Sample Category Title

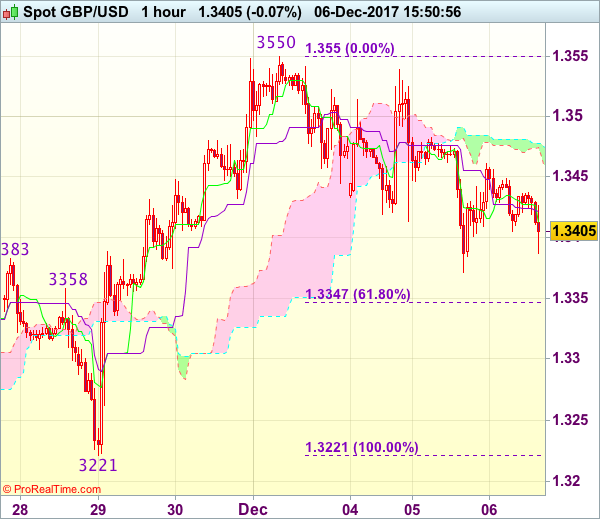

Trade Idea : GBP/USD – Hold short entered at 1.3440

GBP/USD - 1.3401

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3412

Kijun-Sen level : 1.3416

Ichimoku cloud top : 1.3478

Ichimoku cloud bottom : 1.3467

Original strategy :

Sold at 1.3440, Target: 1.3340, Stop: 1.3475

Position : - Short at 1.3440

Target : - 1.3340

Stop : - 1.3475

New strategy :

Hold short entered at 1.3440, Target: 1.3340, Stop: 1.3465

Position : - Short at 1.3440

Target : - 1.3340

Stop : - 1.3465

Cable recovered after the anticipated selloff to 1.3371 and minor consolidation would be seen, however, reckon upside would be limited to 1.3450 and bring another decline, below said support would extend the fall from 1.3550 for retracement of recent rise to 1.3340-50 (61.8% Fibonacci retracement of 1.3221-1.3550) but near term oversold condition should prevent sharp fall below 1.3300 and reckon 1.3260-65 would hold, bring rebound later.

In view of this, we are holding on to our short position entered at 1.3440. Above 1.3460-65 would defer and risk test of resistance at 1.3483 but only break there would signal an intra-day low is formed instead, bring another bounce to 1.3530-35 first.

Forex: US Trade Gap Widens, Aussie GDP Disappoints

Data released by the US Commerce Department on Tuesday indicated that the US trade gap rose 8.6% in October from $44.9 billion in September, as imports from China and other suppliers hit a record high ahead of the holiday shopping season. Imports hit a record $244.6 billion in October, and exports were unchanged at $195.9 billion. For 2017, the US is running a trade deficit of $462.9 billion, up 11.9% over the same period in 2016. U.S. exports are up 5.3% this year. Imports totaled $48.2 billion from China, $39.4 billion from the EU and $28.7 billion from Mexico — all record highs. During President Trump's recent visit to Beijing, US companies signed contracts valued by the Commerce Department at around $250 billion. But it could be months before any of those transactions are reflected in U.S. trade data.

On Tuesday, data from Markit's Eurozone Services PMI for November was released coming in at 56.2 (previously 55.0), the composite was higher at 57.5 (56.0 in October). The strong number reflects a strengthening of economic expansion across the big-four Eurozone countries, with output growth accelerating to the fastest in over 78 months. Additionally, job creation has risen to a 17-year high and price pressures have strengthened.

Data from the Australian Bureau of Statistics published earlier today showed Australian GDP grew by 0.6% in seasonally adjusted chain volume terms, slightly below the 0.7% level expected by the markets. Annualized GDP came in at 2.8%. This is markedly better than the 1.8% seen in Q2, but was below the 3% growth that the markets had hoped for. AUDUSD fell on the news to near month lows of around 0.75717 before stabilizing.

EURUSD is 0.15% higher in early Wednesday trading at around 1.1840.

USDJPY is 0.4% lower in early trading at around 112.11.

GBPUSD is 0.15% lower in early session trading at around 1.3422.

AUDUSD is 0.3% lower following the GDP release, trading around 0.7585.

Gold is 0.1% higher overnight, currently trading around $1,267.5 after touching close to 2-month lows around $1,264.11.

WTI is little changed overnight, trading around $57.45.

Major data releases for today:

At 08:00 GMT: the European Central Bank (ECB) Non-monetary policy meeting is scheduled to take place in Frankfurt, Germany.

At 13:15 GMT: Automatic Data Processing Inc in the US will release ADP Employment Change for November. The markets are forecasting a gain of 190K, a drop from Octobers' gain of 235K. The ADP data may hold clues as the markets await Friday's all-important NFP release.

At 15:00 GMT: The Bank of Canada (BoC) is scheduled to provide a rate statement and interest rate decision. The markets are forecasting that the BoC will keep interest rates on hold at 1%. If there is a change in Canadian monetary policy and rates are hiked we can expect to see CAD volatility. That said, many believe the likelihood of such a hike is unlikely until Q2 of 2018.

Currencies: Risk-Off Correction To Slow Further USD Gains

Sunrise Market Commentary

- Rates: Commodity sell-off could hurt risk sentiment

Risk sentiment deteriorates in Asia this morning with Japan losing up to 2%. Yesterday's commodity sell-off continues on Asian exchanges and gains traction cross markets. Spillover to Europe could lift core bonds via safe haven flows. Trading was lackluster so far this week with investors unwilling to front run on Friday's payrolls and next week's Fed meeting. - Currencies: Risk-off correction to slow further USD gains

The dollar profited slightly from the protracted rise in US ST yields yesterday. Especially EUR/USD drifted gradually lower. However, the US rebound was blocked later in the session by a risk-off correction. This correction continues this morning in Asia. USD/JPY remains vulnerable. The jury is still out, but USD/EUR looks more resilient.

The Sunrise Headlines

- US stock markets ended around 0.4% lower yesterday. Asian risk sentiment deteriorated with Japan losing up to 2%. Asian commodity markets catch up with yesterday's sell off in mainly industrial metals.

- UK PM May is facing a revolt from inside her Cabinet over her plan to keep UK regulations aligned with the EU after Brexit, a split that threatens to undermine her hopes of breaking the deadlock in negotiations.

- Donald Trump plans to recognise Jerusalem as the capital of Israel and will announce plans to move the US embassy there from Tel Aviv, defying fears among counterparts in the Middle East and elsewhere that such a move would threaten efforts to broker peace.

- Australia's economy expanded by 0.6% Q/Q in Q3 (vs 0.7% Q/Q expected) thanks to a long-awaited jump in business investment, though marked weakness in household spending cast a cloud over the outlook for growth.

- Chicago Fed Evans questioned whether the Fed is really in a hurry to raise rates. “What if we just decided to wait until the middle of the year and if we saw inflation pick up, then we could do something?”

- BoJ board member Masai advocated sticking with ultra-easy monetary policy due to uncertainty over how fast inflation will rise, while warning that the central bank should remain on guard against the possible side-effects.

- Today's eco calendar contains US ADP employment and Bank of Canada's interest rate decision. ECB Mersch is scheduled to speak and Germany taps the market.

Currencies: Risk-Off Correction To Slow Further USD Gains

Risk-off correction to cap further USD gains?

There were few data with market moving potential yesterday. US ST yields rose further, widening the interest rate differential in favour of the dollar. Of late, the dollar often ignored the guidance from interest rate markets, but this time it helped the US currency to some cautious gains. The US non-manufacturing ISM was slightly softer than expected. It didn't hurt the dollar much, but the US currency lost slightly ground later as equities turned again negative. EUR/USD closed the session at 1.1826. USD/JPY finished at 112.60.

The US equity slide accelerated in Asia overnight. Commodity related stocks are taking the lead in the decline after a sell-off of copper yesterday. Losses on Asian markets vary from about 0.5% (India) to almost 2% (Japan). The equity decline pressures US yields with modest impact on the dollar. USD/JPY dropped to the low 112 area. EUR/USD is less affected and trades in the 1.1840 area. Yesterday, the Aussie dollar profited from positive comments in the RBA statement. Part of the gain was already undone yesterday (copper correction). The reversal continued this morning as Australian Q3 GDP was slightly softer than expected at 0.6% Q/Q and 2.8% Y/Y (0.7% Q/Q and 3.0% Y/Y was expected).

There are few data with market moving potential in Europe or in the US today. The ADP labour market report is the exception to the rule. The consensus expects 190 000 net job growth in the US private sector (from 235 000 in October, probably still affected by the consequences of the hurricanes). We have no reason to take a different view from consensus. The expected job growth remains good, given that the US eco cycle has already advanced quite a long way. Of late, the reaction of the (FX) market to the ADP was mostly modest as the month-on-month correlation with the payrolls is not that tight

The dollar showed a mixed picture last week, rebounding against the yen but holding relatively soft against the euro. This week, there were tentative signs (especially yesterday) that the US currency could get a bit more support from the protracted rise in ST US yields (2-y US yield rising above 1.8%). Markets are gradually moving a bit more in the direction of the Fed guidance (dot-plot). For now, it didn't help the dollar that much. Even so, it should at least help to put a floor for the US currency as USD shorts are becoming ever more expensive.

Of course, this process might again be aborted if global markets fall prey to an outright risk-off correction. Even so, we have the impression that the topside in EUR/USD is becoming a bit tougher.

We still see no reason for EUR/USD to rise beyond the 1.1961/1.20 area ahead of next week's Fed meeting, unless there comes high profile negative news from the US. USD/JPY reacted more to interest differentials of late, but the pair might be more vulnerable in case of a risk-off correction.

From a technical point of view: EUR/USD set a post-ECB low mid-November, but dollar momentum wasn't strong enough. EUR/USD regained the 1.1880 MT correction top, opening the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. For now, there is no clear technical signal. USD/JPY's momentum deteriorated early November, dropping below the 111.65 neckline. No aggressive follow-through selling occurred though. Last week the pair succeeded a nice rebound, calling off the downside alert. The pair again hovers in the 110.84/114.73 consolidation range. We amend our ST bias from negative to neutral.

EUR/USD: rally aborted, but no sustained downside correction yet

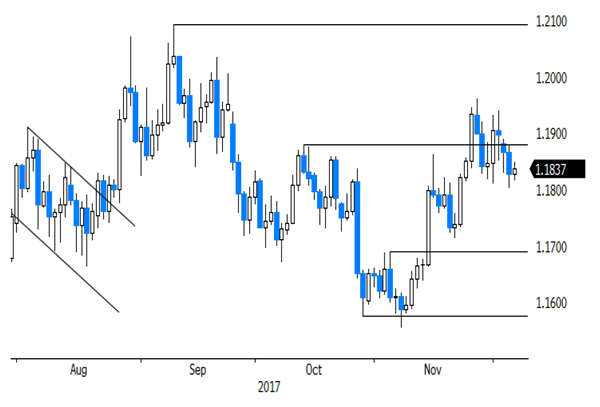

EUR/GBP

Sterling awaiting less diffuse news from Brexit

Monday's last minute failure to strike a separation deal on Brexit kept sterling in the defensive yesterday morning. The UK services PMI came out slightly softer than expected at 53.8 from 55.6 (55.00 was expected), but price indictors in the report rose quite sharply. Sterling traded already off the recent lows at the time of the PMI release and regained some further ground late in the session. Markets apparently still hope that a deal can be reach in the near future even if the political signals from the UK remain very diffuse. EUR/GBP closed the session at 0.8797. Cable finished the day at 1.3443, but this move still reflected some USD strength.

There are no important eco data in the UK today. So, Brexit headlines/rumours will continue drive GBP trading. The comments this morning at least suggest that UK PM May has still plenty of work to do to convince hard-line Brexit supporters in her party and to meet the wishes of the DUP. Sterling is slightly in the defensive this morning. Sterling traders remain reluctant to place big directional bets as the Brexit news flow might change minute by minute. An agreement is still possible ahead of next week's EU summit. However, given recent developments, we don't add sterling longs at this stage. More erratic trading might be on the cards unless there comes some real clarity on Brexit.

MT view/technical picture: A BoE driven sterling rebound ran into resistance early last month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral mid-November. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: downside test rejected as separation deal is no done thing yet

Trade Idea : EUR/USD – Sell at 1.1900

EUR/USD - 1.1826

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1832

Kijun-Sen level : 1.1839

Ichimoku cloud top : 1.1885

Ichimoku cloud bottom : 1.1862

Original strategy :

Sell at 1.1915, Target: 1.1815, Stop: 1.1950

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1900, Target: 1.1800, Stop: 1.1935

Position : -

Target : -

Stop : -

As the single currency recovered after falling to 1.1800 yesterday, minor consolidation would be seen and corrective bounce to 1.1860 cannot be ruled out, however, reckon 1.1900 would limit upside and bring another decline later, below said support would extend the fall from 1.1961 (last week’s high) to 1.1770 and possibly towards support at 1.1736 but price should stay above previous key support at 1.1713.

In view of this, we are looking to sell euro on recovery as 1.1900 should limit upside and bring another decline. Above last Friday’s high at 1.1940 would revive bullishness, bring retest of 1.1961, break there would confirm early upmove has resumed for headway to 1.1990-00 which is likely to hold from here.

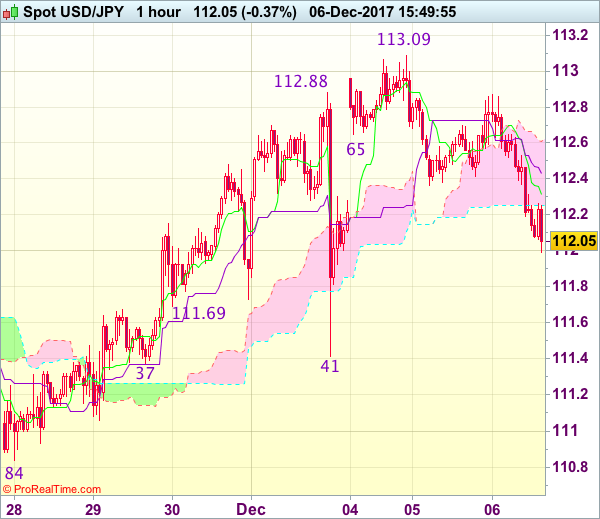

Trade Idea : USD/JPY – Hold long entered at 112.10

USD/JPY - 112.07

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.31

Kijun-Sen level : 112.43

Ichimoku cloud top : 112.61

Ichimoku cloud bottom : 112.25

Original strategy :

Bought at 112.10, Target: 113.30, Stop: 111.75

Position : - Long at 112.10

Target : - 113.30

Stop : - 111.75

New strategy :

Hold long entered at 112.10, Target: 113.30, Stop: 111.75

Position : - Long at 112.10

Target : - 113.30

Stop : - 111.75

Although the greenback slipped again today and marginal weakness from here cannot be ruled out, reckon downside would be limited and 111.80 should hold, bring rebound later, above 112.90 would signal the retreat from 113.09 has ended, bring retest of this level, break there would extend recent rise to resistance at 113.33 but loss of upward momentum should prevent sharp move beyond 113.60-70.

In view of this, we are holding on to our long position entered at 112.10. Below 111.80 would defer and risk weakness to 111.60 but only break of said support at 111.37-41 would abort and signal top is formed instead.

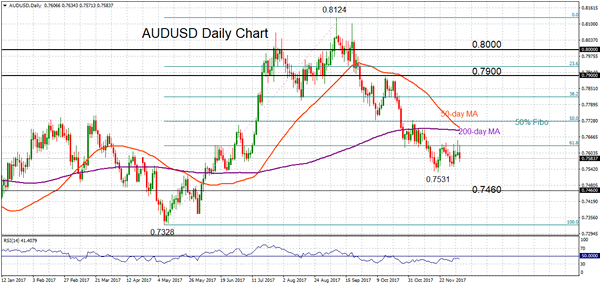

AUDUSD Neutral In Near Tterm, Bearish Market Structure Intact

AUDUSD has turned increasingly bearish as the pair continues to trade below its 200-day moving average and has retraced more than half of the rise from 0.7328 to 0.8124. Prices are now close to the lowest level in six months.

In the near term, the market is in a consolidation phase, capped by the 61.8% Fibonacci retracement level at 0.7631. AUDUSD needs to rise above this resistance level to ease immediate downside pressure. The 50% Fibonacci at 0.7725 is a strong resistance as well and a break above this area would indicate the start of a more sustained recovery with scope to target the key 0.7900 level and then the psychological at 0.8000. A re-test of the 0.8124 peak could set the AUDUSD on the path for a resumption of the May-August uptrend.

A breach of the 0.7531 low would make AUDUSD more vulnerable and weak with increased odds to fall through 0.7460 to reach 0.7328. Such a move would strengthen the bearish outlook.

Th RSI has no clear direction now and is pointing to more range trading in the near term. The overall market structure remains bearish as long as prices remain below the 200-day MA, with a high probability of AUDUSD continuing its downward trajectory.

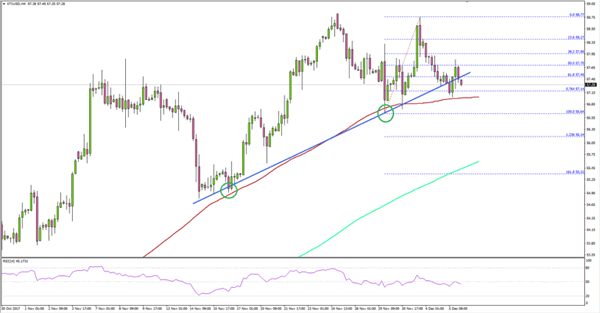

Crude Oil Price To Decline Further Towards $55.00?

Key Highlights

Crude oil price struggled to move above the $58.00-59.00 levels and moved down against the US dollar.

There was a break below a major bullish trend line with support at $57.40 on the 4-hours chart of XTI/USD.

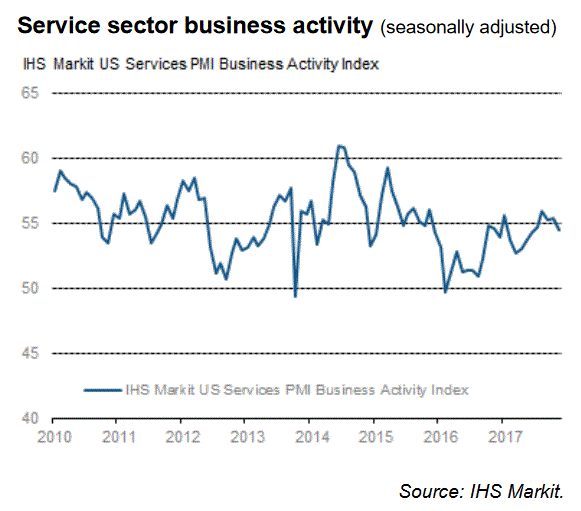

The US Services PMI in Nov 2017 decreased from the preliminary reading of 54.7 to 54.5.

Today, the US ADP Employment Change will be released for Nov 2017, which is forecasted to post a change of 185K, less than the last 235K.

Crude Oil Price Technical Analysis

Crude oil price gained heavily in November 2017 and moved above $58.00 against the US dollar. However, the price struggled during the start of December 2017 and is currently under bearish pressure.

Crude oil price struggled to move above the $58.00-59.00 levels and moved down against the US dollar.

There was a break below a major bullish trend line with support at $57.40 on the 4-hours chart of XTI/USD.

The US Services PMI in Nov 2017 decreased from the preliminary reading of 54.7 to 54.5.

Today, the US ADP Employment Change will be released for Nov 2017, which is forecasted to post a change of 185K, less than the last 235K.

Crude Oil Price Technical Analysis

Crude oil price gained heavily in November 2017 and moved above $58.00 against the US dollar. However, the price struggled during the start of December 2017 and is currently under bearish pressure.

Commenting on the report, the Chief Business Economist at IHS Markit, Chris Williamson, stated:

The slowest growth of services sector business activity since June, alongside a slight dip in the pace of manufacturing expansion, means the November PMI surveys registered a modest cooling in the overall rate of business growth. Mid-way through the fourth quarter, the surveys are still pointing to a reasonable GDP growth rate of approximately 2.5%.

Overall, the result was a bit less than the market forecast, which helped Crude oil price is staying above $57.00.

Economic Releases to Watch Today

US ADP Employment Change Nov 2017 – Forecast 185K, versus 235K previous.

BoC Interest Rate Decision – Forecast 1.00%, versus 1.00% previous.

US Dollar Slumped On Lower Long-Term US Yields

Market movers today

Germany is due to release factory orders for October this morning. In line with strong surveys, German order growth has been strong in recent months and showed the highest growth rate in six years in September of 9.5% y/y.

The ECB's Yves Mersch is due to speak in Frankfurt (11:30 CET ) on the theme ‘Challenges for Monet ary Policy in 2018', and will be the last ECB speaker before the silent period ahead of the December meeting.

This afternoon, the US ADP employment report for November is due. It is not a good predictor of the monthly non-farm payrolls but nevertheless tends to get some attention as a warm-up for Friday 'spay rolls (see also US Labour Market Monitor: Expect strong November report). The October ADP employment increase was quite robust at +235k.

The Bank of Canada is due to announce its rate decision at 16:00 CET. We and consensus expect rates to be unchanged at 1.0%. The Bank of Canada raised rates in July and September by 25bp at each meet ing.

This afternoon, the DOE is due to release US crude oil inventories.

Selected market news

Asian stock markets slipped this morning, dragged by earlier losses on Wall Street as the technology sector stuttered yet again after a brief rebound, while the US dollar slumped on lower long-term US yields. The spread between five-year and 30-year US yields fell below 60bp, which is the lowest since November 2007. Industrial metals also plunged overnight on the prospect of slower Chinese demand, dollar gains and a rise in stockpiles. S&P 500 futures are slightly higher this morning, shrugging off reports that Republican efforts to avoid a government shutdown have stalled.

US President Donald Trump is expected to make an announcement today about moving the US embassy from Tel Aviv to Jerusalem, thereby implicitly recognising it as the capital of Israel and upending decades of US foreign policy. Such a move has been strongly criticised by Arab leaders and risks fuelling renewed violence and conflict in the Middle East .

In Norway, the November Regional Network Survey, which is Norges Bank's preferred gauge of economic activity, indicated improved growth prospects in all sectors besides construction, with capacity utilisation at the highest level since 2013.

This morning we published Danske Bank 2018 Fixed Income and FX Top Trades . In the fixed income sphere, we recommend positioning for further performance for carry strategies, small moves in out right yields, performance for Danish and Swedish fixed income, periphery performance, tighter USD liquidity in the CCS market and a further flat tening of the US yield curve . In it , we focus on five themes: (1). cyclical support for carry – but volatility is low, (2) policy normalisation, (3) a ‘new' Fed, (4) Scandi housing fragility and (5) currency vulnerability as the foundation of our trades.

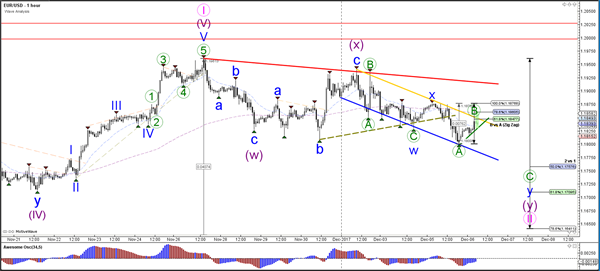

Daily Wave Analysis: EUR/USD Bearish Channel Aiming At 1.17 And 50-61.8% Fibonacci

Currency pair EUR/USD

The EUR/USD is building a bearish correction as expected. The choppy and corrective price action is making a wave 1-2 (pink) pattern more likely. The bearish channel could take price down lower to the Fibonacci levels of wave 2. A break below the bottom (purple box) invalidates this wave pattern.

The EUR/USD broke below the support trend line (dotted green) and fell below 1.18 but is a sturdy pullback. This could be part of a wave B (green) within a larger bearish ABC zigzag.

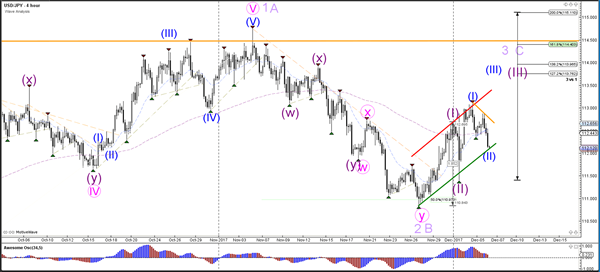

Currency pair USD/JPY

The USD/JPY is testing the bottom / support (green) of the uptrend channel. An impulsive bullish bounce could indicate that price is building a wave 2 (blue) whereas a sideways movement could mean a bear flag pattern and more downside.

The USD/JPY will need to bounce at support first of all and later on break above the resistance (red/orange) to confirm the wave 3 pattern (purple). For the moment, price could have built a bearish ABC pattern within wave 2 (blue) and the Fibonacci levels and the support trend line could stop price from falling.

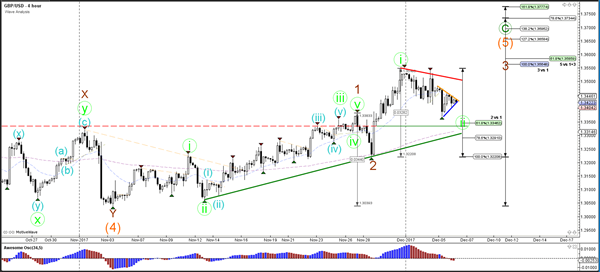

Currency pair GBP/USD

The GBP/USD is building a bearish correction which is probablypart of a larger a wave 1-2 (green).This is invalidated if price breaks below the 100% Fibonacci level of wave 2 vs 1.

The GBP/USD is showing a triangle chart pattern (orange/blue). A break below or above the triangle could indicate a potential breakout.

Market Update – Asian Session: BOJ Masai Warns Of Downside Risks To Inflation

Headlines/Economic Data

General Trend: Asian equities trade generally lower after US declines

Profit warning from Samsung Heavy weighs on shipbuilders

Volatility seen in shares of tech name Tencent

NY Copper +0.6% (declined over 3% on prior session); Copper futures higher

Japan

Nikkei 225 opened -0.4%; closed

TOPIX Iron & Steel Index -2% (gained over 1.4% during prior session)

Financials trade generally lower: TOPIX Securities index -2%

Toshiba +2.5% (expected to hold settlement talks with Western Digital)

BoJ Masai: Vital to show ‘determination’ to create stable prices; risks tilted to downside for prices, think downside risks to prices are 'big'

MUFJ-MS sees Japan stocks heading for a "boom phase"

(US) Japan govt plans to raise tax on heated tobacco to 80% of conventional tobacco tax over 5-yrs - Japan press

Looking Ahead: 30-year JGB auction expected on Thursday

Korea

Kospi opened flat

Korean Won (KRW) -0.5%

South Korea Finance Ministry: President Moon to visit China next week (Dec 13-16th)

North Korea said to be showing some interest in Russia diplomatic initiative – press

US to send B-1B bombers to South Korea for drills today - Korean press

South Korea govt think tank (KDI) sees 2018 GDP at 2.9%, accommodative policy is needed

Bank of Korea (BOK) sells KRW2.6T in 2-yr monetary stabilization bonds at 2.06%

South Korea raises corporate tax rate to 25% for the highest earning companies (as expected) from 22% - Korean press

South Korea parliament approves KRW428.9T budget for 2018 (as expected) - South Korea press

010140.KR Guides FY17 Op loss KRW490B; Planning to sell KRW1.5T in shares, opens down over 20%

005930.KR Begins mass producing flash memory for smartphones with doubled capacity to 512 GB from 256 GB – Nikkei; -1%

China/Hong Kong

Markets open mixed: Hang Seng flat, Shanghai -0.4%

Bourses later move lower: Hang Seng Materials Index 3.5%; Shanghai Copper opened down over 3% (below 200-day MA)

Hang Seng Consumer Goods index -1.9% amid weakness in auto sector (Geely -6%, BYD -4%)

Hang Seng Information Technology Index -1.5%; Volatility seen in shares of Tencent

Hang Seng Property/Construction Index -1.2%, Financial Index -1.1%

(CN) Moody’s: Expects China PBOC to leave policy unchanged in 2018

PBoC skips open market operation for 4th straight session, elects to conduct 1-year MLF operation

(CN) PBOC LENDS CNY188B V CNY404B PRIOR IN MEDIUM-TERM LENDING FACILITY (MLF) OPERATION; OFFERS 1-YEAR LOANS AT 3.20% V 3.20% PRIOR

(CN) PBOC Open Market Operations (OMO): skips v skips prior (4th consecutive skip)

(CN) China Financial News: PBOC expected to conduct MLF lending one more time this month and ahead of Lunar New Year 2018

(HK) Moody's: Raises Hong Kong Banking System outlook to Stable from Negative

(CN) China MoF sells 1-yr upsized bonds at 3.6975% v 3.62%e, bid-to-cover 1.72x; 10-yr upsized bonds at 3.8396% v 3.85%e, bid-to-cover 2.82x

(CN) PBoC sets yuan reference rate at 6.6163 v 6.6113 prior (8th consecutive weaker setting, longest run since Nov 2016)

(CN) China 2018 GDP growth seen at 6.7% ahead of Central Economic Work [**Note: On Dec 4th, the State Info Center (China think tank) recommended a 2018 GDP growth target of around 6.5%]

(CN) China Vice Premier Wang Yang: World economy is recovering

(CN) China researcher sees China GDP at 6.3% in 3-yrs - China Securities Journal

(CN) China Banking Regulatory Commission (CBRC) vice chairman Wang Zhaoxing: Govt will further regulate financial markets and get tough on illegal financial activities

(CN) PBOC deputy Gov Pan Gong-sheng: China authorities were right to rein in cryptocurrencies

(CN) US Commerce Dept to collect duties up to 265.79% on China origin steel imported from Vietnam

(CN) China MoF sells 1-yr upsized bonds at 3.6975% v 3.62%e, bid-to-cover 1.72x; 10-yr upsized bonds at 3.8396% v 3.85%e, bid-to-cover 2.82x

China's HNA seeks extension related to CNY3B loan linked to acquisition of Gategroup – financial press

Looking Ahead: China trade data released on Friday

Australia/New Zealand

ASX 200 opened flat, later moved lower; close: -0.4%

ASX 200 Resources Index -1.5% (tracks Tuesday’s decline in copper prices)

Aussie and Australian bond yields decline after GDP data

(AU) AUSTRALIA Q3 GDP Q/Q: 0.6% V 0.7%E; Y/Y: 2.8% V 3.0%E; Prior GDP q/q revised higher from 0.8% to 0.9%

(AU) Australia Treasurer Morrison: Australia having strongest job growth in 40-yrs; Q3 GDP still places near the "top of the pack" for growth compared with other wealthy nations and was driven by investment

Amazon said its first day launch orders in Australia were ‘higher than any other launch day’; ASX 200 Consumer Discretionary Index +0.2%

(AU) Morgan Stanley comments on Amazon’s launch Australia: Says range of products offered is relatively weak, pricing of certain products higher vs some competitors – US financial press

(AU) Australia sells A$900M v A$900M indicated in 2.25% May 2028 Bonds, avg yield 2.5846%, bid to cover 2.59x

(AU) Australia Nov Port Hedland Iron Ore Exports 41.3M tons v 41.0M m/m, iron ore exports to China 35.2Mt v 35.2Mt m/m

(NZ) Fonterra Global Dairy Trade Auction: Dairy Trade price index: +0.4% v -3.4% prior

(NZ) New Zealand Ministry recommends Commerce Commission study into fuel market

SCL.NZ Guides FY17 EBITDA to be at the upper end of NZ$55-62M; Guides initial FY18 NZ$58-65M; +6%

AKP.AU Gives integration stage update; currently forecasts delivery time of wafers meeting required specifications for latter part of Q1 2018; -13%

Looking Ahead: Australia Oct Trade Balance due for release on Thursday

Other Asia

Moody’s: Sees 3 Fed rate hikes in 2018; Some Asian central banks to raise rates along with Fed; India may be among central banks that cut rates in 2018.

(IN) Reserve Bank of India (RBI) due to release rate decision at 4 GMT (no changes expected)

(MY) Malaysia Oct Trade Balance (MYR): 10.6B v 9.8Be; Exports y/y: 18.9% v 17.3%e

(MY) Malaysia sells 2027 bonds; avg yield 3.946%

(ID) Indonesia Central Bank Assistant Gov Waluyo: Won’t change policy rate if Rupiah and inflation within target; No reason to change rate at this time

North America

US equity markets ended broadly lower: Dow -0.5%, S&P500 -0.4%, Nasdaq -0.2%, Russell 2000 -1%

S&P500 Utilities Sector -1.3%, Industrials -0.9%; Technology flat

Homebuilder Toll Brothers declined over 7% after reporting quarterly results

UPS: Spokesperson: transit times for an unspecified number of deliveries have been extended by a day or two due to Cyber Monday sales, expects to have things back to normal by midweek

M&A: Tronox: FTC challenges proposed merger of Tronox and Ti02 business of Cristal

(US) Senate Banking Committee advances Jerome Powell nomination for Fed Chair by 22-1 vote – press; Nomination now heads to full Senate for confirmation vote

(US) White House Press Sec Sanders: reports regarding subpoena sent to Deutsche Bank are totally false; still believe special counsel probe will wrap up soon

(US) House Rules Committee Chair Sessions (R-TX): House plans vote Weds on short-term funding bill through Dec 22nd

(US) Weekly API Oil Inventories: Crude: -5.5M v +1.8M prior

UAE Oil Min Mazrouei: Sees crude demand increasing on cold winter; Sees 2018 oil demand at least at 2017 level

Bank of America CEO: Trading Rev seen down 15% this quarter y/y

Looking Ahead: US Nov ADP Employment Change, DoE Weekly Crude Inventories and Bank of Canada rate decision due for Wednesday

Europe

(UK) EU official: UK must provide proposal on separation by Weds – press; If EU doesn't receive a proposal this week, EU won't have sufficient time to get ready for the beginning of talks on future trade agreement at the mid-Dec meeting

(UK) Govt spokesperson: cabinet supports Prime Min May in making progress in Brexit talks; Does not believe PM May and DUP Leader Foster have not spoken yet

(UK) DUP Leader Foster: told PM May yesterday that DUP would not support deal unless text of Brexit agreement was changed

(UK) Ireland PM Varadkar: a huge amount of work remains on seeking border deal with UK; the ball is in London's court; very much regrets failure to reach accord; We must hold firm on the border issue

(UK) Said to have been an Islamist suicide plot to assassinate PM May, which was foiled - Sky News

M&A: Nestle: Confirmed agreement to acquire Atrium Innovations for $2.3B

Levels as of 01:00ET

Nikkei225 -2.0%, Hang Seng -1.7%; Shanghai Composite -1.0%; ASX200 -0.4%, Kospi -1.1%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.5%, Dax -0.2%; FTSE100 -0.3%

EUR 1.1848-1.1816; JPY 112.63-112.10; AUD 0.7636-0.7572;NZD 0.6904-0.6871

Feb Gold +0.3% at $1,269/oz; Jan Crude Oil -0.4% at $57.39/brl; Mar Copper +0.6% at $2.97/lb