Sample Category Title

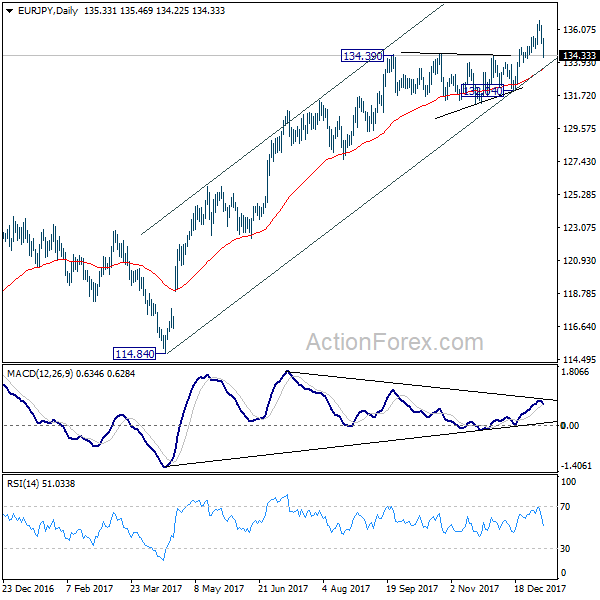

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 134.87; (P) 135.59; (R1) 136.05; More....

EUR/JPY's break of 134.39 resistance turned support now suggests that rise from 132.04 has completed at 136.63. It's also seen as an early sign of trend reversal. But it's yet to be confirmed. In any case intraday bias is now on the downside for 132.04 support. Above 135.12 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 136.63 holds.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should now be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indciate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

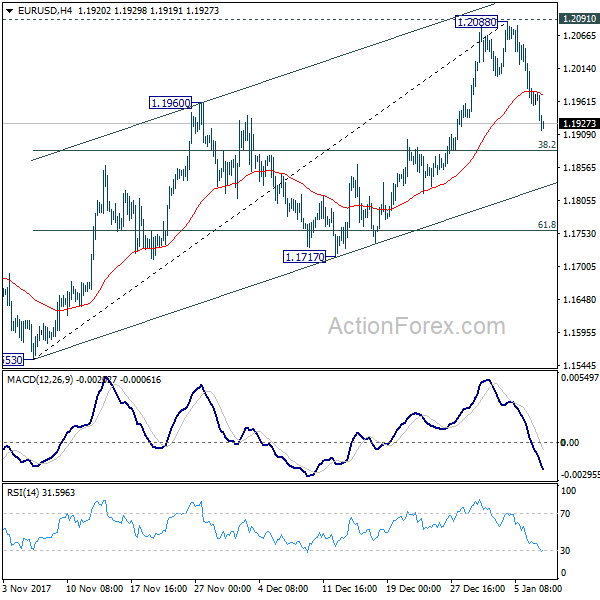

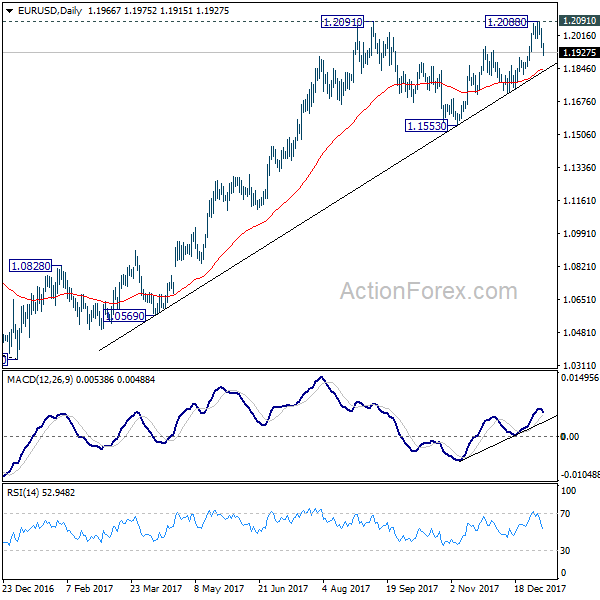

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1931; (P) 1.1991 (R1) 1.2028; More....

EUR/USD's fall from 1.2088 is still in progress and intraday bias remains on the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Such decline might be the third leg of consolidation pattern from 1.2091. Break of 1.1884 will target 61.8% retracement at 1.1757 and below. On the upside, firm break of 1.2091 is needed to confirm up trend resumption. Otherwise, we'd expect more corrective trading in near term.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

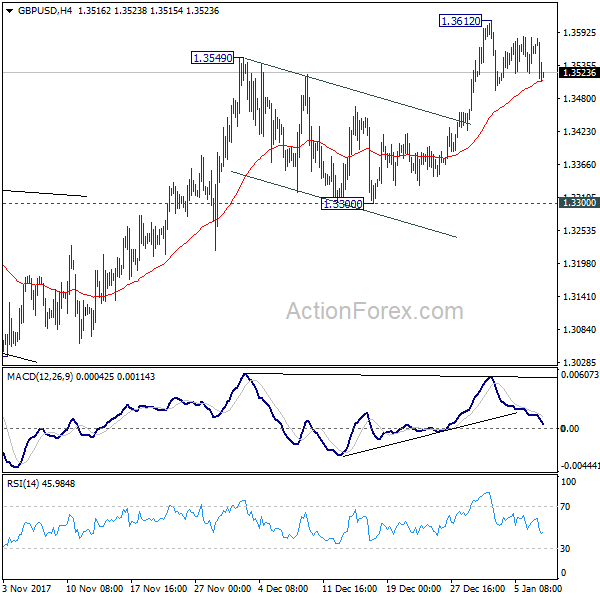

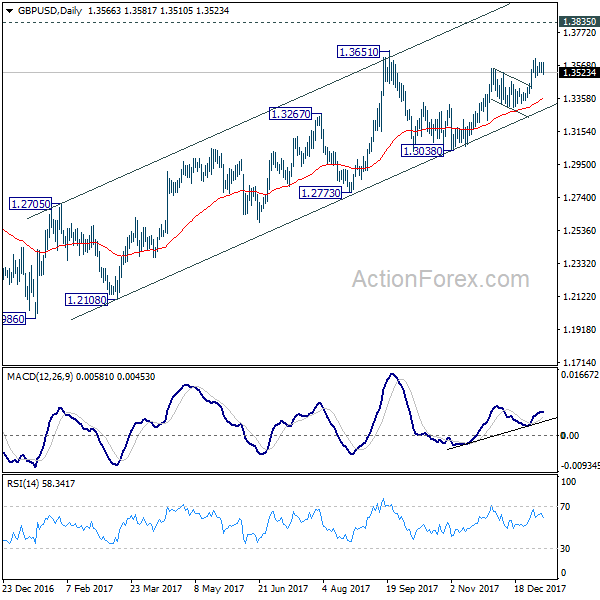

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3530; (P) 1.3558; (R1) 1.3593; More.....

Outlook in GBP/USD is unchanged. Intraday bias stays neutral. As long as 4 hour 55 EMA (now at 1.3509) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support instead.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

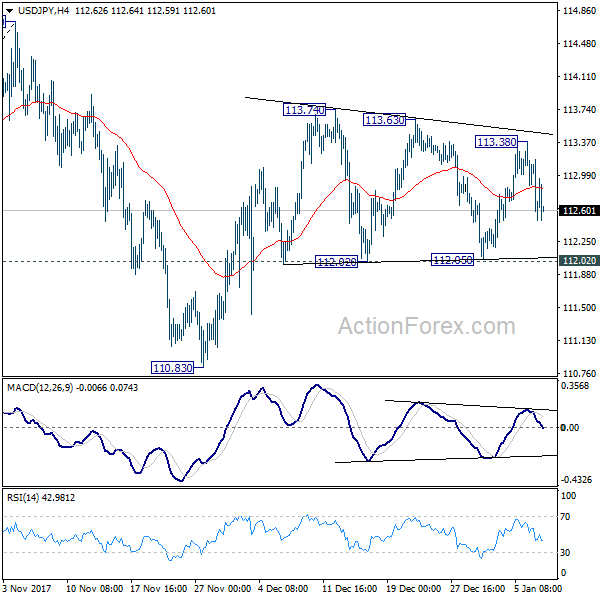

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.85; (P) 113.11; (R1) 113.35; More...

USD/JPY is still staying in range of 112.02/113.74. Intraday bias remains neutral at this point. Also, outlook remains cautiously bullish as long as 112.02 holds and further rise is in favor. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

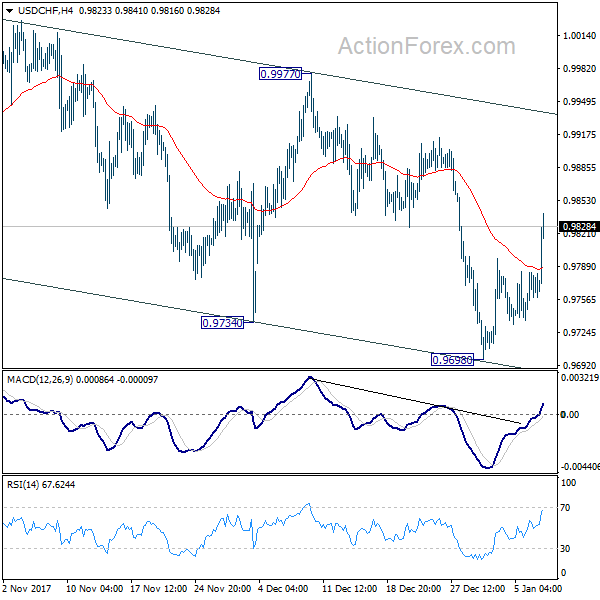

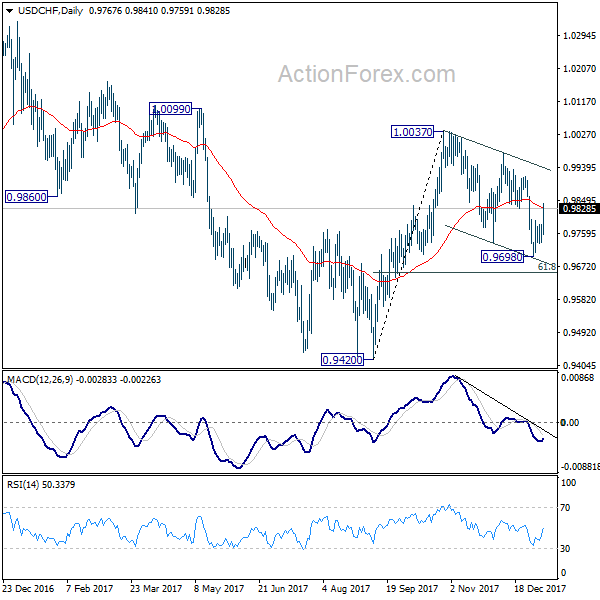

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9745; (P) 0.9764; (R1) 0.9791; More....

USD/CHF's strong break of 4 hour 55 EMA argues that correction from 1.0037 has completed with three waves down to 0.9698. Intraday bias is back on the upside for 0.9977 resistance first. Break there will likely resume whole rise from 0.9420 through 1.0037 high. For now this will be the favored case as long as 0.9698 support holds.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Yen Maintains Gains on BoJ Stimulus Exit Talks, Dollar Catching Up

Yen remains the strongest major currency for today as BoJ operates spurred speculations of stimulus exit. Dollar also follow closely as the second strongest one. On the other hand, European majors are under much selling pressure as recent rally fails to sustain momentum. Euro continue to shrug off positive economic data while EUR/USD's fall gathers steam. Elsewhere, commodity currencies are generally mixed. Speculations for a January BoC rate hike continue to grow. But Loonie's rally is looking stretched.

Technically, USD/CHF takes out 4 hour 55 EMA firmly today. That's accompanied by strong break of 4 hour 55 EMA in EUR/USD too. Both suggests near term reversal and favors more gain in Dollar. EUR/JPY's break of 134.39 also indicates near term reversal and puts 132.04 support back into focus. But USD/JPY is holding in range above 112.02 support, maintaining mild near term bullishness.

Eurozone unemployment hit almost 9 years low

Eurozone unemployment rate dropped to 8.7% in November, down from 8.8% and met expectations. That's also the lowest level in nearly 9 years since 2009. Strength in the economy is translating into jobs and would hopefully into inflation too. While at the last forecast, ECB is not expecting inflation to return to 2% target at least till 2020, there are already calls for exit of stimulus. A key argument is that even if the asset purchase program ends in September, monetary accommodations are still there. Some ECB officials argued that would just mean putting the foot off the gas a little bit, instead of pressing on the break.

Also released from Europe, German industrial production rose 3.4% mom in November. German trade surplus widened to EUR 22.3b in November. Swiss unemployment rate dropped to 3.0% in December, foreign currency reserves rose to CHF 744b. Swiss retail sales dropped -0.2% yoy in November.

BoJ cut 10-25 years JGB purchase by JPY 10b, spurred stimulus exit talks

Yen surges broadly today as data showed BoJ has cut its long-dated JGB purchases in market operations. That's seen as a sign by many of BoJ is finally moving towards stimulus exit. Today, BoJ offered to buy JPY 190b of JGBs with 10 to 25 years maturity. That's JPY 10b lower from the prior tender on December 28. Besides, BoJ also lower the offer on 25 to 40 years maturity JGBs by JPY 10b to JPY 90b. Nonetheless, it should be emphasized that it's far still early for BoJ to start stimulus exit as inflation remains way off target.

Also, it's still uncertain whether BoJ Governor Haruhiko Kuroda's term would be renewed this year. Prime Minister Shinzo Abe said during the weekend that "Gov. Kuroda has met my expectations with job availability at a 43-year high," and "I want him to keep up his efforts". But Abe also noted that "I haven't made up my mind" on who's going to lead BoJ after Kuroda's term expires in April.

Released from Japan, labor cash earnings rose 0.9% yoy in November, above expectation of 0.6% yoy.

North and South Korea agreed military talks to ease tensions

The highly anticipated meeting between North and South Korea officials ended with some fruitful results. The high level meeting was the first time in more than two years, at the Korean peninsula's heavily fortified demilitarized zone known as "peace village". IN a joint closing statement, it's noted that North Korea will send a high-level delegation comprising athletes, a cheering squad, an art troupe, a visitors' group, a Taekwondo demonstration team and a press corps, to the Winter Olympic in South next month.

Also, the two nations announce military talks "to ease the current military tensions between the two Koreas." South Korean unification vice minister Chun Hae-sung said that "We expressed the need to promptly resume dialogue for peace settlement, including denuclearization, and based on the mutual respect (the two Koreas) cooperate and stop activities that would raise tensions on the Korean Peninsula." And that was agreed by the North.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9745; (P) 0.9764; (R1) 0.9791; More....

USD/CHF's strong break of 4 hour 55 EMA argues that correction from 1.0037 has completed with three waves down to 0.9698. Intraday bias is back on the upside for 0.9977 resistance first. Break there will likely resume whole rise from 0.9420 through 1.0037 high. For now this will be the favored case as long as 0.9698 support holds.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Nov | 0.90% | 0.60% | 0.60% | 0.20% |

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Dec | 0.60% | 0.30% | 0.60% | |

| 00:30 | AUD | Building Approvals M/M Nov | 11.70% | -1.00% | 0.90% | -0.10% |

| 05:00 | JPY | Consumer Confidence Index Dec | 44.7 | 45 | 44.9 | |

| 06:45 | CHF | Unemployment Rate Dec | 3.00% | 3.00% | 3.00% | 3.10% |

| 07:00 | EUR | German Industrial Production M/M Nov | 3.40% | 1.80% | -1.40% | -1.20% |

| 07:00 | EUR | German Trade Balance Nov | 22.3B | 20.7B | 19.9B | |

| 08:00 | CHF | Foreign Currency Reserves Dec | 744B | 738B | ||

| 08:15 | CHF | Retail Sales Real Y/Y Nov | -0.20% | -2.50% | -3.00% | -2.60% |

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 8.70% | 8.70% | 8.80% | |

| 13:15 | CAD | Housing Starts Dec | 217K | 240K | 252K |

Canadian Dollar Stays Sideways, Housing Starts Next

The Canadian dollar continues to move sideways this week. In the Tuesday session, the pair is trading at 1.2423, up 0.03% on the day. On the release front, Canada releases Housing Starts, with an estimate of 240 thousand. In the US, today's key event is JOLTS Job Openings, which is expected to climb to 6.05 million. On Wednesday, Canada releases Building Permits.

After a strong December, the Canadian dollar hasn't missed a beat in January, with gains of 1.2% percent. Recent economic indicators have pointed upwards, led by sizzling employment numbers. The economy added 78.6 thousand jobs, crushing the estimate of 1.8 thousand. In November, the economy added 79.5 thousand. The unemployment rate dropped to 5.7%, down from 5.9% a month earlier. The strong numbers sent the Canadian dollar higher on Friday. Last week marked a third winning week for the rejuvenated Canadian dollar, and on Friday the currency hits its highest level against the US dollar since late September.

Much of the Canadian dollar's recent climb can be attributed to the rise in oil, which has jumped 6.8% since mid-December. Geopolitical tensions have boosted oil prices, in particular tensions with North Korea and the recent civil unrest in Iran. There is pressure on the Bank of Canada to raise its benchmark rate of 1.0%, which is lagging behind the Federal Reserve rate of between 1.25%-1.50%. With the Fed widely expected raise rates in January, the Canadian dollar could lose ground if the BoC fails to respond with a rate hike of its own on January 17. However, the BoC may hold back, as it concerns continue over US threats to dismantle the free trade agreement.

Interest rates may be in the headlines, but another important parameter is the Federal Reserve's balance sheet. As of this month, the Fed has started to shrink its massive balance sheet of $4.4 trillion. The balance sheet ballooned during the financial crisis of 2008-2009, and good times have allowed the Fed to begin trimming its portfolio. Incoming Fed Chair Jerome Powell, who takes over in February, has estimated that the balance sheet could drop to anywhere between $2.4 trillion to $2.9 trillion after several years of cuts. Fed policymakers have not indicated a magic number for the balance sheet, but the cuts indicate a vote of confidence in the US economy.

CAC Rally Continues, Investors Eye French Industrial Production

The CAC index has posted gains in the Monday session. Currently, the index is at 5515.00, up 0.50%. On the release front, France's trade deficit widened to EUR 5.7 billion, above the forecast of EUR 4.8 billion. This marked the highest trade deficit since August.

Stock markets have jumped out of the gates in 2018, and the CAC has jumped onto the bandwagon, posted strong gains of 3.8% in January. Investors are giving the eurozone economy a thumbs-up, as the bloc is on track for a solid fourth quarter, as growth continues and unemployment falls. Inflation has also moved higher, although the ECB is unlikely to reconsider its current stimulus program, which ends in September.

The political vacuum hasn't affected the robust German economy, but it has sidelined President Angela Merkel, arguably the head of the eurozone. French President Emmanuel Macron has grandiose plans for the further integration of the eurozone, such as harmonizing corporate tax regimes and establishing a eurozone budget. Merkel would make an ideal partner to reform the bloc, but she can't lend Macron a helping hand while she leads a caretaker government. Merkel's conservative bloc is talking with the Social Democrats, but German coalition talks tend to move slowly, and could last for several more months.

Dollar Index Crawls up ahead of JOLTs Job Openings; European Stocks Drift Higher

Here are the latest developments in global markets:

FOREX: The dollar pared some losses versus the yen, crawling up to 112.80 (-0.25%) after a trim of bond buying from the BOJ send the currency to a five-day low earlier in the day. Euro/dollar moved further down to 1.1924 (-0.33%) probably due to investors engaging in profit-taking, while pound/dollar corrected lower towards 1.3530 (-0.27%) on the back of a stronger greenback. The dollar index peaked at a 1 ½-week high of 92.30.

STOCKS: European stocks extended their gains on Tuesday to fresh 2 ½-year highs with consumer sectors leading the indices. The pan-European STOXX 600 was 0.30% up at 1015 GMT, boosted by news that the high indebted Netherlands-based cable group Altice, whose shares tumbled by 54% last year, agreed to restructure its European operations and separate its US unit by distributing that unit's shares to existing shareholders. The blue-chip Euro STOXX 50 also jumped by 0.30%. The German DAX 30 and the French CAC 40 surged by 0.55% while the British FTSE 100 rose by 0.32%, with the British food retailers including Marks & Spencer performing the best. Earnings reports will be in the spotlight this week.

COMMODITIES: Oil prices lost positive momentum during early European session but remained near fresh 2 ½ -year highs touched during the Asian trading hours amid expectations of a tighter market supported by falling US oil inventories and OPEC-led supply cuts. WTI crude was last trading at $61.87 (+0.23%) and Brent was steady at $67.81 after breaking brefly above the 68-key level. Gold retreated by 0.40% to $1,314.70 per ounce

Day ahead: US JOLTs job openings and Canadian housing starts eyed

Looking through the rest of the day, markets will keep a close eye on the US and the Canadian dollar as data releases associated with a medium to high-risk volatility are scheduled to be delivered during European afternoon.

At 1315 GMT, Canada will report on housing starts, with analysts expecting the annualized gauge to post a softer increase of 212,500 compared to a rise of 252,200 seen in November when the measure reached its highest level in almost a decade. Note that the Canadian government plans to impose stricter regulations on mortgage borrowers in 2018, a strategy that could weaken housing demand.

In the US, the Bureau of Labor Statistics will publish JOLTs job openings at 1500 GMT, a survey conducted to record changes in the US job vacancies. According to forecasts, in November 6.038 million positions were opened, slightly higher than 5.996 million seen in the prior month and marginally below September's all-time high of 6.177 million.

Meanwhile, Minneapolis Fed President, Neel Kashkari, who was on the opposition of monetary tightening since he took office in 2016, voting against last year's three rate hikes, will be participating in a Q&A session at 1500 GMT. However, it is worth to note that Kashkari will not be a voting member in 2018.

In addition, political developments in Germany will gather some attention as Merkel's Christian Democrats (CDU) are holding five-day talks started on Sunday with their former coalition partner Christian Social Union (CSU) and Social Democrats (SPD) in an effort to form a coalition government.

Besides that, news out of the Korean peninsula will be in focus after South and North Korea held high-level talks for the first time in more than two-years earlier today to discuss on Winter Olympic Games taking place in South Korea in February.

EURGBP Steadies after Two Strong Sell-off Days But Remains Bearish

EURGBP appears poised for further losses and slipped beneath the 0.8850 barrier, while euro was the worst performing major currency during yesterday's trading session. The single currency had been under pressure versus sterling during the US trading session on Tuesday and ended the day near its low.

The price recorded the second straight bearish day and plummeted almost 1% following the bounce off the 0.8923 resistance level. Currently, in the short-term timeframe, the pair is developing between the 38.2% and the 50.0% Fibonacci retracement levels of the last significant upward movement with the low at 0.8690 and the high at 0.8923. The aforementioned levels are holding near the 0.8833 resistance level and the 0.8805 support level respectively.

In case of further losses, the price could drop until the 61.8% Fibonacci mark near 0.8780 or moreover towards 0.8760. An alternative scenario is an upward correction until the 0.8850 obstacle and the 23.6% Fibonacci level 0.8867, which is close to the 25-simple moving average in the 4-hour timeframe.

During the previous sessions, the two SMAs (14 and 25) posted a bearish crossover, indicating a continuation of the sell-off. However, the momentum indicators seem to be in confusion. The RSI indicator is sloping to the upside in the negative territory, signaling for a pause of the downward movement, but the MACD oscillator is still strengthening its negative momentum below the zero and trigger lines.

Having a brief look in the daily timeframe, EURGBP has been trading within a downward sloping channel since October 2017, endorsing the scenario for bearish behavior in the medium term.