Sample Category Title

UK Manufacturing Data Headlines Wednesday Trading

The economic calendar is back in full swing on Wednesday, with the UK set to headline the release schedule with reports on manufacturing.

Action begins at 07:45 GMT with a report on French industrial production. Output in the French economy is projected to fall 0.5% in November, after rising 1.9% the previous month.

The UK Office for National Statistics will release its monthly manufacturing report at 09:40 GMT. The report is expected to show month-on-month growth of 0.3% in November, which translates into a year-over-year gain of 2.8%.

Industrial production – a broader measure of factory output – is expected to rise 0.3% from October and 1.8% annually.

The ONS will also report the November trade balance on Wednesday. Britain's goods trade deficit with the rest of the world is forecast to drop slightly to £10.7 billion from £10.781 billion. The trade deficit with non-European Union countries is expected to rise to £2.6 billion from £2.382 billion.

In a separate report on Wednesday, the National Institute of Economic and Social Research (NIESR) will provide a forecast of GDP for the three months ended December.

In the United States, a report on export and import prices will make headlines at 13:30 GMT. Later in the session, the Department of Commerce will report on wholesale inventories for the month of November.

Oil traders will also be monitoring the weekly crude inventory report courtesy of the US Energy Information Administration (EIA). The EIA is expected to show a weekly drawdown of 4.1 million barrels in the week ended 5 January, following a drawdown of 7.41 million barrels the week before.

In monetary policy, Federal Reserve Bank of Chicago President Charles Evans will deliver a speech at 14:00 GMT. The Fed will hold its next monetary policy meeting later this month. It will be the last meeting chaired by Janet Yellen.

EUR/USD

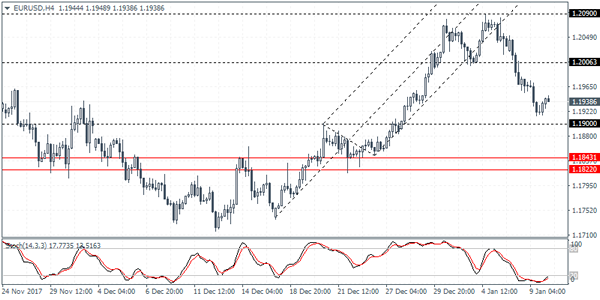

Europe's common currency consolidated on Tuesday following a sharp drop at the start of the week. The EUR/USD exchange rate was last seen trading at 1.1943 for a gain of 0.1%. The pair faces immediate support at 1.1890. On the opposite side of the spectrum, immediate resistance is located at 1.2000.

GBP/USD

Pound sterling was trading within a narrow range on Wednesday, as investors awaited fresh trading catalysts in the form of economic data. The GBP/USD exchange rate was last seen trading at 1.3534, where it was little changed. Cable is well supported at 1.3495, the low from the previous week. Resistance is likely found up ahead near 1.3600.

USD/JPY

The Japanese yen declined on Wednesday, as the dollar regained its composure following a series of heavy losses early in the week. The USD/JPY exchange rate fell 0.3% to 112.30. It now faces a support level of 112.10. On the opposite side of the ledger, resistance is likely found at 113.40.

Forex Analysis: Japanese Yen Continues To Extend Gains

After yesterday's surprise move by the Bank of Japan to reduce bond purchases, the Yen has continued its move against other currencies. GBPJPY, for example, is down -0.65%, trading at 151.556, adding to yesterday's move. Stops are being triggered in an unwind of the recent trend. Even the Japanese stock market is under pressure, with the Japan 225 down -0.36%, trading around 23777.00 for a second consecutive down day.

Chinese Consumer Price Index (YoY) (Dec) came in at 1.8% v 1.9% expected with a prior of 1.7%. Producer Price Index (YoY) (Dec) was 4.9% v 4.8% expected with the previous number of 5.8%. Consumer Price Index (MoM) (Dec) came in at 0.3% v 0.4% expected from a previous of 0.0%.

German Trade Balance s.a. (Nov) came out at 22.3B v an expected 20.9B, from a previous 19.9B. Exports (MoM) (Nov) were 4.1% v an expected 1.2%, from -0.4% previously that was revised up to -0.3%. Imports (MoM) (Nov) were 2.3% v 0.8% expected, from 1.8% prior. Current Account n.s.a. (Nov) was 25.4B v 25.5B consensus, from a previous of 18.1B. EURUSD moved higher after the data to test 1.19707 but sellers took price lower subsequently.

Swiss Real Retail Sales (YoY) (Nov) came in at -0.2% compared to a consensus of -2.5% and the previous number was -3.0%, but this was revised up to -2.6%. USDCHF moved higher when the data was published to test resistance at 0.88335.

Eurozone Unemployment Rate (Nov) was as expected at 8.7% v a prior of 8.8%. EURGBP sold off from 0.88254 to 0.88084 following the data release.

Canadian Housing Starts s.a (YoY) (Dec) was in at 217K v an expected 212.5K, from a prior of 252.2K which was revised to 251.7K. USDCAD sold off from 1.24438 to 1.24243 in reaction to this.

EURUSD is down -0.09% overnight, trading around 1.19253.

USDJPY is down -0.43% in the early session trading at around 112.157.

EURJPY is down -0.51% this morning, trading around 133.754.

GBPUSD is down -0.20% to trade around 1.35138.

USDCAD is up 0.08%, trading around 1.24731.

Gold is down -0.23% in early morning trading at around $1,309.37.

WTI is down -0.09%, trading around $63.35.

Major data releases for today:

At 09:30 GMT, UK Industrial Production (MoM) (Nov) will be released with an expected reading of 0.3% from a prior of 0.0%. Industrial Production (YoY) (Nov) consensus reading is 1.8%, with a prior of 3.6%. Manufacturing Production (MoM) (Nov) is expected to be 0.3%, with a previous reading of 0.1%. Manufacturing Production (YoY) (Nov) is expected at 2.8% from a prior of 3.9%. Traders of GBP pairs will be watching these data points closely.

Tentative – German 10-year Bond Auction. The previous auction's Interest Rate was 0.3%. EUR pairs may react to this data.

At 13:00 GMT, UK NIESR GDP Estimate (3M) (Dec) data will be released. The previous data came in at 0.5%. This data attempts to predict the Government's released data.

Tentative – US 10-Year Note Auction. The previous auction's interest rate was 2.384%. USD crosses could react to this data.

At 18:30 GMT, US FOMC Member Bullard will be speaking. This may affect USD crosses, stocks, commodities and bonds.

NZDUSD Intraday Analysis

NZDUSD (0.7170):The New Zealand dollar was seen holding on to the gains with price briefly testing the support established at 0.7160. Price action has remained flat above this level and comes at a risk of a downside correction to 0.7062. However, the Stochastics oscillator is currently pointing to the bullish momentum being resumed. This could see NZDUSD sustained above the 0.7160 handle. Assuming the sharp rising wedge pattern is validated, we could expect to see some downside correction taking place

USDJPY Intraday Analysis

USDJPY (112.31):The USDJPY also extended losses yesterday with price action falling close to the 112.04 level of support. Currently, we notice a rebound in prices but, the bearish momentum is likely to see price eventually retest the familiar support level. Price action in USDJPY remains flat at the moment unless we see a breakdown of the support level. In this case, USDJPY could be seen testing the lower support near 111.50 area. To the upside, a rebound off the 112.04 support could keep prices continuing to trade sideways.

EURUSD Intraday Analysis

EURUSD (1.1938):The EURUSD extended declines for the third consecutive day. Price action posted a reversal after falling to a two week low. However, we expect the declines to continue towards the 1.1900 handle as mentioned previously. To the upside, the gains are limited to the 1.2000 handle where resistance could be formed following a brief spell of this level serving as support.

Yen Strengthens On Rumors Of BoJ Tightening

The U.S. dollar was seen extending it's gains from the previous day. The lack of economic data on the day saw the markets focusing on rumors that the Bank of Japan could be reducing its bond purchases. The Japanese yen strengthened significantly across the board, rising 0.34% on the day. The U.S. dollar was the second best performing currency pair on Tuesday.

Data from the Eurozone showed that the unemployment rate fell to 8.7% as forecast. The unemployment rate was better than the previous month's 8.8%. However, the common currency continued to extend losses.

Looking ahead, data from the UK stands out with the manufacturing, industrial and construction output data. Overall, output from all the three sectors is expected to show a modest improvement from the previous month. In the U.S. the import price data is expected to show a 0.4% increase, which is slower than the previous month.

Currencies: USD/JPY, EUR/JPY And EUR/USD Drifting South

Sunrise Market Commentary

- Rates: US 10-yr yield breaks above 2.5%, heading to 2016/2017 highs

The technical break of the US 10-yr yield suggests a move to 2.63%/2.64% and thus more downside for the US Note future. Higher oil prices, rising inflation expectations and more signs of global monetary policy normalization are at play. US inflation readings (tomorrow and Friday) and German wage negotiations have the potential to accelerate the move. - Currencies: USD/JPY, EUR/JPY and EUR/USD drifting south

Yesterday, yen strength was the name of the game and it looks that this trend might continue today. The dollar is a good second best. The eco calendar is thin today. A less buoyant risk sentiment might reinforce the rebound of the yen. Sterling hardly profits from the UK government reshuffle

The Sunrise Headlines

- US stock markets ended marginally higher yesterday (+0.1%) with the Dow Jones outperforming (+0.4%). Most Asian stock markets lose some ground overnight with China underperforming.

- China's producer prices rose at their slowest pace in 13 months in December, as the government's war against winter smog dented factory demand for raw materials in a sign the world's second largest economy has started to slow.

- US job openings fell for a second straight month in November, with declines in the manufacturing and real estate sectors. The monthly JOLTS also found that layoffs dropped to a six-month low, showing continued labour market strength.

- Italy's 5-Star leader Luigi Di Maio says that he doesn't think the country needs to leave the euro anymore because the French-German alliance isn't as strong as in the past, Corriere della Sera reports

- Global growth appears to have peaked, with demographics, a lack of investment, a slowing in productivity gains and tightening monetary policy placing limits on economic expansion, the World Bank said.

- The EU is systematically warning UK companies of a regulatory chill after Brexit as it seeks to accelerate the private sector's preparations for a no-deal UK exit, according to recent legal notices reviewed by the FT.

- Today's eco calendar contains UK industrial production and US import/export prices. Germany and the US tap the market. Chicago Fed Evans discusses the economic outlook

Currencies: USD/JPY, EUR/JPY And EUR/USD Drifting South

USD/JPY, EUR/JPY and EUR/USD all drifting south

The swings in the yen took centre stage on FX markets yesterday. The yen rose against most majors. The BOJ bought fewer long-dated bonds, raising speculation that it might consider a first step to a less easy monetary policy. The yen held strong and USD/JPY closed the day at 112.65. The dollar was a good second best. The trade-weighted dollar (DXY) rebounded of recent lows, supported by higher US yields. EMU eco data remained very strong, but didn't help the euro. The correction in EUR/USD and EUR/JPY longs that started on Friday, continued. EUR/USD closed the day at 1.1937. EUR/JPY dropped to 134.47, compared with an intraday top of 136.64 on Friday.

The equity rally lost momentum overnight, but the correction is limited given recent gains. Yesterday's rise of the yen continues. USD/JPY trades near 112.30. EUR/USD trades in the 1.1930 area, holding with reach of yesterday's ST correction low. The eco calendar is again only modestly interesting. US import prices will be published. Markets are growing more sensitive to price data. A small reaction is possible in case of a big surprise, but the PPI's and CPI later this week are more important. This morning, it looks that the FX trends of the previous days continue. A less buoyant risk sentiment might support further yen gains. The decline of USD/JPY and EUR/JPY also weighed on EUR/USD earlier this week. The EUR/USD decline might slow if the rise in US yields slows. Even so, we see no trigger for a sharp EUR/USD rebound right now. The price action since Friday suggest that the topside in EUR/USD is rather well protected. In a broader perspective, slightly disappointing payrolls didn't cause USD damage. EUR/USD 1.2092 resistance survived. This week's US price data are a next reference for USD trading. Recently, the greenback suffered as the global recovery might force other major CB's to join policy normalisation. We keep the hypothesis that enough good news on the euro/'bad news' on the USD is discounted and that a sustained break beyond 1.2092 is not evident.

Yesterday, sterling held a tight sideways range against the euro and declined against a stronger dollar. The UK government reshuffle had no big impact. UK production and trade balance data will be published today. Production is expected rather solid. However, we don't expect a the data to be really supportive for sterling. The EUR/GBP correction might slow (underlying GBP weakness), but a rebound will be difficult if EUR/USD remains under pressure. EUR/GBP 0.8700/60 support looks solid. We keep a EUR/GBP buy-on-dips in case of return action to 0.87.

USD/JPY: repositioning out of yen-shorts continues

EUR/SEK 1H Chart: Pair Trades In Falling Wedge

EUR/SEK has been trading in a channel up since late 2016. During its last wave down which started mid-December, the common European currency has likewise formed a falling wedge. It tested the bottom boundary of this pattern on January 5 and has since edged slightly higher. From technical point of view, the Euro should approach the upper wedge line in the 9.84/86 territory. Meanwhile, the pair has been currently stranded between the 55-, 100– and 200-hour SMAs in a diminishing trading range. It is likely that a breakout from this area would determine the subsequent direction. Technical indicators show that the southern barrier might surrender under the bearish pressure, thus possibly sending the Euro down to 9.76 area where the monthly S1 and the weekly S2 are located. An upside breakout, however, could result in a test of the 9.90 mark within the following week or more.

GBP/AUD 1H Chart: Pound Remains Sticky To Channel Line

The Pound has been constrained by an ascending channel against the Aussie since mid-July. The lower boundary of this long-term pattern was reached last week. The pair, however, has since remained trading along this line. The Pound's inability to initiate a new wave up suggests that it might breach the given pattern in the nearest time. An early indication that such a scenario might occur could be a breakout of the 55-, 100– and 200-hour SMAs circa 1.7280. On the other hand, technical indicators flash bullish signals during the following week, thus pointing to a minor weakness which could be followed by a period of appreciation. A possible upside target for the following two weeks might be the combined resistance of the monthly PP and the weekly R2 circa 1.75.

EURUSD Analysis: Expectedly Slides To Monthly PP

The appreciation of the Dollar continued on Tuesday, as expected. After reaching support level set up by the monthly PP at 1.1917 the currency rate resumed the surge. However, recovery of the Euro is unlikely to last for long due to resistance formed, first, by the weekly S2 and the 55-hour SMA and, second, by the weekly S1 in conjunction with the 100- and 200-hour SMAs. From daily perspective, the pair is expected to continue moving towards the lower boundary of a three-month long ascending channel. In support of this assumption, two-thirds of all pending orders in both in 50- and 100-pip range are set to sell. Nevertheless, there is a need to take into account that the 61.8% Fibonacci retracement level located at 1.1887 might temporarily halt the downfall.