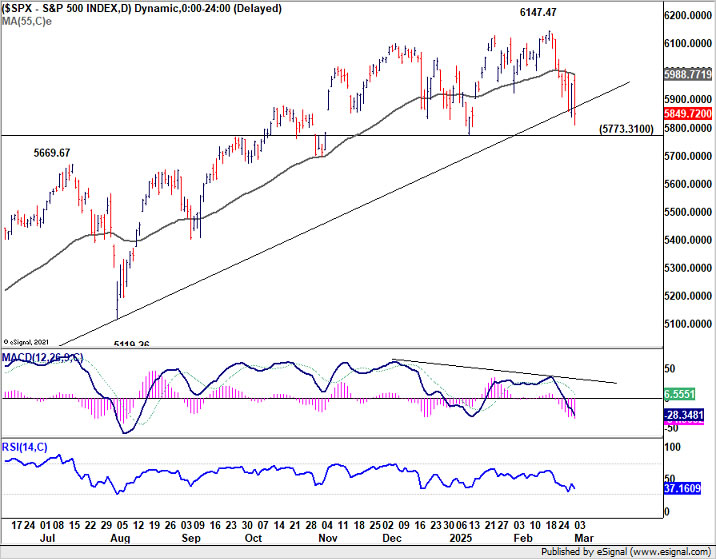

Technically, S&P 500's rejection by 55 D EMA (now at 5988.77) is a near term bearish sign. Immediate focus is on 5773.31 support this week. Considering bearish divergence condition in D MACD, firm break of 5773.31 should confirm medium term topping that 6147.47. That would set up deeper correction to 55 W EMA (now at 5594.28) at least.

RBA minutes: No commitment to further rate cuts

The minutes from RBA’s February meeting reinforced the central bank’s cautious approach to monetary easing, making it clear that the recent 25bps rate cut to 4.10% does "not commit them to further reductions" in subsequent meetings.

Policymakers acknowledged that inflation has been falling at a “somewhat faster pace than expected,” which helped ease concerns over upside risks. However, they stressed that the path to returning inflation to target while maintaining labor market gains is “not yet assured.” The Board ultimately deemed that the stronger case was to ease policy, given the downside risks to the economy.

Despite the decision to cut, RBA members debated the risks of "easing policy too soon", recognizing that a premature policy shift could lead to resurgence in inflation.

They noted that if inflation proved “more persistent than expected,” holding the cash rate at 4.1% for an “extended period” or even tightening policy would be warranted.

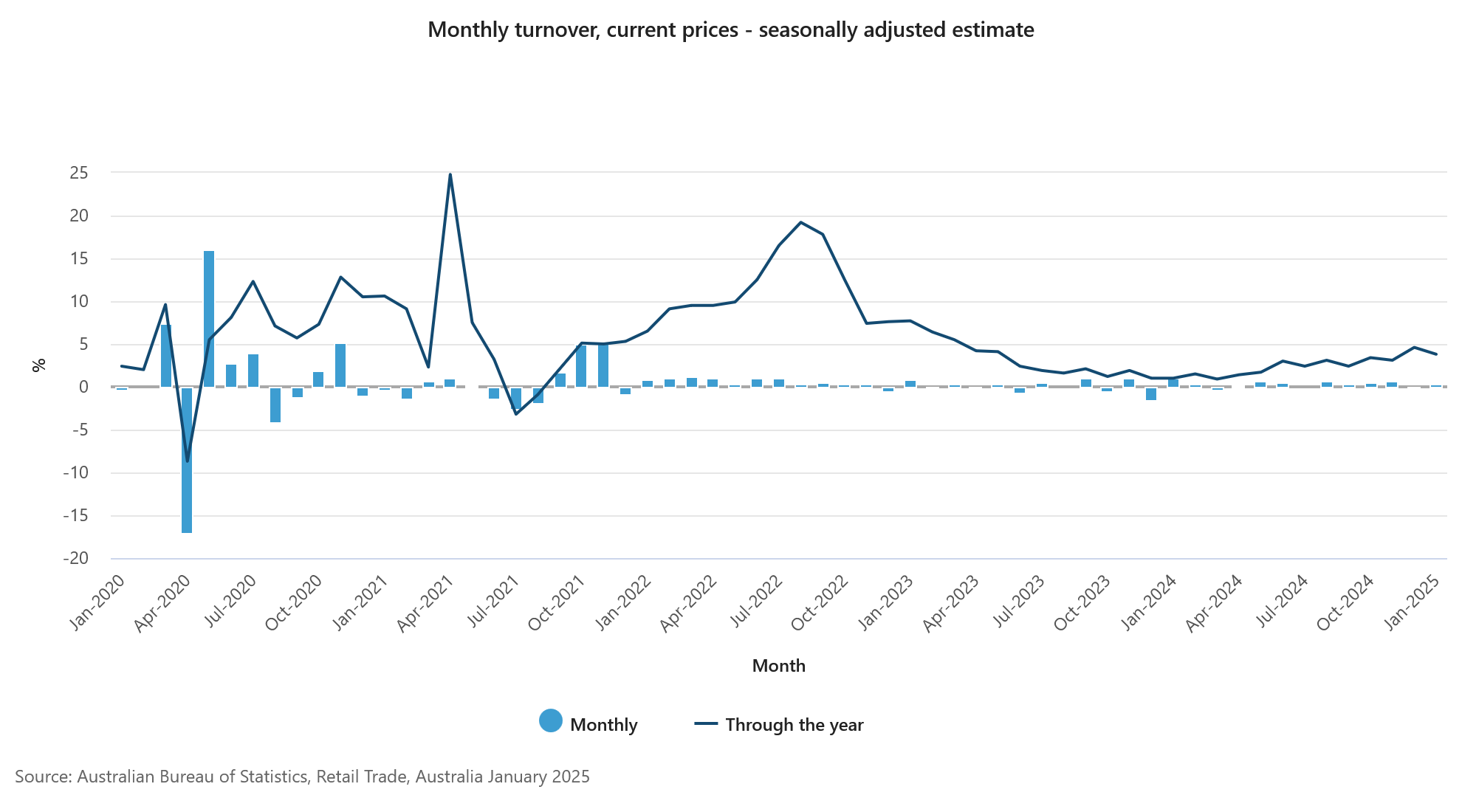

Australia retail sales rises 0.3% mom, driving by food-related spending

Australia's retail sales turnover rose 0.3% mom to AUD 37.08B in January, matched expectations.

Robert Ewing, ABS head of business statistics, said: "While the pick-up in retail spending since mid-2024 has been boosted by more discretionary spending, this month’s rise is mostly driven by food-related spending."

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.63; (P) 149.97; (R1) 150.83; More...

Intraday bias in USD/JPY is turned neutral again as it quickly reversed after recovering to 151.29. Overall outlook is unchanged that the decline from 158.86 is seen as the third leg of the corrective pattern from 161.94 high. On the downside, below 148.55 will resume the fall and target 61.8% retracement of 139.57 to 158.86 at 146.32 next. On the upside, break of 151.29 will delay the bearish case, and bring more consolidations.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

S&P 500 sinks as US tariffs on Canada, Mexico, and China set to begin

US equities tumbled sharply on Monday, kicking off March with the biggest single-day decline in months, and the markets were rattled by the formal commencement of a US-led trade war.

The selloff started in the afternoon after US President Donald Trump reaffirmed that 25% tariffs on imports from Mexico and Canada would go into effect as scheduled on Tuesday. Hopes for a last-minute deal to avert the full imposition of tariffs were dashed. The Federal Register confirmed that the new duties would be officially imposed at 05:01 GMT.

Similarly, the additional 10% duty on Chinese goods was also slated to take effect at the same time, effectively raising the total tariff on thousands of Chinese products to 20%.

In quick response, Canada announced retaliatory measures, with Prime Minister Justin Trudeau confirming that CAD 155B worth of US goods would be hit with 25% tariffs if Trump's levies proceed as planned. China’s commerce ministry also vowed countermeasures, calling the US tariffs "unreasonable and groundless, harmful to others."

Technically, S&P 500's rejection by 55 D EMA (now at 5988.77) is a near term bearish sign. Immediate focus is on 5773.31 support this week. Considering bearish divergence condition in D MACD, firm break of 5773.31 should confirm medium term topping that 6147.47. That would set up deeper correction to 55 W EMA (now at 5594.28) at least.

Australia retail sales rises 0.3% mom, driving by food-related spending

Australia's retail sales turnover rose 0.3% mom to AUD 37.08B in January, matched expectations.

Robert Ewing, ABS head of business statistics, said: "While the pick-up in retail spending since mid-2024 has been boosted by more discretionary spending, this month’s rise is mostly driven by food-related spending."

RBA minutes: No commitment to further rate cuts

The minutes from RBA’s February meeting reinforced the central bank’s cautious approach to monetary easing, making it clear that the recent 25bps rate cut to 4.10% does "not commit them to further reductions" in subsequent meetings.

Policymakers acknowledged that inflation has been falling at a “somewhat faster pace than expected,” which helped ease concerns over upside risks. However, they stressed that the path to returning inflation to target while maintaining labor market gains is “not yet assured.” The Board ultimately deemed that the stronger case was to ease policy, given the downside risks to the economy.

Despite the decision to cut, RBA members debated the risks of "easing policy too soon", recognizing that a premature policy shift could lead to resurgence in inflation.

They noted that if inflation proved “more persistent than expected,” holding the cash rate at 4.1% for an “extended period” or even tightening policy would be warranted.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Sydney – 17 and 18 February 2025

Members present

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Others present

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penny Smith (Head, International Department)

Financial conditions

Members commenced their discussion of financial conditions by noting that central banks in most advanced economies had cut policy interest rates further in response to easing inflationary pressures and weaker labour market conditions. Many of these central banks had signalled that additional rate cuts were also likely. However, market expectations of the number of further cuts in the United States had declined somewhat, reflecting stronger-than-expected economic data, communication by the US Federal Reserve (Fed) about the balance of risks, the prospect of increased US fiscal stimulus and the anticipated inflationary impact of tariffs.

Sovereign bond yields in advanced economies had tended to drift higher since the start of the year. For the United States and Japan, this reflected rising inflation expectations and a higher expected path for policy interest rates. Projections for ongoing growth in public debt were also placing upward pressure on sovereign yields in the United States, the United Kingdom and parts of Europe.

Equity prices had risen since the US presidential election in most advanced economies, including Australia, and measures of equity risk premia remained very low. In the United States, this appeared to reflect stronger macroeconomic outcomes and expectations, following the US election, of lower corporate taxes and reduced regulation. Recent profit outcomes internationally had also been generally favourable. Outside of the United States, the anticipated impact of tariffs on company earnings had been partly offset by the associated appreciation of the US dollar, which increased the local currency earnings of non-US exporters and multinational companies.

In China, authorities had communicated that monetary and fiscal policy settings would be loosened further in 2025 to support economic growth objectives, against the backdrop of a potentially sustained increase in US tariffs. Longer term Chinese Government bond yields had declined to around historical lows, amid strong demand for bonds and persistently low inflation. Equity prices had been little changed in China after increasing in late 2024 following the announcement of stimulus measures. The renminbi had depreciated only slightly following the announcement of US tariffs, as Chinese authorities continued to lean against exchange rate depreciation.

For Australia, the staff continued to assess financial conditions as restrictive overall. Interest rates on household and business lending were above their average since 2009, household debt repayments were high as a share of income, and growth in private activity was subdued. Estimates of the neutral interest rate are inherently uncertain and different modelling approaches used by the staff suggested a wide range of alternative values; all these lay below the cash rate, even before downward revisions to some of the staff estimates. In light of this pervasive uncertainty, members agreed that these revisions did not change their view about the stance of monetary policy, namely, that it remained restrictive.

Market participants had brought forward their expectations of an easing in monetary policy, and now saw a high likelihood that the cash rate would be reduced by 25 basis points at this meeting. The Board’s communication following the December meeting and the flow of data since then, including lower-than-expected outcomes for inflation and growth in GDP, had all been influential in moving market expectations for the current meeting. Market pricing continued to imply three or four 25 basis point cuts by mid-2026.

Although financial conditions remained restrictive overall, expectations for an early decline in the cash rate had contributed to some recent easing. Housing and business credit growth had increased further, wholesale funding conditions remained favourable and equity valuations were high. Members noted that the apparent strength in credit growth was partly explained by nominal growth in the economy. Indeed, household credit had declined relative to income and indicators of business gearing remained low.

The Australian dollar had depreciated since November 2024, by 4 per cent against the US dollar and 2 per cent on a trade-weighted basis. In trade-weighted terms, the Australian dollar was at the bottom of the trading range seen over the prior four years. The depreciation reflected broad-based US dollar strength associated with the prospect of tariffs, a decline in yield differentials between Australia and major advanced economies, and ongoing uncertainty around the outlook for the Chinese economy. Members noted that the impact of a deprecation of the Australian dollar on domestic inflation depended on its cause. For example, an exchange rate depreciation is less likely to result in higher inflation if it is associated with a decline in the terms of trade or a significant downgrade of the global growth outlook.

International economic conditions

Uncertainty about the global economic outlook remained high, given evolving developments in US Government policies relating to trade, the fiscal position, deregulation and immigration. Members discussed the potential impact on global growth of the announced higher tariffs on imports to the United States and the early responses by other major economies. They judged that the uncertainty about policy settings was likely to weigh on business investment, and perhaps household consumption, until the situation becomes clearer.

Output growth in the United States had remained robust towards the end of 2024 and timely indicators pointed to continued strong growth in the near term. US labour market conditions appeared to have stabilised at a level consistent with the Fed’s assessment of full employment, and earlier downside risks to the labour market had diminished. By contrast, growth in some other advanced economies remained subdued, and more so than had been expected. Inflation had continued to ease in most advanced economies, but the imposition of tariffs could potentially undo some of the progress on disinflation – particularly in the United States.

China achieved its 5 per cent GDP growth target in 2024, with growth picking up towards the end of the year. Some part of this pick-up was judged to be temporary, relating to government subsidies for consumer durable goods in China and strong exports ahead of anticipated US tariffs. Chinese authorities had announced additional fiscal measures to boost consumption, with further support measures expected. While conditions in the Chinese housing market had improved, overall conditions remained weak and a sustained recovery still faced headwinds.

Members noted that the ongoing uncertainty around US Government policy settings meant that Consensus global growth forecasts had not yet changed materially. Accordingly, the central forecast for growth in Australia’s major trading partners was unchanged for 2025. The outlook for 2026 was slightly lower, however, reflecting a softer growth outlook for North America (owing to the prospects of higher tariffs in the region). Members noted the potential for global trade tensions to escalate, in which case these forecasts could change quickly and significantly.

Domestic economic conditions

Turning to the domestic economy, members noted that data on output, inflation and wages had been a little weaker than expected at the time of the November meeting, while data on the labour market had been stronger.

Members considered the staff’s judgement that the easing in labour market conditions since late 2022 had at least stalled and may even have reversed a little in late 2024. The unemployment rate had unexpectedly edged lower in the December quarter to be around the same level as in mid-2024, and the underemployment rate had declined noticeably. Employment growth had remained strong and a range of leading indicators of the labour market also signalled ongoing strength.

Employment growth in the non-market sector continued to be very strong, most notably in health care. Members discussed analysis by the staff that suggested growth in health care employment had been achieved in part by drawing in workers from other industries, not only those who had previously been unemployed or not been in the labour force. Members observed that strong demand for labour in this sector had not resulted in greater dispersion of wages growth, because the movement of labour across industries had alleviated wages pressures in health care while reducing labour supply in industries where broader demand conditions were more subdued. In turn, this had likely contributed to relatively tight labour market conditions more broadly.

Wages growth had remained steady over 2024 in quarterly terms, though it had eased in year-ended terms. Public sector wages growth had been volatile in preceding quarters – and further volatility was possible in coming quarters pending the timing of some large enterprise agreements – but continued to show underlying strength. Unit labour cost growth had also eased but was still higher than consistent with inflation being sustainably at target.

Members welcomed the further easing in underlying inflation in the December quarter. Trimmed mean inflation was 0.5 per cent in the quarter and 3.2 per cent over the year; on a six-month annualised basis it had fallen to 2.7 per cent. There had been a broad-based easing in sub-components of the index. New dwelling cost inflation had eased considerably and unexpectedly owing to builders offering discounts. Inflation in rents had also continued to ease; this was partly due to an increase in the average number of people per household, which had alleviated some of the tightness in the rental market. Inflation in the price of a number of consumer services – including insurance – had declined, though services inflation overall remained high because of ongoing cost pressures. A wide range of transitory falls in various other components, mostly due to increased government subsidies, had collectively and temporarily lowered underlying inflation a little in the quarter. Headline inflation had eased to 2.4 per cent, and remained lower than underlying inflation, in part because of the effect of government subsidies to households.

In light of these developments, members considered the staff’s assessment that overall conditions in the labour market remained tight. That judgement reflected the relatively low rates of unemployment and underemployment, the recent increase in the stock of job vacancies, high growth in labour costs and reports from firms across a range of industries (via both business surveys and liaison) of ongoing difficulties finding suitable labour. At the same time, there had been an earlier-than-expected moderation in wages growth and underlying inflation.

Members then discussed staff analysis of a range of possible factors that could mean labour market conditions might not be as tight as implied by the central forecasts. Among other things, this included the possibility that factors unrelated to labour market tightness – such as workers’ attempts to restore real wages after the material reduction following the surge in inflation – or challenges measuring productivity in the non-market sector might be contributing to an over-assessment of the extent of tightness in the labour market. Members also considered whether the recent easing in inflation at a time of subdued growth in activity was attributable to some firms’ profit margins being compressed (as had been reported in liaison with firms) or to capacity pressures having eased in specific parts of the economy (such as the housing market). Some weight had been put on these arguments in the central projection, pushing down a little on the inflation forecast. However, it was possible that these effects could prove somewhat larger.

Members noted that GDP growth over the year to the September quarter had remained well below estimates of potential growth, consistent with a further narrowing of the output gap. However, timely indicators were implying that growth may have picked up in late 2024 and this recovery was expected to continue over the coming year. As a result, the staff’s judgement was that GDP growth would return to its potential growth rate and that the output gap was therefore unlikely to narrow much further, although the range of uncertainty around this judgement was material. These forecasts embodied a gradual pick-up in productivity growth to around its longer run average, following weak outcomes over preceding years. The unemployment rate was now expected to rise to around 4¼ per cent, lower than expected in November, before stabilising. Members noted that the forecasts were conditioned on market expectations for a cumulative 90 basis points of reductions in the cash rate over the forecast period.

The outlook for household consumption was a key factor underlying the projected recovery in GDP growth. Partial indicators suggested that consumption growth (excluding the effect of energy rebates) may have picked up a little further in late 2024, although it was unclear how much of this related to the increased prevalence of discounting and sales events. More generally, consumption growth was expected to recover alongside growth in real household disposable incomes, although a bit slower than had been expected in November. Members noted that there were credible arguments to suggest that consumption could be either weaker or stronger than the staff forecast. Looking beyond consumption, public demand had continued to support growth in overall activity and the outlook for public demand had been revised up, in line with the mid-year budget reviews by the Australian Government and state and territory governments.

Underlying inflation was forecast to return to the 2–3 per cent range earlier than previously expected. The staff had taken some signal from the weaker-than-expected December quarter inflation outcome, although quarterly underlying inflation was expected to pick up in early 2025, in part owing to the unwinding of some temporary factors. However, underlying inflation was forecast to settle a little above the midpoint of the 2–3 per cent range from late 2025, assuming the cash rate followed the implied market path conditioning the forecasts. Members noted that this forecast was underpinned by the staff’s judgement that labour market conditions would remain tight into the future if the cash rate followed this market-implied path, sustaining some upward pressure on inflation. Based on this forecast for underlying inflation, headline inflation was expected to exceed 3 per cent temporarily owing to the scheduled unwinding of cost-of-living measures.

Members discussed potential risks to the forecasts identified by the staff. One related to the possibility that the extent of excess demand in the labour market had been overestimated, as discussed earlier. Another related to uncertainties over US Government policy. Members noted the staff’s stylised scenarios that combined different assumptions of output growth of Australia’s trading partners, shifts in global trade patterns, the impact of high uncertainty on investment and household spending, and financial linkages such as movements in the exchange rate. All the scenarios indicated that the effect on domestic growth would be negative to some degree, but it was less clear whether the effect on inflation would be positive or negative.

Considerations for monetary policy

Turning to considerations for the monetary policy decision, members noted that inflation had declined, and by more than had been expected, while wages growth had slowed. Output growth had remained subdued, reflecting weak growth in private demand over the prior year amid restrictive financial conditions. At the same time, underlying inflation remained above the midpoint of the 2–3 per cent range. Output was most likely a little above its potential level and the labour market was still judged to be tight; there had also continued to be very strong growth in employment and a decline in measures of underemployment. Consumption growth looked to have picked up in the December quarter, as expected. Given these factors, underlying inflation was expected to be a little lower in the near term than had been forecast in November, but it was then forecast to remain above the midpoint of the target range if the cash rate were changed in line with market expectations.

In light of these developments, members considered their decision on the cash rate.

Leaving the cash rate unchanged at this meeting could be appropriate if members formed the view that labour market conditions were still tighter than consistent with sustaining inflation at target, that the upside risks to inflation were still material or that a cut in the cash rate would not leave monetary policy sufficiently restrictive. Members noted that placing significant weight on any of these arguments could imply that it would be best to wait for additional data before deciding to adjust the cash rate.

Conditions in the labour market provided the strongest reason to leave the cash rate unchanged. Members noted that a broad range of labour market indicators had strengthened over prior months and that the staff had lowered their forecast for the unemployment rate. They observed that there was a possibility that conditions in the labour market could prove even stronger than assumed in the staff’s forecasts. Members noted that, while there was significant uncertainty about the extent of excess demand in the economy, the staff’s judgement was that the tightness in the labour market was not consistent with inflation being at the target.

A second argument to hold the cash rate steady related to the possibility that growth might pick up more quickly than forecast. That might come from household consumption, given the nascent recovery in real incomes and the aggregate financial position of the household sector. Or it might come from stronger global growth, if recent trends in equity markets were correct in implying that any adverse impact on growth of evolving US Government policy might not be material. Against this backdrop, members noted that the output gap was judged to be positive and unlikely to close over the forecast period if the cash rate followed the market path.

A third potential reason for leaving the cash rate unchanged could be if members formed the view that the stance of monetary policy would not be sufficiently restrictive following a cut in the cash rate. Members noted that while there were various indicators underpinning the staff’s judgement that current policy was restrictive, the signal from some other indicators (including credit growth, and equity and corporate bond market pricing) clouded this conclusion somewhat. The Australian dollar had also depreciated a little over preceding months. Members observed that not having lifted interest rates as high as in countries that had faced a similar inflation challenge meant the Board should be cautious when deciding to lower the cash rate.

By contrast, reducing the cash rate at this meeting would be appropriate if members judged that their confidence that inflation could sustainably be returned to target had risen, if they placed greater weight on the downside risks to the economy than on those to the upside, or if the risk of leaving interest rates at current levels for too long was assessed to be greater than the risk of easing policy too soon.

The strongest reason to lower the cash rate at this meeting was based on the signal from recent trends in inflation and wages. Members noted that inflation in the December quarter had been weaker than expected: indeed, underlying inflation was already close to the midpoint of the target range on a six-month annualised basis. The composition of inflation – with house-building costs having fallen and the pace of increase in rents and insurance premiums moderating – had also been favourable. Wages growth had been a little softer than expected, and the prospect that it would pick up had perhaps diminished given inflation had declined and if firms and workers were adjusting to weaker productivity growth.

These developments could also be taken to imply that there was possibly more capacity in the labour market than members had previously judged. Members debated the range of explanations reviewed by staff that could be consistent with this. These included the possibility that a reasonable portion of the growth in wages over the prior year was attributable to real wage catch-up, or that productivity growth in the non-market sector had been higher than the official measure.

The case to lower the cash rate at this meeting could be further supported if members assessed that the risks surrounding the outlook for economic growth were, on balance, to the downside. In the domestic economy, members considered it unlikely that employment in the non-market sector would continue to grow as strongly over the forecast period as it had done over the preceding year, and noted that any slowing would weigh on overall employment unless hiring in the market sector strengthened. The recovery in consumption was also not yet assured, given uncertainty about how much the December quarter data had been influenced by discounting or promotional activity and the risk that earlier falls in real household disposable income would exert a persistent drag. Consistent with that, some firms had recorded a narrowing in their profit margins. Internationally, uncertainty about US Government policy was high and members noted that this could have a material adverse effect on the propensity of firms and possibly also households to spend. Activity in the Chinese economy was also expected to slow.

Having weighed up these alternative arguments, members decided that the case to lower the cash rate target at this meeting was, on balance, the stronger one. Members judged that the continued fall in underlying inflation, and at a somewhat faster pace than expected, meant that the upside risks to inflation had abated enough that they no longer needed the insurance they had taken out when raising the cash rate target in November 2023. Members tended to place more weight on the downside risks to the economy, and on the possibility identified by the staff that capacity in the labour market might be somewhat greater than embodied in the central projection. Given these judgements, members were particularly mindful of the risk of keeping monetary policy tight for too long, with adverse impacts on economic activity, the labour market and inflation.

In taking this decision, members considered the risk that easing policy too soon could add to inflationary pressures. They observed that the central forecast for inflation to settle a little above the midpoint of the 2–3 per cent target range over the medium term was predicated on three to four reductions in the cash rate target over the year or so ahead. An alternative projection, in which the cash rate was left at 4.35 per cent for an extended period, showed underlying inflation undershooting the midpoint of the target range over the medium term. Members noted that both projections were subject to material uncertainty. But if the evolving data signalled that inflation was proving more persistent than expected, it would be reasonable to maintain a more restrictive stance of policy by holding the cash rate at 4.1 per cent for an extended period – given members’ assessment that this level would still be restrictive – or by even tightening policy if the outlook was for inflation to rise materially. On balance, members judged that accepting the risk of needing to adopt such a course of action was preferable to accepting the risk of holding interest rates high for too long.

In light of these considerations about the risks surrounding the Board’s decision, members agreed that their decision at this meeting did not commit them to further reductions in the cash rate target at subsequent meetings. While economic outcomes had given members more confidence that they could return inflation to target at the same time as preserving most of the gains in the labour market with a lower cash rate, they agreed that this was not yet assured. As a result, members expressed caution about the prospect of further policy easing, which could also be seen in the forecast for inflation based on the market path. Members distinguished their current situation from that faced by central banks in other countries that had lowered interest rates several times. They noted that interest rates in Australia had not risen as high as elsewhere and that the labour market domestically was in a much stronger position than had been the case in other economies when their central banks first lowered interest rates.

In finalising the policy statement, members affirmed their commitment to returning inflation to the midpoint of the target range, consistent with the Board’s mandate set out in the Statement on the Conduct of Monetary Policy. They emphasised that the decision at this meeting acknowledged the progress that had been made in reducing inflation while not committing the Board to ease policy further. Members also agreed that future decisions would be guided by the incoming data and evolving assessment of risks. Returning inflation to target remains the Board’s highest priority and it will do what is necessary to achieve that outcome.

The decision

The Board decided to reduce the cash rate target by 25 basis points to 4.10 per cent and to decrease the interest rate on Exchange Settlement balances by 25 basis points to 4.00 per cent.

Bitcoin’s (BTC/USD) Wild Ride – Open Interest, ETF Flows Amid Trump’s Crypto Remarks

- Bitcoin’s (BTC/USD) price experienced significant volatility, dropping to $78k before rising to $95,000 due to Trump’s cryptocurrency reserve comments, then settling around $86k.

- Open interest for Bitcoin is at a six-month low, which historically has preceded price jumps.

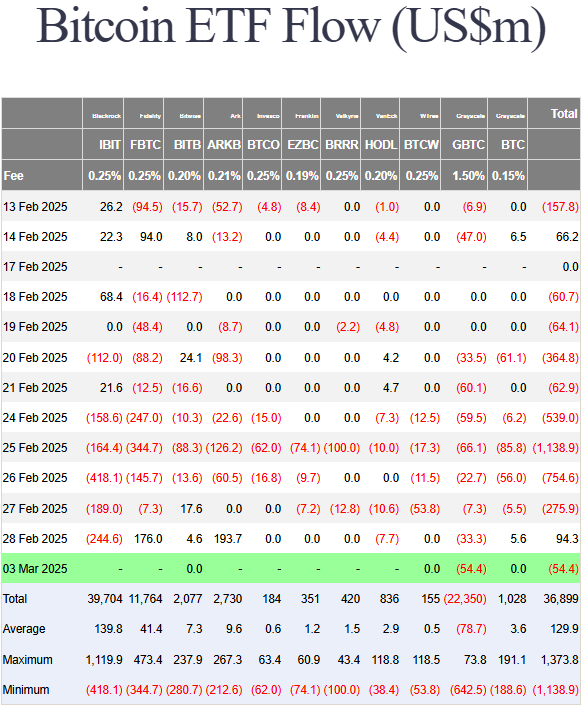

- Spot Bitcoin ETF flows saw a $94.3 million investment on the last day of February, ending a period of significant withdrawals. Can it continue?

- Technical analysis indicates a potential downtrend for BTC/USD.

Bitcoin’s rollercoaster ride continued today with the world’s largest cryptocurrency rising about 18% since Friday’s low. The gains proved short-lived however, as Bitcoin surrendered half of those gains to trade back at $86k at the time of writing.

Crypto Heatmap, March 3, 2025

Source: TradingView (click to enlarge)

President Trump and the Crypto Reserve

Bitcoin’s price surged by 11%, reaching almost $95,000, after U.S. President Donald Trump mentioned on March 2 the idea of creating a strategic cryptocurrency reserve.

Initially, he said it would include XRP, Solana, and Cardano, but later added on his Truth Social platform that it would also include Bitcoin, Ether, and other cryptocurrencies.

The move followed a rise of 2% on March 1 and a recovery in price on Friday 28 from lows of 78197 to close almost flat at 84321.

Trump’s post gave crypto a positive push, but bigger issues like tariffs still play a big role for traders. Cryptocurrencies are still affected by overall economic conditions and that was reflected by price action today as tariff uncertainty and geopolitics continue to dominate.

There are concerns around President Trump’s plans as according to James “MetaLawMan” Murphy, a lawyer focused on crypto issues, he does not believe a strategic digital asset reserve can be established by executive order.

Murphy went further and pointed out on X that even if Congress quickly approves the strategic digital asset reserve which is unlikely, the main question is how it will be funded. Most likely, the plan would start by stopping government sales of crypto assets, which would have only a small effect on prices.

The question in the short-term is whether Friday’s lows around $78k handle serve as a floor for another push toward $100k, or crumble as overall market sentiment remains one of caution.

ETF Flows

Spot Bitcoin ETFs in the U.S. saw $94.3 million in investments on the last day of February, marking the end of crypto’s toughest month in three years.

This amount ended an eight-day period of withdrawals when investors took out more than $3.2 billion from these funds as crypto prices dropped.

The new week will be pivotal for ETF flows as it will be interesting to see if ETF flows improve following the crypto reserve comments by President Trump over the weekend.

Source: Farside Investors (click to enlarge)

Bitcoins Open Interest Paints a Positive Picture

CrediBULL Crypto shared on X that Bitcoin’s open interest is now at its lowest point in six months. He mentioned that the last time it was this low, Bitcoin’s price was between $50,000 and $60,000. He also pointed out that Bitcoin’s funding rate has turned negative, which is the same thing that happened before Bitcoin’s price jumped to $100,000 when it was trading in the $50,000-$60,000 range.

Interestingly, he stated that these signals look “fantastic” for Bitcoin and support his belief that it has hit a bottom. This seems true, as Bitcoin has bounced back to $95,000 after dropping below $80,000 last week.

Source: ‘CrediBULL Crypto’ on X (click to enlarge)

Technical Analysis BTC/USD

Bitcoin (BTC/USD) from a technical standpoint on the daily timeframe remain in a downtrend despite the weekend rally.

The failure of the daily candle to close above the 96572 handle leaves BTC/USD vulnerable to further downside.

There is also a death cross formation as the 50-day MA crosses below the 100-day MA which usually hints at further downside potential.

Bitcoin (BTC/USD) Daily Chart, March 3, 2025

Source: TradingView.com (click to enlarge)

Dropping down to a two-hour chart and the inverse head and shoulders pattern that formed over last week with a break occurring over the weekend has played out to perfection.

The target was around the 95000 handle which has also been fulfilled and preceded a significant pullback on Monday.

The concern part is that the bullish rally has not just faded but a candle close below the previous swing low at 85600 means we have had a shift in structure favoring bears at this stage.

There is also the 50 and 100-day MAs both of which will provide significant resistance hurdles should bulls look to make a move once more.

Immediate resistance rests at 86567 and 88096 before the 90000 handle comes back into focus.

Immediate support rests at 85000 before the 83500 and 80000 handles come into focus.

Bitcoin (BTC/USD) Two-Hour (H2) Chart, March 3, 2025

Source: TradingView.com (click to enlarge)

Support

- 85000

- 83500

- 80000

Resistance

- 86567

- 90000

- 91804