Sample Category Title

GBP/JPY Daily Outlook

Daily Pivots: (S1) 154.04; (P) 155.06; (R1) 155.70; More...

With 153.66 support intact, further rally is expected in GBP/JPY. Next target is 100% projection of 139.29 to 152.82 from 146.96 at 160.49. However, break of 1.5366 will indicate short term topping and turn bias back to the downside for 150.18 support.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

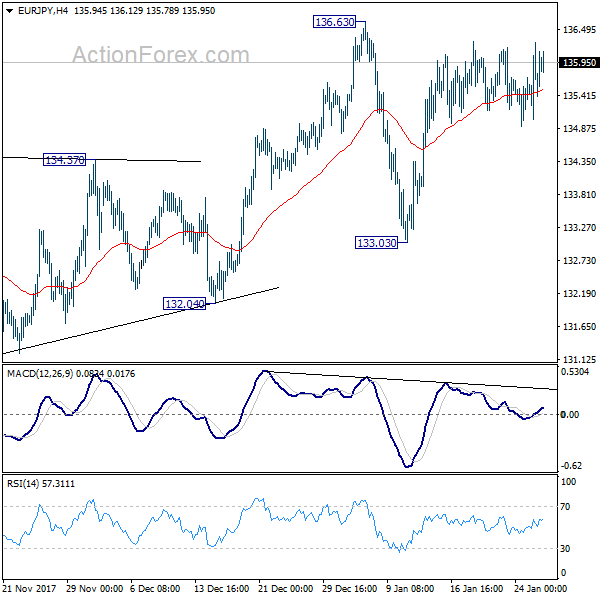

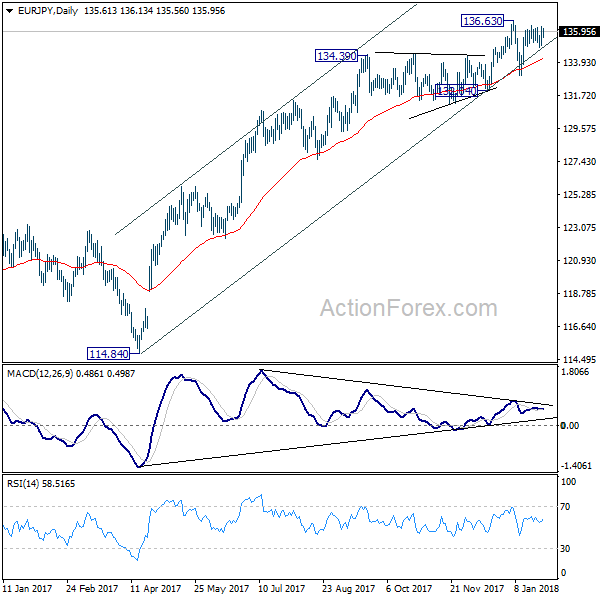

EUR/JPY Daily Outlook

Daily Pivots: (S1) 135.01; (P) 135.64; (R1) 136.26; More....

Intraday bias in EUR/JPY remains neutral and more consolidation would be seen in range of 133.03/136.63. But after all, outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

4Ds: Donald Trump, Davos, Dollar Index, Economic Data | Gold Set For Weekly Gain

Equity and forex relationship matter

Dollar index facing major turbulance

Trump to speak in Davos

Today is not the 3D day but 4D. The letter 'D' matters for traders; Donald Trump, Davos, Dollar and Economic Data. The World Economic Forum in Davos comes to an end, Donald Trump will speak in Davos, Dollar index would be under the spotlight after a massive rollercoaster ride yesterday and the UK's Prelim GDP Data will be released which would impact sterling and the FTSE index.

The relationship which is prominent in the markets is that when a currency picks up some steam, the equity index of that country loses esteem among investors. The strength in the Sterling is matched by the weakness in the FTSE index which touched the lowest level YTD yesterday. The Euro erupted to the upside and this capped the gains for the European stocks.

The dollar index experienced massive turbulence yesterday. Perhaps, the US Treasury Secretary wasn't on the same page as President Donald Trump. One was saying that the lower dollar is good for the economy and other was trying to sway the markets that the dollar is going to become stronger and stronger. The dilemma created by both brought enormous volatility for the dollar index and currencies such as the Euro and Sterling experienced mammoth moves. The dollar index is on track for its worst monthly performance since March 2016.

The Euro by any measure is highly undervalued in our view and the weakness in the dollar index isn't the only reason that we have seen it surpassing the 1.25 mark yesterday. The European Central Bank policy members failed to show united front and investors saw that there aren't many reasons going to stop the ECB from increasing the interest rate next year. We think one interest rate hike is surely on the cards before mid-2019. We think that the Euro would continue to move higher and the next major resistance is sitting at 1.27 against the dollar.

Sterling is in a better position in hopes that Theresa May has survived the most difficult part and the European partners are striking a more favourable tone in relation to develop a new deal.

Mr Trump's speech in Davos is going to be the highlight of the day, he wants to talk about tax, America first and what he thinks a fair deal. However other leaders are less enthusiastic towards his speech. Investors would like to know if the Cold War has already started which triggered by Mr Trump who inflated the import duties and tariffs.There could be some significant headlines on the relationship between the two countries (UK and US) which preferred antiglobalisation. His views on Pacific trade deal could also generate some flashing newswires. Overall, we think the event would create more volatility and it would be across the equity and forex markets.

As for the precious metal, the dollar strength is fading again and the precious metal is set for another weekly gain. The dollar may remain under pressure due to the policies which Mr Trump has adopted and this plague could drag the dollar index lower. Improving fundamental over in Europe and the Chinese Lunar year should keep the gold price rising. It is more than likely that we may see a test of the $1400 mark next week. Gold having its best month since February 2017.

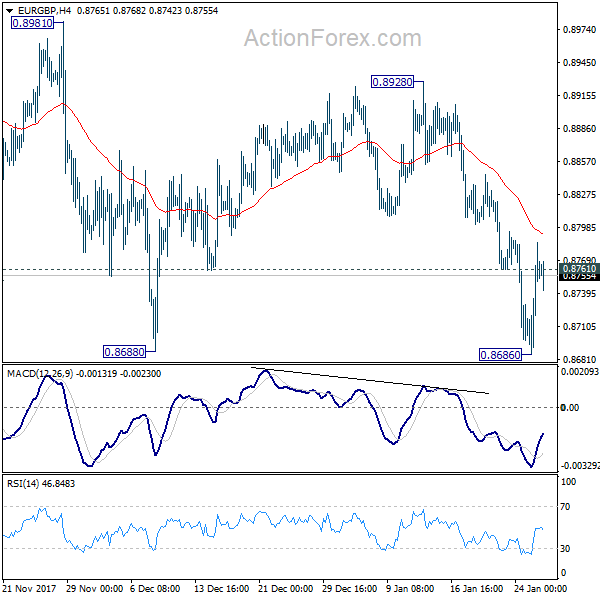

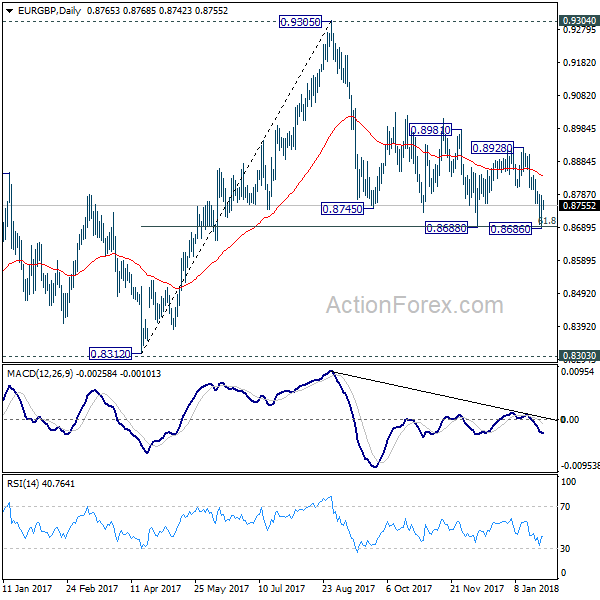

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8706; (P) 0.8745; (R1) 0.8804; More...

EUR/GBP recovered after forming a temporary low at 0.8686, drawing support from 0.8688. Intraday bias is turned neutral first. Stronger recovery could be seen. But outlook will stay bearish as long as 0.8928 resistance holds. Break of 0.8688 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

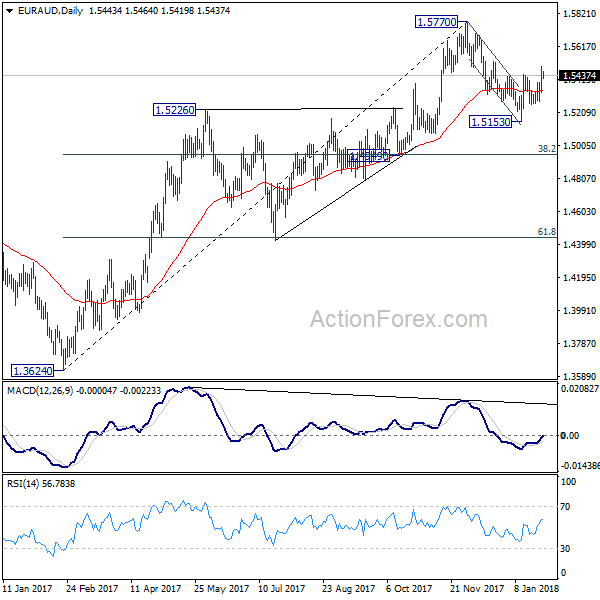

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5356; (P) 1.5425; (R1) 1.5516; More....

Break of 1.5446 resistance revives that case that pull back from 1.5770 is already completed at 1.5153. Intraday bias is turned back to the upside for retesting 1.5770. Break will resume whole medium term rise from 1.3624. This will remain the favored case as long as 1.5259 minor support holds.

In the bigger picture, price actions from 1.5770 so far suggests that it's corrective in nature. That is, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

USDCAD Has More Room To Fall, Struggles Below 61.8% Fibonacci Level

USDCAD has been underperforming over the last sessions, breaking back below the 61.8% Fibonacci retracement level around 1.2385 of the up-leg with the low of 1.2060 and the high of 1.2915. When looking at the bigger picture the pair holds the bearish structure and has been trading lower on the back of US dollar weakness.

Short-term momentum indicators are also pointing to a continuation of the bearish bias. The RSI indicator stands in the negative territory and is pointing south, suggesting further losses. Also, the stochastic oscillator is ready to reach the oversold area and the %K line is attempting a bearish cross with the %D line.

If price remains below the 61.8% Fibonacci mark, it could open the way for the 1.2240 level, which is acting as a major support barrier. A drop below it would reinforce the bearish move in the medium-term and open the way towards the next key level of 1.2060.

On the flip side, in case of a jump above the aforementioned significant Fibonacci level, the pair could hit the 50.0% Fibonacci mark around the 1.2485 level. A break above this level would shift the short-term outlook to a more neutral one as it could take the pair above the 20-day SMA.

Overall, for a resumption of the major medium-term downtrend, USDCAD would need to beat the September 2017 low of 1.2060.

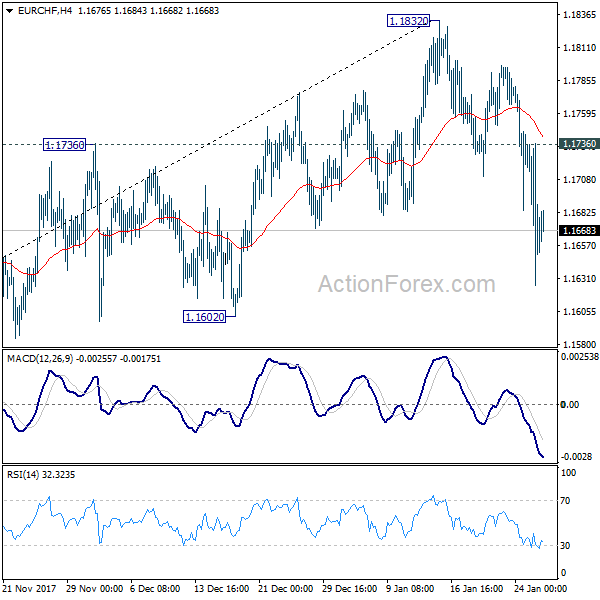

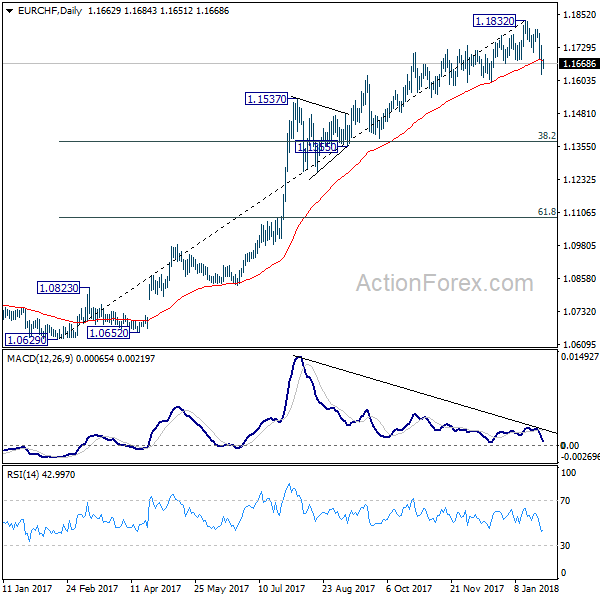

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1614; (P) 1.1675; (R1) 1.1725; More...

EUR/CHF's break of 1.1683 support is taken as an early sign of trend reversal. Intraday bias is back to the downside for 1.1602 support first. Sustained break there should confirm our view and bring deeper correction to 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372. On the upside, above 1.1736 minor resistance will turn focus back to 1.1832 high instead.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect further rise to prior SNB imposed floor at 1.2000 and above. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

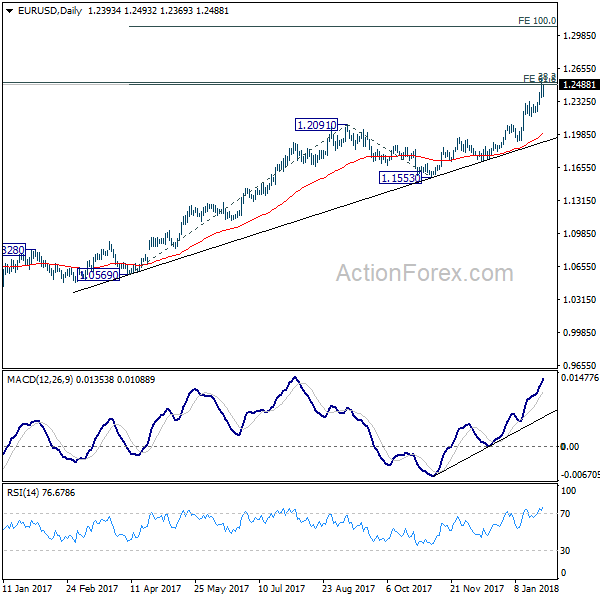

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2327; (P) 1.2432 (R1) 1.2501; More....

EUR/USD reached as high as 1.2537 and breached 1.2494/2516 cluster resistance. Subsequent retreat indicates temporary topping and turns intraday bias neutral first. At this point outlook will remain bullish as long as 1.2222 support holds. Sustained break of 1.2494/2516 will target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.

Forex Analysis: Trump Supports A Strong Dollar

Markets have had a volatile session this week thanks to various US officials and yesterday was no exception, with President Trump speaking in Davos. He made comments about the TPP, saying he would do a deal if it was 'substantially' better. On NAFTA he said he may terminate or may not and that they were still trying to renegotiate it. On Brexit Trump and May want a US-UK trade deal as soon as possible. Perhaps his most important comments were on the US dollar when he said he wanted to see a strong dollar. He said that Treasury Secretary Mnuchin's comments were taken out of context. Mnuchin said that a softer dollar would benefit exports in the short term, but that in the long-term, the dollar would strengthen. 'The dollar is going to get stronger and stronger, and ultimately I want to see a strong dollar,' Trump said. This had an impact on the Dollar with EURUSD falling back from the 1.25000 area to 1.23636 and USDJPY rising from 108.545 to 109.695.

German IFO – Current Assessment (Jan) was 127.7 v an expected 125.4, from 125.4 previously, which was revised up to 125.5. IFO – Business Climate (Jan) was 117.6 v an expected 117.1, from 117.2 previously. IFO – Expectations (Jan) was 108.4 v an expected 109.4, from 109.5 prior, revised to 109.4. EURUSD moved higher from 1.23962 to 1.24331 after the data.

The ECB Interest Rate Decision was as expected, left unchanged at 0%. The ECB Deposit Rate Decision, also released at this time, was left unchanged at -0.4%. During the ECB Press Conference at 13:30 GMT, ECB President Draghi was asked questions on monetary policy, saying that there were additional concerns over unwanted tightening of US FED policy as well as international relations. On the Euro, he said that markets should ask whether FX movement comes from a stronger economy, statements or monetary policy elsewhere. EUR has strengthened also on comments by 'someone else'. On rate hikes, he said that 'based on today's data little chance at all that ECB interest rates will be raised this year'. For the Governing Council, the impact on inflation is always the main concern and the commitment to the inflation target remains firmer than ever. 'We can't yet declare victory'. He also said that there hasn't been much of a change since October and therefore the statement was unchanged. He was firm that monetary policy would remain accommodative well past QE ending, as per ECB statements. The EURUSD rallied from 1.24000 to a high of 1.25372 on the back of Draghi's comments.

Canadian Retail Sales Ex-Autos (MoM) (Nov) was 1.6% v an expected 0.8%, from 0.8% previously. Retail Sales (MoM) (Nov) was 0.2% v an expected 0.7%, from 1.5% previously, which was revised up to 1.6%. USDCAD sold off to 1.22811 after this release.

US New Home Sales (MoM) (Nov) was 0.625M v an expected 0.679M, from 0.733M previously, revised down to 0.689M. New Home Sales Change (MoM) (Nov) was -9.3% v an expected -7.9%, from 17.5% previously, which was revised down to 15.0%.

EURUSD is up 0.45% overnight, trading around 1.24478.

USDJPY is down -0.18% in early session trading at around 109.208.

GBPUSD is up 0.53% to trade around 1.42130.

USDCAD is down -0.28%, trading around 1.23413.

Gold is up 0.44% in early morning trading at around $1,353.90.

WTI is up 0.25% this morning, trading around $65.40.

Major data releases for today:

At 09:30 GMT, UK Gross Domestic Product (QoQ) (Q4) is expected to come in unchanged at 0.4%. Gross Domestic Product (YoY) (Q4) is expected at 1.4% v 1.7% previously. GBP crosses could see a spike in volatility should the actual data differ from the expected consensus.

At 13:30 GMT, Canadian Consumer Price Index (MoM) (Dec) is expected to be -0.3% from 0.3% previously. BOC Consumer Price Index Core (YoY) (Dec) is expected to be 1.5% from 1.3% previously. BOC Consumer Price Index Core (MoM) (Dec) is expected at -0.6% v a prior -0.1%. Consumer Price Index (YoY) (Dec) is expected to be 1.9% from 2.1% previously. CAD crosses could be affected by this release.

At 13:30 GMT, US GDP Annualized (Q4) is expected to be 3.0% from 3.2% previously. GDP Price Index (Q4) is expected to be 2.35% from 2.1% previously. Durable Goods Orders Ex-Transportation is expected to come in at 0.5%, from -0.1% previously. Durable Goods Orders (Dec) is expected at 0.8% v 1.3% previously. USD crosses may be heavily traded as a result of this data.

At 14:00 GMT, Bank of England Governor Carney and Bank of Japan Governor Kuroda will sit on a panel discussion entitled 'Global Economic Outlook' in Davos. The panel will discuss topics on QE and monetary policy paths, addressing low productivity in a high-tech world and managing climate change risk in economic planning.

At 18:00 GMT, Baker Hughes US Rig Count numbers will be released. The prior number last Friday showed that there were 747 Oil rigs in operation. WTI traders will be paying close attention to this number as they look to the week ahead.

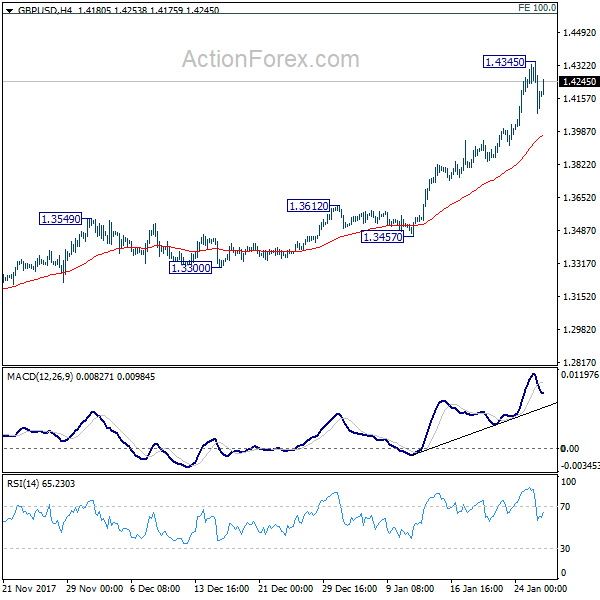

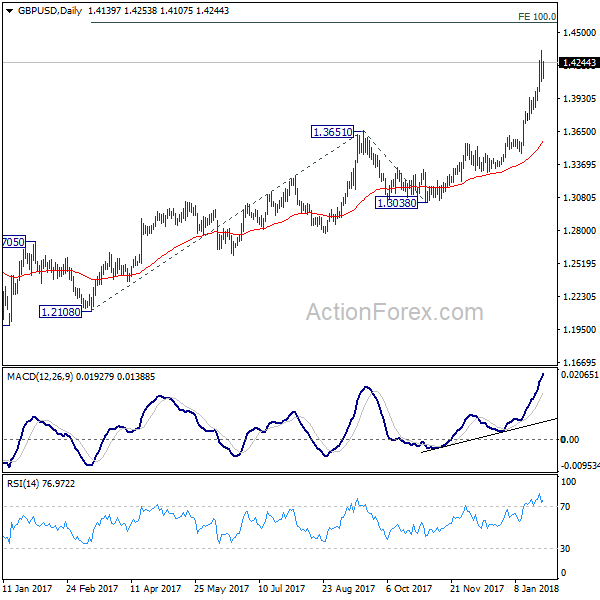

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4031; (P) 1.4188; (R1) 1.4294; More.....

A temporary top is in place at 1.4345 and intraday bias in GBP/USD is turned neutral first. Downside of retreat should be contained above 1.3651 resistance turned support and bring another rise. Above 1.4345 will extend medium term rally to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.