Sample Category Title

Dollar Pressured ahead of Fed Rate Decision; European Stocks Rebound

Here are the latest developments in global markets:

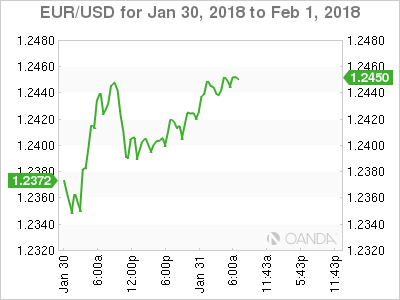

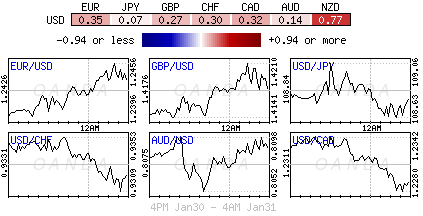

FOREX: Kiwi/dollar remained the biggest winner in early European trading, approaching fresh one-week highs at 0.7400 (+0.94%), while aussie/dollar reached an intra-day high at 0.8109. Dollar/yen inched up to 108.76 but was unable to recover earlier losses despite the BOJ increasing its medium-term Japanese government bonds. Trump's State of Union speech also failed to feed dollar bulls, giving few details on US policies. The dollar index was moving sideways around three-year lows at 88.90 (-0.29%). Euro/dollar changed hands at 1.2450 (+0.40%), showing little reaction to Eurozone's core CPI inflation which came in better than expected. Pound/dollar erased today's gains, falling back to 1.4144. Yesterday, comments by the BOE Governor Mark Carney signaled that the BOE could raise rates faster than previously thought to mitigate inflation. Dollar/loonie retreated to a two-week low of 1.2271 (-0.38) ahead of the Canadian GDP growth figures.

STOCKS: European stocks recovered after holding onto losses the last two days as investors remained optimistic on European markets amid a strong start in the new year. The benchmark European STOXX 600 and the blue-chip Euro STOXX 50 were up by 0.06% at 1100 GMT. The German DAX 30 improved by 0.17%, the French CAC 40 gained 0.24% and the British FTSE 100 was steady.

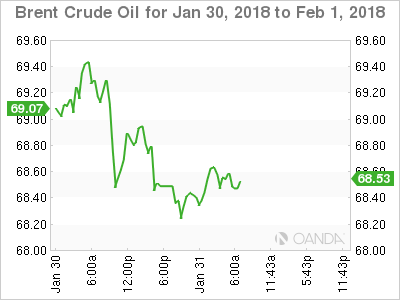

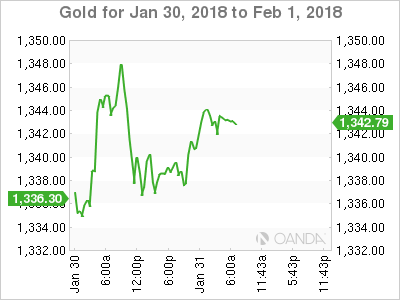

COMMODITIES: Oil prices were on the backfoot for the third day but were on track to post gains for the fifth month in a row. The market weakened as recent stats showed that US rig counts increased amid rising oil prices, threatening to disturb the OPEC-led supply cuts. WTI crude oil retreated by 0.54% to $64.15 per barrel and Brent fell by 0.64% to $68.58 per barrel. Gold was last seen at $1343.30 per ounce, gaining 0.35% in the day.

Day ahead: Fed policy meeting concludes; Canadian GDP growth in focus

US and Canadian data will dominate the economic calendar in the remaining of the day, while the outcome of the Fed's two-day policy meeting will be closely scrutinized by investors.

Fed policymakers are anticipated to announce their decision on interest rates and provide a monetary policy statement today at 1900 GMT, with markets widely expecting the central bank to keep its fund rates unchanged and probably hint that more stimulus reduction is on the way during the year. Note that this is the last meeting for Janet Yellen who was the head of the Fed for the last four years, as Jerome Powell has been officially appointed to take over in February.

In terms of data out of the US, the ADP Research Institute will give an early indication on national employment ahead of the government's comprehensive nonfarm payrolls due on Friday. The report which tracks employment changes only in the private sector is expected to show that 185,000 workers joined the labor market in January compared to 250,000 seen in December, hinting that Friday's nonfarm payrolls might also come lower. The report is expected to be released at 1315 GMT. Chicago PMIs for the month of January, and December's pending home sales will be also available at 1445 GMT and 1500 GMT respectively.

Canada will see the release of GDP growth readings and producer prices at 1315 GMT. Analysts forecast that the Canadian economy will expand by 0.4% m/m in November after posting no growth in October. This would be the highest growth print recorded since May. On the other hand, producer prices might show some weakness in December, declining by 0.1% after posting the biggest rate of expansion since March 2015.

In energy markets, investors will be looking forward to the EIA weekly report on the US oil inventories for the week ending January 26 (1530 GMT). Crude oil inventories are said to rise by 0.126 million barrels following ten weeks of consecutive losses. Gasoline stocks are projected to increase by a smaller amount of 1.809 billion barrels and distillate stocks to decrease by 1.454 million barrels.

In equity markets, AT&T, Boeing, Facebook, and Microsoft will be among companies releasing quarterly earnings on Wednesday.

USDJPY Selling Still Expected 108.98

The USDJPY pair remains intraday bearish while trading below the 108.98 level, further declines towards 108.25 and 107.32 seems possible.

Should the USDJPY pair start to gather bullish momentum above the 108.98 level, we may see buyers move price-action towards the 109.52 and 110.18 levels.

GBPUSD Sellers Look Towards 1.4130 Pivot

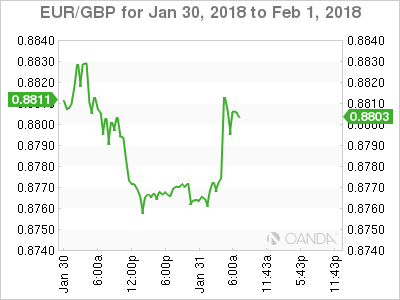

The British pound has turned sharply lower against the greenback during the European trading session, after earlier hitting 1.4214, following a dramatic rebuttal from EU officials. The GBPUSD pair has fallen back towards the 1.4130 level after European Union officials handling Brexit rejected a proposal from the United Kingdom on financial services. Moving into the U.S session, downside pressure on the pair is gathering, as overall risk-on sentiment towards the British pound is starting to wane.

The GBPUSD pair is likely to encounter a deeper sell-off below the 1.4130 level, with downside support layered at 1.4082 and 1.4024.

Should the GBPUSD pair maintain price-action above the 1.4130 level, we may see further upside towards 1.4214 and 1.4284.

EURUSD: Strengthens, Eyes At 1.2493 Zone

EURUSD: The pair was seen heading higher during early Wednesday trading session today. While it holds on to that strength, more bull pressure is likely in the days ahead. On the upside, resistance comes in at 1.2500 level with a cut through here opening the door for more upside towards the 1.2550 level. Further up, resistance lies at the 1.2600 level where a break will expose the 1.2650 level. Conversely, support lies at the 1.2400 level where a violation will aim at the 1.2350 level. A break of here will aim at the 1.2300 level. Below here will open the door for more weakness towards the 1.2250. All in all, EURUSD faces further price upside pressure.

European Stock Markets Up Slightly as Eurozone Inflation Report as Expected

The DAX and CAC indices have posted slight gains in the Tuesday session. The DAX is trading at 13,217.50, up 0.15% since the close on Tuesday. The CAC is following a similar trend, trading at 5484.90, for a 0.20% gain since the Tuesday close. The Eurozone CPI Flash Estimate ticked lower to 1.3%, its lowest level since July 2017. However, investors focused on the fact that the reading matched the forecast.

German releases continue to be sluggish this week. Retail Sales slipped 1.9%, well short of the estimate of -0.3%. It was the sharpest decline since June 2015. Preliminary CPI declined 0.7%, the weakest reading since January 2016. There was some good news, as unemployment claims dropped by 25 thousand, beating the estimate of 16 thousand. Eurozone numbers for fourth quarter 2016 remain solid, the unemployment rate has been steadily dropping, and remained at 8.7% in December, matching the forecast. On Tuesday, Preliminary Flash GDP for the fourth quarter remained unchanged at 0.6%, matching the forecast.

With eurozone inflation well under the ECB target of 2 percent, the ECB has some breathing room regarding its stimulus program (QE), which is scheduled to terminate in September. A stronger eurozone economy has raised speculation that the ECB could wind up QE and shift to normative policy, and perhaps even raise interest rates. However, ECB members have been cautious, trying to keep in check any market enthusiasm about a major change in policy. Last week, ECB President Mario Draghi went as far as saying that QE could be extended or increased if necessary.

Fed Could Signal Changes To Outlook

Wednesday January 31: Five things the markets are talking about

Month-end USD sales and event risk of today''s Fed''s interest rate decision (2 pm EDT) have seen a dramatic pick-up in realized volatility that''s given implied vols another boost this week.

Ahead of the U.S open, Euro stocks have stemmed the bleeding; Asian bourses were mixed, even as the EUR (€1.2454) and JPY (¥108.69) both climbed.

The U.S dollar has found little support from President Trumps first State of the Union address last night as his speech offered few clues on U.S policy.

At today''s FOMC meeting, officials are likely to keep interest rates steady, but they could provide clues on whether their 2018 outlook has changed amid a steadily expanding economy.

Up to now, many investors have doubted the Fed''s dot plot; initially for good reason as central-banker predictions on the pace of rate hikes were not as aggressive as Fed officials predicted. However, that was last years thinking.

In the past month, the market has gotten on board with the prospect that the Fed just might follow up last year''s three-rate hikes with three more in 2018.

Fed-fund futures now show a +36% probability that three +25 bps increases are to happen in 2018, versus +25% a month ago. Meanwhile, for just one hike it''s slumped to +10% from +23% and for two hikes dropped to +29% from +36%.

Conversely, bets have surged that three may be 'too conservative''; the probability of four rate increases is at +19%, versus +8.7% a month ago.

1. Stocks rebound, on pace for monthly gains

Global stocks and bonds mostly rebounded overnight, keeping major indexes on track for solid monthly gains.

Ahead of the U.S open, investors have been analysing President Trump''s first State of the Union address, a slew of corporate earnings and Janet Yellen''s final meeting as leader of the Federal Reserve.

In Japan, the Nikkei fell for a sixth consecutive session overnight, with most sectors in negative territory. The Nikkei was down -0.8%. The index is still up +1.5% this year, it has fallen -4.5% from the 26-year peak hit a week ago. The broader Topix has declined -1.2%.

Down-under, Aussie shares shrugged off lower oil prices and rising bond yields to end the overnight session higher as real estate stocks strengthened. The S&P/ASX 200 index gained +0.3%. In S. Korea, the Kospi climbed +0.2%.

In Hong Kong, stocks reversed earlier losses to end higher overnight, posting its best month in nearly three-years, helped by gains for financial and services firms. At close of trade, the Hang Seng index was up +0.86%, while the Hang Seng China Enterprises index rose +1.29%.

In China, stocks ended the session mixed, with the blue-chip index recouping earlier losses to close higher, aided by a bounce in real estate and consumer firms. At the close, the Shanghai Composite index was down -0.19%, while the blue-chip CSI300 index was up +0.48%.

In Europe, regional indices are trading mostly higher, rebounding from yesterday''s steep declines on the back of upbeat earnings and a small retreat in bond yields.

U.S stocks are set to open in the 'black'' (+0.3%).

Indices: Stoxx600 +0.1% at 396.6, FTSE +0.1% at 7592, DAX +0.3% at 13235, CAC-40 +0.2% at 5483 , IBEX-35 +0.2% at 10452, FTSE MIB flat at 23874 , SMI flat at 9433, S&P 500 Futures +0.3%

2. Oil drops for a third day, gold prices higher

Oil prices are under pressure for a third consecutive day, but remain on track for its biggest gain in January in five-years, and this in spite of data that shows that U.S stocks rose more than expected last week.

Brent is down -49c at +$68.43 a barrel, after touching a two-week intraday low earlier overnight. U.S West Texas Intermediate (WTI) futures are down -39c at +$64.11.

Yesterday, U.S crude fell -1.6% to close at +$64.50 a barrel, far outpacing a -0.6% drop in the price of Brent.

Note: Prices of WTI and Brent are still on track for a fifth month of gains and Brent is set for its largest percentage increase in the month of January since 2013, with a rise of +2.7%.

Providing price pressures are U.S producers increasing their rig count – energy companies added 12 oil rigs last week, the biggest weekly increase in 11 months.

A report from the API Tuesday shows that U.S crude stocks rose by +3.2m barrels last week. Expect dealers to take their cue from today''s U.S DoE report (10:30 am EDT) – the report is expected to show an increase in inventories for the first time in 11-weeks.

Ahead of the U.S open, gold prices have rebounded a tad as the U.S dollar resumes its downtrend. Spot gold is up +0.4% to +$1,342.80 per ounce.

Note: Many believe that gold bullion remains vulnerable to weakness ahead of the Lunar New Year. On Tuesday, the 'yellow'' metal touched its lowest since Jan. 23 at +$1,334.10 an ounce.

3. Sovereign yields remain elevated

U.S government bonds continue to gyrate near this weeks low prices prints, pushing sovereign yields stateside a tad higher towards their four-year high yield print.

U.S yields, in particular, have hit fresh four-year high yields this month as investors have bet on a pickup in growth and inflation following the passage of the U.S corporate tax cuts.

The great debate – the rise in U.S sovereign yields has certainly raised a number of concerns about the durability of the stock rally, while others have said that U.S corporate earnings growth looks solid enough to support further stock gains.

The Fed is expected to send an upbeat message in its statement later today as market based inflation expectations and the growth outlook have improved since the last meeting. The Fed''s 'dot plot'' forecasts three rate increases for 2018.

The odd''s for a Fed hike in March – the first meeting this year that has a press conference and fresh projections outlook, is around +70%.

The yield on U.S 10-year Treasuries fell -2 bps to +2.70%. In Germany, the 10-year Bund yield has declined -1 bps to +0.67%, the first retreat in a week, while in the U.K, the 10-year Gilt yield declined -1 bps to +1.46% and the biggest fall in a fortnight.

Note: In Japan, the Bank of Japan (BoJ) increased its purchases in 3-5 year JGB''s by +¥30B to +¥33B – the first increase in six-months.

4. Dollar on the defense

The once 'mighty'' USD remains on the back foot outright vs. G10 currency pairs and is poised to close out its worst monthly performance in 24-months.

The EUR/USD is slowly edging back towards the psychological €1.25 handle as dealers discount some disappointing Euro inflation data (see below), while believing (pricing-in) that the ECB would tighten policy aggressively down the road. The techies see €1.25 as key resistance in the short-term.

The GBP (£1.4138) trades atop of its overnight lows, mostly weighed down by report the E.U Commission officials had rejected the City of London''s proposal to strike a post-Brexit free trade deal on financial services.

USD/JPY (¥108.82) remains little changed ahead of the U.S open.

Elsewhere, South Africa''s rand (ZAR $11.8285) has gained +1% – its strongest rate outright in almost three-years.

5. Eurozone inflation continues to lag, despite robust economic growth

Despite some stellar job numbers and stronger domestic growth in Europe, data this morning once again highlights a missing ingredient in the eurozone''s expansion – an acceleration in the rate at which consumer prices are rising.

The E.U said prices were +1.3% higher in January than a year earlier, the lowest rate of annual inflation since July 2017 and well short of the ECB''s target, which is just below +2%.

Some of that decline had been expected by the ECB, since energy prices jumped at the turn into 2017, and those sharp rises have not been repeated this year.

Note: But not all of the weakness in inflation is down to energy prices. According to Eurostat, services prices rose at an annual rate of +1.2%, unchanged for four straight months. Overall, the core rate of inflation edged up to +1.0% from +0.9%.

The ECB continues to expect that inflation will eventually rise, driven in large part by a rise in wages as unemployment falls and as skilled workers become scarce.

Other data this morning showed that eurozone employment continues to run strong. In Germany, Europe''s powerhouse, January unemployment rate has hit fresh its post-unification low of +5.4%, while the eurozone matches its December 2008 lows of +8.7%.

Euro Higher As Eurozone CPI Matches Forecast

The euro has posted slight gains in the Wednesday session, in what continues to be an uneventful week f0r EUR/USD. Currently, the pair is trading at 1.2451, up 0.39% on the day. On the release front, German Retail Sales plunged 1.9%, much weaker than the estimate of -0.3%. This marked the strongest decline since June 2015. On the inflation front, Eurozone CPI Flash Estimate, ticked lower to 1.3%, the lowest level since July 2017. In the US, there are a host of key events. ADP Nonfarm Employment Change is expected to slow to 186 thousand. The Federal Reserve will release a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%. On Thursday, German and the eurozone will release Manufacturing PMIs, while the US publishes unemployment claims and the ISM Manufacturing PMI.

Inflation levels in the eurozone pointed upwards in 2017, but softened in January. Eurozone CPI Flash Estimate came in at 1.3%, as inflation remains well below the ECB target of around 2 percent. Lower inflation gives the ECB some breathing room regarding its stimulus program (QE), which is scheduled to terminate in September. A stronger eurozone economy has raised speculation that the ECB could wind up QE and shift to normative policy, and perhaps even raise interest rates. However, ECB policy members have been cautious, trying to keep in check any market enthusiasm about a major change in policy. Last week, ECB President Mario Draghi went as far as saying that QE could be extended or increased if necessary.

All eyes are on the Federal Reserve, which will make a rate announcement on Wednesday, the final one under Janet Yellen’s watch. The tone of the rate statement could affect investor sentiment and have an impact on gold prices. It’s a virtual certainty that the Fed will leaves rates unchanged this time around, although it’s likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.

Market Update – European Session: Euro Zone Employment Continues To Run Strong, Jan Inflation Data Mixed

Notes/Observations

German Jan Unemployment Rate hits fresh post-unification low of 5.4%; Euro Zone matches Dec 2008 lows of 8.7%

European inflation data mixed (France, Euro Zone beat, Spain miss;

German Dec Retail Sales miss expectations

Trump’s State of the Union touched on many issues but was short on details on his policy proposals.

Fed is expected to send an upbeat message in its statement today as market based inflation expectations and the growth outlook have improved since the last meeting

Asia:

Australia Q4 CPI Q/Q: 0.6% v 0.7%e; Y/Y: 1.9% v 2.0%e v 1.8% prior; Trimmed

China Jan Govt Official Manufacturing PMI at a 8-month low (51.3 v 51.6e)

China PBoC skipped its OMO operation for the 5th straight session citing appropriate and stable liquidity in banking system

Bank of Japan (BOJ) Summary of Opinions from Jan 22-23rd meeting noted that it must continue powerful monetary easing as inflation remained weak. Still had a long way to go until 2% inflation target is reached. If cut in BOJ super long JGB buying gave unintended signal on monetary policy, BOJ must correct that

Bank of Japan (BoJ) Gov Kuroda: taking time to change Japan deflationary mindset; will persistently continue easing for price goal. Reiterated high chance of meeting 2% inflation target around FY2019.

BOJ increased its purchases in 3-5 year JGBs by ¥30B to ¥33)B (1st increase since July)

Europe:

BOE Gov Carney: UK economy's outperformance versus BOE's Aug outlook is because of a stronger world economy and looser fiscal stance than expected. Inflation pass through due to the exchange rate shock had further to go and saw inflation remaining above 2% target in near future

UK PM May: leaked Brexit analysis were preliminary, selective and not signed off by ministers (reply to Unreleased, internal UK govt Brexit analysis: UK would be worse off outside the EU under every scenario modeled

ECB’s Weidmann (Germany): German surplus will shrink as investment rises. Reiterates view that cheap oil and loose monetary policy helped to explain German current account surplus

Americas:

US President Trump State of the Union Address: Will work to fix bad trade deals and negotiate new ones; Will protect American workers and intellectual property through strong enforcement of our trade rules. Wants Congress to produce legislation that generates at least $1.5T for new infrastructure investment

Treasury Sec Mnuchin: strong dollar is in the long-term interests of the US; supported free FX markets with no intervention

Energy:

Weekly API Oil Inventories: Crude: +3.2M v +4.8M prior

Economic Data:

(DE) Germany Dec Retail Sales M/M: -1.9% v -0.4%e; Y/Y: -1.9% v +2.8%e

(CH) Swiss Dec UBS Consumption Indicator: 1.69 v 1.73 prior

(DK) Denmark Dec Gross Unemployment Rate: 4.3% v 4.3%e; Unemployment Rate (Seasonally Adj): 3.3% v 3.4%e

(TR) Turkey Dec Trade Balance: -$9.2B v -$9.6Be

02:30 (TH) Thailand Dec Current Account: $3.1Be v $5.3B prior; Overall Balance of Payments (BOP): No est v $2.3B prior; Trade Balance: No est v $3.3B prior; Exports Y/Y: No est v 12.3% prior; Imports Y/Y: No est v 11.9% prior

(FR) France Jan Preliminary CPI M/M: -0.1% v -0.3%e; Y/Y: 1.4% v 1.2%e

(FR) France Jan CPI EU Harmonized M/M: -0.1% v -0.5%e; Y/Y: 1.5% v 1.1%e

(FR) France Dec PPI M/M: 0.0 v 1.5% prior; Y/Y: 1.7% v 2.6% prior- 03:00 (TW) Taiwan Q4 Preliminary GDP Y/Y: % v 2.5%e; Overall annual 2017 GDP: % v 2.7%e

(ES) Spain Jan Preliminary CPI M/M: -1.1% v -1.0%e; Y/Y: 0.5% v 0.9%e

(ES) Spain Jan CPI EU Harmonized M/M: -1.5% v -1.4%e; Y/Y: 0.7% v 0.8%e

(HU) Hungary Dec PPI M/M: 0.0% v 1.0% prior; Y/Y: 3.9% v 4.5% prior

(DE) Germany Jan Unemployment Change: -25K v -17Ke; Unemployment Claims Rate: 5.4% v 5.4%e record low)

(IT) Italy Dec Preliminary Unemployment Rate: 10.8% v 10.9%e (lowest since Aug 2012)

(CH) Swiss Jan Credit Suisse Survey Expectations: 34.5 v 52.0 prior

(PT) Portugal Preliminary Jan CPI Y/Y: M/M: -0.1% v 0.0% prior; Y/Y: 1.1% v 1.5% prior

(PT) Portugal Preliminary Jan CPI EU Harmonized M/M: -1.2% v -0.2% prior; Y/Y: 1.1% v 1.6% prior

(EU) Euro Zone Jan Advance CPI Estimate Y/Y: 1.3% v 1.2%e; CPI Core Y/Y: 1.0% v 1.0%e

(EU) Euro Zone Dec Unemployment Rate: 8.7% v 8.7%e (matches lowest reading since Dec 2008)

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month, 6-month and 12-month bills

(SE) Sweden sold SEK5.0B in 3-month bills; Avg Yield: -0.7221% v -0.7251% prior; bid-to-cover: 3.17x v 2.45x prior

(NO) Norway sold NOK3.0B vs. NOK3.0B indicated in 1.75% Feb 2027 bonds; Avg Yield: 1.81% v 1.52% prior; Bid-to-cover: 2.48x v 2.00x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.1% at 396.6, FTSE +0.1% at 7592, DAX +0.3% at 13235, CAC-40 +0.2% at 5483 , IBEX-35 +0.2% at 10452, FTSE MIB flat at 23874 , SMI flat at 9433, S&P 500 Futures +0.3%]

Market Focal Points/Key Themes:

European Indices trade mostly higher rebounding from steep falls yesterday on the back of upbeat earnings and a small retreat in bond yields.

Notable earners this morning included Siemens which reported stronger profits, although Revenue slightly missed forecasts; Infineon slightly missed forecasts and lowered guidance largely on the back of the stronger Euro, while in the UK Capita trades sharply lower after a profit warning, and suspension of dividend along with the proposal of a rights issue. In Sweden Electrolux trades higher after earnings, while Ericsson trades sharply lower after worse than expected loss.

Looking ahead notable earners include Dow component Boeing, alongside Eli Lily, Textron and Anthem among others.

Movers

Consumer Discretionary [H&M [HMB.SE] -7.4% (Earnings), Capita [CPI.UK] -45% (Profit warning, suspends dividend)]

Industrials [Siemens [SIE.DE] +1.2% (Earnings), Volvo [VOLVB.SE] +3.6% (Earnings), Electrolux [ELUXB.SE] +6.6% (Earnings)

Financials [ Julius Baer [BAER.CH] -2.5% (Earnings), Santander [SAN.ES]+0.6% (Earnings), SEBA [SEBA.SE] +2.6% (Earnings), ING [INGA.NL] -1.8% (Earnings)]

Ericsson [Ericsson [ERICB.SE] -9% (Earnings)]

Materials [ArcelorMittal [MT.NL]-1.4% (Earnings)]

Technology [ Infineon [IFX.DE] -1.1% (Earnings)]

Speakers

Sweden Central Bank (Riksbank) Gov Ingves: Now on target with inflation and inflationary expectations are back

European Commission officials said to have rejected the City of London’s proposal to strike a post-Brexit free trade deal on financial services

Czech Central Bank: Financial sector maintains high resilience to adverse shocks. Ready to raise counter-cyclical capital buffer further in case of continued fast credit growth, bank vulnerability and higher risks of real estate financing

South Africa ANC party said to discuss change of power with Zuma this week

BoJ Iwata: Not at the point where can change interest rates soon. there was a misunderstanding in the market that BoJ would exit easy policy soon. The 2% inflation target remained far away so current YCC was appropriate; no need to change YCC for some time. Important for BOJ to be ready to change yield control if economy, price and financial conditions change

Thailand Central Bank official Nakornthab: Could raise 2018 GDP growth forecast from 3.9% due to improving exports and govt spending

Currencies

USD remained on the defensive against the major pairs as the greenback was poised to have its worst monthly performance in two years

EUR/USD edged back towards the 1.25 area as participants discounted recent inflation data out of Europe and seemed to believe that ECB would tighten policy aggressively down the road. Dealers noted that 1.25 level could be tough to breech in the short-term

The GBP was slightly lower in the session. Cable weighed down by report the EU Commission officials had rejected the City of London’s proposal to strike a post-Brexit free trade deal on financial services. Pair near 1-week lows at 1.4135

USD/JPY little changed at 108.75 just ahead of the NY morning.

Fixed Income

Bund Futures trades up 30 ticks at 159.14 as Euro Zone inflation slows in January. Continued upside targets 160.50, while a move lower targets the158.75 low.

Gilt futures trade at 122.48 up 13 ticks, but still near the lows for the month of January. Support continues to stand at 122.25 then 121.75, with upside resistance at 123.75 then 124.33.

Wednesday’s liquidity report showed Tuesday’s excess liquidity fell to €1.869T from €1.885T prior. Use of the marginal lending facility fell to €56M from €65M prior.

Corporate issuance saw 1 issuer raise $0.4B in the primary market.

Looking Ahead

05:30 (EU) ECB allotment in 3-month LTRO

05:30 (DE) Germany to sell €4.0B in 2023 BOBL

06:00 (BR) Brazil Dec National Unemployment Rate: 11.9%e v 12.0% prior

06:00 (IL) Israel Dec Unemployment Rate: No est v 4.3% prior

06:00 (RU) Russia to sell combined RUB30B in 2024 and 2033 OFZ bonds

06:45 (US) Daily Libor Fixing

07:00 (IN) India FY16/17 Annual GDP Estimate Y/Y: No est v 8.0% prior

07:00 (IN) India Dec Eight Infrastructure (Key) Industries: No est v 6.8% prior

07:00 (CL) Chile Dec Total Copper Production: No est v 505.7K prior

07:00 (CL) Chile Dec Industrial Production Y/Y: 1.0%e v 2.3% prior; Manufacturing Production Y/Y: 0.5%e v 1.9% prior

07:00 (CL) Chile Dec Unemployment Rate: 6.3%e v 6.5% prior

07:00 (ZA) South Africa Dec Trade Balance (ZAR): 10.1Be v 13.0B prior

07:00 (US) MBA Mortgage Applications w/e Jan 26th: No est v 4.5% prior

07:30 (BR) Brazil Dec Primary Budget Balance (BRL): -30.8Be v -0.9B prior; Nominal Budget Balance: -59.6Be v -30.0B prior; Net Debt to GDP: 51.6%e v 51.1% prior

08:05 (UK) Baltic Dry Bulk Index

08:15 (US) Jan ADP Employment Change: +185Ke v +250K prior

08:30 (US) Q4 Employment Cost Index (ECI): 0.6%e v 0.7% prior

08:30 (CA) Canada Nov GDP M/M: 0.4%e v 0.0% prior; Y/Y: 3.4%e v 3.4% prior

08:30 (CA) Canada Dec Industrial Product Price M/M: 0.0%e v 1.4% prior; Raw Materials Price Index M/M: -2.5%e v +5.5% prior

08:30 (US) Treasury quarterly refunding announcement for 3-year, 10-year and 30-year bonds

09:45 (US) Jan Chicago Purchasing Manager: 64.0e v 67.6 prior

10:00 (US) Dec Pending Home Sales M/M: 0.5%e v 0.2% prior; Y/Y: 1.7%e v 0.6% prior

10:00 (CO) Colombia Dec National Unemployment Rate: No est v 8.4% prior; Urban Unemployment Rate: 10.3%e v 9.6% prior

10:00 (MX) Mexico Dec Net Outstanding Loans (MXN): No est v 3.991T prior

10:30 (US) Weekly DOE Crude Oil Inventories

14:00 (US) FOMC Interest Rate Decision: Expected to leave Interest Rates unchanged

14:00 (AR) Argentina Dec Industrial Production Y/Y: No est v 3.5% prior

16:00 (NZ) New Zealand Jan ANZ Job Advertisements M/M: No est v -0.3% prior

17:00 (AU) Australia Jan CBA Australia PMI Manufacturing: No est v 57.1 prior

17:30 (AU) Australia Jan AiG Manufacturing PMI: No est v 56.2 prior

18:00 (AU) Australia Jan CoreLogic House Px M/M: No est v -0.4% prior

18:00 (KR) South Korea Jan CPI M/M: 0.6%e v 0.3% prior; Y/Y: 1.3%e v 1.5% prior

19:00 (KR) South Korea Jan Trade Balance: $4.0Be v $5.8B prior

Technical Outlook: Spot Gold In Recovery Mode Ahead Of Fed Decision

Spot Gold bounced on Wednesday, driven by weaker dollar, after four-day pullback from $1366 found footstep at $1334 (Fibo 76.4% of $1324/$1366 upleg). Near-term bears are taking a breather and awaiting the outcome of Fed’s policy meeting, due later today, looking for signals of next steps of the US central bank in the near future. Fed chair Janet Yellen is leading her last policy meeting as head of the central bank before transferring the chairmanship to her successor Jerome Powell. Gold’s overall picture remains bullish and keeps focus at the upside with recent pullback seen as positioning for fresh upside action. Close above 10 SMA is needed to generate fresh bullish signal and confirm that probes below were minor threat to underlying bulls. Extension above $1346 (Fibo 38.2% of $1366/$1334 pullback) will be next bullish signal with confirmation of reversal seen on extension above $1353 (Fibo 61.8%). Bearish scenario sees increased risk for retesting $1324 pivot (18 Jan trough) on loss of $1334 handle.

Res: 1346, 1350, 1353, 1357

Sup: 1340, 1334, 1331, 1328

Technical Outlook: WTI Oil – Downside Remains At Risk On Fears Of Crude Inventories Build

WTI oil is holding within narrow consolidation after posting new one-week low at $63.66 on Wednesday. Near-term bias is negative following two-day fall from $66.64 high, with bearish signal generated on Tuesday's close below 10SMA ($64.65). Fresh weakness on Wednesday cracked next important support at $63.97 (rising 20SMA) and sustained break here would expose pivot at $62.50 (Fibo 38.2% of $55.81/$66.64 upleg/rising daily Kijun-sen). Negative near-term sentiment is boosted by fears in the markets about increase in US oil supplies as API report, released late Tuesday, showed US oil inventories rose by 3.2 million barrels, coming well above forecasted build of 0.1 million barrels. Focus is on EIA weekly crude stocks data, due later today, with forecast for build of 0.12 million barrels after ten straight weeks of draws in US crude stocks. Stronger than expected build in crude inventories would further depress oil price, while another draw in weekly crude stocks would ease existing downside pressure. Bearish scenario requires close below $62.50 Fibo support to signal deeper correction, while firmer bullish signal could be expected on return and close above broken 10SMA.

Res: 64.23, 64.65, 65.54, 66.64

Sup: 63.66, 62.83, 62.50, 61.79