Sample Category Title

GBPJPY Hits New 19-Month High; Bearish Correction is Possible

GBPJPY surged sharply higher this week and during today's trading session it reached a fresh 19-month high of 156.60. Prices have broken above the 156.00 handle for the first time since June 2016. The bullish picture in the short-term chart is further supported by the technical indicators.

From the technical point of view, the Relative Strength Index (RSI) is flattening in the positive territory and is approaching the overbought area. Also, the MACD oscillator is holding in the bullish area with weaker momentum than before. However, in the 4-hour chart, the 20-simple moving average posted a bullish crossover with the 40-SMA, indicating further gains.

If price action remains positive, there is scope to test the 160.00 strong psychological level taken from the peak in June 2016, while the price is currently trading slightly lower.

If the price creates a bearish correction, then the focus could shift to the downside towards the 23.6% Fibonacci retracement level around 154.30 of the up-leg from 147.00 to 156.60. If this level is breached, it could increase downside pressure until the 38.2% Fibonacci mark at 152.90.

The U.S. Economy Kicks off 2018 with Another Healthy Job Gain

U.S. payrolls rose by 200k in January, meeting survey expectations for 190k. Gains were largely in the private-sector hiring (+196k). The unemployment rate remained unchanged at 4.1%.

All eyes were on wage growth in this report, and it didn't disappoint. Average hourly earnings rose a relatively strong 0.3% in January and accelerated to 2.9% year-over-year. That marks the fastest pace of wage gains since 2009.

Payrolls gains were broad based. In the lead were construction (+36k), food services (+31k), health care (+21k) and manufacturing (+15k). Both goods-producing employment (+57k) and services employment (+139k) saw healthy growth.

The combined revisions to November and December, saw payrolls growth 24k lower than previous estimates. But job growth has still averaged 192k over the past three months, a very healthy pace.

January's household survey incorporated updated population estimates. While the population, labor force, employment and unemployment were all revised up, the unemployment rate, and participation rate were unaffected.

The one negative in the report was a decline (-0.6%) in hours worked in January. This is not positive for economic growth, but we suspect it may have been affected by the brief government shutdown and/or the heavy winter storms that hit the Northeast early in the month.

Key Implications

There appears to be no stopping the U.S. labor market. With both jobs and wages beating expectations, there is little to criticize in this report. A better-than-expected print this morning has added to the pressure on the bond market, pushing the U.S. 10-year yield above the 2.8% mark.

As the labor market tightens, new jobs will increasingly be filled by workers (re-)entering the labor force. The labor force participation rate for core age workers (25-54 yrs) has made notable gains since 2015, but there is room for further improvement. Indeed, our economic forecast relies on further improvements in labor force participation in order to sustain job growth. Still, as this slack is absorbed, we expect monthly payrolls gains will slow over the course of 2018.

Stronger wage growth will help to draw workers back to the workforce. Indeed, January's wage gain is just what the Fed is looking for, and helps to cement the case for a rate hike in March. That also puts the balance of risks toward more rate hikes over the course of the year.

Dollar Uplifted by Solid US Jobs Report

The Dollar flickered back to life on Friday afternoon, with prices sprinting towards 89.20 as investors cheered January's solid US jobs data.

The US economy created 200,000 new jobs in January, while the unemployment rate remained steady at 4.1%. Yearly wage growth dished out an upside surprise by rising 2.9% (an eight-and-a-half-year high), throwing the Dollar a much-needed lifeline. Repeated signs that wage growth is building momentum are likely to support rising inflation expectations, which could boost speculation of higher US interest rates this year. The Dollar clearly needed support this week, and January's impressive US jobs data has come to the rescue.

From a technical standpoint, the Dollar Index is still pressured on the daily charts. Prices remain at risk of depreciating back below 89.00, if bulls are unable to break above the 89.60 level. Sustained weakness below 89.00 may invite decline back towards 88.50. Alternatively, breakout above 89.60 could pave the way towards 90.00.

By the Numbers: U.S January NFP Fallout

- Non-farm payrolls: +200k vs. +148k prev.

- Private payrolls: +196k vs. prev. +146k)

- Manufacturing payrolls: +15k vs. prev. +25k

- Unemployment rate: +4.1% vs. prev. +4.1%

- Average hourly earnings: +0.34% m/m, +2.9% y/y vs. prev. +0.4% m/m, +2.7% y/y

- Workweek hours: 34.3 vs. prev. 34.5 – -0.2

- U.S 10-year yield: +2.83%

U.S employers added +200,000 jobs in January (employers added an average of +181k a month in 2017).

Construction, manufacturing and restaurants had strong job growth, while Government payrolls grew by +4k last month.

Strong back-month revisions for average hourly earning and headline job prints – Dec payrolls revised to +160k and Nov revised to +216k

Average hourly earnings rose +0.34% from Dec following an upwardly revised +0.4% gain. Year-over-year, it was +2.9% compared with projections for a +2.6% increase. December's gain was revised upward to +2.7%.

USD (€1.2455, £1.4165, ¥110.33, C$1.2361) is better bid across the board, while the 10-year yield has backed up to +2.834% as wage growth is starting to accelerate.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2418; (P) 1.2470 (R1) 1.2556; More....

EUR/USD failed to take out 1.2537 resistance and drops notably in early US session. But for the moment, intraday bias remains neutral. As long as 1.2222 support holds, near term outlook remains bullish. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

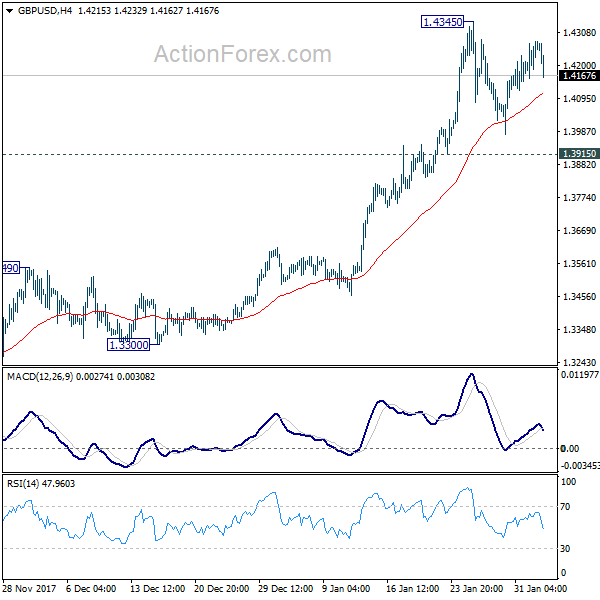

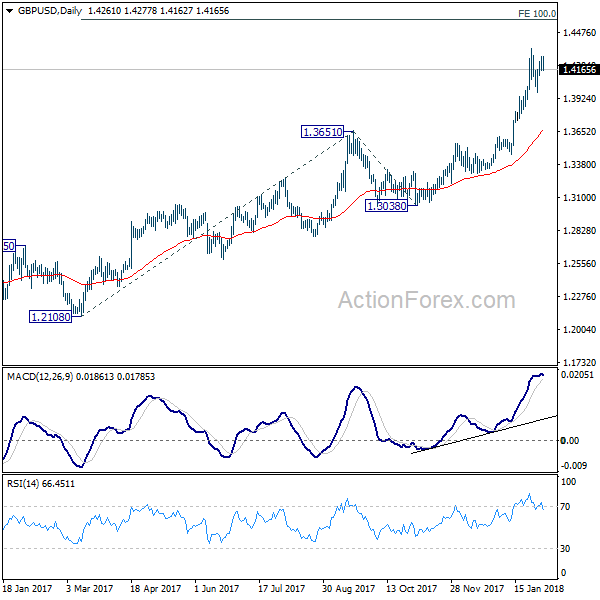

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4188; (P) 1.4233; (R1) 1.4307; More.....

GBP/USD weakens in early US session but stays in range below 1.4345. Intraday bias remains neutral as consolidations from 1.4345 might extend. Still, in case of another fall, downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

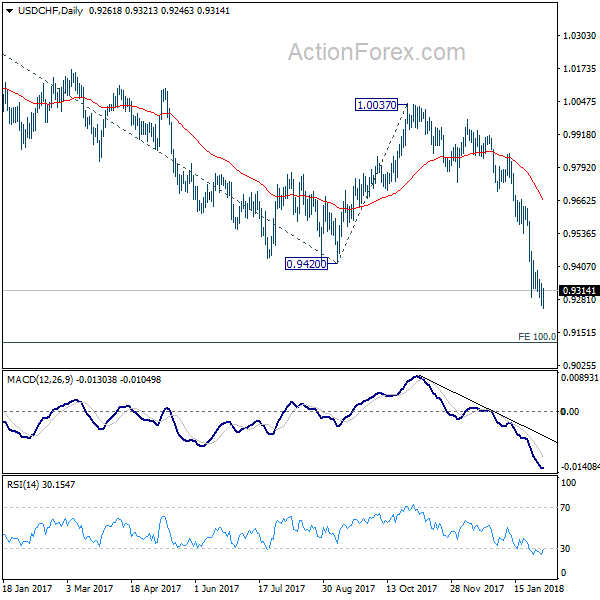

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9232; (P) 0.9287; (R1) 0.9317; More...

USD/CHF recovers in early US session but stays below 0.9392 minor resistance. Intraday bias remains on the downside and deeper fall is still mildly favored. Current decline from 1.0037 should extend to next key fibonacci level at 0.9115. On the upside, break of 0.9392 minor resistance, however, will indicate short term bottoming and bring stronger rebound.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.07; (P) 109.41; (R1) 109.73; More...

USD/JPY's rebound from 108.27 extends higher today. Break of 110.18 support turned resistance is taken as the first sign of near term reversal. Intraday bias is turned back to the upside for 111.47 resistance first. Sustained break there will also have 55 day EMA (now at 11.39) firmly taken out. In such case, further rise would be seen back to 113.38/114.73 resistance zone. On the downside, however, below 109.22 minor support will turn focus back to 108.27 instead.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Dollar Rises after Solid NFP, Reversing against Yen, But Unsure about Europeans

Dollar jumps in early US session after another set of solid employment data. Non-farm payrolls report shows 200k growth in January, above expectation of 180k. Prior month's figure was revised up by 12k to 160k. Unemployment rate was unchanged at 4.1% as expected. Average hourly earnings also grew 0.3% mom, in line with consensus. The recovery in greenback is broad based. But we'd like to point out that firstly, USD/JPY's break of 110.18 resistance is now seen as a sign of near term reversal. AUD/USD has topped out earlier this week and the post NFP decline also affirms the case of near term reversal. However, against European majors, Dollar is just in staying in range and the rebound might just be part of consolidation patterns.

UK PMI construction indicated a difficult start to 2018

UK construction PMI dropped to 50.2 in January, down from 52.2 and missed expectation of 52.0. Markit noted in the release that "January's PMI data indicated a difficult start to 2018 for the UK's construction sector, underlined by business activity growth slumping to a four-month low and new orders sliding back into decline." Also, "a contraction in house building added to lackluster commercial building and civil engineering markets, and reduced inflows of new work suggest overall activity could slip into decline in February." And further more, "cost pressures remained intense, fuelled by shortages of input materials and high costs for imported products."

ECB Coeure: The euro area needs reform

ECB Executive Board member Benoit Coeure warned today that "to assume that the current economic expansion will heal all wounds is naive. The euro area needs reform." He pointed out that the next financial crisis could force ECB interest rates "much deeper into negative territory" or "require purchases of assets that are riskier than public or corporate debt", or " it may draw us dangerously close to monetary financing of governments." He suggested greater integration in services and in financial markets, and a more complete banking union.

Released from Eurozone, PPI rose 0.2% mom, 2.2% yoy in December.

Nomination for BoJ Governor might be revealed mid-to-late February

In Japan, it's reported that the government will likely announce the nominations of next BoJ Governor and Deputy Governors around mid-to-late February. At this point, it's still believed that current Governor Haruhiko Kuroda is the front runner, given the praises by Prime Minister Shinzo Abe and his officials. However, it's far from being certain. From the government's point of view, the choices could be indifferent if the next Governor will be persistent enough in following through with Abenomics.

BoJ conducted a special bond purchase operation today, offering to buy an "unlimited" amount of long-term JGBS. That's the first time in six months that such special operations were conducted. On the top of that, the purchase of 5- to 10- years JGBs was also raised from PY 410b to JPY 450b. It's seen by the markets as a pre-emptive move to fend off rise in JGB yields, which was taken higher by global counterparts in recent weeks.

Released from Japan, monetary base rose 9.7% yoy in January.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.07; (P) 109.41; (R1) 109.73; More...

USD/JPY's rebound from 108.27 extends higher today. Break of 110.18 support turned resistance is taken as the first sign of near term reversal. Intraday bias is turned back to the upside for 111.47 resistance first. Sustained break there will also have 55 day EMA (now at 11.39) firmly taken out. In such case, further rise would be seen back to 113.38/114.73 resistance zone. On the downside, however, below 109.22 minor support will turn focus back to 108.27 instead.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Dec | -9.60% | 10.80% | 9.60% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | 9.70% | 11.00% | 11.20% | |

| 00:30 | AUD | PPI Q/Q Q4 | 0.60% | 0.40% | 0.20% | |

| 00:30 | AUD | PPI Y/Y Q4 | 1.70% | 1.20% | 1.60% | |

| 09:30 | GBP | Construction PMI Jan | 50.2 | 52 | 52.2 | |

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.20% | 0.20% | 0.60% | |

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 2.20% | 2.30% | 2.80% | |

| 13:30 | USD | Change in Non-farm Payrolls Jan | 200K | 180K | 148K | 160K |

| 13:30 | USD | Unemployment Rate Jan | 4.10% | 4.10% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.30% | 0.30% | |

| 15:00 | USD | Factory Orders Dec | 0.90% | 1.30% | ||

| 15:00 | USD | U. of Mich. Sentiment Jan F | 95 | 94.4 |

Dollar Posts Gains ahead of NFP Report; European Stocks Tumble

Here are the latest developments in global markets:

FOREX: The dollar continued to rise slowly against its major peers after US Treasury yields peaked at fresh highs early today but remained closed to 3-year lows. The dollar index inched up to an intra-day high of 88.88 (+0.16%) and dollar/yen was on track to break above 110, posting a fresh one-week high at 109.91 (+0.46%). Today's news that the BOJ was planning to buy an unlimited amount of Japanese government bonds also worked in favor of the greenback. Euro/dollar slipped to 1.2475 (-0.18%) and pound/dollar declined to 1.4229 (-0.34%) on the back of a stronger dollar, while weaker-than-expected readings on the British construction PMI and the Eurozone PPI also weighed on the two currencies. The antipodean currencies were the bigger losers as spreads between the local and US yields were falling. Aussie/dollar stretched downwards to 0.7975 (-0.63%) and kiwi/dollar retreated to 0.7141 (-0.61%).

STOCKS: A sharp loss in Deutsche Bank's shares dragged the pan-European STOXX 600 lower on Friday, with the index falling by 0.91% at 1100 GMT and being set to post its bigger weekly loss since August after a strong start to the year. The blue-chip Euro STOXX 50 dived by 1.01% and the German DAX 30 tumbled by 1.13%. The UK FTSE 100 was down by 0.28%, weighed by losses in telecommunication services. US stock futures were mixed.

COMMODITIES: WTI crude oil was trading 0.10% up on the day at $65.88/barrel supported by OPEC-led supply cuts despite rising US production. Brent was down by an equivalent percentage at $69.58/barrel. Gold was last seen at $1345.40/ounce, down by 0.25% on the day.

Day ahead: NFP report said to show better results in January

US Nonfarm payrolls will take center stage during the day with the potential to shake the dollar which has been gaining against a basket of major currencies so far in the day.

Following Wednesday's upbeat APD employment report which tracks changes in the private sector, the government's comprehensive nonfarm payrolls due at 1330 GMT are expected to come higher at 180,00 new positions in January compared to 148,000 seen in December. Regarding the unemployment rate, this is anticipated to remain steady at a 17-year low of 4.1%. However, wage growth figures are expected to be of greater importance for the dollar as the Fed has been long concerned about subdued wages which probably are the reason why inflation is weak. Analysts believe that average hourly earnings have risen by 2.6% y/y in the twelve months to January compared 2.5% in the previous month, while on a monthly basis they project that the measure has continued to increase at the December's pace of 0.3%. Any upside surprise in the wage growth, though, would add optimism that the Fed's monetary policy is going in the right direction and hence justify any plans for further policy tightening this year. Note that private sector wages rose by 2.8% y/y in the fourth quarter, above the previous print of 2.6%, posting the highest increase since the first quarter of 2015.

In other data out of the US, December's factory orders and the University of Michigan's final readings on consumer sentiment for the month of January will also gather attention at 1500 GMT. Both measures are anticipated to show some improvement.

In energy markets, the US Baker Hughes oil rig count is due at 1800 GMT.

Public appearances today will involve comments by the Dallas Fed President Robert Kaplan – a non-voting FOMC member in 2018 – who will be participating in a Q&A session before the Teacher Retirement System of Texas Annual Conference at 1830 GMT. A few hours later, the San Francisco Fed President John Williams – a voting FOMC member in 2018 – will be talking about the US economy before the Financial Women of San Francisco at 2030 GMT.

Energy companies Chevron and Exxon Mobil and pharma firm Merck & Co. are among firms releasing quarterly results on Friday. All three will be releasing their reports before the US market open.