Sample Category Title

U.S Dollar Bulls Require A Wider Yield Spread

Monday January 29: Five things the markets are talking about

U.S Treasuries have extended their selloff, pushing yields to its highest in three-years as capital markets prepare itself for a busy week of data releases and monetary policy announcements.

Note: Higher sovereign yields have given the 'mighty' U.S dollar a temporary lift from its multi-year lows against G20 currency pairs print from last week. Is this sustainable? Not if other sovereign yields back up at the same rate. U.S dollar bulls require a wider spread.

Investors can expect the FX market to most likely to continue to lean on the U.S dollar until they elicit another response from U.S Treasury Secretary Mnuchin that suggests, 'he cares' – because U.S economic data alone will find it rather difficult to turn the tide of the current general dollar weakness.

On Wednesday (Jan 31), Federal Open Market Committee (FOMC) gathers for Chair Janet Yellen's final meeting on interest rates before her term ends.

This is also jobs week in the U.S and on Friday (Feb 2) U.S employers are expected to have added more jobs in January than a month earlier. Government data is also expected to show the jobless rate held steady atop of its two-decade low, and the pace of wage growth picked up from a year earlier.

In China, estimates of Chinese manufacturing and services industries are due Wednesday (Jan 31), while in Europe, growth and inflation are on display this week. On Tuesday (Jan 30), data is expected to show the euro economy with a solid expansion, while on Wednesday (Jan 31), the core euro-zone inflation report may show an uptick from a year ago.

Elsewhere, the sixth round of NAFTA talks conclude in Montreal.

On Tuesday evening (9:00 pm EDT), President Trump delivers his first State of the Union address – he is expected to build momentum for legislation on infrastructure and immigration.

1. Global stocks rally pauses

U.S indices finished last week on yet another positive note pressing new highs.

In Japan, the Nikkei ended flat in choppy trade overnight, with gains in cyclicals (computer chips) offset by weakness in shares sensitive to domestic demand, notably railroad and construction companies. The broader Topix produced a small gain (+0.1%).

Down-under, Aussie shares rose +0.4% on Monday, led by financials, taking a cue from Wall Street, while in S. Korea, the Kospi hit another record high, climbing +0.91%.

In Hong Kong, the Hang Seng Index fell overnight, ending a seven-day winning streak, as the market took a breather after repeatedly hitting record highs. At close of trade, the Hang Seng index was down -0.56%, while the Hang Seng China Enterprises index fell -0.47%.

In China, stocks tumbled on Monday, with the blue-chip index posting its worst day in more than two months, led by a slump in consumer and healthcare firms as investors booked profits after a recent strong rally. The Shanghai Composite index was down -0.97%, while the blue-chip index was down -1.81%.

In Europe, regional indices trade mostly lower, tracking the declines in U.S futures after their record closes stateside Friday.

U.S stocks are set to open in the black (-0.3%).

Indices: Stoxx600 – 0.2% at 399.8, FTSE flat at 7669, DAX -0.4% at 13287, CAC-40 -0.2% at 5521, IBEX-35 -0.5 at 10544, FTSE MIB -0.2% at 23820, SMI -0.2% at 9497, S&P 500 Futures -0.3%

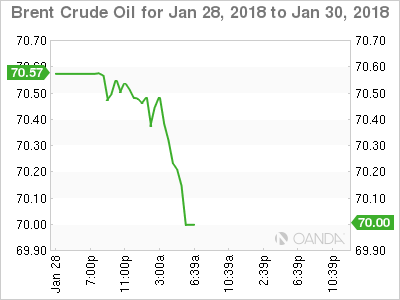

2. Oil dips as North American output soar, gold lower

Ahead of the U.S open, oil prices have dipped as soaring North American production is seen as undermining efforts led by OPEC and Russia to tighten supplies.

Brent crude futures are holding above +$70 per barrel, but are down by -19c from Friday's close at +$70.34 a barrel. U.S West Texas Intermediate (WTI) crude futures are at +$66.19 a barrel, up +5c.

Despite generally bullish sentiment, consensus believes the market is beginning to come under pressure from rising output in North America.

U.S crude production has grown by over +17% mid-2016 to +9.88m bpd in mid-January.

Note: Output is expected to break through the +10m bpd soon.

Baker Hughes on Friday stated that U.S energy companies added 12 oilrigs drilling for new production last week, taking the total to 759.

U.S production is already on par with top OPEC exporter, Saudi Arabia. Only Russia produces more.

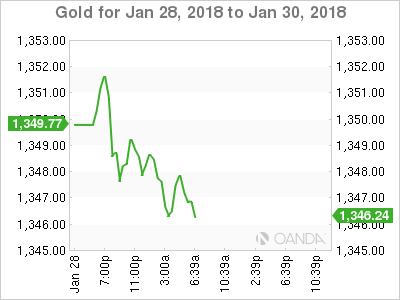

Ahead of the U.S open, gold prices have eased a tad as the U.S dollar gained some lost ground. Nevertheless, the yellow metal continues to hover within striking distance of its 17-month high print of last week. Spot gold is down -0.2% at +$1,347.60 per ounce.

3. Likelihood grows for a Fed rate rise in March

The recent rise in U.S market inflation expectations – boosted by rising oil prices – goes someway to support the Fed's confidence in its inflation outlook.

Currently, the market is not expecting an interest rise at the policy decision on Wednesday (Jan 31) – the Fed fund odd's are +6% for a back up in o/n rates.

Note: It will be Chair Janet Yellen's final meeting on interest rates before her term ends.

The odd's for a hike in March – the first meeting this year that has a press conference and fresh projections outlook – is around +70%.

Note: The Fed's 'dot plot' forecasts three rate increases for 2018.

The yield on U.S 10-year Treasuries has backed up +4 bps to +2.70%, the highest in almost four-years. In Germany, the 10-year Bund yield increased +2 bps to +0.65%, the highest in more than two-years, while in the U.K, the 10-year Gilt yield climbed +1 bps to +1.451%, the highest in a year.

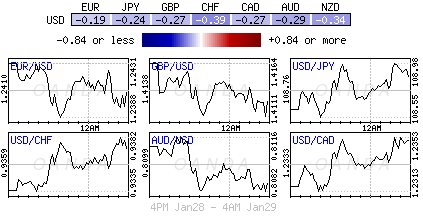

4. Dollar consolidates for now

The U.S dollar starts this week somewhat consolidating, as G10 currencies failed to break last Thursday's highs.

The dollar has advanced after capping a seventh week of losses on Friday. The yen (¥108.69) fell as the BoJ downplayed Governor Kuroda's comments on stronger inflation. The U.S dollar has been unable to remain above the psychological ¥109 level in a quiet session.

GBP (£1.4090) remains on the back foot as pressure builds on PM Theresa May over Brexit.

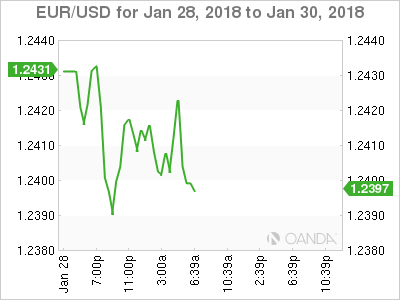

EUR (€1.2401) trades atop of its recent low registered outright after President Trump's reply to the 'weak' dollar environment comment last week. The pair tested €1.2385 before inching back above €1.24 in quiet trading.

Bitcoin (BTC) has climbed, holding its value above +$11,000 even after a heist of nearly +$500m in a different digital token prompted calls for more cryptocurrency regulation.

5. German import prices rose +3.8% y/y

The index of German import prices rose by +3.8% on an annual average in 2017 compared with 2016 (2016: –3.1% compared with 2015).

Note: This was the highest price increase since 2011 (+6.4% compared with 2010).

In December 2017 the index of import prices increased by +1.1% compared with the same month of the preceding year, and the lowest price increase since November 2016 (+0.3% compared with November 2015).

In November and in October 2017 the annual rates of change were +2.7% and +2.6%, respectively. From November to December 2017 the index rose by +0.3% m/m.

Euro Softens, Investors Await German CPI, Eurozone GDP

The euro has posted slight losses in the Monday session. Currently, EUR/USD is trading at 1.2419, down 0.09% on the day. On the release front, German Import Prices slowed to 0.3%, matching the forecast. In the US, today’s key event is Personal Spending, which is expected to edge lower to 0.5%. Tuesday will be busier, with key events on both sides of the pond. Germany releases Primary CPI and the eurozone publishes Preliminary Flash GDP for fourth quarter 2016. In the US, the key event is CB Consumer Confidence, and President Trump will deliver the State of the Union address.

The markets have become accustomed to GDP releases above 3.0%, so Advance GDP for Q4 was disappointing. The reading of 2.6% fell short of the estimate of 3.0%. The economy grew 2.3% in 2017, compared to 1.6% in 2016. Growth in Q4 was affected by stronger consumer spending, which led to a surge in imports. At the same time, the increase in consumer spending also boosted inflation, as the personal consumption expenditures index, which the Fed prefers to use, rose 1.9% in the fourth quarter, up from 1.3% in Q3. Meanwhile, the US manufacturing sector is booming, as durable goods orders in December hit 2.9%, crushing the estimate of 0.6%. This was the highest gain in six months, and helped make 2017 a banner year. Durable good orders increased 5.8% in 2017, the sharpest expansion since 2011.

The euro posted sharp gains on Thursday after comments from ECB President Mario Draghi, but the gains didn’t last, as EUR/USD continues to show limited movement. Draghi was more dovish than expected, saying that the ECB was prepared to increase QE in “size or duration”, a reminder to the markets that it is premature to expect normalization anytime soon. He added that interest rates would not rise until well after the ECB’s asset-purchase program (QE) was over. The QE program will not end until September at the earliest, so Draghi essentially ruled out any rate hikes before early 2019. A new headache for ECB policymakers is the streaking euro, which has hit 3-year highs against the US dollar. Investors are worried that a stronger euro could hurt exports and company earnings. EUR/USD has jumped 3.3% in January, as the dollar continues to struggle.

EUR/CHF Slides To More Than Two-Month Low

Did the SNB intervene in the FX market to prevent further CHF strength?

The Swiss franc started the year in the best possible way against the single currency, at least in the view of the Swiss National Bank, as EUR/CHF climbed to its highest level since January 2015 and hit 1.1832. Unfortunately, for Thomas Jordan his team, this period of respite was short-lived as the currency pair headed back down over the last week and fell as low as 1.1572 during the Asian opening.

The second half of 2017 were like holidays for the SNB, with EUR/CHF climbing as much as 10% to reach 1.1832 on January 15th, and allowed the monetary institution to reduce dramatically – if not completely phasing out – it FX intervention. Indeed, total sight deposits at the SNB stabilized at around CHF 575 billion, down from the record level of CHF 579.7 billion reached in August last year.

Last night, EUR/CHF’s price action was volatile before the currency pair starts to pick up towards 1.1630. There is rumours that the SNB has had to step to stop further CHF appreciation. As usual, it is hard to tell whether the rumours are true or not. However, given the sharp appreciation of the Swiss Franc of the past couple of weeks, there is little doubt the central bank won’t stand and watch the CHF going to the moon. Market participants will get more information next Monday when the SNB will release its weekly report. We believe the central bank won’t let the currency pair move below the 1.15 threshold.

Japan economy is in good shape

Japan presents modest to promising economic results since the beginning of the year. The BoJ remained optimistic as to reaching its “medium- to long-term inflation expectations”, thus approaching its CPI Y/Y 2% target according to its January quarterly outlook for economic activity and prices report (effective December 31st 2017 inflation rate at 1%). With positive output gap, Japan is showing signs of improvement in private consumption (view lifted for the first time in 7 months by the Japanese Cabinet Office), though still not strong enough according to officials. Tight market conditions also allowed Japanese government’s view to be revised upward, with a December unemployment rate expected to remain at 2.70%, a 24-year low (release on January 30th 2018).

Consumer spending slow increase (December Core CPI Y/Y at 0.90%) is attributed to low wage growth according to Shinzo Abe who declared on December 26th 2017 that companies have to raise wages by 3% or more, in order to broaden the benefits of his Abenomics stimulus. On the trade side, Japan presented robust December Exports Y/Y at 9.30% (slightly below consensus at 10.10%) and December Imports Y/Y at 14.90%, suggesting economic data that are in line with global economic growth. This week we will be looking at December Retail Sales and Household Spending on Tuesday and December Industrial Production on Wednesday and see if these indicators are supporting growth.

Recent published indicators suggest that Japan might be on the way to leaving its 2-decades long stagnation phase, though the BoJ has still a long way to go until reaching its 2% headline inflation rate target.

CRUDE OIL Holding Above 66

Crude oil keeps increasing. Strong support is given at 60.93 (05/01/2018 low). Expected to keep increasing as demand remains strong.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness is very likely. For the time being the pair lies in an upside trend since June 2017. Support lies at 42.20 (16/11/2016) while resistance point is located at 77.83 (20/11/2014). Crude oil is trading largely above its 200 DMA.

SILVER Skewed To The Downside

Silver is slightly decreasing but remains above 17.16. Hourly support is at 16.75. The short-term technical structure is turning positive while hourly resistance lies at 18.21 (08/09/2017 high).

In the long-term, the trend remains negative/ flattish. Further downside is very likely. The pair is trading slightly above its 200 DMA. Resistance is located at 21.58 (10/07/2014 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Increase Maintained

Gold increases, though a slight decline below the 1'350 mark. Hourly support is at 1'331 (23/01/2018 low) while further support remains at 1'323 (12/01/2018 low). The technical structure indicates further short-term upside moves.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1'392 (17/03/2014) is required to confirm it. A major support can be found at 1'045 (05/02/2010 low).

BITCOIN Sideways Trading

Bitcoin is trading sideways. Hourly support is at 9'185 (17/01/2018 low) while resistance is located at 12'130 (18/01/2018 high). The short-term technical structure might be suggesting potential increase.

In the long-term, the digital currency has had an exponential growth but also presented important downturns. There is decent likelihood that the currency could stabilize between 9'000 - 12'000 in 2018. Bitcoin is trading far above its 200 DMA (5K+ gap)

EUR/CHF Decline Confirmed

EUR/CHF is trading slightly higher. Hourly support at 1.1607 (18/12/2017 low) is now broken. Expected to show further short-term downside moves.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's slowing QE program is likely to cause buying pressures on the euro, which should weigh in favour of the EUR/CHF. Support can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

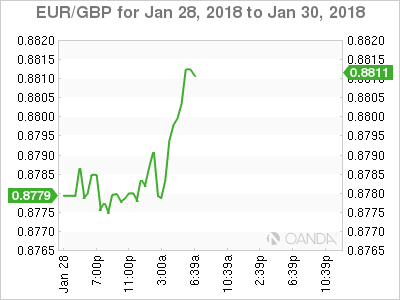

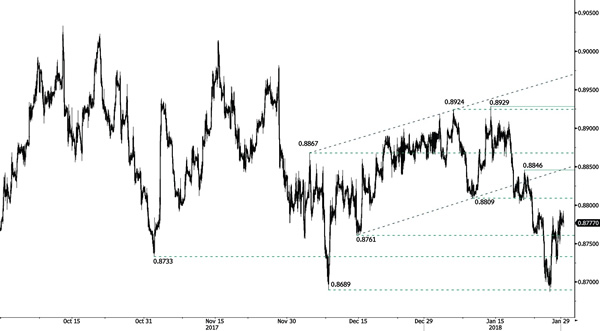

EUR/GBP Trading Higher To Target At 0.88

EUR/GBP is bouncing back after slight decrease on Friday. The pair is approaching resistance at 0.8846 (19/01/2018 high). Expected to show further short-term strength.

In the long-term, the pair has largely recovered from lows in 2015. The technical structure suggests an upside momentum. The pair is trading below the range of its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Higher Ride Continues

AUD/USD's upside pressures keeps growing. Support stands at 0.7957 (23/01/2018 low). The technical structure indicates further short-term upside move.

In the long-term, the trend is turning positive. Key support stands at 0.6009 (31/10/2008 low). A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view (drawing near).