Sample Category Title

NZD/CAD 1H Chart: Channel Up Prevails

A descending channel has confined NZD/CAD since late August. The latest test of its bottom boundary occurred on November 17 when the New Zealand Dollar reversed to the upside and formed a channel up. In line with this pattern, the pair should still appreciate up to the 0.89 area where the upper boundaries of this pattern and the senior one are located. However, the Kiwi faces a significant resistance cluster set by the weekly and monthly PPs and the 200-hour SMA in the 0.8780/0.8800 territory. As suggested by technical indicators, this might mark a point of reversal. In this case, the Kiwi is likely to breach the channel up and continue trading in a newly-formed one-day channel down towards the bottom boundary of the senior pattern. The nearest support of significance is the 55-hour SMA at 0.8723; the weekly and monthly S1s are likewise located nearby circa 0.8670.

Trade Idea: GBP/USD – Exit long entered at 1.3410

GBP/USD – 1.3390

Original strategy :

Bought at 1.3410, Target: 1.3600, Stop: 1.3350

Position: - Long at 1.3410

Target: - 1.3600

Stop: - 1.3350

New strategy :

Exit long entered at 1.3410,

Position: - Long at 1.3410

Target: -

Stop:-

Although cable rebounded from 1.3371, as renewed selling interest emerged at 1.3461 and sterling has slipped again, suggesting near term downside risk remains for the retreat from 1.3550 (last week’s high) to bring retracement of recent rise, hence weakness to 1.3330-35, then 1.3300 cannot be ruled out, however, reckon downside would be limited to 1.3250-60 and previous support at 1.3221 should remain intact, bring rebound later.

In view of this, would be prudent to exit long entered at 1.3410 and stand aside in the meantime. Only above said resistance at 1.3461 would suggest low is possibly formed, bring rebound to 1.3500, break there would signal the pullback from 1.3550 has ended and revive bullishness for retest of this level first. Looking ahead, a break of 1.3550 would extend the rise from 1.3027 low to 1.3595-00, however, reckon recent high at 1.3658 (Sept high) would hold from here due to near term overbought condition, bring retreat later. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

AUD/USD: Australian Gross Domestic Product

The Aussie fell sharply against the US Dollar on the dissapointing GDP report this morning. The AUD/USD lost initially 29 base points or 0.38% to continue consolidation in the 0.7585 area.

Australian economy expanded at a weaker-than-anticipated pace, as household spending grew at the slowest pace since the financial crisis in 2008, reinforcing the possibility of the Reserve Bank of Australia keeping its key interest rate unchanged for a longer period of time. The Australian Bureau of Statistics reported that the country's gross domestic product rose 0.6% in the third quarter, following an upwardly revised 0.9% in the prior period, with the largest downward contribution coming from a weak consumer spending affected by the insufficient pay growth.

EUR/USD: ISM Non-Manufacturing PMI

The US Dollar was seen trading slightly higher against the European single currency, as the US economic reports revealed weaker than estimated results on Tuesday. The EUR/USD currency pair fell 6 base points, where the Euro was strong enough to return in the 1.1835 area.

The Institute for Supply Management stated that its non-manufacturing PMI for the US fell to 57.4 in November, compared with 60.1 in October, suggesting that the services sector’s growth slowed due to moderation in both export and new orders. Another release showed that the country’s trade deficit widened to a nine-month high in the same month amid higher oil prices and lingering deficits with Mexico and Canada, despite the strong increase of exports to the both countries.

USD/CAD: Canadian Trade Balance

The Greenback rebounded from a weekly low against the Loonie, as the report showed that the Canadian trade deficit shrunk in October. The USD/CAD currency pair fell 10 base points to the 1.2634 mark, but succumbed bulls to move the exchange rate higher to the 1.2700 area.

Canadian export sector revealed unexpected signs of strengthening in October, as it marked the first raise since May on increased shipment to the US, while imports kept disappointing. Statistics Canada said that the countryš trade deficit fell to the lowest level in five months of C$1.5B from C$3.4B in the prior month. Strong data came late to influence the Bank of Canada’s monetary policy decision today, which is widely expected to keep interest rate unchanged.

GBP/USD: UK Services PMI

The Sterling was little changed against the US Dollar on the UK Services PMI data, though the report managed to sustain the exchange rate above the 1.3400 level. The GBP/USD rose 15 base points or 0.11% to make further attempts to overcome 1.3440.

The UK economy suffered by the end of 2017, compared to the Euro zone’s strong recovery, as the effects of Brexit vote kept weighing on businesses and shoppers. Markit said that country’s services PMI dropped to 53.8 in the month of November. The businesses within the industry faced double impact, as costs increased mainly due to the lack of skilled labour, while inflation growth continued to squeeze household incomes and their willingness to spend.

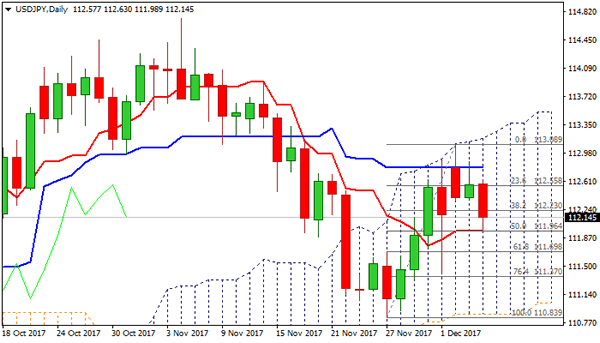

Technical Outlook: USDJPY – Break Below 112.00 Support Zone To Confirm Reversal

The pair holds in red on Wednesday and tested pivotal support at 111.96 (daily Tenkan-sen) after strong bearish signal was generated on multiple strong upside rejections under daily cloud top.

Confirmation of reversal needs break below Tenkan-sen which would expose supports at 111.69 (200SMA / Fibo 61.8% of 110.83/113.08) and 111.27 (76.4% retracement).

Corrective upticks are expected to hold below daily Kijun-sen (112.78) and keep near-term bearish bias in play.

Res: 112.63, 112.78, 113.17, 113.24

Sup: 111.96, 111.69, 111.57, 111.27

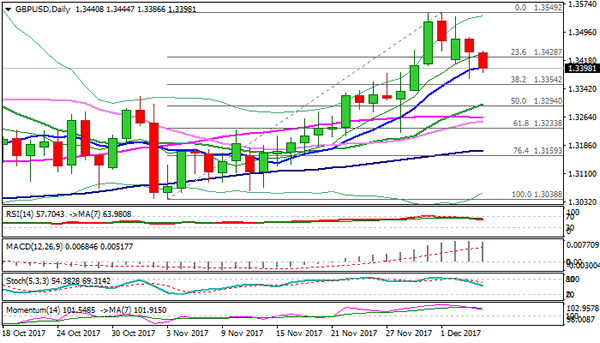

Technical Outlook: GBPUSD – Downside Remains At Risk On Political Uncertainty

Cable maintains weak tone on Wednesday, weighed by Brexit concerns and probes through cracked rising 10SMA (1.3400).

Tuesday dip to 1.3370 was short-lived, marking strong downside rejection on daily close well above 10SMA which marks initial support. However, political uncertainty keeps the pound under pressure and risk extension of pullback from 1.3549 peak, despite bullishly aligned daily studies, as twisting daily cloud continues to attract.

Firm break below 10SMA would open next pivotal support at 1.3354 (Fibo 38.2% of 1.3038/1.3549 upleg) with extended correction expected to find support at 20SMA (1.3300) and keep overall bulls in play for fresh attempts higher.

Close below 20SMA will be strong bearish signal.

Res: 1.3447, 1.3481, 1.3500, 1.3549

Sup: 1.3386, 1.3370, 1.3354, 1.3294

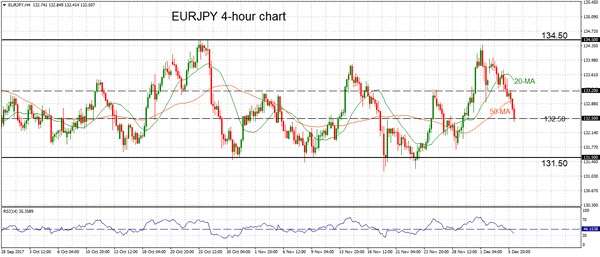

EURJPY Bearish Short-Term Bias After Reversing Near Top Of Medium-Term Range

EURJPY continues to trade in its 3-month range but in the short-term, the bias is bearish after the pair failed to break out of the top of the range at 134.50. There is limited upside in the near term and risk remains tilted to the downside as the RSI is bearish.

Looking at the 4-hour chart, the market became overextended before reversing, as indicated by the RSI reaching over 70. The drop from 134.47 resulted in falling below the 20 and 50-period moving averages into the 132 handle. Prices have stabilized near 132.50 but with a bearish RSI, the odds are high for continued downside momentum.

A daily close below 132.50 would yield significant additional weakness to set EURJPY on the path towards 131.50. Breaking the base of the medium-term range and below 131 would shift the longer-term trend to a more bearish one.

In the short term, a deeper pullback towards 132.50 is possible while RSI is bearish and the 20-period MA is falling. The medium-term range is expected to remain intact between 131.50-134.50.

Aussie Sinks On GDP Miss, BoC Decides On Rates

Here are the latest developments in global markets:

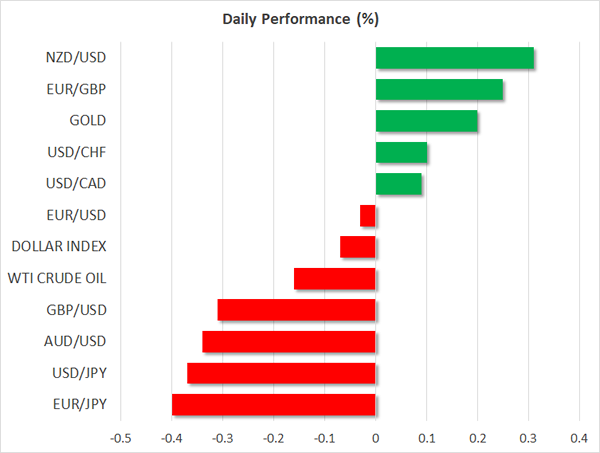

FOREX: The dollar weakened against its major counterparts on Wednesday as unless a deal is reached the government will run out of funds on Friday. This is spreading fears of a partial government shutdown. The pound was under pressure amid weakening hopes for progress on Brexit talks and on reports of a failed plan to kill the UK Prime Minister. The aussie tumbled in the wake of disappointing GDP growth figures and the kiwi surged to a one-week high.

STOCKS: There was a broad selloff in Asian equities following yesterday’s declines on Wall Street; the Nikkei 225 closed 2.0% lower and the Hang Seng was last down by 1.8%. Euro Stoxx 50 futures traded 0.8% lower at 0747 GMT. Dow futures were lower by 0.3%, S&P 500 contracts were down by 0.2% and Nasdaq 100 equivalents traded down by 0.4%.

COMMODITIES: Oil prices retreated after the API weekly report showed gasoline and distillate inventories in the US climbed unexpectedly. WTI crude fell by 0.33% to $57.43 per barrel and Brent declined by 0.24% to $62.70. Gold rose by 0.20% on the day to $1,268.30 per ounce but remained near four-month low levels.

Major movers: Dollar struggles as government budget deadline looms; aussie back to $0.75

US government agencies will run out of funds on Friday midnight unless a deal is reached, with Republicans postponing the planned House vote on the temporary budget – aiming to finance the government until December 22 – from Wednesday to Thursday to solve disputes with conservatives who desire a tighter budget. However, Republicans are said to push harder to pass the bill this week as they are also under pressure to address other issues by the year-end, including the tax overhaul bill. The dollar breached slightly below 112 yen, approaching a one-week low of 111.98 (-0.44%). Dollar/swissie retreated to a session low of 0.9856 but managed to erase losses afterwards, rising to 0.9870 and dollar/loonie retreated to 1.2700 (0.11%). The dollar index was steady at 93.31.

The euro remained flat around $1.1828 despite German factory orders in October surprising to the upside, while the pound was on a downtrend towards to $1.3400 (-0.33%).

Looking at the antipodean currencies, the aussie took a knock versus the greenback after the readings on Australian GDP growth indicated that the economy expanded by 2.8% y/y in the third quarter, below the forecasts of 3.0% but far above the previous mark of 1.8%. Household spending slowed down as well, narrowing to a multi-year low of 0.2% from 0.9% (upwardly revised from 0.8%) as heavily indebted consumers have to come tom terms with sluggish wage grwoth. Aussie/dollar tumbled close to a one-week low of 0.7570 (-0.34).

Its New Zealand cousin surged to a one-week high of $0.6915, being the best performer of the Asian session (+0.35%).

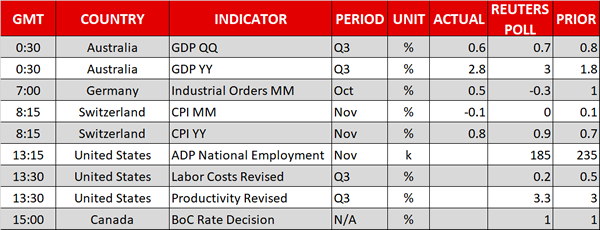

Day ahead: Bank of Canada rate decision, US ADP jobs report and EIA data the main focus

In a relatively quiet day in terms of releases, the November ADP national employment report out of the US will be released at 1315 GMT. This pertains to positions added to the economy by the private sector and is often perceived as giving an indication on the nonfarm payrolls report (due on Friday). Analysts expect the ADP report to show an addition of 185k positions. This compares to 235k in October. Shortly after (at 1330 GMT), data on third quarter US nonfarm productivity are due.

The Bank of Canada today completes its meeting on monetary policy with its decision on rates as well as the bank’s monetary policy statement being made public at 1500 GMT. No change in interest rates as expected though still the event will be closely watched for any market sensitive comments having the capacity to steer dollar/loonie as well as other loonie pairs.

The EIA’s weekly report on, among others, US crude and gasoline stocks will be released at 1530 GMT. Oil prices will be in focus with the release often causing volatility in prices.

Beyond data, deliberations on tax reform as well as on averting a government shutdown are continuing in the US, while in Europe, the European Commission College of Commissioners will be assessing whether sufficient progress has been made on Brexit discussions that would justify moving negotiations to the next step – that of the eventual future relationship between Britain and the EU.

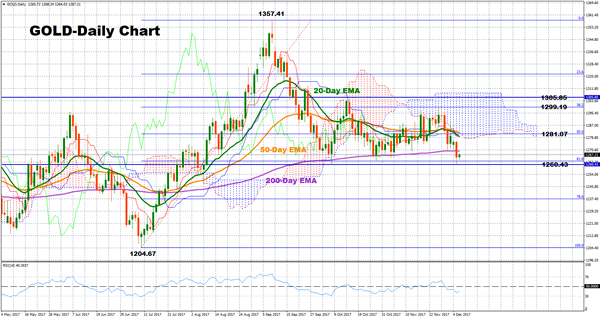

Technical Analysis: Gold breaks below 200-day EMA; neutral short-term bias

Gold has slid below the 200-day exponential moving average line (EMA) and is close to exiting the range-bound market between 1260.43 and 1305.85.

The neutral bias though remains intact in the short-term as the pair continues trading within the aforementioned range. Adding to this, the RSI has been in large part moving sideways in recent days.

However, if the ADP report out of the US beats expectations pushing the greenback higher, dollar-denominated gold could head down, reaching the lower bound of the range at 1260.43, which is not far below the 61.8% Fibonacci retracement (1262.94) of the upleg from 1204.67 to 1357.41. Further decreases could also meet the 1250 and the 1240 key-levels.

Alternatively, an upside move could face strong resistance at the 50% Fibonacci at 1281.07 before the focus shifts to a previous top at 1299.19, which is also the 38.2% Fibonacci of the previously mentioned upleg.