Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2375; (P) 1.2424 (R1) 1.2463; More....

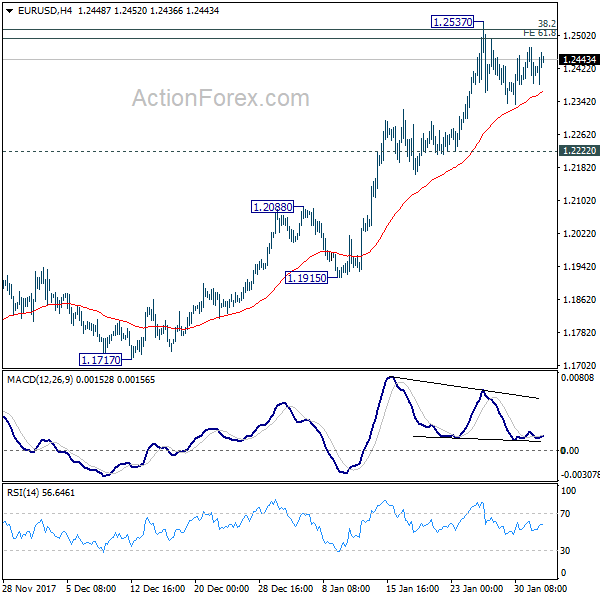

Intraday bias in EUR/USD remains neutral as consolidation from 1.2537 is extending. As long as 1.2222 support holds, near term outlook remains bullish. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

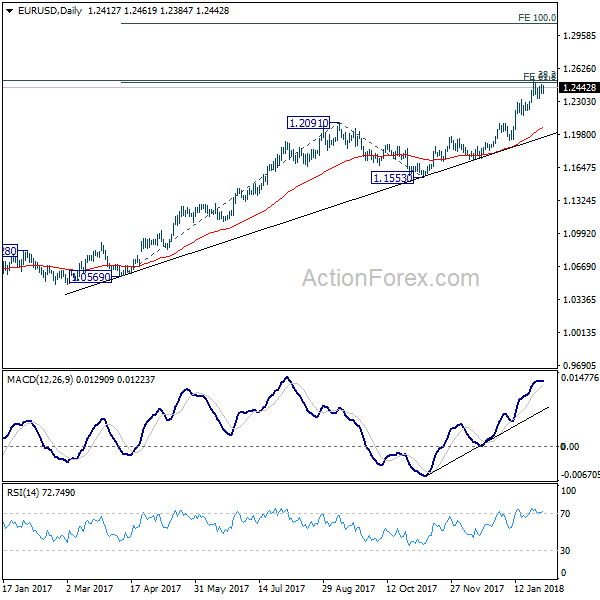

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

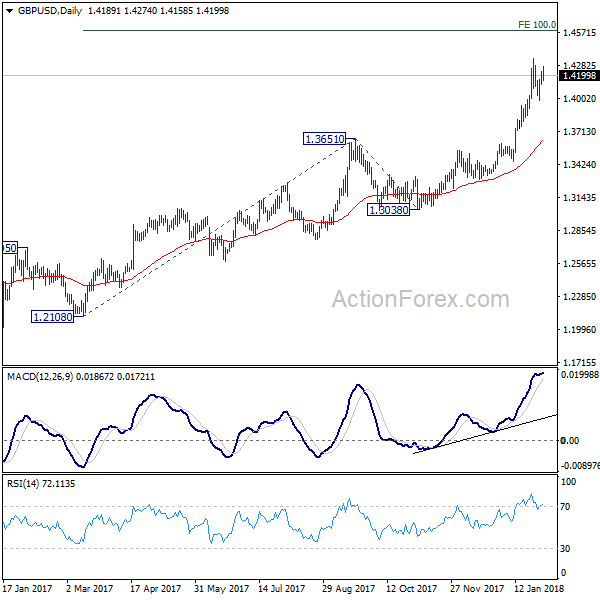

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4131; (P) 1.4181; (R1) 1.4243; More.....

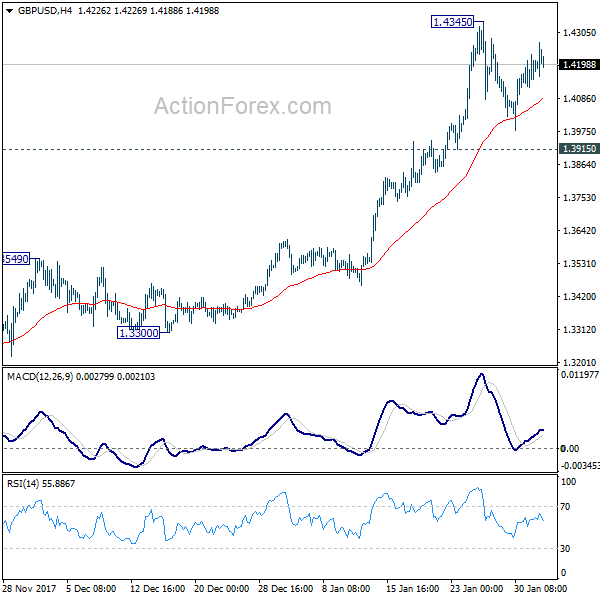

GBP/USD's consolidation from 1.4345 is still in progress. Intraday bias remains neutral for the moment. In case of another fall, downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

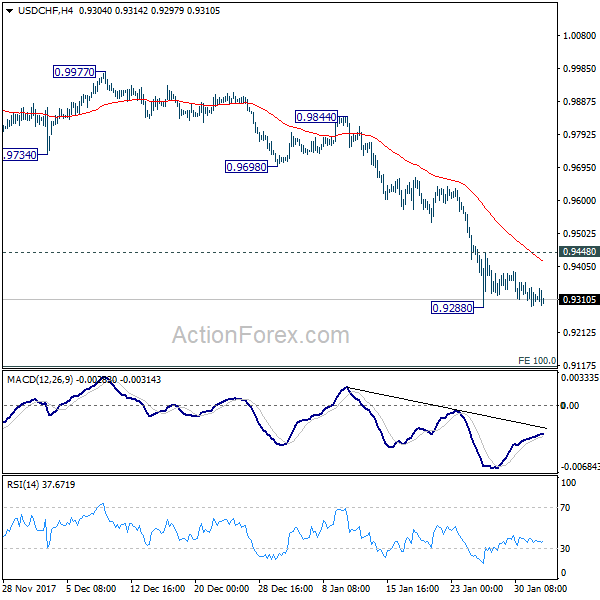

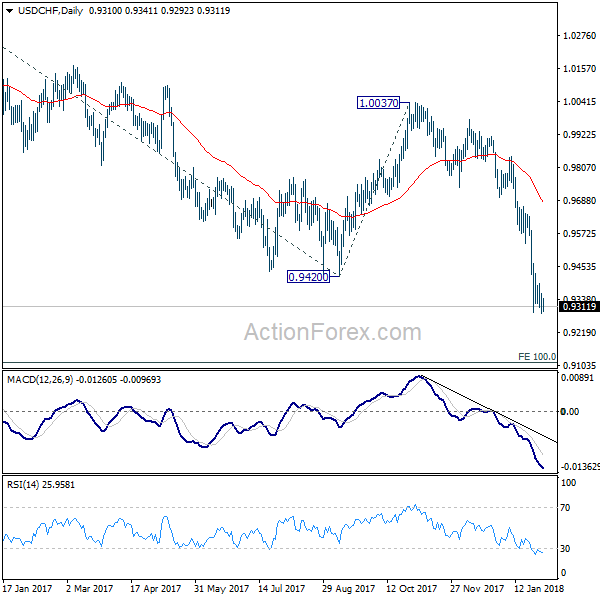

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9281; (P) 0.9320; (R1) 0.9350; More...

No change in USD/CHF's outlook as consolidation from 0.9288 continues. Intraday bias stays neutral. As long as 0.9448 resistance holds, another decline is expected. Break of 0.9288 will extend larger down trend to next key fibonacci level at 0.9115. Nonetheless, break of 0.9448 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.69; (P) 109.07; (R1) 109.54; More...

USD/JPY's recovery continues today but is staying well below 110.18 resistance. Intraday bias remains neutral and outlook stays bearish. That is, deeper decline is still expected. On the downside, break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

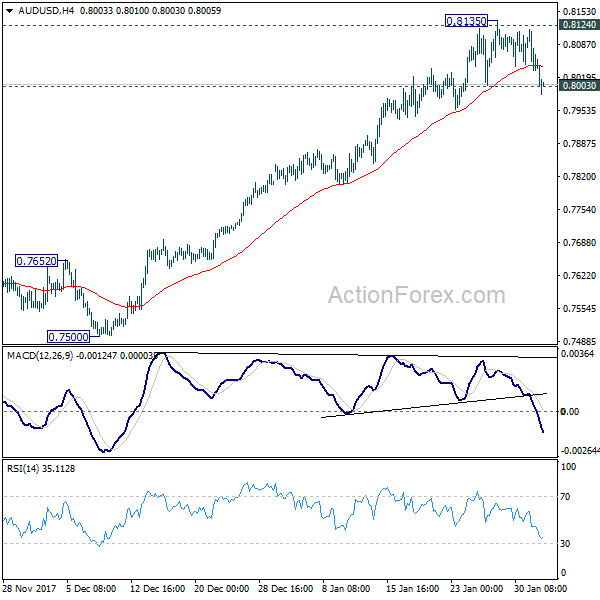

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.8021; (P) 0.8069; (R1) 0.8104; More...

AUD/USD's decline today and break of 0.8003 minor support suggests that a short term top is formed at 0.8135, on bearish divergence condition in 4 hour MACD. That also came after failing to sustain above 0.8124 resistance. Intraday bias is turned back to the downside for 55 day EMA (now at 0.7851). At this point, we'd expect strong support from there to bring rebound. But sustained trading below the EMA will bring retest of 0.7500 key near term support. On the upside, sustained break of 0.8124 will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451.

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside and bring reversal. Break of 0.7500 support will indicate that the medium term trend has reversed.

Dollar Continues to Trade Mixed, Initial Jobless Claims Dropped to 230k

Dollar continues to trade mixed in today as markets are holding their bets ahead of tomorrow's non-farm payrolls report. Data from US today are positive. Initial jobless claims dropped 1k to 230k in the week ended January 27. Challenger job cuts showed -2.8% yoy decline in planned layoffs. But, also despite yesterday's slightly hawkish FOMC statement, there is no sign of sustainably buying in the greenback yet.

Elsewhere in the forex markets, Euro is trading as the strongest one as supported by optimistic economic outlook. Sterling follows closely as the second strongest today. Aussie is trading as the weakest one as dragged down by iron ore price. Iron ore attempted at 80 handle twice since last September but failed. For the near term, it could have peaked back in January.

UK May: A golden era in relationship with China

UK Prime Minister is in China visiting President Xi Jinping today. At a joint press conference, May said that UK and China are enjoying a "golden era" in the relationship. May wanted to "take further forward the global strategic partnership that we have established". Chinese Premier Li Keqiang promised yesterday to open up its markets to UK including agricultural products and financial services. And May is expecting business deals at up to GBP 9b to be signed during the visit.

Separately, May told reporters that "there's a difference between those people who came prior to us leaving and those who will come when they know the U.K. is no longer a member of the EU." That is, EU citizens going to UK during and after the transition period will have difference rights than the prior ones. However, European Parliament's chief Brexit spokesman Guy Verhofstadt insisted that "citizens' rights during the transition is not negotiable."

UK PMI manufacturing dropped to seven month low

UK PMI manufacturing dropped to 55.3 in January, down from 56.2 and missed expectation of 56.5. That's the lowest level since June 2017 but nonetheless, stayed well above long-run average at 51.7. Markit noted in the release that "the UK manufacturing sector reported an unwelcome combination of slower growth and rising prices at the start of 2018." However, "encouragingly, despite the slowdown, the latest survey is consistent with production rising at a solid quarterly rate of around 0.6% in January, with jobs also being added at a faster pace." But, "the trend in demand will need to strengthen in the near-term to prevent further growth momentum being lost in the coming months.'

ECB Praet: An ample degree of stimulus needed

ECB Chief Economist Peter Praet reiterated his cautious stance regarding stimulus exit. He said today that "we have not yet accomplished our mission: with inflation convergence proceeding only gradually, patience and persistence in our monetary policy remain warranted." And, "inflation developments remain subdued...and we are still some distance away from meeting the Governing Council's criteria for a sustained adjustment in the path of inflation". Therefore, "overall, an ample degree of monetary stimulus remains necessary.

In an interview with Irish RTE broadcast, ECB Executive Board member Benoit Coeure talked about recent comments by US Treasury Secretary Steven Mnuchin's comment that a weaker dollar is welcomed. Mnuchin's comment triggered steep selloff in Dollar and in turn pushed Euro up. Coeure echoed ECB President Mario Draghi's stance to "keep to what we've agreed in the relevant fora, which is we're not targeting exchange rates". But he warned that if what the US is doing would affect ECB's chance of meeting its own mandate of price stability, ECB could be forced to response. He said that "we've seen quite some volatility recently. If that kind of volatility would lead to an unwarranted tightening of our monetary policy, we would have to reassess and consider.

Release from Europe, Eurozone PMI manufacturing was finalized at 59.6 in January, unrevised. Germany PMI manufacturing was finalized at 61.1, revised down by 0.1. France PMI manufacturing was finalized at 58.4, revised up by 0.3. Italy PMI manufacturing rose to 59. Swiss PMI manufacturing rose to 65.3 in January. Swiss retail sales rose 0.6% yoy in December. SECO consumer confidence improved to 5 in January.

China Caixin PMI manufacturing showed resilience

China Caixin PMI manufacturing was unchanged at 61.6 in January, meeting expectations. The survey showed resilience in the small to mid-sized manufacturing sector in the country. Zhengsheng Zhong, director of macroeconomic analysis at CEBM Group, a subsidiary of Caixin, noted that "the manufacturing industry had a good start to 2018. Going forward, we should keep a close eye on the stability of the demand side."

Also from Asia pacific, Australia import price index rose 1.5% qoq in Q4. Building approvals dropped sharply by -20% mom in December. Japan PMI manufacturing was revised up by 0.4 to 54.8 in January.

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.8021; (P) 0.8069; (R1) 0.8104; More...

AUD/USD's decline today and break of 0.8003 minor support suggests that a short term top is formed at 0.8135, on bearish divergence condition in 4 hour MACD. That also came after failing to sustain above 0.8124 resistance. Intraday bias is turned back to the downside for 55 day EMA (now at 0.7851). At this point, we'd expect strong support from there to bring rebound. But sustained trading below the EMA will bring retest of 0.7500 key near term support. On the upside, sustained break of 0.8124 will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451.

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside and bring reversal. Break of 0.7500 support will indicate that the medium term trend has reversed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Import price index Q/Q Q4 | 1.50% | 1.50% | -1.60% | |

| 00:30 | AUD | Building Approvals M/M Dec | -20.00% | -7.60% | 11.70% | 12.60% |

| 00:30 | JPY | PMI Manufacturing Jan F | 54.8 | 54.4 | ||

| 01:45 | CNY | Caixin PMI Manufacturing Jan | 51.5 | 51.5 | 51.5 | |

| 06:45 | CHF | SECO Consumer Confidence Jan | 5 | 2 | -2 | |

| 08:15 | CHF | Retail Sales Y/Y Dec | 0.60% | 1.50% | -0.20% | |

| 08:30 | CHF | PMI Manufacturing Jan | 65.3 | 64.1 | 65.2 | |

| 08:45 | EUR | Italy Manufacturing PMI Jan | 59 | 57.3 | 57.4 | |

| 08:50 | EUR | France Manufacturing PMI Jan F | 58.4 | 58.1 | 58.1 | |

| 08:55 | EUR | Germany Manufacturing PMI Jan F | 61.1 | 61.2 | 61.2 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Jan F | 59.6 | 59.6 | 59.6 | |

| 09:30 | GBP | PMI Manufacturing Jan | 55.3 | 56.5 | 56.3 | 56.2 |

| 12:30 | USD | Challenger Job Cuts Y/Y Jan | -2.80% | -3.60% | ||

| 13:30 | USD | Nonfarm Productivity Q4 P | -0.10% | 1.10% | 3.00% | 2.70% |

| 13:30 | USD | Unit Labor Costs Q4 P | 2.00% | 1.00% | -0.20% | -0.10% |

| 13:30 | USD | Initial Jobless Claims (JAN 27) | 230K | 236K | 233K | 231K |

| 14:45 | USD | Manufacturing PMI Jan F | 55.5 | 55.5 | ||

| 15:00 | USD | Construction Spending M/M Dec | 0.40% | 0.80% | ||

| 15:00 | USD | ISM Manufacturing Jan | 58.6 | 59.7 | ||

| 15:00 | USD | ISM Prices Paid Jan | 69.5 | 69 | ||

| 15:30 | USD | Natural Gas Storage | -288B |

Spot Gold Under Pressure after Hawkish Fed but Downside is Still Limited by Rising 20SMA

Spot Gold price eased on Thursday, pressured by hawkish comments from Fed which improved the outlook and boosted hopes for further rate hikes this year. The price returned below 10SMA (1342) after recovery attempts were repeatedly capped at $1347 zone, but remains within $1332/47 congestion which extends into third day and showing no clear near-term direction while the price holds in this range. Rising 20SMA ($1334) reinforces support and so far keeps the downside protected. Daily MA's are still in bullish setup but descending RSI/Momentum continue to warn of further easing. Sustained break below $1334/30 support zone (20SMA/pullback low/Fibo 61.8% of $1308/1365 upleg) is needed to generate stronger bearish signal for deeper correction of $1236/$1366, 12 Dec/25 Jan rally) which would expose targets at $1324 (18 Jan trough) and $1316 (Fibo 38.2% of $1236/$1366 rally) in extension. Bullish scenario requires firm break above $1347 congestion top to neutralize immediate downside risk.

Res: 1347; 1350; 1353; 1357

Sup: 1337; 1334; 1332; 1330

Dollar Rallies Versus Yen on Inflation Prospects; European Stocks Rebound

Here are the latest developments in global markets:

FOREX: Dollar/yen stretched towards a one-week high of 109.74 (+0.51%) during early European trading after the FOMC statement highlighted yesterday that the US inflation is expected to "move up this year". However, the dollar index inched down to 89.00, remaining near 3-year lows, on the face of a strengthening euro and pound. Euro/dollar crawled up to 1.2450 (+0.14%) amid prospects that the ECB will reduce monetary stimulus this year and pound/dollar was on track to post gains for the third consecutive day, surging to 1.4273 (+0.27%). On Tuesday, the BOE Governor, Mark Carney, acknowledged the strength of the economy and said that the focus was turning to inflation. Aussie/dollar dipped into further losses towards a one-week trough of 0.7992, harmed by worse-than-expected readings on Australian building approvals.

STOCKS: Encouraging earnings results helped European stocks to erase yesterday's losses on Thursday. The benchmark European STOXX 600 was up by 0.50% at 1000 GMT, underpinned by gains in the tech, utility and financial sectors, while the blue-chip Euro STOXX 50 increased by 0.40%, with energy shares leading the index's gains. The Italian FTSE MIB jumped by 1.0%, the French CAC 40 rose by 0.46% and the German DAX 30 moved up by 0.38%. The British FTSE 100 edged up by 0.06%.

COMMODITIES: Oil prices rallied after a survey noted that OPEC's commitment to curb supply remains in place, despite increases in US production. WTI crude surged to an intraday high of $65.42/barrel (+0.96%) and Brent hit a top at $69.67/barrel (+ 1.06%). Gold slipped to a low of $1338/ounce (-0.50%).

Day ahead: US initial Jobless claims & ISM Manufacturing PMI eyed

For the remainder of the day, the calendar will feature US data, with attention turning mainly to initial jobless claims (1330 GMT) and ISM manufacturing PMI readings (1500 GMT).

In the week ending January 26, analysts expect that 238,000 people applied for unemployment benefits for the first time compared to 233,000 seen in the preceding week, reflecting a strong labor market as long as the measure continues to remain below the threshold of 300,000 that is linked to a strong jobs market.

The Institute for Supply Management (ISM) will release stats on manufacturing activity for the month of January. The index is expected to inch down by 0.9 points to 58.8, though, any print above 50 would indicate that the manufacturing industry is generally expanding.

Other releases that might draw some attention out of the US are Q4 2017 preliminary data on labor costs and productivity (1330 GMT), Markit's final reading on January manufacturing PMI (1445 GMT), December construction spending figures (1500 GMT) and January's total vehicle sales (2030 GMT).

On the equities front, corporate giants Alibaba, Amazon, Apple and Google parent Alphabet will be among companies releasing quarterly earnings reports on Thursday.

Canadian Dollar Unchanged, Investors Await NFP, Wage Growth Reports

The Canadian dollar has recorded small gains in the Thursday session. Currently, the pair is trading at 1.2318, up 0.02% on the day. On the release front, there are no major Canadian events. Over in the US, there are two key events. Unemployment claims are expected to rise to 237 thousand, and the markets are forecasting that ISM Manufacturing PMI will slow to 58.7 points. On Friday, the focus will be on US job reports, with the release of wage growth, nonfarm payrolls and the unemployment rate.

Will NAFTA survive past March? Negotiators are working against a self-imposed deadline to wrap up talks by March, with limited progress. The latest round of negotiations over NAFTA ended in Montreal last week, and there were no breakthroughs. Still, the sides continue to talk, and a Merrill Lynch has lowered the odds of the United States leaving the pact to 25 percent. The US has demanded far-reaching concessions from Canada and Mexico, such as shifting more auto production to the US. Canada and Mexico are strongly opposed to the US demands, but both economies would take a sharp hit if NAFTA is terminated. At the same time, many US businesses don't want to blow up NAFTA and are pressuring President Trump to remain in the trade pact. The next round of negotiations is scheduled for late February in Mexico.

The Federal Reserve held the course on interest rate policy on Wednesday, as expected. In the rate statement, policymakers said that they expected the economy to continue to expand at a moderate pace and that the labor market would remain strong in 2018. What was more noteworthy was that the Fed predicted that inflation would rise to the Fed's 2 percent target this year. This marks an upgrade in the inflation forecast, as the December statement said that inflation was expected to "remain somewhat below 2 percent." Higher inflation is likely to open the door to tighter monetary policy, and the Fed appears on track for three, or even four rate hikes in 2018, assuming that the US economy remains strong. This policy meeting was the last under Janet Yellen, as Jerome Powell will take over as Fed chair on February 3. The slightly hawkish tone of the rate statement has raised the odds of a rate hike to 83% when the Fed next meets in March.

Dollar Depressed Despite Hawkish Fed, Gold Dips

It's remarkable how the Dollar remains depressed and unloved, despite the Federal Reserve expressing optimism over increased inflationary pressures as the year moves on.

Although the U.S. Federal Reserve left rates unchanged as expected in January, the relatively upbeat appraisal of the economy and rising inflation expectations offered a hawkish touch. The fact that the Dollar remains pressured following the hawkish Fed meeting, continues to suggest that other key fundamental drivers are impacting the currency. As Janet Yellen prepares to pass the baton of leadership to Jerome Powell, there are widespread discussions over how this will impact the Dollar, current monetary policy and the U.S. economy.

While it may be too early to predict how the FOMC under Powell's leadership could impact the U.S. economy it obviously breeds uncertainty, resulting in a weaker Dollar. It must be kept in mind that there are many new Fed governors on board as well, and the new Fed Chair is a lawyer by practice, not an economist. Although the central bank may avoid obstacles further down the road by following the status quo, there could be some issues if the U.S. economy experiences unexpected shocks.

Other themes that continue to punish the Dollar revolve around political uncertainty in Washington and concerns over the United States' stance on global trade. With the prospects of other major central banks gradually tightening monetary policy also adding to the mix and denting buying sentiment, further losses could be on the cards for the U.S. Dollar.

Taking a look at the technical picture, the Dollar Index remains heavily bearish on the daily charts. There have been consistently lower lows and lower highs, while the MACD trades to the downside. Sustained weakness below the 89.00 level may encourage a decline towards 88.50 and 88.00, respectively.

Currency spotlight - GBPUSD

Sterling edged lower during Thursday's trading session, after weaker-than-expected data from Britain's manufacturing sector weighed on sentiment. The U.K's manufacturing sector activity fell in January to 55.3, from 56.2 in December. This disappointing report is likely to instill bears with fresh inspiration to attack the British Pound.

Focusing on the technical outlook, the GBPUSD continues to find support in the form of Dollar weakness on the daily charts. A decisive breakout and daily close above 1.4230 could encourage an incline higher towards 1.4300. Alternatively, a failure of prices to keep above the 1.4230 may inspire a move back towards 1.4110 and 1.4000.

Commodity spotlight - Gold

Gold found itself under noticeable selling pressure on Thursday, with prices dipping below $1340 after the Federal Reserve hinted of more rate hikes taking place this year.

While further losses could be witnessed in the short term, a vulnerable U.S. Dollar is likely to cushion the yellow metal's downside. Gold remains bullish on the daily charts and is poised to venture higher, if the NFP report, that is due for release on Friday, fails to meet market expectations. From a technical perspective, Gold remains in the process of creating a new higher low. Sustained weakness below $1335 may invite a decline back towards $1324.15. Alternatively, an intraday breakout above $1340 may open a path towards $1360.