Sample Category Title

Dollar Bears Yield To Higher Interest Rates

Dollar Bears Yield to higher interest rates

There has been a pause for thought in the bearish dollar trend after an enigmatic spike in US Treasury yields yesterday sent dollar bears heading for shelter while leaving a sea of red in their wake across FX markets.

The higher US ten-year yield has triggered risk reduction on weaker short dollar positions. A surge in US bond yields has left more questions than answers. The rationale for the spike in rates probably lies somewhere between 1) supply fears as both ECB and the Federal Reserve are set to commence the weighty task of removing QE, and 2) speculation is seeping in that the FOMC could deliver an upbeat statement with a more hawkish assessment of inflation.

The higher US yields are providing the dollar with a modicum of support, but recently bond yields, ten-year rates, in particular, have offered little traction for the dollar. Rubber would eventually meet road with regards to supply concerns; this fact is as much a factor as are hawkish hopes from the Federal Reserve Board driving this technical momentum.

But US fixed income is the clear driver for now with ten-year yields pushing above 2.70. As the market looks for some consensus, the thematic shift is likely to be confirmed or refuted by the profusion of economic data due later this week.

But do not ignore the Treasury refunding announcement this week as which will be sizable, ultimately until the debts ceiling is resolved little can be issued.

Expect FX traders heads remain on swivels due to the sudden jump in US yields and the abundance of economic data left in the diary this week

The US Stock Markets

The US equity markets are broadly lower with tech and energy stocks accounting for much of the decline. And while the surge in US bond yields has factored, I suspect the busy week ahead on both corporate and economic news has investors reducing risk while banking some well-earned profits.

Oil Markets

Oil market bulls have been watching the USD with exasperation as the reasons to sell oil are outbalancing reasons to buy with the inescapable influence of the stronger dollar clearing the path lower.

But when combing bearish signals from the jump in US rig counts and Iran’s Oil Minister Bijan Zanganeh pushing back against higher prices warning that it would lead to more shale production, the markets remain fragile to the downside.

However, with traders dialling in on Venezuela’s political turmoil, it should continue to offers support as the country remains the most significant risk in the oil markets global supply chain.

Gold Markets

Gold is under pressure due to the surge in global bond yields as central bank get set to reduce stimulus as economies improve. While QE reduction was always on the cards, but the sudden global bond markets repricing caught a consolidating Gold market off guard triggering waves profit taking as higher interest rates make gold less attractive.

There was no surprise that this week’s expected rise in two-way US dollar risk was going to tame the Gold bulls temporarily, but there was no accounting for this inexplicable push higher in global yields that touched multi-year highs. But one day is hardly a trend, and given that there’s little to no consensus agreement as to what’s actually behind the recent bond market fire sale, markets will probably sit tight awaiting the business end of the week which offers more considerable event risk hopefully to show us the way.

The primary focus will be on Dr Yellen opening remarks post FOMC and does she explicitly see inflation picking up or remains a transitory factor in Fed thinking.

G-10

The US dollar continues to consolidate but perhaps with a lot more stronger bias than had been expected due to the bond market fire sale.

The Australian Dollar

It’s impossible for the Aussie to escape the broader US dollar influence but market remain well above the psychological 80 level supporting positive sentiment. And with the RBA conspicuously refraining from any verbal currency pushback, it suggests we are ways away from that trigger point. ON the back of the weaker NZD CPI print, local traders are by extension factoring in a tepid AUD CPI print tomorrow suggesting we could see a significant repricing of risk if the CPI beats estimates. Tomorrow’s CPI will be pivotal for near-term sentiment, but the underpriced STIRT curve remains attractive as the Feb 5 RBA comes into focus.

The Japanese Yen

Bond yields helped underpin the USD ahead of a busy week on the US economic data front.But we remain stuck in the middle of new ranges in USDJPY awaiting the next catalyst. Indeed, the market is still hanging on the premise the BoJ policy does pivot, but with a hefty supply of economic data this week, traders are reducing short dollar risk looking re-engage above 109.50 with stops likely placed above 110.25 as that would be a more precise signal of a trend reversal.

Asia FX

Malaysian Ringgit

The markets opened relatively calm yesterday with the Ringgit caught between portfolio inflows and the USD strength, but the market handling the later better than regional peers. However, yesterday’s spike in Global bond yield in Asia caught regional traders by surprise who had likely become too complacent regarding the USD sensitivity to rising yields. But in fact, its a faster rise in US yields than expected that poses the largest threat to regional currencies, so predictably the bullish bets on the MYR have backed off as profit-taking has moved to the fore.

The short dollar position squeeze occurred across all currencies, so it is not a Ringgit specific move. But two-way dollar risk gave the extensive diary of US economic data. However, there remains much debate about what’s driving this global market sell-off, but we will get further clarity as move through the FOMC and US economic data which will likely clear up some of the debate.

Dollar Recovers Awaits Trump First State Of The Union

Dollar Regains Footing Ahead of State of the Union

The USD surged against all major pairs after having touched three year lows last week. US treasury yields rose with the 10 year yield touching 2.7 percent. President Trump will deliver his first state of the union address on Tuesday, January 30 at 9 pm EST. The Trump administration was behind most of the dollar weakness as comments from Secretary of the Treasury Steve Mnuchin triggered a sell off of the currency. President Trump’s first year has been characterized by political uncertainty even as markets continue a record run and the US economy continues to grow. He is expected to ask for unity as the senate and congress remain deeply divided ahead of the US primary elections in the fall.

- US consumer confidence expected to have risen in January

- BoE Governor Carney testifies before House of Lords

- Trump said his State of the Union address will cover immigration and trade

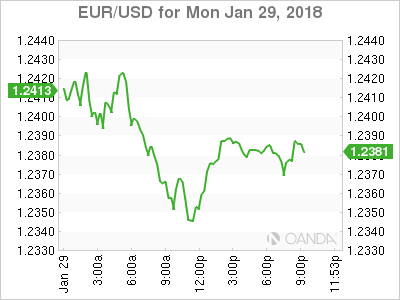

- USD Appreciated Against Majors on Busy Week

The EUR/USD lost 0.33 percent on Monday. The single currency is trading at 1.2388 after the US dollar bounced back from a terrible week. President Trump tried to clarify the comments from Mnuchin and stressed that the dollar should be strong as it is the reflection of a powerful economy. The comments were made during the World Economic Forum at Davos, Switzerland. Trump’s visit had been a question mark given the government shutdown the previous weekend, but the short shutdown allowed the President to attend and extend an olive branch. His America First was softened to First, but not alone, meaning America is open to negotiate. NAFTA and TPP negotiations notwithstanding the President was surprisingly open to new trading deals.

US President Trump will deliver its first Sate of the Union address on Tuesday, January 30, at 9:00 pm EST. Failing to avoid a government shutdown Trump will focus on the positives during his first year. His achievements in passing legislation came late in 2017 but he is sure to mention the tax reform bill. The stock market record breaking pace and overall strength of the economy while inherited will also be mentioned with the infrastructure plan something to look for in the immediate future. The USD got a Trump bump in late 2016 when just after winning the elections .

European bonds rose as the European Central Bank (ECB) gets closer to reducing stimulus with a possible rate hike in early 2019 or sooner. With more central banks shifting to a tighter monetary policy the pressure is on the Fed to keep ahead of the pack or else the USD will keep depreciating in 2018.

US jobs data will start pouring in on Wednesday with the ADP private payroll report and will close with The U.S. non farm payrolls (NFP) that will be published on Friday, February 2 at 8:30 am EST. Economists are expecting the US to add 184,000 positions in January. Last month’s report came in lower than expected but the saving grace for the USD was that hourly wages grew 0.3 percent as expected. There are similar gains forecasted for January wages with a special emphasis on inflationary data as the Fed ponders what to do with stagnant wages despite a strong job component.

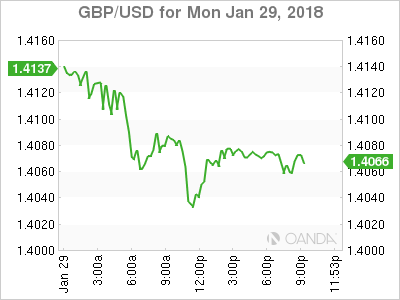

The GBP/USD lost 0.64 percent in the last 24 hours. The currency pair is trading at 1.4072. The surge of the USD combined with political news out of the United Kingdom. Prime Minister Theresa May faces a tough three months ahead of local elections. Her decision to trigger a snap election ending up costing the party dearly and although the probability of a softer Brexit has risen and with it the pound, further uncertainty could trigger a sell off of the currency.

May did not have a great time at Davos and her speech felt flat and prompted new calls for her leadership to end. Europe has been firm on their view of Brexit but lately it has hinted that there are provisions for cancelling the divorce if both parties wish to do so. On the other side Chancellor of the Exchequer Philip Hammond called for a very modest Brexit which might have gone well with the Davos crowd, but are sure to draw heavy criticism amongst conservatives who voted to Leave the EU.

Market events to watch this week:

Tuesday, January 30

10:00am USD CB Consumer Confidence

10:30am GBP BOE Gov Carney Speaks

7:30pm AUD CPI q/q

9:00pm USD President Trump State of the Union

Wednesday, January 31

8:15am USD ADP Non-Farm Employment Change

8:30am CAD GDP m/m

10:30am USD Crude Oil Inventories

2:00pm USD FOMC Statement

2:00pm USD Federal Funds Rate

Thursday, February 1

4:30am GBP Manufacturing PMI

10:00am USD ISM Manufacturing PMI

Friday, February 2

4:30am GBP Construction PMI

Gold Slips As US Dollar Selloff Hits The Brakes

Gold has started the week with losses. In Monday’s North American trade, the spot price for an ounce of gold is $1341.32, down 0.62% on the day. On the release front, Personal Spending slowed to 0.4%, shy of the estimate of 0.6%. On Tuesday, the key indicator is CB Consumer Confidence and President Trump will deliver the State of the Union address.

January has been good to gold, with the metal climbing 2.8% during this period. Gold prices touched $1366 last week, its highest level since August 2017. The US dollar selloff was in full flight on Wednesday, as the dollar tumbled against gold and major currencies following comments from US Treasury Secretary Steven Mnuchin. Speaking in Davos, Mnuchin said that the US was comfortable with a low dollar. This drew a rebuke from ECB President Mario Draghi, who accused the US of targeting the exchange rate. Mnuchin sheepishly backtracked, claiming his remarks had been taken out of context and that he was in favor of a stronger dollar.

In the US, recent GDP releases have pointed to strong growth of 3% or higher. This resulted in some disappointment on Friday, as Advance GDP came in at 2.6%, short of the estimate of 3.0%. The economy grew 2.3% in 2017, compared to 1.6% in 2016. Growth in Q4 was affected by stronger consumer spending, which led to a surge in imports. At the same time, the increase in consumer spending also boosted inflation, as the personal consumption expenditures index, which the Fed prefers to use, rose 1.9% in the fourth quarter, up from 1.3% in Q3. A strong US economy has boosted the manufacturing sector, as durable goods orders in December hit 2.9%, crushing the estimate of 0.6%. This was the highest gain in six months, and helped make 2017 a banner year. Durable good orders increased 5.8% in 2017, the sharpest expansion since 2011.

Sharp Losses For Pound, Investor Eye Carney Speech

The British pound has posted sharp losses to kick off the week. In Monday's North American session, GBP/USD is trading at 1.4035, down 0.91% on the day. On the release front, there are no British events. In the US, Personal Spending slowed to 0.4%, shy of the estimate of 0.6%. On Tuesday, the UK releases Net Lending to Individuals. In the US the key indicator is CB Consumer Confidence and President Trump will deliver the State of the Union address.

The US dollar continues to struggle, and the pound jumped on the bandwagon, jumping 4.0% in January. Last week, GBP/USD pushed above 1.43 for the first time since June 2016. The greenback didn't get any favors from US Treasury Secretary Steven Mnuchin, who said that the US had no problem with a weak US dollar. That comment pushed the dollar sharply lower, with the pound gaining 1.5% on Wednesday.

The EU has drafted guidelines regarding the transition period after Britain leaves the European Union in 2019. The European proposal calls for Britain to abide by EU rules, including freedom of movement, during the transition period which would last until 2020. However, it's unlikely that the May government will simply accede to this proposal. Britain wants a longer transition period as well as say in the makeup of the transition period.

In the US, recent GDP releases have pointed to strong growth of 3% or higher. This resulted in some disappointment on Friday, as Advance GDP came in at 2.6%, short of the estimate of 3.0%. The economy grew 2.3% in 2017, compared to 1.6% in 2016. Growth in Q4 was affected by stronger consumer spending, which led to a surge in imports. At the same time, the increase in consumer spending also boosted inflation, as the personal consumption expenditures index, which the Fed prefers to use, rose 1.9% in the fourth quarter, up from 1.3% in Q3. A strong US economy has boosted the manufacturing sector, as durable goods orders in December hit 2.9%, crushing the estimate of 0.6%. This was the highest gain in six months, and helped make 2017 a banner year. Durable good orders increased 5.8% in 2017, the sharpest expansion since 2011.

US Dollar Rebounds. What Next?

Another bounce in the dollar to fade? The greenback was the top performer while the pound lagged. Japanese employment and retail sales are due up next.

US Treasury yields continued the march higher with 10-years hitting 3.70% on Monday and that was part of the reason for a bounce in the dollar. Another factor was US personal income beating expectations a +0.4% m/m compared to +0.3% expected. Spending was slightly lower than expectations but the prior revised higher. The Atlanta Fed pegged its first tracking estimate at Q1 GDP at 4.2%.

While there is solid optimism about the US dollar, there are higher hopes elsewhere and that's the paradigm driving the dollar trade right now. All the money that flowed into the US dollar during the European crisis is now headed back home.

Emerging market and commodity investors are also shifting towards more aggressive investments and that's usually outside the US.

So long as risk appetite remains robust – and there is no reason to think it won't – then dollar bounces will continue to be sold. Even on Monday, the strong start for the dollar that pushed the euro down to 1.2337 faded later and it bounced to 1.2375.

In terms of USD/JPY, the pair battled to get above 109.00 and was helped by talk of a BOJ/MOF meeting but it's too soon to talk about intervention, especially with the dollar struggling so broadly and Japan's economy doing relatively well. As for what's next, Japanese employment is due at 2330 GMT but the more-intriguing release is 20 minutes later with retail sales. The consensus is for a 0.4% m/m decline.

It's unlikely to be a market mover but if Japan can put together a long string of strong data points, then yen buying could get very aggressive.

Spending Closed the Year Strong

Personal income increased a better than expected 0.4 percent in December while personal spending increased 0.4 percent. Personal spending was revised up to 0.8 percent in November from 0.6 percent originally.

Personal Income Stronger in December

Personal income increased a better than expected 0.4 percent in December with no change reported to the 0.3 percent print in November. Meanwhile, disposable personal income increased 0.3 percent while real disposable personal income increased 0.2 percent after a flat month reported for November. Clearly, personal income, specifically real personal disposable income, has improved since its weak performance in late 2016 and early 2017. However, both measures continue to trail the growth rate of real spending, which improved further in the last quarter of the year.

This means that the saving rate remained low at the end of the year, at 2.4 percent, down from a 6+ percent rate in late 2015. That said, the U.S. consumer will need to see continuous growth in income over the year in order to be able to continue to keep up the current pace of consumption. It is true that the gains in consumer confidence as well as in financial (stock market) and housing wealth are making Americans feel much better today than they were previously.

Spending Boomed at the End of 2017

Personal spending was in line with expectations in December, up 0.4 percent. However, the November measure, which was originally reported at 0.6 percent, was revised to an increase of 0.8 percent. This means that November was a very strong month for consumption. In real terms, personal spending increased a weaker than expected 0.3 percent in December but the November number was upwardly revised to an increase of 0.5 percent. Therefore, the end of the year was one of the strongest performances for consumption in several years even though the year as a whole was not as strong as previous years.

The numbers on consumption during the last quarter of the year also show that consumption was on an upward trajectory at the end of 2017. This report also confirmed the strong performance of holiday sales reported several weeks ago. However, as we said above, the strength in spending may not last much longer if we do not see further improvement in income measures.

Of course, consumers are looking forward to an increase in income coming from the effects of tax reform. They could also be planning to increase borrowing in order to complement any short to medium term shortfall in income as they have been doing for more than a year.

PCE Index Remained Contained in December

Consumer prices, as measured by the PCE deflator, were in line with expectations, increasing 0.1 percent for the overall index and 0.2 percent for the PCE deflator excluding volatile items like food and energy. Thus, even inflation behaved well at the end of the year, supporting higher real income as well as higher real spending.

Gold Creates Bearish Correction; Next Level to Watch 23.6% Fibonacci Mark

Gold is moving lower over the last hours following the strong pullback from the 4-month high of 1366. The price headed south and is challenging the short-term ascending trend line, which has been holding since December 12, near 1345 support level. The short-term technical indicators seem to be turning negative and point to more weakness in the market.

In the 4-hour chart, the RSI indicator is pointing sharply to the downside, below the 50 level, while the MACD oscillator is falling and is losing momentum in the positive territory. Technical indicators are signaling further losses in the near-term.

Currently, the price is slipping below 1345 (immediate support) and the 40-day SMA, opening the door to test the 23.6% Fibonacci retracement level at 1335 of the up-leg with the low of 1236 and the high of 1366. Clearing this key level could see additional losses towards the 1331 barrier.

Conversely, upside moves are likely to find resistance at 1357 but the precious metal would first need to go through the 20-day SMA. A climb above the aforementioned obstacles could see gains towards the 1366 barrier.

Sunset Market Commentary

Markets:

The global core bond sell-off accelerated today. German Bunds underperformed US Treasuries. The move was mainly technical in nature. US yields pierced through key resistance levels last week (2.42% for 5y and 2.64% for 10y), creating space for further gains. Good spending/income data and in-line-with consensus PCE inflation had no specific impact. An attempt to go through similar resistance in German yields failed last week, but today's attempt succeeds. The German 2y yield moves above -0.55%, the 5y yield above -0.05% (first time in positive territory since the end of 2015) and 10y yield above 0.62%. Last week's upbeat economic assessment by the ECB and subtle hint towards a mid-2019 rate hike still resonate cross markets. Dovish comments by ECB chief economist Praet couldn't change the tide. Intraday changes on the German yield curve range between +2.2 bps (2y) and +5.5 bps (10y). US yields add 1.6 bps (2y) to 3.5 bps (10y). 10y yield spread changes vs Germany are nearly unchanged with the periphery outperforming (-4 bps).

The dollar finally bottomed at the end of last week and this process continued today. There was little highly profile news to explain the move. The laws of gravity are again weighing more on USD/JPY than on USD/EUR. There was no one-on-one link between the USD's performance and interest rate differentials. Even so, we have the impression that the environment of higher yields (with US and EMU yields breaking beyond key levels) is becoming again a bit more supportive for the USD. Investors might also turn a bit more cautious on USD shorts going into Wednesday's Fed meeting. EUR/USD trades currently in the 1.2360 area. Soft comments from ECB Praet helped the euro correction. USD/JPY underperforms other USD cross rates. The pair doesn't succeed any further gains beyond Friday's late session 'spike'.

The recent sterling rally lost momentum at the end of last week. Investors grew less convinced that Brexit negotiations could go rather smoothly. There was plenty of noise on a flaring up of internal opposition against PM May within the Conservative Party. The House of Lords also sees some 'fundamental flaws' to the UK Brexit law. EUR/GBP rebounded north of 0.88 this morning, the move was reversed later, at least partially driven by the overall correction of the euro. EUR/GBP trades little changed in the 0.8775 area. The correction of cable continues. The pair trades in the high 1.40 area (compared to a top of 1.4345 last week).

European stock markets trade flat today. Main US indices opened on a weak footing with Nasdaq underperforming after Nikkei reported, without citing anyone, that Apple notified suppliers it decided to cut iPhone X's production target for January-March period to about 20m units due to slower-than-expected sales in year-end holiday shopping season in key markets such as Europe, the US and China.

News Headlines:

US consumer spending rose at a solid pace in December (0.4%) after an upwardly revised advance a month earlier (0.8%) as shoppers splurged during the holiday season. While incomes also rose (0.3%), the saving rate fell to a fresh 12-year low. The Federal Reserve's preferred inflation gauge -- tied to consumption -- rose 0.1% in December from the previous month and 1.7% from a year earlier. Excluding food and energy, so-called core prices climbed 0.2%, matching the survey median. The core was up 1.5% from December 2016.

The ECB will only stop pumping cash into the euro zone economy when it is confident that inflation is heading towards its target even without its extra help, the chief economist Praet said. He also added the ECB had not decided yet how to end the asset purchase programme, whether gradually or at once.

EURJPY: Declines On Bear Pressure

EURJPY - The pair now looks to weaken further after it saw a move lower during Monday trading session. On the downside, support comes in at the 134.00 level where a break if seen will aim at the 133.50 level. A cut through here will turn focus to the 133.00 level and possibly lower towards the 132.50 level. On the upside, resistance resides at the 135.00 level. Further out, we envisage a possible move towards the 135.50 level. Further out, resistance resides at the 136.00 level with a turn above here aiming at the 136.50 level. On the whole, EURJPY faces further weakness threats.

Copper – Repeated Recovery Rejections Keeps the Downside Vulnerable

Copper price is struggling to hold recovery as repeated upside rejection occurred today ($3.1975) after Friday' long-legged Doji signaled that weakness from last week's high at $3.2565 might be running out of steam. Long bullish candle that was left on Wednesday after the biggest one-day rally since 16 Oct, formed bullish outside day pattern which continues to underpin, along with rising and widening daily cloud, but upside attempts so far stay under cracked pivotal barrier at $3.2384 (Fibo 61.8% of $3.3200/$3.1065 downleg). The downside is expected to remain vulnerable while the latter stays intact, with risk of retesting Friday's low ($3.1840) and further retracement of $3.1065/$3.2565 upleg on break lower. Daily MA's are in mixed setup; RSI is neutral, while momentum studies remain negatively aligned and not showing clear near-term direction. Fresh bearish signal could be expected on firm break below Friday's low ($3.1840) while sustained lift above Fibo barrier at $3.2384 will be bullish signal.

Res: 3.2132; 3.2384; 3.2565; 3.2696

Sup: 3.1932; 3.1840; 3.1638; 3.1419