Sample Category Title

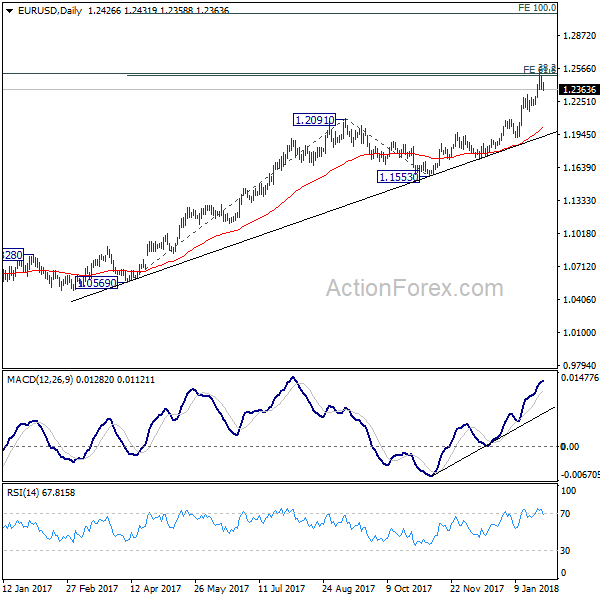

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2366; (P) 1.2430 (R1) 1.2491; More....

Intraday bias in EUR/USD remains neutral at this point but further rally is expected as long as 1.2222 support holds. On the upside, sustained break of 1.2494/2516 resistance zone will extend recent rally to 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

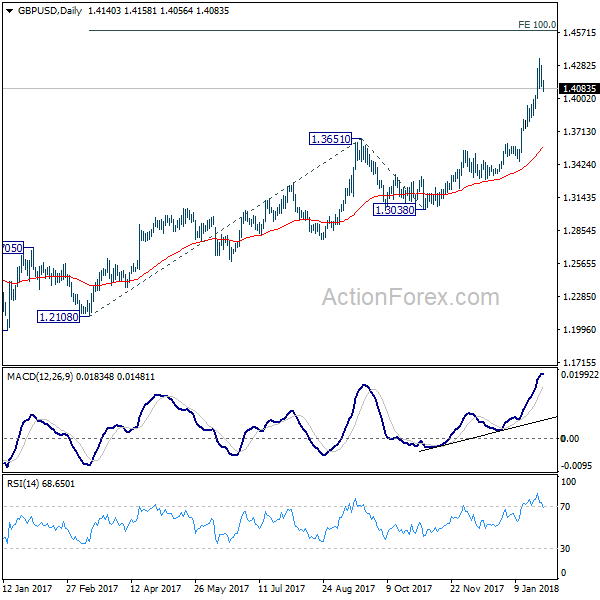

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4079; (P) 1.4180; (R1) 1.4256; More.....

GBP/USD's retreat from 1.4345 extends lower today but outlook remains unchanged. Intraday bias stays neutral and further rise is still expected with 1.3915 support intact. On the upside, break of 1.435 will extend the up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Dollar Recovery Continues, Sterling Weighed Down by Political Uncertainties

Dollar's recovery continues in early US session and is gathering some extra momentum against Sterling and Euro. But still, there is no clear indication of near term trend reversal yet. Meanwhile, Sterling is under broad based selling pressure. Profit taking after recent strong rally is one of the reasons. Additionally, the pound is weighed down by re-emerging political uncertainties in the UK. Elsewhere in the FX markets, Euro is following as the second weakest one. Kiwi and Aussie are also soft.

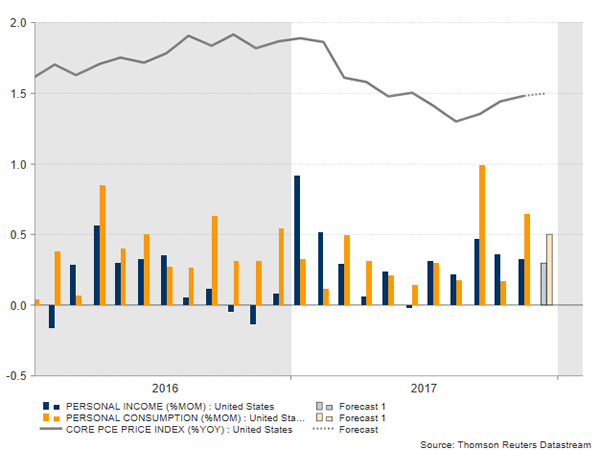

Release from US today, personal income rose 0.4% in December versus expectation of 0.3%. Personal spending rose 0.4%, in line with consensus. Headline PCE slowed to 1.7% yoy. Core CPI was unchanged at 1.5% yoy. Released earlier, German import price index rose 0.3% mom in December.

Sterling broadly lower on political uncertainties

Sterling tumbles broadly today on re-emergence of political uncertainties. It's reported that Prime Minister Theresa May could face another leadership challenge after the House of Lords Constitution Committee criticize3d that May's Brexit legislation had "fundamental flaws". The committee chairwoman Baroness Taylor said that "we acknowledge the scale, challenge and unprecedented nature of the task of converting existing EU law into UK law, but as it stands this bill is constitutionally unacceptable." And, there is additional complexity because "in many areas the final shape of that law will depend on the outcome of the UK's negotiations with the EU". The committee added that the method proposed to create a new category of "retained EU law" will cause "problematic uncertainties and ambiguities."

Additionally, regarding the transition deal is set to insist that UK must apply EU laws as if it were a member state during the transition period. And such compliance is expected to be unconditional. On the other hand, the UK is clearly uncomfortable with the demand. Brexit secretary David Davis hinted that he would demand the power to object. As Davis said, "means to remedy issues" are needed if laws were "deemed to run contrary to our interests". But some EU officials see the UK's position on it being counter productive, in particular as Prime Minister Theresa May is targeting to complete a transition deal in March, as businesses requested.

ECB Praet: Some distance from meeting ending QE

ECB chief economist Peter Praet sounded cautious as he pushed back the idea of ending the asset purchase program. He said that ECB is still "some distance" away from meeting the three measurements on the the program. And the three criteria are:

- Firstly, "headline inflation will have to be on course to reach levels below, but close to, 2 percent by the end point of a meaningful medium-term horizon."

- Secondly, "the Governing Council wants to be sure that the expectation of an upward adjustment in inflation has a sufficiently high probability of being realized and is being met on a sustainable basis."

- Thirdly, "if the inflation outlook is overly dependent on monetary support, the upward adjustment cannot be considered sustained. So we want to verify that the path would be maintained even in less supportive monetary policy conditions."

Praet emphasized that "the transition toward a normalization will begin once we have established that there is a sustained adjustment in the path of inflation." However, "despite the strong cyclical momentum, domestic price pressures remain subdued, as do measures of underlying inflation."

ECB Governing Council member Klass Knot delivered some hawkish comments over the weekend. He said "there is no reason whatsoever to continue" the EUR 30b a month asset purchase program after it ends in September. He added "we don't have to communicate yet that it will be over after September, but I think that's where we're headed." Meanwhile, interest rates would stay low in the coming years. Knot noted that "Interest is mainly low because there are more people that want to save, than that want to invest. This will change as the economy grows, but that will take time."

FOMC to highlight a busy week

The highlight of the coming week is the FOMC meeting. This is also the last time for outgoing Fed Chair Janet Yellen to preside the meeting. While it has been widely expected that no change would be made in the monetary policy, the market focus is on the Fed's economic outlook and whether there are hints on the rate hike path. Notwithstanding the fact that inflation has remained soft, the robust employment market, with unemployment rate below the Fed's long-term target, should have anchored the Fed's confidence over the economic outlook. We do expect the Fed to address the issue recent USD weakness. On the monetary policy outlook, the market continued to price in over 70% of a rate hike in March.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4079; (P) 1.4180; (R1) 1.4256; More.....

GBP/USD's retreat from 1.4345 extends lower today but outlook remains unchanged. Intraday bias stays neutral and further rise is still expected with 1.3915 support intact. On the upside, break of 1.435 will extend the up trend to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, break of 1.3915 will argue that, at least, deeper pull back in underway to 1.3651 resistance turned support.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | German Import Price Index M/M Dec | 0.30% | 0.20% | 0.80% | |

| 13:30 | USD | Personal Income Dec | 0.40% | 0.30% | 0.30% | |

| 13:30 | USD | Personal Spending Dec | 0.40% | 0.40% | 0.60% | 0.80% |

| 13:30 | USD | PCE Deflator Y/Y Dec | 1.70% | 1.70% | 1.80% | |

| 13:30 | USD | PCE Core M/M Dec | 0.20% | 0.20% | 0.10% | |

| 13:30 | USD | PCE Core Y/Y Dec | 1.50% | 1.50% | 1.50% |

Pound Slips as Brexit Talks Resume; Dollar Waits for PCE Inflation

Here are the latest developments in global markets:

FOREX: The dollar consolidated gains earned early in the day on the back of rising US bond yields which jumped to peaks last seen in 2014. The dollar index was trading at 89.60 (+0.22%) and dollar/yen was steady at 108.70 (+0.05%). Euro/dollar eased to 1.2397 (-0.19%) as German bonds yields continued to rise for the fourth day reaching two-year highs after the Dutch central bank said on Sunday that the ECB should be clear on its plans to end the asset purchase program in September. Pound/dollar was the worst performer, correcting lower to 1.4070 (-0.70%) in the first day of the new Brexit phase where EU foreign ministers will discuss terms regarding transition period. Although the EU leaders showed their thumbs to move Brexit talks to the next stage, some believe that the UK is not ready to complete the divorce.

STOCKS: European stocks were in the red except the British FTSE 100. The pan-European STOXX 600 was down by 0.23% at 1100 GMT unable to gain from upbeat AMS earnings results. The Austrian chipmaker AMS saw its shares surging by 17.60% after its revenues doubled in 2017 and its iPhone component supplier upgraded its growth forecasts more than expected. The blue-chip Euro STOXX 50 retreated by 0.30% weighed by losses in healthcare and consumer cyclicals. The German DAX 30 lost 0.19%, the Spanish IBEX 35 decreased by 0.32% and the French CAC 40 edged down by 0.04%. On the other hand, the UK's FTSE 100 increased by 0.20%.

COMMODITIES: Oil prices were on the backfoot as the US oil production seemed to offset OPEC-led supply cuts. WTI crude was last down by 0.50% on the day at $65.80 per barrel and Brent was weaker by 0.88% at $69.90. Gold moved up by 0.20% to $1346.40 per ounce.

Day ahead: US PCE inflation eyed; Japanese employment data due in Asian session

The dollar will remain in the spotlight during the European afternoon on Monday as inflation data and figures on consumption out of the US are expected to bring fresh volatility to the currency.

The core PCE index which excludes volatile items - the Fed's most preferred inflation measure - is expected to remain steady at 1.5% y/y in December at 1330 GMT, finishing 2017 below the Fed's target of 2.0%, while on a monthly basis, the gauge is anticipated to inch up from 0.1% to 0.2%. However, personal consumption and personal spending figures released at the same time might gather greater attention as any surprise to the upside would signal higher inflationary pressures for 2018. According to forecasts, personal income is said to grow at November's pace of 0.3% m/m, whereas personal spending is projected to slow down to 0.4% m/m from 0.6% seen in the previous month.

Later in the day, the Asian session will see the release of the Japanese household spending and employment data at 2330 GMT. While the employment stats are forecasted not to deviate much from previous prints in December, with the unemployment rate standing flat at a multi-decade low of 2.7% and the jobs to application ratio edging up to a fresh 44-year high of 1.57, household spending is seen declining on a monthly basis. Particularly the gauge might have fallen by 0.6% m/m after it surged by 2.1% in November, posting the biggest expansion since March. On an annual basis, the measure is expected to ease to 1.6%.

A few minutes later, December's Japanese retail sales might come softer at 1.8% m/m at 2350 GMT.

Beyond the above releases, the economic calendar is relatively light today with New Zealand's trade data for December gaining some interest. Those are scheduled for release at 2145 GMT.

Brexit developments will also be in focus as negotiations on transition period resume today, while discussions on other issues including trade will be in preparation.

In equity markets, corporate earnings releases will continue to keep investors busy.

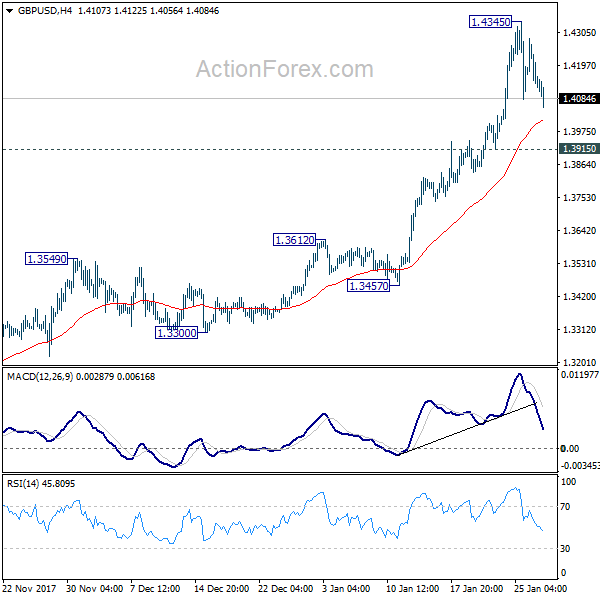

GBPUSD Selling Accelerating Below 1.4082

The British pound is gathering downside momentum against the greenback on Monday, with price-action falling well below the 1.4100 level. The GBPUSD pair is currently trading around the 1.4070 level, which remains close to the current intraday price-low, at 1.4061. The sell-off in the pound is largely due to growing unhappiness inside the ruling Conservative party, over British PM Theresa May's handling of Brexit negotiations with the European Union.

GBPUSD selling is likely to gather momentum while trading below the 1.4082 level, with sellers aiming towards the 1.4041 and 1.4000 levels.

If price-action can move above the 1.4082 level on the GBPUSD pair, buyers may test towards the 1.4109 and 1.4171 levels.

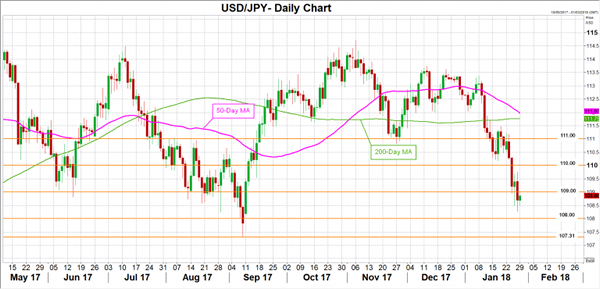

USDJPY Still Under Pressure Below 108.98 Level

The U.S dollar continues to see selling pressure against the Japanese yen in early week trading, with the pair so far ignoring a bounce-back in the broader U.S dollar index. The USDJPY pair currently trades well below the 109.00 mark, as buyers remain cautious after last week's strong sell-off in the U.S dollar. Traders now look to the release of the CORE PCE Index later today, and a steady stream of high-impacting macroeconomic data coming out from the United States economy this week.

The USDJPY pair to remain under pressure while price-action trades below the 108.98 level. Key downside support is located at 108.51 and 108.27.

If the USDJPY pair moves above the 108.98 level, further upside towards 109.30 and 109.59 seems possible.

DAX Quiet in Light Economic Start to Week

The DAX is showing little movement in the Monday session. Currently, the index is trading at 13,334.50, down 0.04% since the close on Friday. On the release front, there is just one eurozone indicator. German Import Prices slowed to 0.3%, matching the estimate. On Tuesday, Germany releases Primary CPI and the eurozone publishes Preliminary Flash GDP for fourth quarter 2016. In the US, President Trump will deliver the State of the Union address.

The euro posted sharp gains on Thursday after comments from ECB President Mario Draghi, but the gains didn't last, as EUR/USD continues to show limited movement. Draghi was more dovish than expected, saying that the ECB was prepared to increase QE in "size or duration", a reminder to the markets that it is premature to expect normalization anytime soon. He added that interest rates would not rise until well after the ECB's asset-purchase program (QE) was over. The QE program will not end until September at the earliest, so Draghi essentially ruled out any rate hikes before early 2019. A new headache for ECB policymakers is the streaking euro, which has hit 3-year highs against the US dollar. EUR/USD has jumped 3.3% in January, as the dollar continues to struggle.

Investors are also concerned about the streaking euro, which could hurt exports and affect company earnings. The euro posted strong gains on Wednesday, after US Treasury Secretary Robert Mnuchin said that the US had no problem with a weak dollar. ECB policymakers were not pleased with Mnuchin's statement, and Mario Draghi, without naming Mnuchin, said that such comments amounted to "targeting the exchange rate". Mnuchin has since backtracked, saying that his words were taken out of context and that the US has a long-term interest in a strong dollar. President Trump added that Mnuchin was misinterpreted, but these attempts at damage control haven't had much effect, as EUR/USD has traded sideways since the Mnuchin comments.

Market Update – European Session: Quiet Start To A Potential Busy Week

Notes/Observations

Action-packed week ahead with Chair Yellen’s last FOMC meeting, President Trump’s State of the Union and heavy data highlighted by US payrolls on Friday

Asia:

Bank of Japan spokesperson noted that Gov Kuroda’s comments at WEF panel were intended to repeat the BoJ's official view that it expects to meet its 2% inflation target around FY19

China National Development and Reform Commission (NDRC) saw 2018 GDP growth between 6.5-6.8%

Europe:

ECB's Knot (Netherlands): central bank has to end its QE program as soon as possible, arguing that there’s not a single reason anymore to continue with it - Chancellor Hammond/Brexit Sec Davis/Business Sec Clark sent open letter to British businesses which reiterated pledge for speedy agreement on Brexit transition phase

Aims to reassure British companies who have called for more clarity on the Govt’s Brexit plans - German IG Metall union: 5th round of regional wage talks ended with no deal; Leadership had decided to call for 24hr strikes (as speculated)

Fitch affirmed France sovereign rating at AA; outlook Stable; Austria sovereign debt at AA+ with stable outlook

Americas:

President Trump will use his State of the Union address to build momentum for legislation on infrastructure and immigration (**Note: scheduled for Tuesday, Jan 30th)

Economic Data:

(DE) Germany Dec Import Price Index M/M: 0.3% v 0.2%e; Y/Y: 1.1% v 1.1%e

(FI) Finland Jan Consumer Confidence: 24.2 v 24.0 prior; Business Confidence: 16 v 17 prior

(ES) Spain Dec Adjusted Retail Sales Y/Y: 1.2% v 2.2%e; Retail Sales (unadj) Y/Y: 1.5% v 3.2% prior

(IT) Italy Dec PPI M/M: 0.0%e v 0.4% prior; Y/Y: 2.2%e v 2.8% prior

(IS) Iceland Jan CPI M/M: -0.1%e v +0.3% prior; Y/Y: 2.4%e v 1.9% prior

(AT) Austria Jan Manufacturing PMI: 61.3 v 64.3 prior (24th month of expansion)

Fixed Income Issuance:

(IT ) Italy Debt Agency (Tesoro)sold €6.5B vs. €6.5B indicated in 6-month Bills; Avg Yield: -0.417% v -0.457% prior; Bid-to-cover: 1.39x v 1.43x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 - 0.2% at 399.8, FTSE flat at 7669, DAX -0.4% at 13287, CAC-40 -0.2% at 5521 , IBEX-35 -0.5 at 10544, FTSE MIB -0.2% at 23820 , SMI -0.2% at 9497, S&P 500 Futures -0.3%]

Market Focal Points/Key Themes: European Indices trade mostly lower this morning, tracking the declines in US futures after record closes on Wallstreet on Friday. News flow has been quiet ahead of a busy earnings week with Siemens, Vodafone, ING and Royal Dutch Shell some of the names reporting. AMS in Switzerland outperforms this morning after a sharp Revenue rise; To the downside Petra Diamond, Santhera and Bankia trade lower following earnings. In the M&A space Sanofi trumped Novo Nordisk by acquiring Ablynx in a €3.9B deal. Elsewhere RELX acquired ThreatMetrix for £580M and Schmolz + Bickenbach received court approval for the acquires of parts of Asco Industrials. Looking ahead notable earners include Seagate, Adient and Dominion Energy.

Movers

Consumer Staples [Conviviality [CVR.UK] -8% (Earnings)]

Financials [ Bankia [BKIA.ES] -3.3% (Earnings) ]

Healthcare [Santhera Pharma [SANN.CH] -3.3% (Earnings), Getinge [GETIB.SE] -6.2% (Earnings), Abylnx [ABLX.BE] +21%, Novo Nordisk [NOVOB.DK] -1.1% (Ablynx to be acquired by Sanofi for €45/shr) ]

Materials [Petra Diamond [PDL.UK] -8% (Prelim results, cuts outlook) ]

Technology [Wirecard [WDI.DE] +1.3% (prelim earnings), AMS [AMS.CH] +17% (Prelim FY17)]

Speakers

ECB's Praet (Belgium, chief economist): Policy will be data-dependent. Domestic price pressures remained subdued; ample degree of monetary accommodation was still needed

ECB said to will accept Spain Fin Min de Guindos to vice chancellor position if there is a consensus

Japan Currency Head Asakawa: To continue to monitor FX market closely; checking what was behind moves; should avoid FX competition; (in-line with G7 rhetoric). Reiterated that would not target FX for competitiveness and that excessive, disorderly moves had bad effects. FX volatility had increased and watching for nervousness or speculative moves

China PBoC Dep Gov Yi Gang: 2018 GDP growth expected to remain on a stable path. Debt and leverage ratios were too high . PBoC to study inclusion of shadow banking into MPA

Iraq State Organization for Marketing of Oil (SOMO) chief: jan exports seen between 3.5-3.55M bpd

Currencies

USD began the week with a small bit of retracement after six straight weeks of losses as FX speculators have been short of dollars. There are a plethora of key events during the week that could account for some of the squaring of USD positions dominated the data agenda, with the Janet Yellen's swan-song FOMC meeting, the ISM data and then the monthly payroll jamboree to come, as well as the State of the Union address. Overall dealers believe that upcoming US economic data won't turn the tide of dollar weakness. Also dealers noted that rise in US bond yields was doing little to support the greenback

EUR/USD in today’s session probed near the lows registered in the aftermath of Trump’s reply to the weak dollar environment last week. The pair tested 1.2385 before inching back above 1.24 in quiet trading. (President Trump noted late last week that the USD would strengthen as the economy did)

USD/JPY was only marginally higher and unable to remain above the 109 level in a quiet session.

Fixed Income

Bund Futures trades down 59 ticks at 159.22 as the German five-year bond yield touches 0%, highest level since 2015. Continued upside targets 162.00, while a move lower targets the158.75 low.

Gilt futures trade at 122.43 down 13 ticks as the 10-year yield hits the highest level since Feb 2017. Support continues to stand at 122.25 then 121.75, with upside resistance at 123.75 then 124.33.

Monday’s liquidity report showed Friday’s excess liquidity rose to €1.874T from €1.872T prior. Use of the marginal lending facility fell to €50M from €0M prior.

Corporate issuance saw 2 issuers raise $2.6B in the primary market.

Looking Ahead

(BR) Brazil Jan CNI Consumer Confidence: No est v 100.5 prior

05:25 (BR) Brazil Central Bank Weekly Economists Survey

06:00 (IE) Ireland Dec Retail Sales Volume M/M: No est v 2.6% prior; Y/Y: No est v 6.8% prior

06:00 (IL) Israel to sell Bonds - 06:45 (US) Daily Libor Fixing

07:00 (RO) Romania to sell 1.35% 2019 Bonds

07:30 (BR) Brazil Dec Total Outstanding Loans (BRL): No est v 3.064T prior; M/M: No est v 0.4% prior; Personal Loan Default Rate: No est v 5.4% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Dec Personal Income: 0.3%e v 0.3% prior; Personal Spending: 0.4%e v 0.6% prior , Real Personal Spending (PCE): 0.4%e v 0.4% prior

08:30 (US) Dec PCE Deflator M/M: 0.1%e v 0.2% prior; Y/Y: 1.7%e v 1.8% prior

08:30 (US) Dec PCE Core M/M: 0.2%e v 0.1% prior; Y/Y: 1.6%e v 1.5% prior

08:55 (FR) France Debt Agency (AFT) to sell combined 4.3-5.5Bin 3-month, 6-month and 12-month BTF Bills

09:00 (BE) Belgium Q4 Preliminary GDP Q/Q: No est v 0.3% prior; Y/Y: No est v 1.7% prior

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tend

10:30 (US) Jan Dallas Fed Manufacturing Activity: 25.4e v 29.7 prior

11:30 (BR) Brazil Dec Central Govt Budget Balance (BRL): -25.0Be v +1.3B prior

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to cut Overnight Lending Rate by 25bps to 4.50%

16:00 (KR) South Korea Feb Business Manufacturing Survey: No est v 82 prior; Non-Manufacturing Survey: No est v 78 prior

16:45 (NZ) New Zealand Dec Trade Balance (NZD): -0.1Be v -1.2B prior

18:30 (JP) Japan Dec Jobless Rate: 2.7%e v 2.7% prior; Job-to-Applicant Ratio: 1.57 v 1.56 prior

18:30 (JP) Japan Dec Overall Household Spending Y/Y: 1.5%e v 1.7% prior

US PCE Inflation Seen Steady In December

Just a day before the Fed starts its two-day monetary policy meeting, the Bureau of Economic analysis will release figures on the core personal consumption expenditure price index (PCE), the Fed’s most preferred inflation measure. However, the results are less likely to drive to a rate hike on Wednesday as markets are already pricing in a 'no-change' rate decision. Still, any upside surprise in the data might generate hawkish feelings about the central bank’s appetite for tighter monetary policy before Jerome Powell replaces Janet Yellen as the new Fed chair in February.

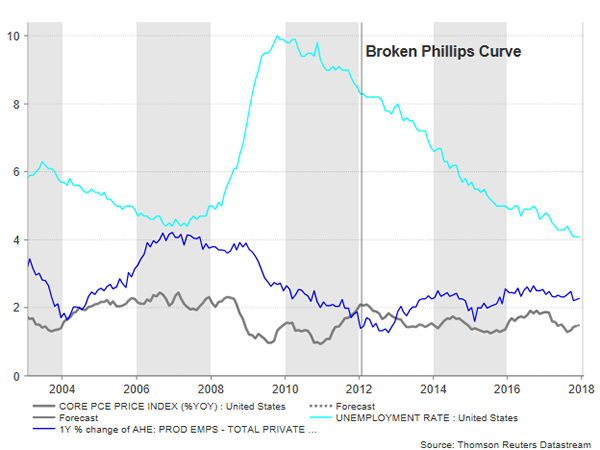

On Monday at 1330 GMT, the US PCE inflation, which excludes food and energy is expected to stand pat at 1.5% y/y in December, finishing 2017 below the Fed’s target of 2.0%, while on a monthly basis the gauge’s change is said to inch up by 0.1 percentage points to 0.2%. Economists are challenged to explain the lack of inflation, as many of them are surprised to see the famous Philips curve, which presents the inverse relationship between inflation and unemployment rate, not holding in times when the central bank was using artificial ways to spread money to the markets. The nationwide unemployment rate hit a 17-year low of 4.1% in December, whereas in several states the jobless rate dropped to historically low levels. On the other side, inflation did not go in the direction predicted but instead eased from 1.8% in the beginning of 2017 to 1.5% y/y in the aforementioned month, with the Fed chair Janet Yellen characterizing the phenomenon a 'mystery'. That also brought doubts whether the gloomy inflation was indeed only transitory. Even so, policymakers remained optimistic that a strengthening labor market will push wage growth higher and eventually drive inflation towards the target probably by the end of this year.

On Friday, the Commerce Department showed that the US economy expanded by 2.6% y/y in initial estimates in the fourth quarter of 2017, failing to meet the 3.0% forecast and falling below the previous print of 3.2% as the trade deficit widened to its biggest since 2008. However, the parts of the report that mattered most for demand came in stronger than expected, pointing that price growth might gain momentum in 2018. Consumer spending turned the strongest in three years, rising by 3.8% y/y, while a measure of core inflation related to consumer spending hit the highest level in a year, jumping by 0.6 percentage points to 1.9% y/y. Hence, today’s readings on personal spending and personal income might also shed light to whether consumption forces have the strength to add speed to the slow-moving inflation and consequently help the Fed to stay on course with its stimulus reduction plans. Still, the market is currently betting that the central bank will hold rates unchanged at the end of its two-day meeting on Wednesday, probably signaling that a rate rise might only come in March.

Turning to forex markets, dollar/yen had its worst start of the year since 2003 last week, breaching the 200-day moving average and making a deep move downwards to the 108 key area. This week, data out of the US will dominate the calendar, with the PCE index being the first to test the greenback’s downside. A disappointing outcome would add further losses to dollar/yen, which could try to find a bottom at 108 psychological level. Any decreases from here would also shift focus to 107.31 critical handle, which if violated would turn the medium-term outlook from neutral to bearish. Alternatively, encouraging results would drive the market back to the 109 key mark, while larger deviations from forecasts would likely retest the area between 110 and 111.

Earnings, Fed And Jobs Data Key This Week

US equity markets are on course to open slightly in the red at the start of what should be another big week for the world’s largest economy.

The S&P 500 and the Dow both made decent gains again on Friday and ended at record closing highs, so the fact that we’re seeing futures pare these isn’t too surprising. Especially when you consider the week the US has ahead of it, which includes almost a quarter of S&P 500 companies reporting earnings, the Federal Reserve monetary policy decision and Friday’s jobs report, to name just a few notable events.

Naturally, the start of the week is looking a little quieter but even then, we’ll get inflation, income and spending figures ahead of the open which will be of interest to traders. The core PCE price index comes a couple of weeks after its CPI alternative ticked higher to 1.8%, but with this being the Fed’s preferred measure of inflation, traders will be playing close attention to it. Inflation has struggled below target for too long as with some policy makers becoming anxious about this, we may need to see evidence of it approaching target soon or interest rate hike expectations will likely be pared.

The income and spending data is also of note to traders as ultimately, improvements in both of these areas should typically feed into the end goal of 2% inflation, not to mention stronger economic growth. With the data covering December, it's too soon for tax reform to have had a positive impact, something we should see over the course of this year. Still, we are expecting to see continued, albeit marginal, progress on both of these even in the absence of reforms.

Wednesday's Fed decision is widely being viewed as a write-off in terms of the odds of a rate hike, with it being Janet Yellen's last meeting as Chair and following December's increase. However, with tax reform having passed towards the end of the year, it may be interesting to see whether it has influenced policy makers views on the economy and inflation, particularly given the challenges with regards to the latter.

Friday's jobs report will ensure traders are kept on their toes this week. As ever, focus will likely be on the earnings component given the challenges the central bank is facing, but we'll also get figures on job creation and unemployment. Again, with tax reform having just passed, we'll likely have to wait a little while before the impact is seen in the jobs data.