Sample Category Title

Daily Wave Analysis: EUR/USD Bullish Price Action Faces 1.25 Resistance Again

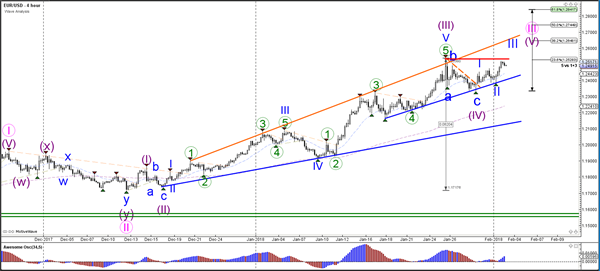

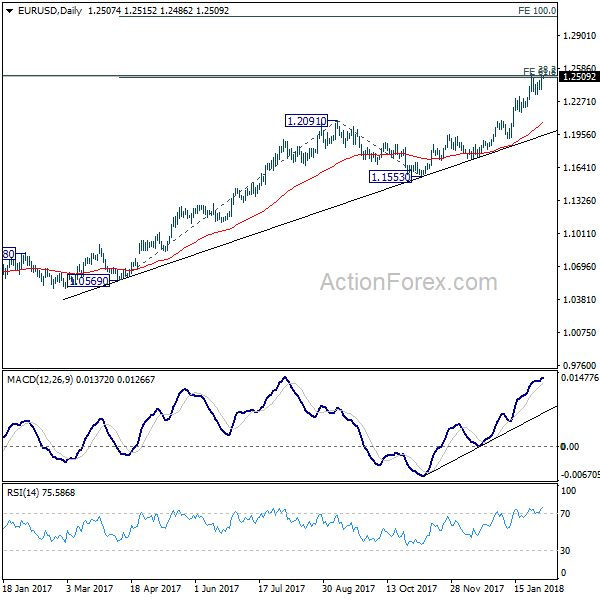

Currency pair EUR/USD

The EUR/USDis now challenging the previous top (red). A bullish breakout would confirm the development of a wave 3 (blue) of a wave 5 (purple). A failure to break could indicate a bullish ABC rather than a 123. In that case the correction could take price below the support trend line (blue).

The EUR/USD is building a small pause within the larger uptrend. The pattern could be a full flag and hence also a wave 4 (green). A bullish breakout could indicate uptrend continuation whereas a break below the 61.8% Fib and support trend line (blue) from the top of wave 1 invalidates the current 5 wave (green).

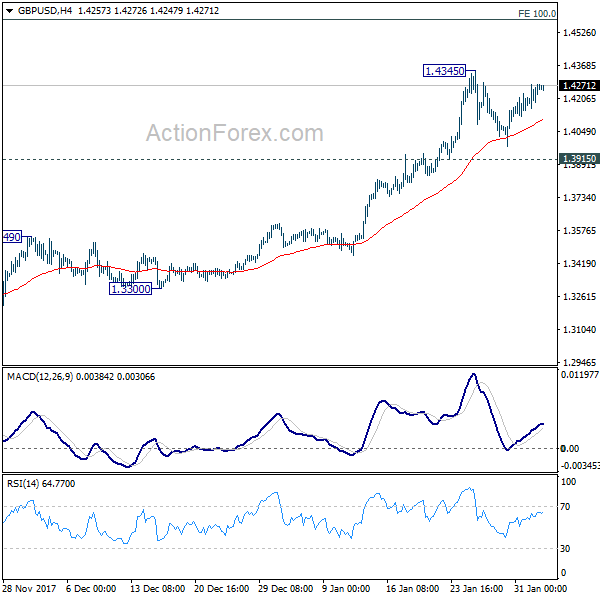

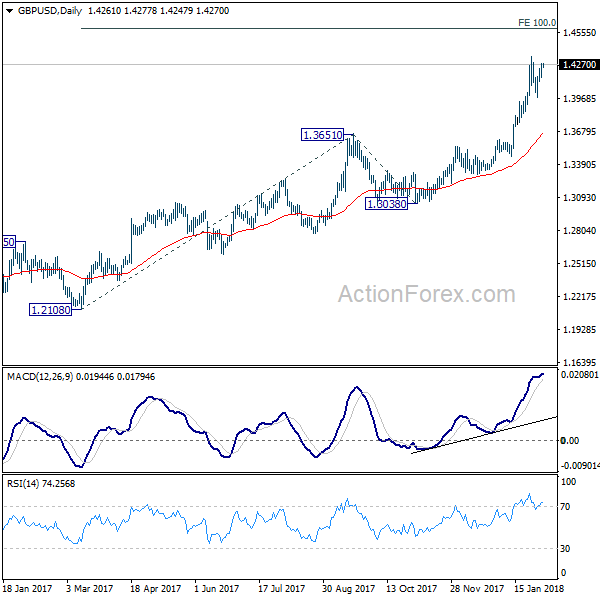

Currency pair GBP/USD

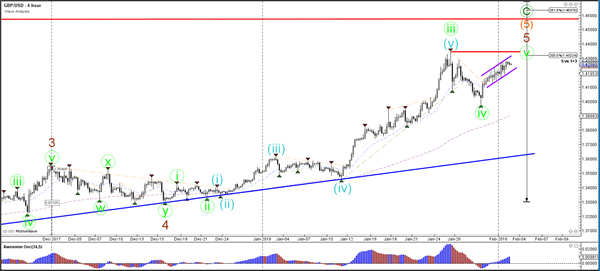

The GBP/USDis building a bullish channel (purple lines) which is testing the previous top. A break below the channel could indicate a larger wave 4 (green) whereas a break above the resistance (red) could indicate uptrend continuation.

The GBP/USD is losing a little bit of its bullish momentum. Price would need to break above resistance (red) to make a bullish break towards the Fib levels of wave 3 (blue) more likely.

Currency pair USD/JPY

The USD/JPYis still testinga larger resistance trend line (red) of the downtrend channel.

The USD/JPY bullish breakout could confirmthe development of a potential wave 3 (purple) if price manages to break above the resistance trend line (red).

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7994; (P) 0.8031; (R1) 0.8074; More...

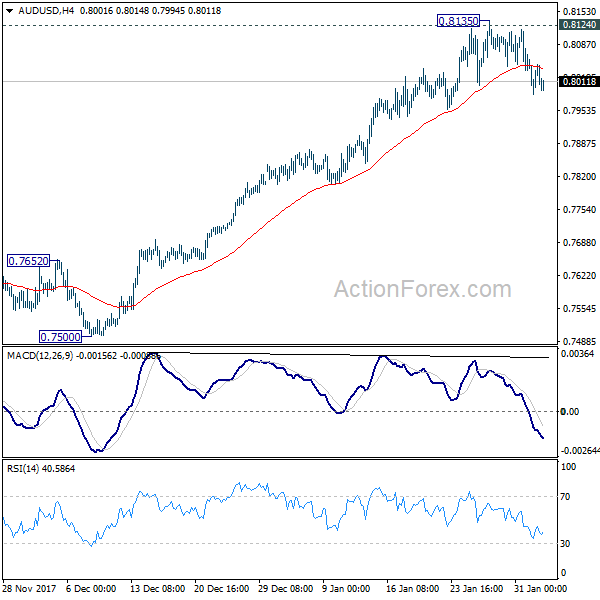

As noted before, a short term top was formed at 0.8135 after failing to sustain above 0.8124 resistance. Intraday bias remains on the downside for 55 day EMA (now at 0.7856). At this point, we'd expect strong support from there to bring rebound. But sustained trading below the EMA will bring retest of 0.7500 key near term support. On the upside, sustained break of 0.8124 will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451.

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside and bring reversal. Break of 0.7500 support will indicate that the medium term trend has reversed.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2238; (P) 1.2285; (R1) 1.2312; More...

Intraday bias in USD/CAD remains on the downside for the moment. Current decline from 1.2919 would extend to retest 1.2061 low. Decisive break there will resume larger down trend. However, considering bullish convergence condition in 4 hour MACD, break of 1.2390 minor resistance should indicate short term bottoming. In this case, intraday bias will be turned back to the upside for rebound to 55 day EMA (now at 1.2531).

In the bigger picture, rebound from 1.2061 is likely completed completed at 1.2919, rejected by 55 week EMA and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2418; (P) 1.2470 (R1) 1.2556; More....

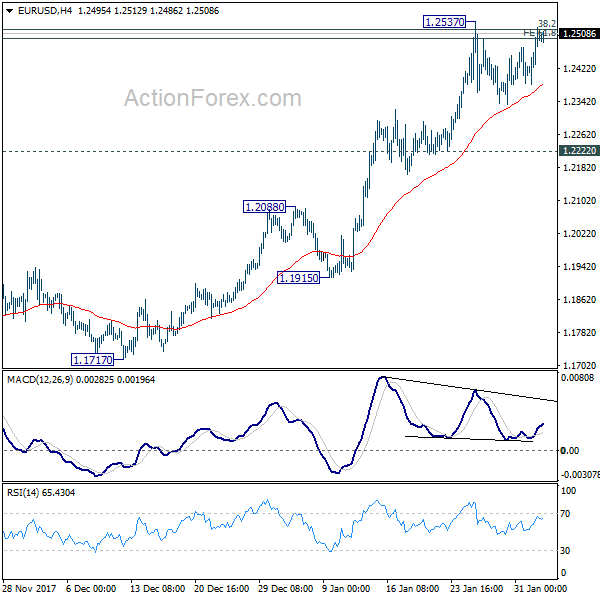

EUR/USD recovered but stays below 1.2537. Intraday bias remains neutral first. As long as 1.2222 support holds, near term outlook remains bullish. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4188; (P) 1.4233; (R1) 1.4307; More.....

GBP/USD is staying in consolidation from 1.4345 and intraday bias remains neutral. Another fall could be seen but downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

USD/JPY Daily Outlook

Daily Pivots: (S1) 109.07; (P) 109.41; (R1) 109.73; More...

Intraday bias in USD/JPY remains neutral as consolidation from 108.27 is in progress. As long as 110.18 resistance holds, near term outlook stays bearish and deeper fall is expected. On the downside, break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Market Update – Asian Session: Markets Await US Payrolls Figures

Headlines/Economic Data

General Trend: Asian equities trade generally lower

Nikkei 225 declines despite BoJ bond operation; another heavy day for Japan corporate earnings

South Korean chip makers decline over 3%

Sony names CFO as new CEO

Japan’s Mitsubishi Electric gains over 1%, as it raised its FY outlook amid higher profits in industrial automation systems business

REITs and Utilities underperform amid rise in global bond yields

Amazon and Apple gain in the afterhours following earnings, while Alphabet declines

Commodity currencies underperform

Markets looking ahead to upcoming US payrolls report

Australia/New Zealand

ASX 200 opened flat; closed +0.5%

ASX 200 Energy Index +2%, Resources +0.7%, Financials +0.5%; REIT -1.2%, Utilities -0.4%

Building materials firm James Hardie [JHX.AU] trades higher by over 4%: Reports Q3 adj Net $69.9M v $62Me; EBIT $97.4M v $92Me; Rev $495M v $493Me

Woolworths [WOW.AU]: Gains over 2% amid positive broker commentary

Telstra [TLS.AU]: Declines over 0.5% after announcing A$273M impairment charge related to US video business

(AU) Australia sells A$500M in 2047 bonds, avg yield 3.4359%, bid to cover 2.53X

(AU) Australia Q4 PPI Q/Q: 0.6% v 0.2% prior; Y/Y: 1.7% v 1.6% prior

(NZ) New Zealand Jan ANZ Consumer Confidence: 126.9 v 121.8 prior

(NZ) New Zealand Dec Net Migration: 5.70K v 5.61K prior

(NZ) New Zealand Dec Building Permits M/M: -9.6% v +9.6% prior

China/Hong Kong

Hang Seng opened -0.2%, Shanghai Composite -0.8%

Hang Seng Energy Index +2.6%, Materials +1.1%; Telecom -0.7%

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.2885 V 6.3045 PRIOR

(CN) China PBoC: Skips OMO (7th straight session) v skipped prior; - For the week, the PBoC drained a net of CNY760B v CNY320B net drain w/w

(CN) According to China Securities Times Commentary piece the yuan (CNY) rate becomes less predictable

(CN) Researchers see China keeping benchmark interest rate unchanged (in line with recent reports) – China Daily

Japan

Nikkei 225 opened -0.5%; Closed -0.9%

TOPIX Real Estate Index -0.9%

Nomura [8604.JP]: Declines over 2.5% after reporting Q3 results

Sony [6758.JP]: Says CEO Hirai to become Chairman and CFO Yoshida to become CEO, effective April 1st

(JP) BOJ announcement related to daily bond buying operation: To buy ¥450B in 5-10 yr JGBs vs ¥410B prior; Offers to buy unlimited amount of 10-yr JGBs at 0.11% in special fixed-rate operation

(JP) BoJ: Again no takers in 5-10 year JGB fixed-rate buying operation [**Note: There were also no bidders in the prior fixed-rate operation held in July 2017]

(JP) Japan Monetary Base Y/Y: 9.7% v 11.2%e prior

(JP) Japan Chief Cabinet Sec Suga: No plan for US Vice President Pence to meet with Finance Min Aso when he visits Japan from Tuesday Feb 6th; No plans to resume Japan-US economic dialogue during Pence's visit next week.

Korea

Kospi opened -0.1%

Chip makers trade lower: Samsung Electronics and Hynix decline by over 3%

North America

US equities ended mixed: Dow +0.1%, S&P500 -0.1%, Nasdaq -0.4%, Russell 2000 +0.3%

S&P500 Real Estate -1.8%, Utilities -1.6%; Energy +1%, Financials +0.9%

Apple [AAPL]: Gained over 3% in the afterhours: Reports Q1 $3.89 v $3.82e, Rev $88B v $86.3Be; Guides Q2 Rev $60-62B v $65.4Be; Q1 iPhone shipments 77.3M v 78.3M y/y (v 80Me)

Amazon [AMZN]: Gained over 6% in the afterhours: Reports Q4 $3.75 v $1.85e, Rev $60.5B v $60.0Be; Guides Q1 Rev $47.8-50.8B v $48.9Be

Alphabet [GOOGL]: Declines over 2% in afterhours: Reports Q4 $9.70 adj v $10.12e, Rev $25.8B (ex $6.45B TAC) v $25.7Be; authorizes $8.6B repurchase of Class C capital stock

AT&T [T]: Said to have hired Bank of America to help examine divestiture of data center business - US financial press

(US) House mulling vote next week on stopgap spending bill to fund govt through March 22nd - Politico

Europe

(EU) ECB's Nowotny: we are now in a situation where we should end asset purchase program; Halting asset purchase program will bring a rise to long-term interest rates; ECB will decide on the future of the asset purchase program by Sept - press

(EU) Some ECB officials reportedly would like clearer interest rate guidance on concerns that vague language will increase market volatility – press

(UK) PM May advisers reportedly considering customs union deal following Brexit – press

(UK) BOE's Brazier: BOE wants to put insurance companies and pension funds through stress simulations

(DE) Germany CSU Scheuer (Bavaria): 'Large' barriers remain in Germany government talks [**Note: The comments follow the government talks in Berlin]

Deutsche Bank [DBK.DE]: CFTC orders Securities unit to pay $70M penalty in relation to alleged attempted manipulation of US dollar (USD) ISDAFIX benchmark swap rates - US financial press

Levels as of 01:00ET

Hang Seng flat; Shanghai Composite -0.4%; Kospi -1.6%

Equity Futures: S&P500 -0.1%; Nasdaq100 +0.5%, Dax -0.2%; FTSE100 flat

EUR 1.2488-1.2519 ; JPY 109.23-109.71; AUD 0.7994-0.8046 ;NZD 0.7362-0.7406

Feb Gold +0.2% at $1,350/oz; Feb Crude Oil +0.5% at $66.11/brl; Mar Copper flat at $3.215/lb

10Y US Treasury Yield Rose By 7Bp To 2.79%

Market movers today

In the US the January jobs report is due out , which we expect to show that employment has continued to rise. Focus remains on average hourly earnings growth (we expect 0.2% m/m), as the missing wage pressure despite the tight labour market is still one of the big puzzles. If the growth in average hourly earnings surprises on the upside, it will, in our view, add fuel to the reflation theme in the financial markets.

Italian January CPI inflation is released, which we expect to have dropped to 0.8% due to energy price base effects. Core inflation will likely continue to be depressed by changes to university education fees which is currently distort ing the true picture of underlying inflation pressures in the economy.

Both ECB’s Coeuré and Fed’s Williams (voter, neutral) are speaking today.

In Norway, unemployment figures for January are out.

Selected market news

The Fixed Income market continued to set the agenda in the global financial markets yesterday, 10Y US Treasury yield rose by 7bp to 2.79%, the highest level since March 2014. The market also continued to revise up Fed expectations, and a March Fed hike is now priced by 95% and almost three full hikes are now priced for 2018. Hence, the market is now getting close to our own forecast for the Fed. The whole US curve bear-steepened as the 2Y bond rose only 2bp and the 30Y rose close to 8bp. Hence, the curve-flat tening we have witnessed in the US came to halt at least temporarily, and noteworthy, 30Y US Treasury yields broke the 3.0% line for the first time in eight months. Note that break-evens (inflation expectations) also moved higher, but not to the same degree, and real-yields also moved higher. The US labour market report today could be decisive for whether we will see a continued bear market in the next couple of days.

There were probably no single explanation behind the FI moves yesterday. In respect of key numbers the ISM manufacturing was in fact marginally down to 59.1 from 59.3 though it was stronger than the consensus forecast . But the employment index saw a big drop to 54.2 from 58.1. Momentum and profit -taking on US flattening trades could also be an explanation.

There has also been a lot of focus on the JGB market and speculations that the BoJ would drop the current yield control policy that intend to keep 10Y JGB yields close to zero especially as the JGB buying at recent auctions have been in the low end. However, this morning the BoJ offered for the first time since July last year to buy unlimited amount of bonds from the market. This time at 0.11%. The strong signal from BoJ should help calm the market today.

The higher yields despite being part of a positive reflation story for the US economy weighed on US equity markets and after a positive opening sentiment turned and Nasdaq ended marginally lower, whereas Dow Jones saw a small positive closing. But nothing dramatic and importantly VIX volatility actually fell slightly after the ‘spike’ earlier in the week. The US dollar got little help from the higher US yields and EUR/USD is back above 1.25.

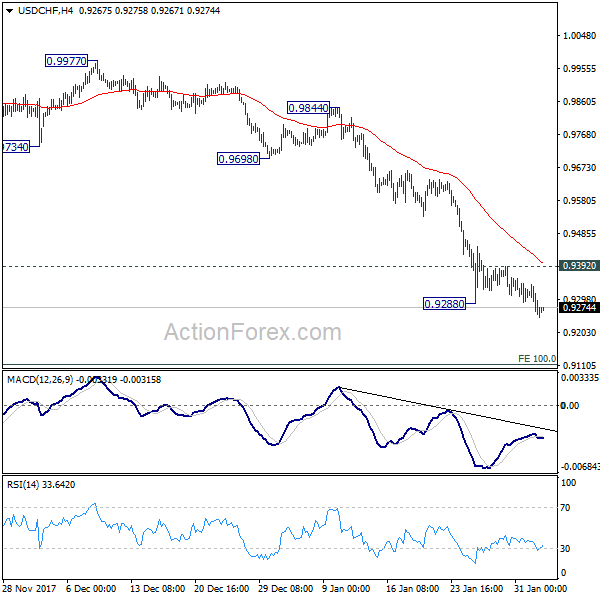

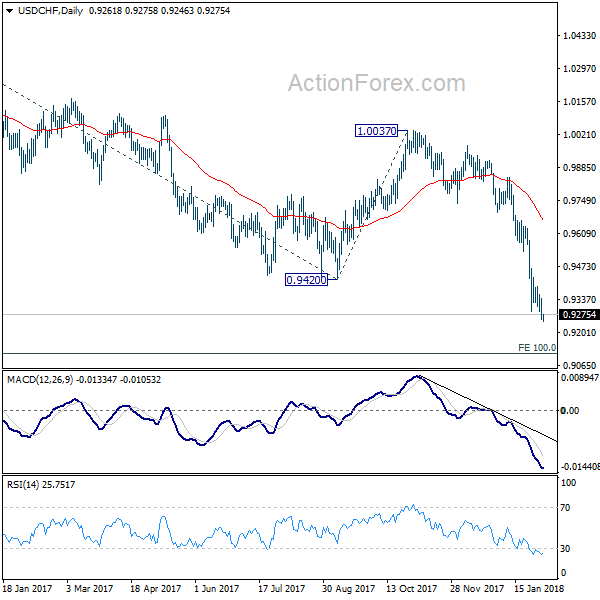

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9232; (P) 0.9287; (R1) 0.9317; More...

USD/CHF's break of 0.9288 indicates recent decline has resumed. Intraday bias is back on the downside. Current fall from 1.0037 should now extend to next key fibonacci level at 0.9115. On the upside, break of 0.9392 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

Dollar Mixed ahead of NFP, Sterling Remains Strongest on Rate Bets

Dollar is trading generally higher in early US session as markets await job data from US. But for the week, Dollar is clearly mixed. In particular, the greenback is under some selling pressure against European majors and Canadian Dollar. EUR/USD, with yesterday's rebound, is back pressing 1.25 handle. Markets are expecting 180k growth in NFP in January. Other employment related data supports this healthy NFP number. Focus will again be on wage growth as average hourly earnings are expected to rise 0.3% mom.

Atlanta Fed predicts 5.4% annualized growth in Q1

According to Atlanta Fed's latest forecast, US GBP is set to rise at a stellar 5.4 annualized rate in Q1. If realized, that will be the best quarter since the global financial crisis. However, the accuracy of the forecast model is always under criticism. For example, back in 2017, Atlanta Fed's tracker predicted 3.4% growth in Q1 but it eventually turned out to be just 1.2% in the final reading. Some economists pointed to the 3.1% prediction of New York Fed's model as a more realistic, yet optimistic forecast.

UBS predicts May BoE hike, conditional on Brexit deal

Sterling continues to trade as the strongest one for the week as supported by rate hike bets. UBS brought forward their forecasts of next BoE hike to May, subject to Brexit transition deal. In a report published earlier this week, strategist John Wraith noted that the new forecast is "explicitly conditional". Also, he warned that "to be clear, while we are now revising our forecast to incorporate another rate hike we did not previously anticipate, we continue to believe the MPC took a risk with the U.K. economy by raising rates in November, and would be compounding this by doing so again in May."

BoJ offered to buy unlimited JGBs

BoJ conducted a special bond purchase operation today, offering to buy an "unlimited" amount of long-term JGBS. That's the first time in six months that such special operations were conducted. On the top of that, the purchase of 5- to 10- years JGBs was also raised from PY 410b to JPY 450b. It's seen by the markets as a pre-emptive move to fend off rise in JGB yields, which was taken higher by global counterparts in recent weeks.

On the data front

New Zealand building permits dropped -0.6% mom in December. Japan monetary base rose 9.7% yoy in January. Australia PPI rose 0.6%, 1.7% yoy in Q4. UK will release construction PMI while Eurozone will release PPI in European session. US will release non-farm payrolls, factor orders and U of Michigan sentiment final.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9232; (P) 0.9287; (R1) 0.9317; More...

USD/CHF's break of 0.9288 indicates recent decline has resumed. Intraday bias is back on the downside. Current fall from 1.0037 should now extend to next key fibonacci level at 0.9115. On the upside, break of 0.9392 minor resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Dec | -9.60% | 10.80% | 9.60% | |

| 23:50 | JPY | Monetary Base Y/Y Jan | 9.70% | 11.00% | 11.20% | |

| 0:30 | AUD | PPI Q/Q Q4 | 0.60% | 0.40% | 0.20% | |

| 0:30 | AUD | PPI Y/Y Q4 | 1.70% | 1.20% | 1.60% | |

| 9:30 | GBP | Construction PMI Jan | 52 | 52.2 | ||

| 10:00 | EUR | Eurozone PPI M/M Dec | 0.20% | 0.60% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Dec | 2.30% | 2.80% | ||

| 13:30 | USD | Change in Non-farm Payrolls Jan | 180K | 148K | ||

| 13:30 | USD | Unemployment Rate Jan | 4.10% | 4.10% | ||

| 13:30 | USD | Average Hourly Earnings M/M Jan | 0.30% | 0.30% | ||

| 15:00 | USD | Factory Orders Dec | 0.90% | 1.30% | ||

| 15:00 | USD | U. of Mich. Sentiment Jan F | 95 | 94.4 |