Sample Category Title

USD/JPY Triple Bottom Pattern Consolidation Breakout

As the BoJ commences a slow process of tapering, this in theory has pushed traders into buying JPY. We already saw it in my previous GBP/JPY analysis. In addition, this has the side-effect of selling risky assets, and we saw Equities pullback from recent highs in alignment with rising JPY demand. Whilst US data has been mixed, with Consumer Credit rising, but lower JOLTS jobs openings, all eyes will be on US CPI and Retail Sales data later on Friday.

The USD/JPY has been consolidating (yellow highlight) within a larger running triangle, and it has formed a triple bottom pattern precisely at M L3 support. The pair broke lower trend line/ W L4, and now it is trying to break W L5. A retest of the POC zone 112.00-35 could reject the price again but a 4h close below the W L5 111.78 could target lower camarilla levels. Targets are 111.38 ( M L4), and if it breaks next target is 110.84 (previous low), followed by 110.30 M L5 camarilla

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

M H4 - Monthly Camarilla Pivot (Very Strong Monthly Resistance)

M L3 – Monthly Camarilla Pivot (Monthly Support)

M L4 – Monthly H4 Camarilla (Monthly Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Market Update – European Session: UK Data Mixed In Session, Nordic Central Banks Viewed More Hawkish

Notes/Observations

UK data mixed in session; Production data beats expectations while trade deficits widened

Riksbank Dec Minutes viewed as more hawkish as Gov Ingves hopes to hike rates before the ECB

Norway CPI data validating Norges view of bringing its 1st potential hike forward

Asia:

China Dec CPI M/M: 0.3% v 0.3%E; Y/Y: 1.8% v 1.9%e; Overall 2017 CPI: 1.6% v 3.0% target

China Dec PPI Y/Y: 4.9% v 4.8%e (lowest reading since Nov 2016)

China PBoC injects CNY120B combined in 7, 14-day reverse repos operation (resumes OMO after skipping last 12)

Europe:

World Bank raised its 2018 global economic growth outlook from 2.9% to 3.1% (1st time since 2008)

Brexit:

Germany is said to show opposition to Brexit trade deal plan proposed by the UK. Chancellor Merkel is strongly opposed to the UK's managed divergence from the EU after Brexit; believes the idea is another ruse for Britain to have its cake and eat it

UK Chancellor of the Exchequer Hammond and Brexit Sec Davis wrote a joint article in the German Press suggesting close cooperation between the EU and UK regulators following Brexit. Both Davis and Hammond are expected to be in Germany on Wed; Jan 10th and want to give German business leaders message that transition period takes priority before final exit from single market, customs union

UK Brexit Ministry: proposes 3-mth window after Brexit to start court cases under general principles of EU law

British Chambers of Commerce (BCC): Survey shows UK services and manufacturing companies less confident about 2018 revenues; set to continue "underwhelming growth trajectory" over near term

Americas:

President Trump: would like to see bipartisan immigration reform; maybe we can do something on DREAMERS

Fed Discount Rate minutes: 9 out of 12 regional Fed banks sought discount rate hike in Dec (3 prior). Reminder: Fed raised rates 25 bps in Dec 2017

Energy:

Weekly API Oil Inventories: Crude: -11.2M v -5M prior

Economic Data:

(DK) Denmark Dec CPI M/M: -0.3% v +0.1%e; Y/Y: 1.0% v 1.4%e

(DK) Denmark Dec CPI EU Harmonized M/M: -0.4% v +0.1%e; Y/Y: 1.1% v 1.4%e

(NO) Norway Dec CPI M/M: 0.0% v -0.1%e; Y/Y: 1.6% v 1.5%e

(NO) Norway CPI Underlying M/M: +0.1% v -0.1%e; Y/Y: 1.4% v 1.2%e

(NO) Norway PPI including Oil M/M: 2.9% v 3.2% prior; Y/Y: 7.3% v 9.7% prior

(FR) France Nov Industrial Production M/M: -0.5% v -0.5%e; Y/Y: 2.5% v 2.6%e

(FR) France Nov Manufacturing Production (beat) M/M: -1.0% v -1.4%e; Y/Y: 3.0% v 2.9%e

(CZ) Czech Dec CPI M/M: 0.1% v 0.1%e; Y/Y: 2.4% v 2.4%e

(CZ) Czech Q3 Final GDP Q/Q: 0.5% v 0.5%e; Y/Y: 5.0% v 5.0%e

(UK) Nov Industrial Production (beat) M/M: 0.4% v 0.4%e; Y/Y: 2.5% v 1.8%e

(UK) Nov Manufacturing Production (beat) M/M: 0.4% v 0.3%e; Y/Y: 3.5% v 2.8%e

(UK) Nov Visible Trade Balance (miss): -£12.2B v -£11.0Be, Overall Trade Balance: -£2.8B v -£1.5Be, Trade Balance Non EU: -£4.7B v -£2.6Be

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month, 6-month and 12-month bills

(EU) EFSF opened its book to sell EUR-denominate 7-year bonds; guidance seen -16bps to mid-swaps; order book over €10B

(PT) Portugal Debt Agency (IGCP) opened its book to sell 10-year OT bonds; guidance seen +117bps to mid-swaps; order book over €13B

(IL) Israel to sell USD-denominated 10-year and 30-year notes

(DK) Denmark sold total DKK2.72B in 2020 and 2027 Bonds

(SE) Sweden sold SEK5B vs. SEK5B indicated in 3-month bills; Avg Yield: -0.7251% v -0.8586% prior; Bid-to-cover: 2.45x v 2.13x prior

(NO) Norway sold NOK3.0B vs. NOK3.0B indicated in 2% May 2023 bonds; Avg Yield: 1.19% v 1.10% prior; Bid-to-cover: 1.88x v 2.41x prior

(IT) Italy Debt Agency (Tesoro) sold €7.5B vs. €7.5B indicated in 12-month Bills; Avg yield: -0.420% v -0.407% prior; Bid-to-cover: 1.41x v 2.1x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at 399.6, FTSE +0.3% at 7752, DAX -0.5% at 13320, CAC-40 -0.1% at 5520, IBEX-35 +0.4% at 10468, FTSE MIB +0.4% at 23095, SMI -0.3% at 9587 , S&P 500 Futures -0.2%]

Market Focal Points/Key Themes: European markets opened slightly lower but later performance was mixed; oil prices continued to support energy stocks; Derichebourg priced at €8.10/shr; Com Hem and Tele2 agree to merge; attention turning to upcoming inflation data from the US; corporate events expected later in the US session include earnings from Lennar, Supervalu and KB Home.

Equities

Consumer discretionary [Brunello Cucinelli BC.IT -3.5% (placement), Continental CON.DE -1.9%(Prelim results), Inter Parfumes ITP.FR +4.0% (outlook), Sainsbury SBRY.UK +1.5% (trading update), Takeaway.com TKWY.NL -3.9% (trading update), Ted Baker TED.UK +8.2% (trading update)]

Energy [Tullow Oil TLW.UK +2.1% (outlook)]

Financials [Plus500 PLUS.UK +4.2% (FCA review)] - Industrials [Gima TT GIMA.IT +4.6% (analyst action), Interserve IRV.UK +22.6% (trading update), Taylor Wimpey TW.UK -3.6% (outlook)]

Technology [CapGemini CAP.FR +1.7% (analyst action)]

Telecom [Altice ATC.NL-4.6% (analyst action), Claranova CLA.FR +13.2% (partnership with Sprint), Com Hem COMH.SE +7.1% (merger), Tele2 TEL2A.SE -4.1% (merger)]

Utilities [Suez SEV.FR -2.0% (analyst action), Veolia VIE.FR -3.8% (analyst action)]

Speakers

Sweden Central Bank (Riksbank) Dec Minutes: Policy needed to continue to be expansionary

Riksbank Gov Ingves stated in the minutes that was coming bit closer to point where monetary policy was expected to change direction but not yet there. Possible to raise interest rates before ECB. Important to note that even if current QE bond buying program was concluded; did not rule out potential needs for future purchases to safeguard inflation target

Riksbank Dep Gov Floden: Appropriate to hold Repo rate until middle of next year; subdued price pressures not problematic. Did not support proposal to reivest bonds from QE program

Riksbank Dep Gov Skingsley: Strong economy increases scope to diverge from ECB; must proceed cautiously to avoid FX volatility

Riksbank Dep Gov Jochnick: Housing market is now a more obvious risk factor

Riksbank Member Jansson: Keeping rate path unchanged was difficult to digest but normalization of policy must not start too early. Inflation expectations going forward was crucial for central bank scope of keeping inflation close the 2% target

ECB again lowered emergency liquidity assistance (ELA) cap for Greece banks from €24.8B to €22.0B

Ireland Agricultural Min Creed: Sensible Brexit more likely following the Dec agreement

South Africa President Zuma said to seek an easing of calls for his resignation or impeachment

Catalan Separatists said to have agree to vote Puigdemont as the regional President later in January

Thailand Fin Min Apisak: Government plans THB100B mid-year budget; plans THB450B FY19 budget deficit

Russia Energy Min Novak: Russian Dec. oil production was 301K bpd lower compared to Oct. 2016 level (in-line with agreed upon OPEC arrangement)

Currencies

USD/JPY dipped further in the aftermath when BoJ trimmed the size of a bond-buying operation that sent JGB yields higher on Tuesday viewed as stealth tapering by some. Some technical damage was done when the pair moved below the 112 level. Discounting for Fed rate hike in March will be UST/JPY recovery gauge by most analysts (Fed seen provided 6-7 hikes over the coming two years).

Mixed UK data forced the GBP currency lower in the session. GBP/USD tested below 1.35 as wider trade deficit in Nov offset better Industrial Production data.

EUR/NOK fell to 2-month lows after higher-than-expected Norwegian CPI data for Dec. Pair tested 9.60 before stabilizing.

EUR/SEK cross was lower by 0.3% as the Dec Riksbank minutes were deemed a bit more hawkish than expected. USD/ZAR was higher by over 1% on reports that South Africa President Zuma was seeking to eae of calls for his resignation or impeachment

Fixed Income

Bund Futures trade down 3 ticks at 161.26 closing the gap after reaching 160.92 low on slight weakness in European Indices. Continued upside targets 161.55 then 162.00, while a move below 160.92 low targets 160.71 then 160.45.

Gilt futures trade at 124.26 down 1 tick trading off a session low of 124.07, with slightly better UK Industrial and Manufacturing data keeping futures lower. Initial support lies at 124.07 then 123.83, with upside resistance at 124.73 then 124.96.

Wednesday's liquidity report showed Tuesday's excess liquidity stood at €1.860T. Use of the marginal lending facility fell to €2M from €40M prior.

Corporate Issuance saw Engie, Caxia Bank and CBA announce Euro denominated issuance this morning, while Israel announced the launch of a $2B bond issuance, and Oman also announced the launch of a 3 tranche dollar denominated issuance.

Looking Ahead

(MX) Mexico Dec Nominal Wages: No est v 5.1% prior

(RU) Russia Dec Sovereign Wealth Funds: Reserve Fund: $B v $17.1B prior; Wellbeing Fund: $B v $66.9B prior

(ZA) South Africa Ruling ANC Party meets (**Note: could oust Zuma)

(ZA) South Africa Parliament to meet on Jan 10-11th on impeachment rules

05:30 (DE) Germany to sell €5.0B in new Feb 2028 Bunds

06:00 (IE) Ireland Nov Industrial Production M/M: No est v 10.5% prior; Y/Y: No est v 13.0% prior

06:00 (IL) Israel Dec Consumer Confidence: No est v 125 prior

06:00 (BR) Brazil Dec IBGE Inflation IPCA M/M: 0.3%e v 0.3% prior; Y/Y: 2.8%e v 2.8% prior

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:30 (CL) Chile Central Bank Economists Survey

06:30 (CL) Chile Central Bank Traders Survey

06:45 (US) Daily Libor Fixing 07:00 (RU) Russia to sell combined RUB40B in 2021 and 2028 OFZ bonds

07:00 (US) MBA Mortgage Applications w/e Jan 5th: No est v +0.7% prior

07:00 (CZ) Czech Central Bank to comment on CPI data

07:30 (EU) ECB account of the monetary policy meeting (Dec Minutes)

08:00 (UK) Dec NIESR GDP Estimate: 0.5%e v 0.5% prior

08:00 (HU) Hungary Central Bank (NBH) Dec Minutes

08:00 (RU) Russia Dec Final CPI M/M: No est v 0.4% prelim; Y/Y: No est v 2.5% prelim; CPI YTD: No est v 2.5% prelim

08:00 (RU) Russia Dec Core CPI M/M: 0.4%e v 0.2% prior; Y/Y: 2.4%e v 2.3% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Dec Import Price Index M/M: 0.4%e v 0.7% prior; Y/Y: 3.1%e v 3.1% prior

08:30 (US) Dec Export Price Index M/M: 0.3%e v 0.5% prior; Y/Y: No est v 3.1% prior

08:30 (CA) Canada Nov Building Permits M/M: No est v 3.5% prior

09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

09:00 (MX) Mexico Nov Leading Indicators M/M: No est v -0.02 prior

09:00 (US) Fed's Evans (non-voter, dove) on economy and policy

09:10 (US) Fed's Kaplan (non-voter, dove) in Dallas

10:00 (PL) Poland Central Bank Gov Glapinski to hold post rate decision press conference

10:00 (US) Nov Final Wholesale Inventories M/M: 0.7%e v 0.7% prelim, Wholesale Trade Sales M/M: No est v 0.7% prior

10:30 (US) Weekly DOE Crude Oil Inventories

11:00 (NZ) New Zealand Dec QV House Prices Y/Y: No est v 6.4% prior

13:00 (US) Treasury to sell 10-Year Notes Reopening

13:30 (US) Fed's Bullard (non-voter, dove) on economic outlook

US Inflation On The Rise, EUR Lower Ahead Of The ECB Monetary Policy Meeting

The wait for US inflation continues

The start 2018 should bring reassuring news for traditional economists as the strong US economy, with minimal slack will start producing steady inflation. Markets expect a strong rebound of US December core CPI of 0.3% m/m following a weak reading of 0.12% in the previous month. Strong monthly read will push up annual read to 1.8% from 1.7% in November. Higher food price should offset decline in energy prices in December (but likely reverse due to adverse weather conditions in Jan). Sharp fall in retail gasoline prices are likely offset by rise in expenditures to heat homes like natural gas, heating oil and electricity prices. We expect December headlines CPI to increased .18% m/m and 2.1% y/y. The overall effect should be supportive of the Fed hawk views that three 25bp hikes are appropriate for 2018.

A marginal USD rally should be anticipated as the Fed fund pricing increase probability in March, June and September, Yet taking a broader view we suspect that trend of inflation will underwhelm the majority of FOMC member likely resulting in the removal of the June rate hike. Disappointing wage growth reported in recent payroll report suggests that wage growth remains subdued despite tighter labor market. On a side note retail jobs create fell suggesting that reports of new online economy replacing old brick in mortar (which is in rapid decline) might be over estimated. Remaining slack in low skill market is another reason why PCE is unlikely to accelerate. Our longer-term view for USD remains bearish against higher yielding EM currencies.

EUR/USD heading higher in 2018?

Looking back at yesterday’s currency exchange moves, we might be asking ourselves whether the EUR/USD pair may be turning differently to what analysts might be considering for the coming period. As such, we’ve been witnessing the slow decrease from January 4th (EUR/USD at 1.2067) up to January 8th, where we’ve reached below 1.20 to end up at 1.1924 yesterday. Similarly, the EUR weakened against the JPY (-0.82%) but remained stable compared to other peers.

Multiple reasons could explain the phenomenon: 1) investors were waiting for German negotiation for a potential coalition between the Union party (CSU/CDU) and the Social Democratic Party (SPD) that appears to have found a compromise as early as yesterday during an agreement with regard to an immigration law that relies on attracting new skilled labor force; 2) Investors might be thinking that the EUR is becoming too strong, impeding EU exportation competitiveness, thus reducing growth perspectives; 3) Investors are looking for the ECB Monetary Policy Meeting taking place on Thursday (which we are confident will not tighten, though economic conditions increasingly improve, as demonstrated by the yesterday’s November EU jobless claim report that falls to its lowest rate in almost nine years, at 8.70%).

Due to strong expected IP growth for November data in Europe (France and UK), we are looking forward to see how the FX market will react. However, over the mid-term period, we remain confident that the market should expect a EUR/USD pair turning around 1.18 for 1Q 18 that slowly reaches the 1.20 in 2Q 18. Keeping in mind the fact that the EUR/USD PPP amounts to 1.33 according to the OECD, we still maintain our opinion that the EUR remains somewhat undervalued within the longer-term.

CRUDE OIL Bullish Breakout

Crude oil is has broken resistance given at 62.21 (04/01/2018 high). Strong support is given at 55.82 (07/12/2017 low). Expected to keep increasing.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high)

SILVER Bearish Retracement

Silver has been bouncing on hourly support at 16.99 (04/01/2018 low). Hourly resistance is given at 17.46 (16/10/2017 high). Expected to show continued bearish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

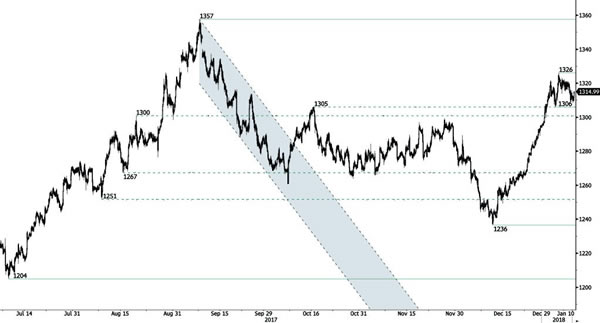

GOLD Pausing Before Another Leg Higher

Gold is pushing higher after the strong collapse even though traders are taking some profit. Hourly support is given at 1236 (12/12/2017 low). Resistance is located at 1326 (04/01/2018).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Ready For A Bearish Breakout

Bitcoin is suffering these past few days. The technical structure has shown a tremendous positive short-term momentum so far. Hourly support area located around 10775 (22/12/2017 low). In the short-term, the technical structure suggests a continued bearish momentum. Expected to show further decline.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.

EUR/CHF Slow Increase

EUR/CHF is trading slightly higher. Hourly resistance is given at 1.1778 (25/12/2017 high). Expected to show continued short-term increase.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Skewed To The Downside

EUR/GBP is trading mixed. The pair is trading between support at 0.8689 (08/12/2017 low) and resistance is located at 0.9046 (14/09/2017 high). Expected to show further sideways trading.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Targeting Resistance At 0.7897

AUD/USD's upside pressures are growing. Hourly resistance given at a distance at 0.7897 (13/10/2017 high). Support stands at 0.7638 (15/12/2017 low). The road is wide open for further upside.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.