Sample Category Title

GBP/USD Recovery Following Minor Decline

GBP/USD is bouncing up. The technicals is positive. Hourly support is given at 1.3742 (16/01/2018 low).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is now moving up to 2016 highs. A long-term support given at 1.1841 (07/10/2017 low) and a strong resistance at 1.5018 (24/06/2016 high) are identified.

EUR/USD Short Squeeze

EUR/USD is regaining strength after a short decline yesterday. The pair has strongly bounced back. Hourly support is given at 1.2165 (17/01/2017 low). The technical structure suggests further short-term upside moves.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2856 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Technical Outlook: GBPUSD Bounces After Pullback, UK GDP Data In Focus

Sterling regained traction on Friday and bounced well above 1.42 after strong upside rejection at 1.4344 on Thursday and subsequent dip to 1.4082 on conflicting comments about dollar’s direction from top US officials.

Fresh strength recovered over 61.8% of 1.4344/1.4082 fall, partially offsetting negative impact from Thursday’s red candle with long upper shadow which marked the first close in red of steep rally from 1.3457 trough.

Overall sentiment remains firmly bullish (the pair is on track for strong bullish weekly close) but overbought daily/weekly studies continue to warn about correction.

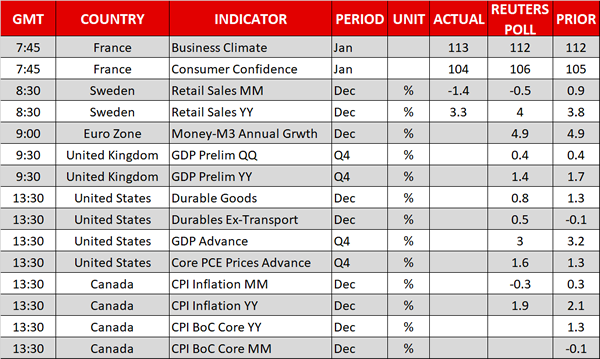

Release of UK Q4 GDP data is seen as key event for pound today. The pace of the UK economy’s growth is expected to stay unchanged at 0.4% in Q4, but annualized figure is forecasted lower for Q4 (1.4% f/c vs 1.7% in Q3).

Better than expected reading could lend fresh support to sterling for further advance and probes through immediate barriers at 1.4288 (cracked Fibo 76.4% of 1.5016/1.1930 post-Brexit vote fall) and 1.4397 (falling weekly 200SMA).

Conversely, GDP miss would have negative impact and risk retest of Thursday’s low at 1.4082 initially, with stronger dip to open lower pivot at 1.4043 (rising daily Tenkan-sen), loss of which will be bearish signal.

Res: 1.4264, 1.4317, 1.4344, 1.4400

Sup: 1.4163, 1.4107, 1.4082, 1.4043

Euro/Dollar Jumps On ECB, But Stumbles After Trump, US & UK Release Flash GDP Figures

Here are the latest developments in global markets:

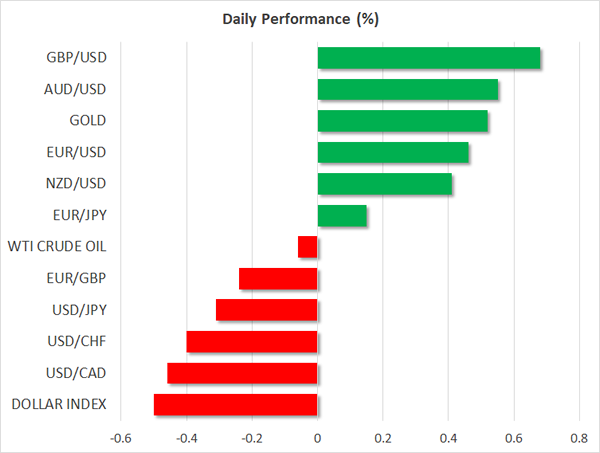

FOREX: The dollar index traded 0.5% lower on Friday, after experiencing heightened volatility earlier on Thursday.

STOCKS: Asian markets were mixed. Japan’s Nikkei 225 and Topix closed 0.2% and 0.3% lower respectively, while in Hong Kong, the Hang Seng was up by an astonishing 1.3%, reaching a fresh all-time high. In Europe, futures tracking the Euro stoxx 50 suggest the index could open 0.3% higher. In the US, the Dow Jones and the S&P 500 continued to march higher, closing at new record highs, though the Nasdaq composite was not as fortunate, ending marginally lower. Futures tracking the Dow, S&P, and Nasdaq 100 are all currently in the green.

COMMODITIES: Oil prices tumbled yesterday, as the greenback regained some poise. Both WTI and Brent crude are lower today as well, albeit only slightly. Despite this pullback, both oil benchmarks are still trading near multi-year highs. In precious metals, gold pulled back yesterday as well, though it recovered most of its losses today, up nearly 0.5%, last trading near the $1355/ounce zone.

Major movers: Euro/dollar trades like a rollercoaster after ECB and Trump’s remarks

Euro/dollar experienced a highly volatile session yesterday. It surged initially on euro strength following the ECB policy decision, only to give back all its gains to trade even lower a few hours later, as the USD gained on some remarks from President Trump. Then, the pair rebounded again early on Friday, as the dollar went back on the defensive.

Kicking off with the ECB, it kept both its policy and its forward guidance unchanged and as such, attention quickly shifted to President Draghi’s press conference. The ECB chief commented on the euro’s appreciation, noting that “recent exchange rate volatility is a source of uncertainty”, but his warning was probably milder than some may have expected. Investors likely anticipated a much more concerned message, and since his tone was only moderate, that may have given them the “green light” to reenter long-euro positions, driving euro/dollar briefly above 1.2500. As for policy signals, Draghi noted repeatedly the progress in Eurozone’s economy, keeping the door open for the Bank to scale back its QE later this year. Interestingly enough, however, he practically eliminated the possibility that the ECB could raise interest rates this year.

Euro/dollar turned down later on Thursday, as the USD surged following remarks from US President Trump that he wants a “strong dollar”. Coming one day after Treasury Secretary Mnuchin said “a weak dollar is good for us”, his comments may have helped to alleviate concerns that the US administration is aiming at a weaker currency. Importantly, President Trump is set to speak again today in Davos, at 1300 GMT. Traders are likely to focus on any further comments on the USD, as well as any hints on protectionism and the latest trade standoff with China.

In Norway, the Norges Bank kept its policy unchanged yesterday as well, providing practically no new policy signals for investors.

Overnight, Japan’s inflation data for December had very little market impact. Even though the headline CPI rate rose, the core rate remained unchanged. This suggests that the progress in the headline print is owed mainly to transitory factors, and enhances the view that the BoJ is unlikely to alter its ultra-loose policy framework anytime soon.

Day ahead: UK & US deliver preliminary GDP growth figures; Canadian inflation pending

The dollar and the pound will be in the spotlight during the European trading hours as the US and the UK are scheduled to deliver preliminary readings on GDP growth, while in Canada, inflation numbers are expected to shake the loonie. In Australia, markets remained closed for the Australia Day holiday.

At 0930 GMT, the UK National Office for Statistics will publish flash GDP growth stats for the final quarter of 2017, with analysts predicting a slower expansion of 1.4% y/y compared to 1.7% seen in the previous quarter. This would be the lowest growth rate seen since 2013. A surprise to the upside would raise the odds for a rate hike but the general opinion is that the BOE would rather keep rates unchanged at its next policy meeting on February 8 as consumer spending remains subdued in times of high inflation and slow-growing wages.

In the US, initial GDP growth estimates due at 1330 GMT are said to come weaker as well. Expectations are for growth to slow down by 0.2 percentage points to 3.0%, but to remain among the highest levels recorded in 2017. Stronger-than-expected results would help the dollar to erase part of its recent dips. Data on the US durable goods orders for the month of December will be also available along with the GDP report.

Elsewhere, CPI inflation will be in focus in Canada at 1330 GMT. Particularly, analysts forecast the headline inflation rate to slip from 2.1% to 1.9% on a yearly basis in December, while in monthly terms they see consumer prices falling by 0.3% for the first time after rising for four consecutive months. Note that the BOC has raised interest rates at its last policy meeting on January 17 and an unexpected increase in inflation could motivate BOC policymakers to apply further monetary tightening.

In oil markets, the US Baker Hughes oil rig count might bring some volatility to oil prices at 1800 GMT.

Regarding public appearances, the BOE chief, Mark Carney and the BOJ chief, Haruhiko Kuroda will participate at a panel discussion at the World Economic Forum in Davos, Switzerland at 1400 GMT. The US President, Donald Trump will also address the event later in the session after his remarks provided a boost to the dollar on Thursday.

In stock markets, Honeywell International Inc. and Gentex Corporation are among companies to report quarterly earnings before the US market open today.

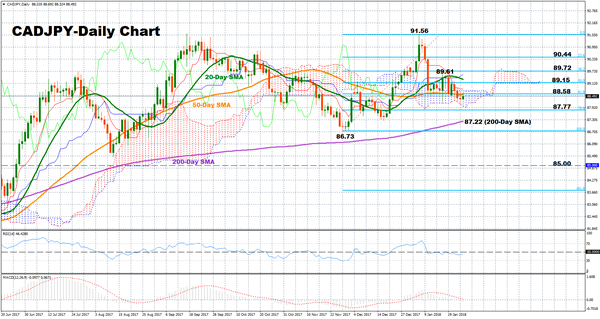

Technical analysis – CADJPY neutral inside Ichimoku cloud

CADJPY stalled its downtrend off a four-month high of 91.56 reached in early January and is currently trading neutral inside the Ichimoku cloud. For the near-term period, the market sends weak bearish signals as the RSI is located slightly below 50, while the MACD has marginally fallen below its trigger line.

Should the pair move lower, support is likely to be found at 87.77, the 78.6% Fibonacci of the upleg from 86.73 to 91.56. The market could also meet the 200-day simple moving average (SMA) at 87.22 before it targets a two-month low at 86.73. Any close below this level would extend September’s downleg towards the 85.00 key level.

On the flip side, if prices rise, immediate resistance could come from the 61.8% Fibonacci at 88.58. However, the pair needs to break above the previous high at 89.61 to turn bullish, while in the best scenario the market could crawl back to the 90.00 key area, shifting focus to 91.56.

Technical Outlook: EURUSD – Near Term Bias Remains Bullish But Firmer Signals Are Needed To Confirm Direction

The Euro stands at the front foot on Friday and looking for retest of 1.25 zone, following bumpy ride on Thursday when it spiked to 1.2537 following ECB Draghi’s speech but reversed quickly on sharp dip to 1.2365.

The Euro moved higher on moderately dovish tone from Draghi but was pulled back on comments from the US President Donald Trump, who supported the policy of stronger dollar, conflicting comments from US Treasury secretary Mnuchin two days ago, who said that weaker dollar is good for America and send the greenback sharply lower across the board.

Fresh rally of Euro on Friday signals that corrective phase might be over as bounce from 1.2365 low retraced over 61.8% of Thursday’s 1.2537/1.2365 pullback and shifted immediate focus higher.

The notion is supported by firmly bullish daily techs with studies on lower timeframes returning to bullish setup after correction.

The pair is on track for strong bullish weekly close, which will mark sixth straight week in green and also for very strong monthly performance, signaling the biggest one month gains since March 2016.

These are strong bullish signals which support further advance for test of next target at 1.2597 (Fibo 61.8% of larger 1.3992/1.0340 fall and possible extension higher.

Weekly close above 1.2500 is seen as minimum requirement for continuation of broader uptrend, with sustained break above 1.2597 barrier to confirm scenario.

On the other side, strong upside rejection on Thursday warns of extended consolidation if the pair fails to regain levels above 1.25, with Thursday’s low at 1.2365, expected to hold.

Conversely, initial bearish signal will be generated on loss of 1.2365 handle, while extension below rising 10SMA (1.2299) would signal reversal.

Res: 1.2493, 1.2537, 1.2567, 1.2597

Sup: 1.2450, 1.2412, 1.2365, 1.2299

NZDUSD Intraday Analysis

NZDUSD (0.7338): The NZDUSD posted a second day of declines on Thursday as the rebound in the U.S. dollar pushed the currency pair lower. Price fell below the 0.7333 level earlier today but quickly managed to rise back. In the short term, NZDUSD could be seen consolidating at these levels but the momentum could be weakening as the support at 0.7160 remains in focus to the downside. For the kiwi dollar to post further gains, price action is expected to rise above the previous highs near 0.7400 in order to continue the rally.

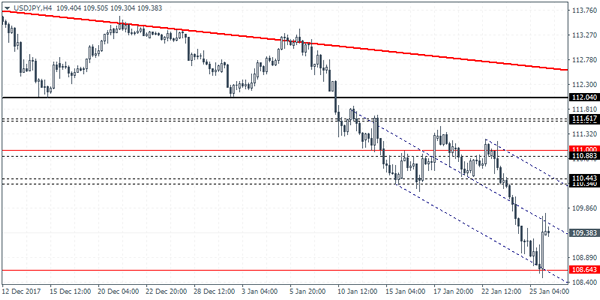

USDJPY Intraday Analysis

USDJPY (109.38): The USDJPY also recovered from the lows of 108.49 and managed to close on a bullish note for the day. Price action however remains doubtful for further gains to the upside. The resistance level at 110.70 could be seen capping the gains in the short term, while to the downside, a retest of the support at 108.26 could be likely. In the near term, we expect USDJPY to maintain a sideways range within these levels. A higher low off the current rebound on the 4-hour chart could indicate a near term rally to 110.44 - 110.34 level.

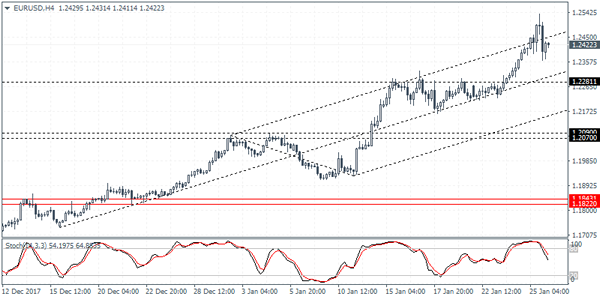

EURUSD Intraday Analysis

EURUSD (1.2422): The EURUSD touched a fresh 4-year high as the intraday rally saw prices reaching for 1.2537. However, the euro gave back the gains rather quickly with the daily session closing with a doji candlestick pattern. Currently, we see some retracement taking place but the gains could be short lived. Initial support is seen at 1.2281 which could be tested if the downside momentum increases. A break down below this level could see the EURUSD extend the declines down to 1.2090 - 1.2070 levels. To the upside, unless price action closes strongly above the 1.2400 handle on the daily basis, we expect the EURUSD to turn flat near the current highs.

USD Whipsaws On Trump’s Comments, Q4 GDP Coming Up

The U.S. dollar was met with another volatile day as late in the day the U.S. President sought to clarify the Treasury Secretary Mnuchin's comments on preferring a weaker dollar. The greenback was seen extending declines earlier in the day as the ECB left the monetary policy unchanged. With Mario Draghi not addressing the exchange rate of the euro, the common currency briefly rallied to a fresh 4-year high only to reverse the gains by the close of business.

The economic calendar was sparse besides the ECB meeting. Canada's core retail sales continued to accelerate, rising 1.6% on the month and beating estimates of a 0.8% increase. Headline retail sales however rose just 0.2% and missed estimates of a 0.7% increase.

Looking ahead, GDP data across the UK, Canada and the U.S. will keep the markets busy. The UK's preliminary GDP is expected to show that the economy advanced 0.4% on the fourth quarter. Canada will be releasing the inflation data which is expected to show a 0.3% decline erasing the increase from the previous month. The U.S. advance GDP report is expected to show a modest increase of 3.0% in the GDP. Later in the day, BoE and the BoJ governors will be speaking at the World Economic Forum in Davos.

Currencies: Dollar Receives Lifeline From President Trump

Sunrise Market Commentary

- Rates: Test of key yield levels in US and Europe continues

Yesterday, US and German 10-year yields again tested key resistances levels as ECB’ Draghi sounded optimistic on (EMU) growth. However, a sustained break didn’t occur as positive comments from President Trump on the dollar eased pressure on US Treasuries. Even so, a break might still occur. Today’s US GDP data and a speech from President Trump in Davos are the next potential triggers. - Currencies: Dollar receives lifeline from President Trump

Yesterday, EUR/USD jumped north of 1.25 during the ECB press conference even as ECB’s Draghi mentione the strong euro as a source of uncertainty. Surprisingly, president Trump finally blocked the rise of EUR/USD as he said to favour a strong US dollar. Are the comments from President Trump a harbinger of some calm to turn to USD trading?

The Sunrise Headlines

- US equities ended the session little changed with the Dow outperforming as investors assessed the potential implications from recent gyrations in the interest rate and FX markets. Asian equity markets are trading mixed with China and Korea outperforming.

- U.S. President Trump said he ultimately wants the dollar to be strong, lifting the greenback and contradicting comments made by Treasury Secretary Steven Mnuchin earlier this week .

- Britain's finance minister Hammond called for a modest Brexit that would keep the UK as closely aligned as possible with the EU after its 2019 exit. However sources in May's office rebuked Hammond, saying the changes that Britain will undergo cannot be described as "very modest".

- Japan's inflation in December continued to lag a strong economic revival. Core inflation rose 0.9% Y/Y, unchanged from November - well off the Bank of Japan's 2 percent price goal.

- Profits for China's industrial firms rose at the slowest pace in a year in December as anti-smog curbs hit activity, but profits clocked the fastest annual rise in six years as cost cutting and a construction boom helped businesses in 2017.

- Ireland's central bank hiked its 2018 growth forecasts, predicting a faster rate of expansion for next year than the government has pencilled in. The CB expects gross domestic product to grow by 4.4 percent this year and by 3.9 percent in 2019.

- The calendar is well filled today. In EMU, the M3 money supply data and the ECB Survey of professional forecasters will be published. The UK will provide a first estimate of Q4 GDP growth. The US calendar contains the Q4 GDP, durable orders, the goods trade balance and inventory data. Markets will also keep a close eye on speeches from Davos, including from US President Trump.

Currencies: Dollar Receives Lifeline From President Trump

Dollar receives lifeline from President Trump

The dollar and the euro had a roller-coaster ride yesterday. EUR/USD spiked again sharply higher during the ECB press conference. ECB’s Draghi mentioned FX volatility as a source of uncertainty. He also said that some recent communication on FX was not in line with what was agreed at the level of the IMF. It didn’t to prevent a resumption of the rise of the euro. EUR/USD jumped above 1.25, supported by a positive economic assessment of the ECB. Euro strength was the dominant trend, but some underlying USD weakness was also at work. Later, the dollar received unexpected support from US president Trump. He wants to see a strong dollar, mirroring the strength of the US economy. EUR/USD tumbled from 1.25+ to below 1.24 and closed the session at 1.2396. USD/JPY finished the day at109.41, after testing 108.50 intraday.

Overnight, Asian equities are trading mixed, mirroring an indecisive close in the US. Some clam also returned to the FX market. EUR/USD hovers in the low 1.24 area. USD/JPY is trading in the mid 109. The yen weakened slightly on soft Japanese inflation data, but rebounded later.

The eco calendar is well filled today, especially in the US, with the first estimate of US Q4 GDP, durable orders and the goods trade balance. The GDP report and the trade balance data are interesting from an FX point of view. Markets will look out whether US growth surpasses 3.0%. The price deflators will also be closely watched (core PCE expected to rise from 1.3% to 1.9%). With the focus on international trade relations, the US trade deficit might get more attention than is usually the case. Evidently, most attention from (FX) markets will go to Davos. President Trump is expected the ‘defend’ its ‘America first’ agenda. Yesterday’s comments suggest that, if needed, he is more inclined to use specific trade measures, rather than aiming for a weaker dollar. Key question for EUR/USD trading is whether yesterday’s spike was some kind of an exhaustion move. Global USD strength might be mitigated after President Trump’s comments. On the other hand, the positive ECB assessment on the economy keeps the debate on a less easy ECB policy on the radar. If EUR/USD today can stay away from the 1.2537/1.2596 area, some consolidation on the euro rally/USD decline might be on the cards. For now, the jury is still out.

Yesterday, EUR/GBP extensively tested the 0.8690 support area, but the test was rejected. Euro strength during the ECB press conference was one factor. However, indications of ongoing discord within the UK government on Brexit maybe also dampened recent hope on a soft Brexit, causing some profit

taking on sterling longs. EUR/GBP closed the session at 0.8764. Today, the focus is on the first estimate of the UK Q4 GDP. A modest 0.4% Q/Q and 1.4% Y/Y is expected. If confirmed, these data suggest that the BoE should be in no hurry to raise rates anytime soon. Yesterday’s price action suggest that 0.8690 is indeed a strong support area. We don’t see a trigger for a break anytime soon.

EUR/USD: Was yesterday’s intraday reversal a sign of an exhaustion move