Sample Category Title

Gold Gains As China Mulls Slowing US Bond Purchases

Gold has posted gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1316.80, up 0.30% on the day. On the release front, it was a quiet day. Import Prices slowed to 0.1%, short of the estimate of 0.4%. On Thursday, the US releases PPI reports and unemployment claims.

The US dollar is under pressure on Wednesday, and gold has moved higher. The catalyst for this move was a report on Wednesday that China was considering slowing or halting the purchase of US government bonds. China boasts the largest currency reserves, estimated at $3 trillion. It is also the biggest holder of US government bonds, in the amount of $1.19 trillion. Why would China make this move? One reason is that it may consider US treasuries less attractive compared to other assets. As well, it could be part of China’s strategy to flex some muscle as a possible trade war looms between the US and China, which are the two largest economies in the world. The report has pushed US Treasury yields higher and sent the US dollar downwards.

Gold prices have shown strong gains since mid-December, leaving many investors scratching their heads. A robust US economy and a December rate hike from the Federal Reserve have increased the appetite for risk, and the stock markets have pushed higher since the New Year. This should translate into lower prices for safe-haven gold, but the base metal has jumped on the bandwagon and posted strong gains in early January. On Friday, gold touched a high of $1326, its highest level since mid-September. Will enthusiasm for gold continue? Much will depend on the strength of the US dollar – if the greenback runs into headwinds against the major currencies, gold could resume its rally.

British Pound Edges Lower As Manufacturing Production Slows

The British pound has posted slight losses in the Wednesday session. In North American trade, GBP/USD is trading at 1.3510, down 0.23% on the day. In economic news, British Manufacturing Production slowed to 0.4% in November, down from 0.7% a month earlier. Still, this beat the estimate of 0.3%. Over in the US, Import Prices slowed to 0.1%, short of the estimate of 0.4%. On Thursday, the US releases PPI reports and unemployment claims.

The US dollar is under pressure, after a report on Wednesday that China was considering slowing or halting the purchase of US government bonds. China boasts the largest currency reserves, estimated at $3 trillion. It is also the biggest holder of US government bonds, in the amount of $1.19 trillion. Why would China make this move? One reason is that it may consider US treasuries less attractive compared to other assets. As well, it could be part of China’s strategy to flex some muscle as a possible trade war looms between the US and China, which are the two largest economies in the world. The report has pushed US Treasury yields higher and sent the US dollar downwards.

Brexit negotiations have been slow and difficult, as Europe is not keen on rewarding Britain for departing the European Union. There are serious divisions within the government with regard to the talks. and May has to walk carefully, as she has a razor thin majority in parliament, Prime Minister May can ill afford any mistakes, and if her government runs into trouble, she may be forced to call elections, which could shake up the markets and send the pound downwards. The public is almost evenly split on whether Brexit is a good idea, and there are serious concerns that the British economy will take a hit, even if a deal is worked out before the March, 2019 deadline. The parties do not have a lot of time to hammer out a host of trade issues, and all indications are that the negotiations road will be bumpy and difficult.

EURJPY Extends Downtrend; Risk of More Downside

EURJPY extended its bearish phase by dropping another leg lower into the 133 handle. The downtrend since January 5 from the high of 136.63 has not shown signs of reversing. RSI on the 4-hour chart is well into bearish territory although close to oversold levels. This suggests some easing in downside pressure for now.

Short-term price action still looks soft and there is a high risk of another extension lower towards 133. This is considered to be a strong support level which saw several tests back in 2017.

Meanwhile, any rebound from current levels is expected to find resistance at 134. Only a move above resistance at 135 would indicate the end of the recent downtrend and would give scope for a test of 136, which was previously a strong support level. As such, it may be a challenge to breach but if successful, EURJPY would likely rise towards the 136.63 peak and beyond.

For now, EURJPY is clearly in a bearish phase with low odds for a rebound past 134 in the near term.

Sunset Market Commentary

Global core bonds trade mixed today with US Treasuries underperforming German Bunds. The main move of the day (sell-off US Treasuries) occurred after rumours that China is contemplating to slow or halt US Treasury purchases from its giant FX reserves. That would come at a time when the US Treasury needs to plug a bigger funding hole. The Bloomberg article triggered more selling and curve steepening in an already fragile US bond market. The US 10-yr yield broke above 2.5% (minor) resistance yesterday and is now definitively on its way to key 2.63%/2.64% resistance (2016/2017 highs). Tomorrow and Friday's inflation readings could be a trigger. US yields add 0.4 bps (2-yr) to 4.4 bps (30-yr) on a daily basis. Rising inflation (expectations), a tight labour market, strong growth and global policy normalization were already at play. The German bund whipsawed around opening levels amid an empty eco calendar. The €5bn German Bund auction drew only €4.56bn bids, but that's no recent phenomenon. Changes on the German yield curve are limited to 1 bp. Peripheral yield spreads widen marginally. The Italian debt agency successfully launched a new 20-yr BTP via syndication (€9bn 2.25% Sep2036). The Portuguese Treasury raised €4bn via a syndicated 10-yr PGB launch (Oct 2028).

This morning, it looked that the dollar would follow a similar pattern as it did yesterday. USD/JPY remained in the defensive as the yen held strong after yesterday's reduced BoJ bond purchases. EUR/USD didn't decline further and EUR/USD settled in the 1.1925/50 area. The headlines on the China reserve policy also unsettled USD trading. The dollar was hit quite hard even as interest rate differentials widened in favour of USD. Investors concluded that less Chinese appetite for US assets could also reduce the share of USD in Chinese FX reserves, triggering USD selling. USD/JPY trades near 111.50. EUR/USD hovers around the 1.20 pivot.

Sterling trading was again mainly driven by the broader price moves in the euro and the dollar. EUR/GBP traded with a positive intraday bias. The pair rebounded from the 0.8820 area to 0.8870, supported by the intraday rise of EUR/USD. Some sterling softness was also at work, probably as markets were disappointed by the UK government reshuffle. UK eco data (production, trade balance, GDP estimate) were mixed to OK, but didn't help sterling much. Cable trades in the 1.3535 area and hardly profits from the overall USD decline.

Stock markets got a snag from the bounce in volatility after the Chinese rumours. European indices lose up to 0.5% with Germany underperforming (-0.90%). Openings losses on US bourses amount to 0.3%.

News Headlines:

Officials in Beijing reviewing the nation's foreign-exchange holdings have recommended slowing or halting purchases of US Treasuries, according to people familiar with the matter. Markets reacted nervous (see above).

Scandinavian currencies were in good shape ahead of the Chinese news. The Norwegian krone profited from higher-than-forecast Norwegian inflation readings (1.6% Y/Y headline and 1.4% Y/Y core CPI) with EUR/NOK temporary hitting 9.60. The Swedish krona received a boost after the publication of slightly more hawkish than expected Riksbank Minutes. Governors Ingves suggested that the Swedish central bank could start its normalization process earlier than the ECB. EUR/SEK reached an intraday low around 9.75.

The Polish central bank kept its policy rate unchanged at 1.5% as widely anticipated. Governor Glapinski and the other central bankers will comment on the decision later this afternoon.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.28; (P) 112.72; (R1) 113.09; More...

USD/JPY drops sharply today with a strong break of 112.02 support. The development now suggests that decline from 114.73 is resuming. Intraday bias is back on the downside for 110.83 first. Break will target 61.8% retracement of 107.31 to 114.73 at 110.14. We'd look for bottoming signal again below 110.14. On the upside, above 112.05 minor resistance will turn intraday bias neutral first.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

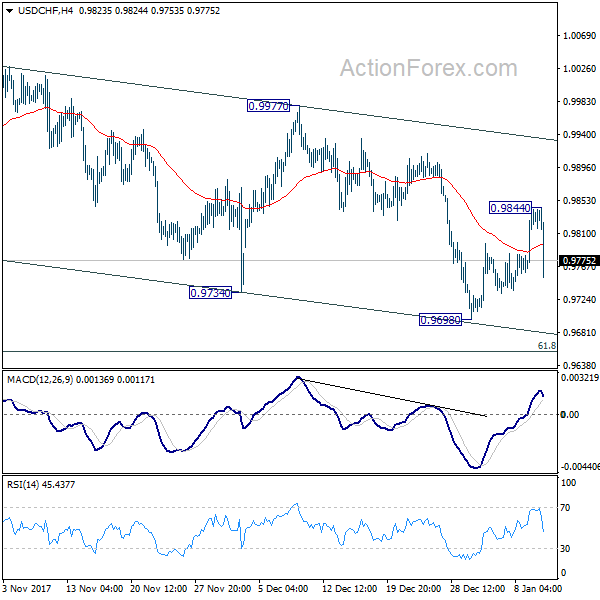

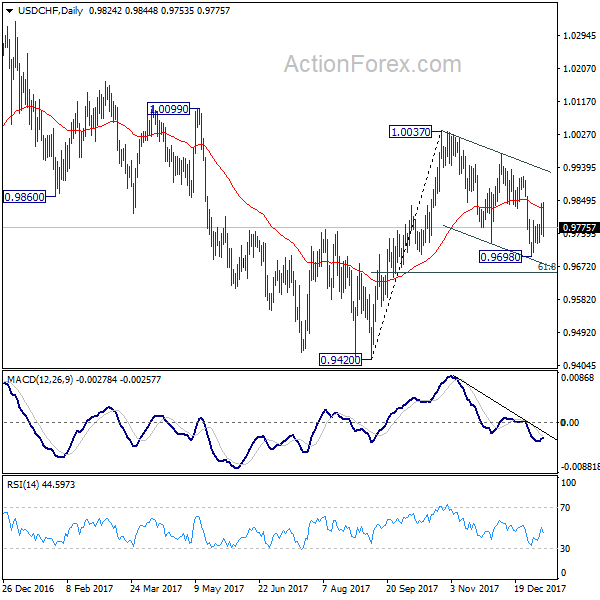

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9780; (P) 0.9811; (R1) 0.9863; More....

USD/CHF's rebound was limited at 0.9844 and drops sharply. Intraday bias is turned neutral first with mixed near term outlook. Nonetheless, we're still slightly favoring that correction from 1.0037 has completed with three waves down to 0.9698. Above 0.9844 will turn bias back to the upside for 0.9977 resistance for confirming this bullish view. However, break of 0.9698 will extend such correction to 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 before completion.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

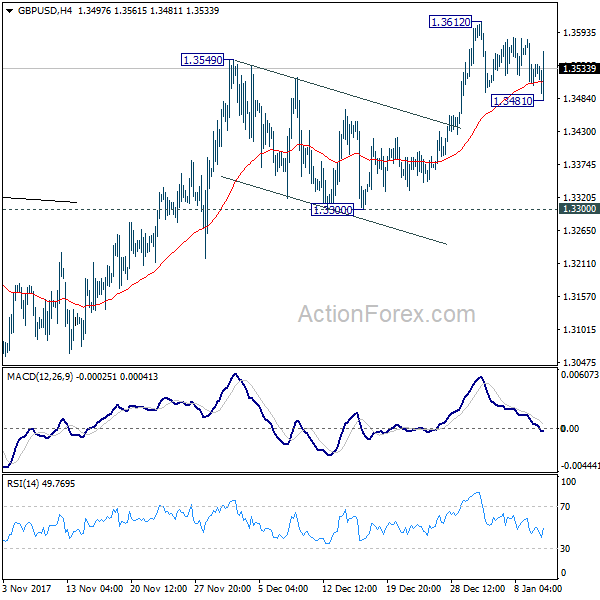

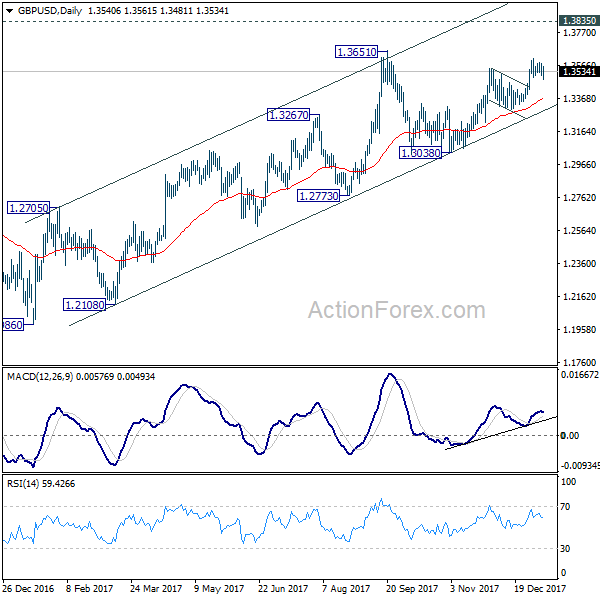

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3502; (P) 1.3541; (R1) 1.3579; More.....

Despite dipping to 1.3481, GBP/USD quickly recovered and is back above 4 hour 55 EMA. Intraday bias remains neutral first. At this point, another rise is still in favor. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, another decline and break of 1.3481 will raise the chance of near term reversal and turn focus back to 1.3300 support.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

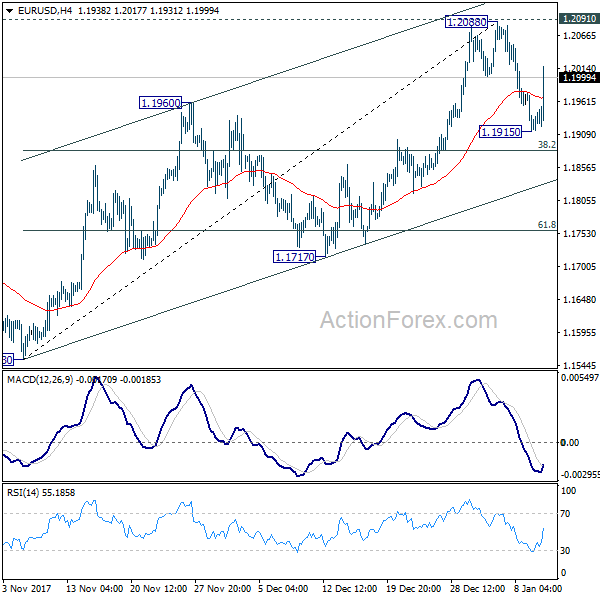

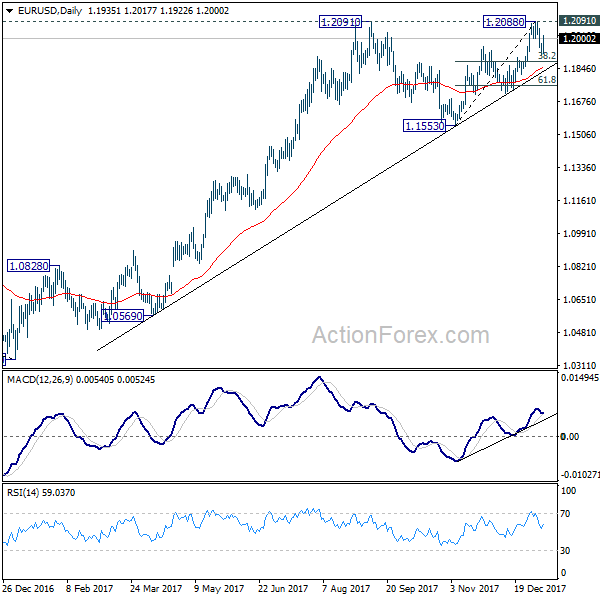

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1908; (P) 1.1942 (R1) 1.1968; More....

EUR/USD rebounds strongly after hitting 1.1915. Intraday bias is turned neutral and near term outlook is turned mixed. But after all, decisive break of 1.2091 key resistance is needed to confirm up trend resumption. Otherwise, more corrective trading should be seen with risk of another fall. Below 1.1915 will turn bias to the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break will target 61.8% retracement at 1.1757 and below.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Dollar Broadly Pressured as China Reported to Halt US Treasury Purchases

Dollar dives broadly today on news that China is considering to diversify its foreign exchange reserves away from Dollar. It's reported by Bloomberg, without unnamed source, that Chinese officials are recommending the government to slow or even halt purchase of US treasuries. The China's State Administration of Foreign Exchange has yet provide a response to press query yet. But it's believed that the lowered attractiveness of US assets, as well as trade tensions between the two countries could be the reasons for the change in strategies.

The report triggered broad based selloff in the greenback, in particular against Yen. USD/JPY's strong break of 112.02 near term support how suggests that recent fall fro m114.73 is resuming and would target 110 handle and below. The development also mixed up the outlook in EUR/USD and USD/CHF. Both pairs appeared to be reversing recent trends but could now be heading back to 1.2088 and 0.9698 respectively. USD/CAD and AUD/USD are relatively steady in range.

Yen remains the strongest major currency for the week. BoJ's cut in JGB purchases has heightened speculations that the central bank is preparing to trim its stimulus measures. However, we do not view this as an abrupt shift from BOJ's monetary stance. Instead, we believe the aim of BOJ is on a steepening of the back end of its yield curve so as to provide support for banks and real money investors. A steeper yield curve would help raise profitability of financial institutions, allowing them to ease lending standards and take risks on their balance sheets. More in BOJ Trimmed JGBs Purchase, Aiming At Yield Curve Steepening Instead Of Policy Normalization

On the data front, US import price rose 0.1% mom in December. Canada building permits dropped -7.7% mom in November. UK industrial production rose 0.4% mom, 2.5% yoy in November. Manufacturing production rose 0.4% mom, 3.5% yoy. Construction output rose 0.4% mom. Visible trade deficit widened to GBP -12.2b. China CPI quickened to 1.8% yoy in December but missed expectation of 1.9% yoy. PPI slowed to 4.9% yoy, above expectation of 4.8% yoy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1908; (P) 1.1942 (R1) 1.1968; More....

EUR/USD rebounds strongly after hitting 1.1915. Intraday bias is turned neutral and near term outlook is turned mixed. But after all, decisive break of 1.2091 key resistance is needed to confirm up trend resumption. Otherwise, more corrective trading should be seen with risk of another fall. Below 1.1915 will turn bias to the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break will target 61.8% retracement at 1.1757 and below.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | CNY | PPI Y/Y Dec | 4.90% | 4.80% | 5.80% | |

| 01:30 | CNY | CPI Y/Y Dec | 1.80% | 1.90% | 1.70% | |

| 09:30 | GBP | Industrial Production M/M Nov | 0.40% | 0.40% | 0.00% | 0.20% |

| 09:30 | GBP | Industrial Production Y/Y Nov | 2.50% | 1.80% | 3.60% | 4.30% |

| 09:30 | GBP | Manufacturing Production M/M Nov | 0.40% | 0.30% | 0.10% | 0.30% |

| 09:30 | GBP | Manufacturing Production Y/Y Nov | 3.50% | 2.80% | 3.90% | 4.70% |

| 09:30 | GBP | Construction Output M/M Nov | 0.40% | 0.70% | -1.70% | -1.10% |

| 09:30 | GBP | Visible Trade Balance (GBP) Nov | -12.2B | -11.0B | -10.8B | |

| 13:00 | GBP | NIESR GDP Estimate Dec | 0.60% | 0.50% | 0.50% | 0.60% |

| 13:30 | CAD | Building Permits M/M Nov | -7.70% | -0.70% | 3.50% | 4.40% |

| 13:30 | USD | Import Price Index M/M Dec | 0.10% | 0.40% | 0.70% | 0.80% |

| 15:00 | USD | Wholesale Inventories M/M Nov F | 0.70% | 0.70% | ||

| 15:30 | USD | Crude Oil Inventories | -7.4M |

Dollar Dives after China Said to Hold Back on US Treasuries; Oil Waits for EIA Report

Here are the latest developments in global markets:

FOREX: The dollar took a knock after Chinese officials recommended to slow down or cut purchases of US Treasuries according to Bloomberg. The dollar stretched its losses toward a two-week low of 111.29 (-1.08%) versus the yen and sank marginally below the 92-key level regarding its index against six major currencies (-0.46%). The euro advanced on the news, flying from $1.1930 to $1.2000 (+0.60%), while the pound erased earlier losses, rebounding to an intra-day high of $1.3558. The antipodean currencies also bounced higher, with the kiwi winning the most among its peers. Kiwi/dollar touched a three-month high at $0.7228 (+0.78%). The Swedish krona rose by 0.70% to 8.07 per dollar supported by Riksbank's meeting minutes which confirmed that a monetary tightening was on the way. Note that in December the Swedish central bank signaled the end of negative interest rates. However, the minutes showed that policymakers were cautious about the timing and the speed of the policy adjustment.

STOCKS: A rise in 10-year US Treasury yields as well as in Germany's 10-year bond yields stressed stocks trading in Europe on Wednesday. The pan-European STOXX 600 was down by 0.44% at 1130 GMT, with all sectors being in the red except financial and energy sectors, while the blue-chip Euro STOXX 50 slipped by 0.32%. The German DAX 30 declined by 0.74%, while the British FTSE 100 and the Spanish IBEX 35 were moving sideways. US stock futures were pointing to a positive opening.

COMMODITIES: After yesterday's strong rally underpinned by declining US oil inventories and ongoing OPEC-led supply cuts, oil prices paused their uptrend near three-year highs during Wednesday's early European trading hours. WTI crude was 0.67% higher at $63.38 per barrel and Brent increased by 0.38% to $69.08. Gold surged to a five-day high of $1,320.76 per ounce on the back of a weaker dollar.

Day ahead: Fed policymakers to deliver further speeches; EIA report pending

Public speeches by a handful of central bankers will dominate economic events later on Wednesday, while data releases will be limited.

At 1330 GMT the US will report on the import price index for the month of December, with analysts seeing the gauge rising by 0.4% m/m below the previous mark of 0.7%. Export prices are also said to come in softer in the aforementioned period, expanding by 0.3% m/m compared to 0.5% seen in the prior month. However, the former will attract a greater attention as higher import costs are likely to have a stronger effect on inflation and therefore have the potential to influence rate hike probabilities.

At the same time, Canada will be publishing readings on building permits. In October, the number of new building permits jumped by 3.5% m/m but for November, forecasts are for the measure to decline by 0.3%.

Next on the calendar, US wholesale inventories due at 1300 GMT are expected to continue rising at October's pace of 0.7% m/m in November.

Regarding public appearances, Chicago Fed President Charles Evans and Dallas Fed President Robert Kaplan will hold discussions at 1400 GMT and 1410 GMT respectively. Kaplan will also give a speech at 1315 GMT.

James Bullard, St. Louis Fed President will give a presentation on the US economy and monetary policy at 1830 GMT.

In the UK, the BOE Deputy Governor Ben Broadbent will answer questions on central bank policy on BBC radio at 1300 GMT.

In energy markets, investors will wait for the EIA report which tracks the weekly change in the US oil inventories to come into view at 1530 GMT.