Sample Category Title

Fed Leaves Rates Steady in Yellen’s Last Meeting as Chair

As widely expected, the Federal Open Market Committee (FOMC) held the target range for the federal funds rate unchanged between 1-1/4 and 1-1/2 percent.

The Fed's views appear little changed from the mid-December meeting round, with only minor wording changes in the policy statement.

The economy was seen as having improved, having posted "gains" in employment, spending, and business investment. Moreover, the unemployment rate was seen as remaining "low." References to fluctuations related to hurricane activity were taken out of the statement.

While overall inflation was believed to continued to run "below 2 percent," the statement outlined the FOMC's expectation that inflation will "move up this year." Moreover, the Fed also acknowledged the improvement in expectations, stating that market-based measures "increased in recent months" while still warning that they "remain low."

As before, the Fed telegraphed future adjustments to the stance of monetary policy. However, the word "further," was added with the FOMC now expecting that "further gradual increases in the federal funds rate" are warranted.

After the double-dissent in December, the status-quo decision and the slightly more hawkish statement was embraced by all the voting members. It is worth noting that the voting membership has changes slightly this year with the exit of the Federal Bank Presidents of Chicago, Dallas, Minneapolis, and Philadelphia, with their places taken over by Presidents from Atlanta, Cleveland, Richmond, and San Francisco. While the Atlanta and Richmond Presidents are newcomers, with their views little publicized so far, the exit of the typically-dovish Minneapolis and Chicago and entry of the typically-hawkish Cleveland has tilted the FOMC slightly to the hawkish side.

Key Implications

This statement was largely of a vanilla-variety, acknowledging the improvement in the economy and inflation expectations in recent weeks, with the only surprise being the addition of the word "further" in front of "gradual increases." On the face of it, this addition suggest that the Fed is preparing to raise rates at its next meeting in mid-March and wants the markets to be ready. This is unlikely to cause much volatility, with the March hike already largely priced in.

This was Chair Yellen's last meeting at the helm of the Federal Reserve. While her Chairmanship lacked significant new policy initiatives, her steady hand at the helm and cool execution of the balance sheet wind down deserves praise. Moreover, the important legacies that she leaves the Fed with are twofold. For one, she has convinced the remainder of the FOMC that the unemployment rate is in and of itself not a perfect measure of labor market slack, with her focus on other forms of underemployment particularly helpful. Secondly, she has managed to change the mind of many of her colleagues as far as the neutral rate, which has come down steadily from near 4% at the beginning of her tenure to about 2.75% at its end. These are both important concepts, which together have led to better policy during her tenure – allowing the economy to improve further given the very gradual rate hikes.

Policy is unlikely to diverge substantially going forward despite Chair Yellen's exit. Chair Powell, who takes over on Saturday, appears to be of a similar mindset to his predecessor and is unlikely to diverge from the gradual path set forth by the Yellen Fed. However, his appointment comes at a critical juncture for the Fed, as it faces a tight labor market coupled with stimulus coming from fiscal policy. It will not be an easy job and we wish him all the best.

USD/CAD Canadian Dollar Higher After Strong GDP And Persistent USD Weakness

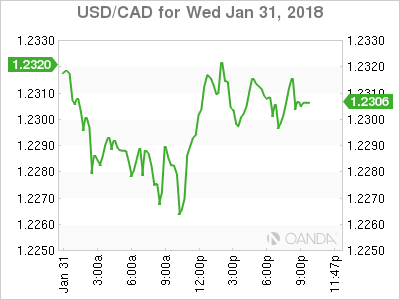

The Canadian dollar is higher on Wednesday after the economy accelerated its growth in November. Canadian GDP is posted monthly and showed a gain of 0.4 percent in November. The Canadian economy started 2017 with a bang which led the Bank of Canada (BoC) to raise rates twice before a slowdown in the third quarter. The two 25 basis points rate hikes, the overall strength of the economy, recovery energy prices and a soft US dollar continued to boost the loonie. In 2018 the BoC has hiked once more leaving the benchmark rate at 1.25 percent.

The Canadian currency has enjoyed a strong start to 2018 and is more than 2 percent higher than the USD year to date. The political uncertainty in the US that delayed pro-growth policies until the end of 2017 remain. The fate of NAFTA has kept the Canadian dollar under pressure as the end of the original timeline fast approaches. The negotiations have shown little progress and with only two rounds to go, the end result could be all parties walking away empty handed. Elections in Mexico and the United States this year will further complicate negotiating in such a divisive topic as trade.

The USD/CAD lost 0.24 percent on Tuesday. The currency pair is trading at 1.2304, a four month high, after the release of the monthly gross domestic product in Canada for November. The 0.4 percent gain is the biggest gain since May 2017 and a signal that growth is back on track after a slowdown in the third quarter.

The U.S. Federal Reserve kept its benchmark interest rate at 1.25 – 1.50 percent on Wednesday. The meeting will mark the last time for Janet Yellen as Chair of the central bank. Jerome Powell will take over next week and with no meeting scheduled for February the Fed is expected to lift rates in March to mark the start of the Powell era.

Prime Minister Justin Trudeau told the CBC earlier that he does not think the US will pull out of NAFTA. The PM is aware that it is a possibility and his government is working on contingency plans. Also today US Secretary of Commerce Wilbur Ross said that the renegotiations are far from being completed at this point. He did recognize that progress has been made, but very little of it in the hard issues.

During his first State of the Union address President Trump mentioned that the US had entered into unfair trade deals and his goal was to turn that page on that period. Pro-growth policies were late to arrive, but after the tax reform gave Trump his first policy victory he intends to build on it by proposing a 1.5 trillion dollar infrastructure spending legislation.

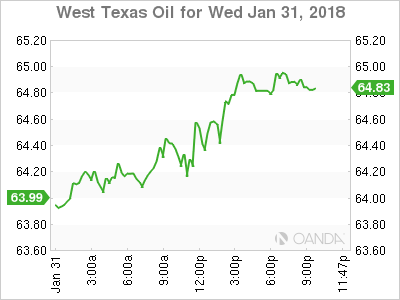

Oil prices are recovering from a drop earlier in the session. West Texas Intermediate is trading at $64.55. The weekly US crude inventories report by there Energy Information Administration (EIA) surged by 6.8 million barrels. The forecast was a mild 100,000 barrels, but it appears the cold weather has slowed down refineries in the south resulting in the buildup. The surprise to the upside was balanced with a larger than expected drawdown of gasoline stockpiles.

Market events to watch this week:

Thursday, February 1

4:30am GBP Manufacturing PMI

10:00am USD ISM Manufacturing PMI

Friday, February 2

4:30am GBP Construction PMI

Fed Goes ‘Further’

Janet Yellen went out with a whisper in her final FOMC meeting. In January, GBP was the top performer while the US dollar lagged. Australian building approvals are up next. The Premium Video below was recorded ahead of the Fed, highlights the rationale to the latest GBP trades. 6 of the existing 8 trades are currently in profit.

Janet Yellen has never craved the spotlight and she chose to make her departure without any special flourish. The statement didn't offer any strong hints about the path of rates. The main line of guidance called for “further gradual increases” in rates. The addition of the word “further” is a bit puzzling by may have been added to hint at a continuity of policy under Powell.

On inflation, the Fed dropped a reference to below-target inflation in the near-term but the most-notable change might have been a line saying market-implied inflation had increased recently.

Expectations for a hike in March were unchanged but beyond that it remains unclear. Presumably, Yellen wanted to leave the next signal to Powell and that's understandable.

The US dollar initially strengthened after the announcement but later gave back the gains. USD/JPY rose as high as 109.45 but slipped back to 109.18.

On the whole, moves in FX on the day were modest but the loonie was an exception as USD/CAD hit a 5-month low at 1.2251 before rebounding to 1.2312. One reason was a solid +0.4% rise in November GDP. That matched expectations but the climb came on strong manufacturing and that's a reason for optimism in the months ahead.

Another pair to watch is AUD/USD as it slipped to a six-day low. It's been on a tear for the past six weeks and it will bear worth closely watching if this is a bump in the road or deeper retracement. Yesterday's CPI numbers were soft and today building approvals are out. The consensus is for a 7.6% m/m drop after an 11.7% rise prior.

(FED) FOMC Statement January 31, 2018

Information received since the Federal Open Market Committee met in December indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Gains in employment, household spending, and business fixed investment have been solid, and the unemployment rate has stayed low. On a 12-month basis, both overall inflation and inflation for items other than food and energy have continued to run below 2 percent. Market-based measures of inflation compensation have increased in recent months but remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market conditions will remain strong. Inflation on a 12‑month basis is expected to move up this year and to stabilize around the Committee's 2 percent objective over the medium term. Near-term risks to the economic outlook appear roughly balanced, but the Committee is monitoring inflation developments closely.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-1/4 to 1‑1/2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Jerome H. Powell; Randal K. Quarles; and John C. Williams.

Gold Steady Ahead of Fed Rate Statement

Gold has posted slight gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1341.29, up 0.20% on the day. On the release front, ADP Nonfarm Payrolls slowed to 234 thousand, but this was much stronger than the estimate of 186 thousand. As well, Pending Home Sales improved to 0.5%, matching the estimate. Later in the day, the Federal Reserve will release a rate statement, and is expected to hold rates at a range between 1.25% -1.50%. On Thursday, the US releases two key indicators – unemployment claims and the ISM Manufacturing PMI.

Gold is down slightly this week, as the dollar has steadied following last week's USD selloff. Since the start of the year, gold is up 2.2%, joining the major currencies which have posted gains against the greenback in 2018. This has been somewhat of a surprise, as a strong US economy has supported risk appetite, yet investors have not abandoned the yellow metal early in 2018.

The Federal Reserve will be in the spotlight later on Wednesday, with the release of rate statement, the final one under Janet Yellen's watch. The tone of the statement could affect investor sentiment and have a substantial impact on the direction of gold. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.

Pound Gains Continue, Investors Eye Fed Statement

The British pound has posted gains for a second straight day. In Wednesday's North American session, GBP/USD is trading at 1.4207, up 0.40% on the day. On the release front, ADP Nonfarm Payrolls slowed to 234 thousand, but this was much stronger than the estimate of 186 thousand. There was positive news from the housing sector, as Pending Home Sales improved to 0.5%, matching the estimate. Later in the day, the Federal Reserve will release a rate statement, and is expected to hold rates at a range between 1.25% -1.50%. On Thursday, the UK releases Manufacturing Production, while the US will publish unemployment claims and the ISM Manufacturing PMI.

Recent reports have forecast that the British economy will be negatively impacted by Brexit, but someone forgot to tell the bad news to the British pound. The currency has posted a sharp 5.2% gain in January, as the USD selloff saw the dollar's rivals post strong gains. Last week, the pound pushed above 1.43, its highest level since June 2016. On the politial front, Theresa May can only wish that her position was as strong as the pound. The May government is facing strong domestic criticism over its handling of the Brexit negotiations, and the Europeans are in no mood to play softball as the Britain departs the European Union in just over a year.

In the latest Brexit development, the EU has drafted guidelines regarding the transition period after Britain leaves the European Union in 2019. The European proposal calls for Britain to abide by EU rules, including freedom of movement, during the transition period which would last until 2020. However, it's unlikely that the May government will simply accede to this proposal. Britain wants a longer transition period as well as say in the makeup of the transition period.

The Federal Reserve will be in the spotlight later on Wednesday, with the release of rate statement, the final one under Janet Yellen's watch. The tone of the statement could affect investor sentiment and have a substantial impact on the currency markets. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.

Yen Lower Despite Mixed Japanese Numbers

The Japanese yen continues to have an uneventful week. In Wednesday's North American session, USD/JPY is trading at 109.05, up 0.29% on the day. On the release front, Japanese indicators were mixed. Preliminary Industrial Production jumped 2.7%, well above the estimate of 1.5%. However, Housing Starts came in at -2.1%, marking a sixth straight decline. The markets had predicted a gain of 1.1%. Later in the day, Japan releases Final Manufacturing PMI, with an estimate of 54.4 points. In the US, ADP Nonfarm Payrolls slowed to 234 thousand, but this was much stronger than the estimate of 186 thousand. There was positive news from the housing sector, as Pending Home Sales improved to 0.5%, matching the estimate. Later in the day, the Federal Reserve will release a rate statement, and is expected to hold rates at a range between 1.25% -1.50%. On Thursday, the US releases unemployment claims and the ISM Manufacturing PMI.

The Bank of Japan has continually said that it has no plans to end its massive stimulus program, but may have sent its most direct message (warning?) on Wednesday. The Bank increased its purchases of 3-5 year government bonds (JGB), while at the same time senior members were on the offensive. BoJ Governor Haruhiko Kuroda and Deputy Governor Kikuo Iwata said that the Bank would maintain "powerful" easing as long as inflation was well of the BoJ target of 2 percent. Iwata stressed that the BoJ had no plans to change its yield target levels "for the time being". Under current yield curve policy, short-term interest rates are at -0.10% and 10-year government bonds are at 0.0%. The Japanese economy has heated up, raising speculation that the Bank could taper its stimulus program and even raise interest rates. However, the BoJ appears determined to hold the course until inflation moves higher.

All eyes are on the Federal Reserve, which will issue a rate statement later on Wednesday. This will be the final rate statement under Janet Yellen's watch. The tone of the rate statement could affect investor sentiment and have an impact on the currency markets. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.

Silver Struggles Below Symmetrical Triangle Again; More Gains are Expected

Silver has come under strong pressure over the last trading days, in the short to medium-term timeframe, following the pullback on the 17.70 resistance level. The price penetrated to the upside of the symmetrical triangle that was holding since July 2017 and ended several days above the descending trend line. However, on Monday, the price slipped again below the diagonal line.

From the technical point of view, the white metal is developing above the short-term 20 and 40 simple moving averages, and is endorsing again the scenario for further gains. The RSI indicator is pointing to the upside in the positive zone, indicating a bullish signal, whilst the MACD oscillator is losing momentum as it is moving below the trigger line.

If price action remains above 20-day SMA, could open the door for the 17.70 resistance level. This is considered to be a strong resistance area which has been rejected a few times in the past. Rising above it could see prices re-test the 18.20 peak.

If the price fails to jump higher, then the focus would shift to the downside towards 16.70, which stands near the 40-day simple moving average. This is an important level, which if breached, would increase downside pressure and the price would be on the path towards the lower band of the symmetrical triangle at 15.60.

EURJPY Runs Sharply Higher; Bulls Took the Lead

EURJPY has reversed back up again after finding support at the 134.10 barrier during yesterday's trading session. The pair has been developing higher along its current trend line since August 18. Additionally, over the last hours, prices broke above the 135.00 handle and are trading above the short-term moving averages.

The pair is recording a sharp upside movement and the short-term momentum indicators are pointing to a bullish bias. The Relative Strength index (RSI) entered the positive territory and is strengthening its momentum, whilst the MACD oscillator is moving higher in the bearish area above its trigger line.

On the upside, if prices continue the bullish rally, there is scope to test the 136.30 resistance level. Clearing this key level could see additional gains towards the 136.60 obstacle, taken from the high on January 05.

If prices reverse lower, immediate support should come at 23.6% Fibonacci retracement level at 134.40 with the low of 127.45 and the high of 136.60. Below that, the 134.10 is another major support around 134.10, which is holding slightly above the ascending trend line.

Sunset Market Commentary

Markets

Global core bond trading slowed to a trickle today ahead of tonight's FOMC meeting. Both the Bund and the US Note future eke out some gains with end-of-month extension buying playing a minor role. EMU CPI remains low at 1.3% Y/Y for the headline and 1% Y/Y for the core reading, but didn't affect intraday trading dynamics. Strong German and US labour market data couldn't do the trick neither. The US yield curve flattens with yield changes ranging between +0.4 bps (2-yr) and -2.9 bps (30-yr). The German yield curve bull flattens with yields 0.5 bps (2-yr) to 6 bps (30-yr) lower. The significant outperformance of the 30-yr yield is partly technically related following the failed attempt to break above the 2017 top (1.38%). 10-yr yield spread changes versus Germany are barely changed with Greece underperforming (+7 bps). We expect the Fed to leave policy rates unchanged tonight (even though the market implied probability of a hike is 20%), but upgrade its assessment of the economy and inflation thereby paving the way for a March hike. Given market positioning, this could trigger a steepening of the US curve, with room for a short term correction lower in yields at the front end. The US Treasury's announcement (quarterly refunding) that it will halt attempts to extend the maturity of its debt also argues in favour of some steepening as supply will be more directed to the front-and of the curve.

EUR/USD continued trading with a positive bias today. Dollar caution ahead of the Fed policy decision was probably at play. At the same time, the euro remained will bid even as EMU eco data were mixed, at best. EMU (un)employment data confirmed an ongoing improvement in labour market conditions. On the other hand, German retail sales printed soft and EMU inflation (headline 1.3% in January from 1.4%) drifted further away from the 2% ECB target. On the other side of the Atlantic, ADP private job growth was very strong (234 k). The report was completely ignored in EUR/USD trading. The pair trades currently at 1.2450. USD/JPY gained a few ticks an is nearing the 109 barrier. The focus now turns to the Fed statement. An unchanged decision is expected, but the Fed might upgrade its assessment on growth and inflation. Will the Fed's assessment by strong enough to put a floor for the dollar?

Sterling opened strong this morning. Political noise from the UK government continued to linger. However, the UK currency was supported by decent data overnight and, more importantly, by modestly hawkish comments from BoE governor Carney. Yesterday, he indicated that the BoE could give some more weight to inflation in its assessment further out this year. EUR/GBP traded in the 0.8760 area at the start of European dealings. However, gradually some sterling selling kicked in. A big EUR/GBP buying order and end-of month position adjustments were rumoured to be behind the move. Euro strength was a secondary factor, too. EUR/GBP trades in the 0.88 area. USD weakness kept cable in the 1.4150/1.42 area.

News Headlines

EMU Inflation slowed at the start of the year, highlighting the hurdles faced by the ECB as it attempts to foster price growth in a region still beleaguered in places by high unemployment. CPI rose 1.3% Y/Y in January, above 1.2% Y/Y consensus, but down from 1.4% Y/Y. Core CPI picked up from 0.9% Y/Y to 1% Y/Y. The EMU unemployment rate stabilized at 8.7%, matching the lowest level since January 2009. German unemployment extended its decline as companies stepped up hiring to meet buoyant demand. The German jobless rate dropped to a record low of 5.4% in January. The number of people out of work plunged by 25,000 to 2.415 mn (vs -17,000 forecast).

Hiring in the US private sector continued to outperform expectations in January, underscoring the strength of the labour market. Non-farm private sector employers added 234,000 jobs this month, according to a report from payroll processor ADP. The figure easily topped expectations for 185,000 jobs and marks the fourth straight month of 200k+ gains. The Chicago PMI declined from 67.8 to 65.7, beating consensus (64) and remaining near the highs