Sample Category Title

USDCAD – Loonie Hits New Over 4-mth High on Weaker Greenback and Solid Canadian Data

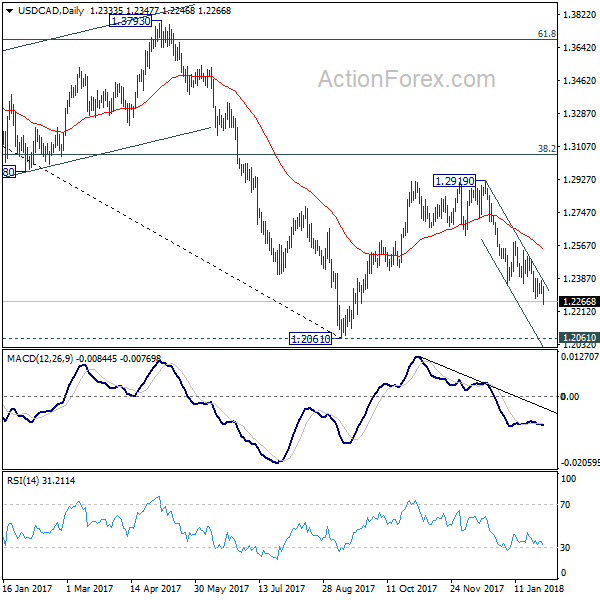

The USDCAD pair fell to new over four-month low on Wednesday at 1.2248 as loonie benefited from weaker greenback after President Trump's speech, with positive impact on upbeat US ADP jobs data (234K in Jan vs 186K f/c).

Canadian dollar received additional support from Canada's solid data on Wednesday as GDP came in line with expectations in Nov (0.4%) but above 0.0% previous month while Industrial Product Price Index (IPPI) and Raw Materials Price Index (RMPI) showed better than expected results in December (IPPI -0.1% vs -0.2% f/c) and (RMPI -0.9% vs -2.2% f/c).

Fresh weakness comes after brief consolidation phase which was capped by falling 10SMA and today's dip cracked support at 1.2263 (Fibo 76.4% of larger 1.2061/1.2920 ascend) which marks the only significant obstacle on the way to key med-term support and target at 1.2061 (08 Sep low).

Close below 1.2263 is needed for fresh bearish signal for continuation of downtrend from 1.2920 (19 Dec high).

The outcome of Fed's two-day monetary policy meeting which ends today is in focus as investors are looking for more clues about US central bank's next steps.

Falling 10SMA marks solid resistance (currently at 1.2378) which is expected to limit upticks and keep immediate bears intact.

Stronger recovery above falling 20SMA (1.2419) would sideline immediate downside risk.

Res: 1.2348; 1.2378; 1.2419; 1.2488

Sup: 1.2263; 1.2248; 1.2195; 1.2118

Dollar Slips ahead of Fed Meeting, Bitcoin Wobbles

Market players who were expecting fireworks from President Donald Trump's first State of the Union address, were left empty-handed following the Dollar's fairly muted response. Although Trump stuck to script and adopted a more conciliatory tone, the address failed to offer fresh insight into the $1.5 trillion infrastructure spending plan.

The Dollar found itself under noticeable selling pressure on Wednesday, ahead of the Federal Reserve decision later today, which is widely expected to conclude with monetary policy unchanged. It is already considered a foregone conclusion that US interest rates will be left unchanged in January, so attention will largely be directed towards the press conference by Yellen. Today's FOMC could have a nostalgic note, considering that this will be Janet Yellen's last Fed meeting as Chair. The Dollar could be offered a lifeline if policymakers adopt a hawkish stance and reinforce markets' expectations of three rate hikes in 2018.

From a technical standpoint, the Dollar Index is under pressure on the daily charts. Sustained weakness below 89.00 could invite a decline towards 88.50, and 88.00.

Carney comes to the rescue

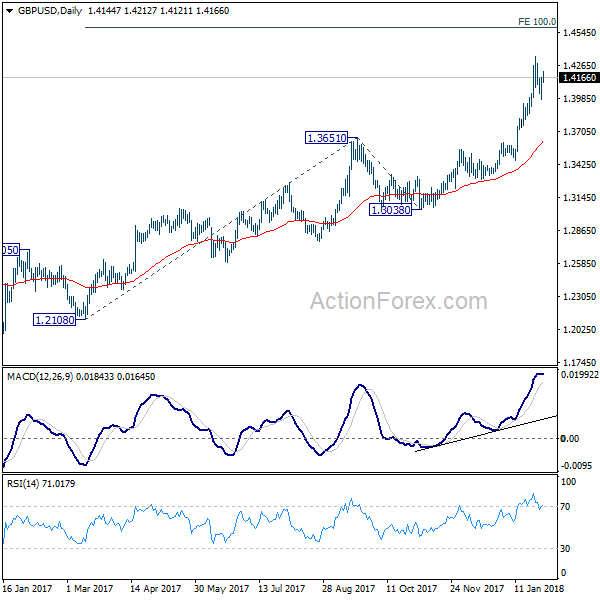

Sterling bulls received a shot in the arm on Tuesday thanks to Mark Carney's upbeat tone on the UK economy. With the Bank of England now turning its focus towards bringing down inflation, speculations may heighten over the central bank raising interest rates faster than expected. Although the Pound could continue to benefit from renewed rate expectations, the upside could be capped by Brexit concerns and political developments at home. From a technical standpoint, the GBPUSD remains bullish on the daily charts thanks to ongoing Dollar weakness. If the upside momentum holds, prices could challenge 1.4230 and 1.4300, respectively. Alternatively, an intraday breakdown below 1.4110 may trigger a decline towards 1.4000 and 1.3850, respectively.

Commodity spotlight - WTI Crude

WTI Crude found itself under intense selling pressure on Tuesday after industry reports illustrated an unexpected build in US crude inventories.

The fact that WTI sharply tumbled following the industry report continues to highlight how oil still remains sensitive to oversupply fears. While optimism over OPEC's production cuts rebalancing markets has inspired bulls, bears remain supported by concerns over US Crude production reaching new records. Oil prices could witness steep losses if US crude production hits the 10 million barrel per day mark. Focusing on the technical picture, WTI Crude bulls remain in control above the $63.00 higher low on the daily charts with the next level of interest at $65. A breakdown below $63 could trigger a decline back to $62.20.

Bitcoin shivers on crackdown fears

Bitcoin was in trouble on Tuesday with prices dipping below $10,000 after US regulators moved to crackdown on one of the world's largest digital currency exchanges. The selling pressure on Bitcoin was fueled by reports of Facebook Inc. banning adverts promoting cryptocurrencies. If cryptocurrencies continue to fall under the intense magnifying glass of regulators, this could weigh on demand and result in further downside. From a technical standpoint, Bitcoin remains heavily bearish with prices struggling to keep above $10,000. Sustained weakness below this level could encourage a further decline towards $9000, $8400 and $8000, respectively.

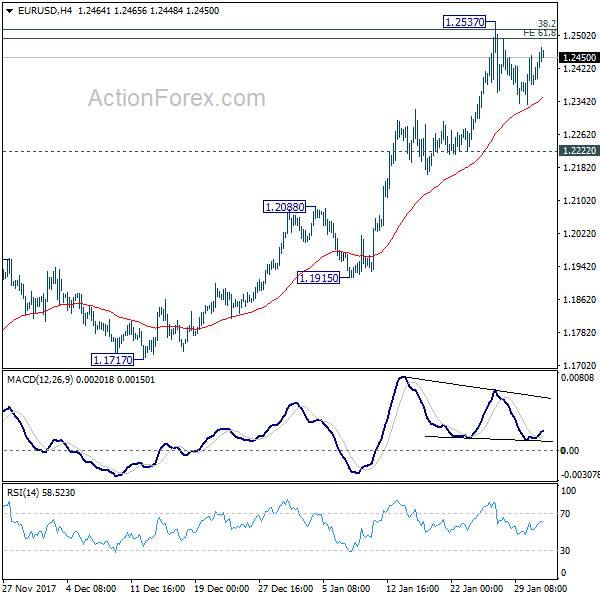

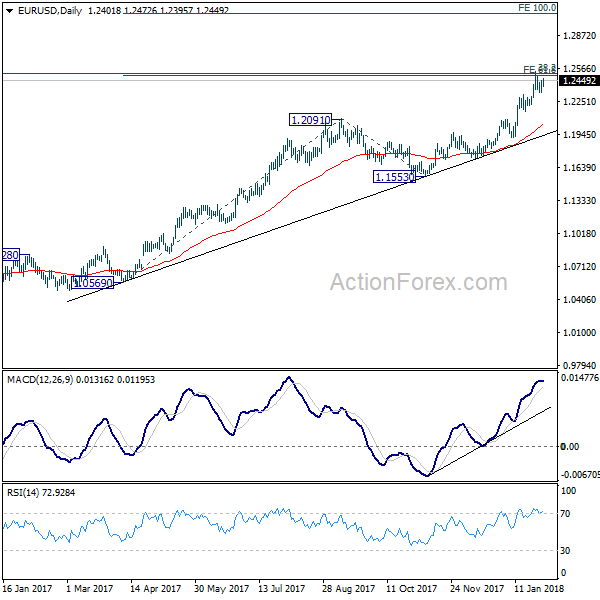

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2335; (P) 1.2383 (R1) 1.2431; More....

EUR/USD is still bounded in consolidation from 1.2537 and intraday bias remains neutral. As long as 1.2222 support holds, near term outlook remains bullish. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

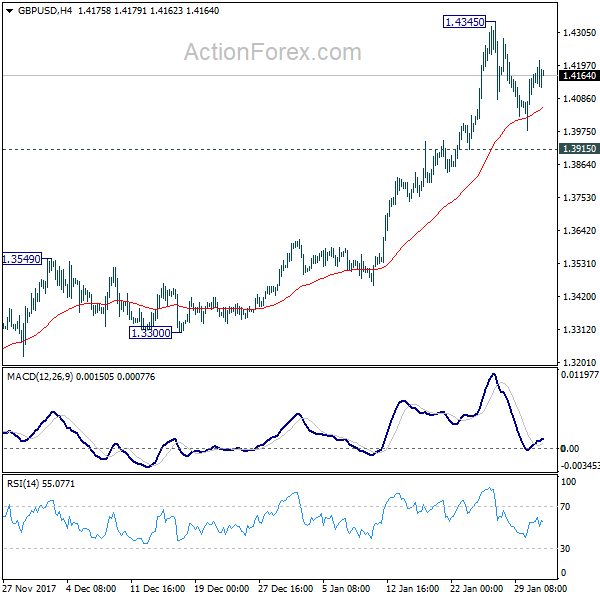

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4029; (P) 1.4098; (R1) 1.4216; More.....

GBP/USD is staying in consolidation below 1.4345 and intraday bias remains neutral first. More corrective trading could be seen. But downside should be contained by 1.3915 support to bring rally resumption. On the upside, break of 1.4345 will resume medium term up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

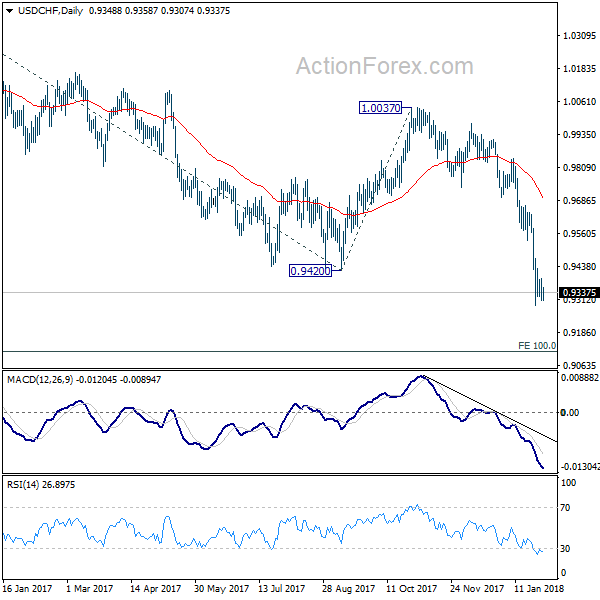

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9301; (P) 0.9347; (R1) 0.9384; More...

Intraday bias in USD/CHF remains neutral as consolidation from 0.9288 temporary low is in progress. With 0.9536 resistance intact, outlook stays bearish and deeper fall is expected. Break of 0.9288 will resume the larger down trend and target next key fibonacci level at 0.9115.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 08545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.39; (P) 108.79; (R1) 109.18; More...

USD/JPY is still bounded in consolidation from 108.27 temporary low. Intraday bias remains neutral at this point. As long as 110.18 resistance holds, deeper decline is expected. On the downside, break of 108.27 will extend recent fall through 107.31 support to next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2304; (P) 1.2341; (R1) 1.2375; More...

USD/CAD drops to as low as 1.2246 so far and break of 1.2281 indicates fall resumption. Intraday bias is turned back to the downside. Fall from 1.2919 should target a test on 1.2061 low. On the upside, however, break of 1.2390 resistance will indicate near term bottoming. That would be accompanied by bullish convergence condition in 4 hour MACD.

In the bigger picture, rebound from 1.2061 is likely completed completed at 1.2919, rejected by 55 week EMA and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

Dollar Weakens ahead of FOMC, Canadian Dollar Jumps after GDP

Dollar weakens broadly in early US session despite solid employment data. In particular, USD/CAD leads the way with Canadian GDP meeting forecasts. The greenback will look into Janet Yellen's last FOMC announcement today. But it's unlikely for Dollar to get any support from there. The key level to watch is 1.25 handle in EUR/USD. It's close to 1.2494/2516 cluster fibonacci level. A firm break there would likely prompt broad-based selloff in Dollar.

US ADP report showed 234k growth in private sector jobs in January, versus expectation of 183k. Employment cost index rose 0.6% in Q4, meeting consensus. From Canada, GDP grew 0.4% mom in November, meeting forecasts. IPPI dropped -0.1% mom in December while RMPI dropped -0.9% mom.

It is widely expected that no change would be made in Yellen's last FOMC meeting as Fed chair. The market focus is on the Fed's economic outlook and whether there are hints on the rate hike path. Notwithstanding the fact that inflation has remained soft, the robust employment market, with unemployment rate below the Fed's long-term target, should have anchored the Fed's confidence over the economic outlook. Fed could make an hawkish tweak in the statement the pave the rate for a March hike. Fed fund futures are already pricing in over 70% chance of that.

ECB Coeure: Not going to be too hasty on stimulus exit

ECB Executive Board member Benoit Coeure said today that the asset purchase program "of course will not last forever". But he emphasized that "there is also a very wide agreement in the Governing Council ... that we have to be patient and prudent because we are not yet where we want to be in terms of inflation." He added that "we are not going to be too hasty". Also, there were speculations that ECB could be soon ready to tweak its communications. But Coeure said that "we are having a discussion on having a discussion" only and "its meta monetary policy".

Release from Eurozone, CPI slowed to 1.3% yoy in January, down from 1.3% yoy and met expectation. CPI core rose to 1.0% yoy, up from 0.9% yoy, also met expectations. Eurozone unemployment rate was unchanged at 8.7% in December. Germany unemployment dropped -25k in January versus expectation of -20k. Germany retail sales dropped -1.9% mom in December, versus expectation of -0.4% yoy.

Also from Europe, Swiss UBS consumption indicator rose 0.2 to 1.69 in December. UK Gfk consumer confidence rose to -9 in January. BRC shop price index dropped -0.5% yoy in January.

Australia CPI picked up but missed expectations

Australia CPI accelerated to 1.9% yoy in Q4, up fro Q3's 1.8 yoy. However, this came in weaker than expectations of 2.0% yoy. On RBA's other inflation measures, the trimmed mean CPI stayed unchanged at 1.8%, missing consensus of 1.9%. The weighted median CPI rose to 2.0% from 1.9% in the third quarter. This exceeded expectations of 1.9%. The set of inflation data gives no pressure for RBA to hike any time soon. And indeed, recent rally in Aussie's exchange rate could give some downward pressure to inflation in near term ahead. And, there is still a lack of evidence of pick up in wage growth.

China manufacturing PMI slipped to 51.3

From China, official manufacturing PMI slipped -0.3 point to 51.3 in January, comparing to consensus of 51.5. Non-manufacturing PMI added 0.3 point to 55.3, beating expectations of 55. Note the government's PMI estimates cover large corporations while the one compiled by Caixin/ Markit covers medium to small firms. Traders should interpret China's economic data with caution as the accuracy is under question. HSBC complained about the country's lack of transparency and withdrew from being the partner of Markit in compilation of China's PMI data in 2015. Meanwhile, several provincial and local governments including Inner Mongolia and Tianjin have admitted exaggerating the economic data earlier this month.

BoJ Iwata: Some distance to 2% inflation

BoJ Deputy Governor Kikuo Iwata said today that the "powerful" monetary easing should be maintained. He noted "the economy is expanding moderately but prices remain weak." And, "there's some distance to 2 percent inflation." And he called for "government steps, as well as appropriate monetary policy, are necessary to achieve price stability with sustained economic growth." BoJ released summary of opinions from the January meeting. One member said that recent surge in market expectation of stimulus exit would be "undesirable".

Released from Japan, consumer confidence was unchanged at 44.7 in January. Housing starts dropped -2.1% yoy in December. Industrial production rose 2.7% mom in December.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2304; (P) 1.2341; (R1) 1.2375; More...

USD/CAD drops to as low as 1.2246 so far and break of 1.2281 indicates fall resumption. Intraday bias is turned back to the downside. Fall from 1.2919 should target a test on 1.2061 low. On the upside, however, break of 1.2390 resistance will indicate near term bottoming. That would be accompanied by bullish convergence condition in 4 hour MACD.

In the bigger picture, rebound from 1.2061 is likely completed completed at 1.2919, rejected by 55 week EMA and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Dec P | 2.70% | 1.50% | 0.50% | |

| 00:01 | GBP | GfK Consumer Confidence Jan | -9 | -13 | -13 | |

| 00:01 | GBP | BRC Shop Price Index Y/Y Jan | -0.50% | -0.40% | -0.60% | |

| 00:30 | AUD | CPI Q/Q Q4 | 0.60% | 0.70% | 0.60% | |

| 00:30 | AUD | CPI Y/Y Q4 | 1.90% | 2.00% | 1.80% | |

| 00:30 | AUD | CPI RBA Trimmed Mean Q/Q Q4 | 0.40% | 0.50% | 0.40% | |

| 00:30 | AUD | CPI RBA Trimmed Mean Y/Y Q4 | 1.80% | 1.90% | 1.80% | |

| 00:30 | AUD | CPI RBA Weighted Median Q/Q Q4 | 0.40% | 0.50% | 0.30% | |

| 00:30 | AUD | CPI RBA Weighted Median Y/Y Q4 | 2.00% | 1.90% | 1.90% | |

| 01:00 | CNY | Manufacturing PMI Jan | 51.3 | 51.5 | 51.6 | |

| 01:00 | CNY | Non-manufacturing PMI Jan | 55.3 | 55 | 55 | |

| 05:00 | JPY | Consumer Confidence Jan | 44.7 | 44.9 | 44.7 | |

| 05:00 | JPY | Housing Starts Y/Y Dec | -2.10% | 1.10% | -0.40% | |

| 07:00 | EUR | German Retail Sales M/M Dec | -1.90% | -0.40% | 2.30% | |

| 07:00 | CHF | UBS Consumption Indicator Dec | 1.69 | 1.67 | 1.73 | |

| 08:55 | EUR | German Unemployment Change Jan | -25K | -20K | -29K | |

| 08:55 | EUR | German Unemployment Claims Rate Jan | 5.40% | 5.40% | 5.50% | |

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 8.70% | 8.70% | 8.70% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Jan A | 1.00% | 1.00% | 0.90% | |

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Jan | 1.30% | 1.30% | 1.40% | |

| 13:15 | USD | ADP Employment Change Jan | 234K | 183K | 250K | 242K |

| 13:30 | USD | Employment Cost Index Q4 | 0.60% | 0.60% | 0.70% | |

| 13:30 | CAD | GDP M/M Nov | 0.40% | 0.40% | 0.00% | |

| 13:30 | CAD | Industrial Product Price M/M Dec | -0.10% | 0.00% | 1.40% | |

| 13:30 | CAD | Raw Materials Price Index M/M Dec | -0.90% | -2.50% | 5.50% | |

| 14:45 | USD | Chicago PMI Jan | 64 | 67.6 | ||

| 15:00 | USD | Pending Home Sales M/M Dec | 0.50% | 0.20% | ||

| 15:30 | USD | Crude Oil Inventories | 0.1M | -1.1M | ||

| 19:00 | USD | FOMC Rate Decision | 1.50% | 1.50% |

Fed Statement Eyed In Yellen’s Final Meeting

US Markets Bounce Back From Tuesday's Month-End Sell-Off

US equity markets are seen opening a little higher on Wednesday, reversing part of Tuesday's declines ahead of the first Federal Reserve interest rate announcement of the year.

US stocks came under pressure on Tuesday but with month end fast approaching and indices having recorded around 7% gains this month, as of last week's close, it's likely that much of this was driven by some rebalancing, rather than being a sign that investors are less bullish. It will be interesting to see how markets trade in the coming days but I don't expect this to be the start of a broader decline.

As is the case for much of the week, there's plenty for investors to focus on today. Donald Trump's first State of the Union address offered little for markets to get excited about, with the President instead taking to opportunity to showcase the triumphs of his first year in charge. This is broadly in line with expectations heading into the event itself and so investors now move on to the next of the week's key events.

Fed Statement Key in the Absence of Press Conference

The Fed monetary policy meeting will be the first of the new year and the last under the leadership of Janet Yellen, who will be replaced as Chair by Jerome Powell. Bearing that – and the fact that the central bank raised interest rates at the last meeting in December – in mind, we're not expecting any changes today, but we may get some insight into whether the new tax reforms have altered the views of policy makers.

Of course, in the absence of a press conference with the Fed Chair, we'll have to rely on the accompanying statement to provide fresh insight, at least until the minutes are released in a few weeks. A slight change in the statement can get quite a reaction in the markets though so traders as ever will be looking for any signs that future rate hikes are under-priced, given the recent changes.

ADP Number and Earnings Also in Focus

Ahead of the central bank announcement, we'll get some employment data from ADP which comes ahead of Friday's jobs report. The ADP is seen as being indicative of the official Non-Farm Payrolls figure but in reality that is often not the case. Still, traders will be looking for signs that market expectations for January are way off the mark and so it always has the potential to move things in the markets.

There's also a lot of companies reporting fourth quarter earnings today – including 34 from the S&P 500 and two from the Dow – which will be of interest to investors and could have an impact on overall market sentiment. Once again though, with it being the final trading day of the month, equity markets may not move entirely rationally today.

Canadian Dollar Improves, GDP Next

The Canadian dollar has posted slight losses in the Wednesday session. Currently, the pair is trading at 1.2281, down 0.45% on the day. On the release front, Canada releases GDP for December, which is expected to climb to 0.4%. Canada will also release an important inflation indicator, the Raw Materials Price Index. The markets are braced for a sharp drop of 2.2%. In the US, the markets will get a good look at employment numbers, starting with ADP Nonfarm Employment Change. The indicator is expected to slow to 186 thousand. The Federal Reserve will release a monetary policy statement, with the markets expecting the benchmark rate to remain unchanged at a range between 1.25%-1.50%. On Thursday, the US publishes unemployment claims and the ISM Manufacturing PMI.

The latest round of negotiations over NAFTA ended in Montreal last week, and there were no breakthroughs. Still, the sides continue to talk, and a Merrill Lynch has lowered the odds of the US leaving the pact to 25 percent. The US has demanded far-reaching concessions from Canada and Mexico, such as shifting more auto production to the US. Canada and Mexico are strongly opposed to the US demands, but both economies would take a sharp hit if NAFTA is terminated. At the same time, many US businesses don't want to blow up NAFTA and are pressuring President Trump to remain in the trade pact. The next round of negotiations is scheduled for late February in Mexico.

All eyes are on the Federal Reserve, which will make a rate announcement on Wednesday, the final one under Janet Yellen's watch. The tone of the rate statement could affect investor sentiment and have an impact on gold prices. It's a virtual certainty that the Fed will leaves rates unchanged this time around, although it's likely that the Fed will raise rates by a quarter-point at the March meeting. Yellen will make way for Jerome Powell, who takes over as chair in early February. Powell is expected to hold the course on monetary policy, which was marked by small, incremental interest rates in order to keep the robust US economy from overheating.