Sample Category Title

Brexit Bears Lead Pound; Stocks Continue Declining; BOC Rate Decision Pending

Here are the latest developments in global markets:

Forex: Sterling stretched toward a fresh one-week low of 1.3360 (-0.61%) as fears over a potential impasse in Brexit talks, which could postpone negotiations until February and therefore scale back business investments, lingered in the background. The dollar steadied versus the yen near one-week lows as concerns over a government shutdown offset positive sentiment related to the delivery of tax reforms. The euro was trading flat against the greenback at 1.1824, while versus sterling it managed to reverse earlier losses, picking up to a session high of 0.8852 (+0.47%). The aussie was moving sideways around one-week lows of 0.7580 after a miss in GDP growth readings (-0.21%). Dollar/loonie inched down to 1.2667 (-0.17%).

Stocks: A strong selloff in tech shares and basic metals continued to lead the drag in European stocks on Wednesday. The benchmark STOXX 600 was down by 0.56% at 1130GMT with all sectors trading down. The Spanish IBEX 35 declined by 0.93%, the German DAX 30 lost 0.92% and the French CAC 40 fell by 0.40%. The British FTSE 100 rebounded on the back of a weaker pound.

Commodities: Oil prices continued to fall as markets perceived the rise in US refinery inventories in the API weekly report as a weakness in demand. WTI crude tumbled by 1.27% to $56.90 per barrel and Brent slipped by 1.0% to $62.18. Gold was steady at $1,267.50 per ounce, trading near four-month low levels.

Day ahead: ADP employment might slow; BOC rates expected steady

The release of the ADP nonfarm employment report out of the US and a final settling of interest rates for this year by the Bank of Canada are expected to be the main highlights on Wednesday.

At 1315GMT, the US-based ADP Research Institute will publish readings on nonfarm employment, indicating the number of jobs added to the private sector in November. The report, which provides a snapshot of US nonfarm payrolls due on Friday, is expected to show a smaller increase of 185,000 positions compared to a six-month high of 235,000 seen in October.

Next in focus would be the Bank of Canada's rate announcement at 1500GMT. Despite November's impressive employment readings, the central bank will likely keep rates on hold as the annualized GDP growth seems to be slowing down, while consumers are struggling to meet their debt obligations as wage growth remains subdued. However, the monetary policy statement following the decision could bring some volatility to the loonie if policymakers use a different language to express their views on the economic outlook.

In energy markets, investors will look through the EIA report on US crude oil inventories. According to forecasts, crude inventories will drop by 3.40 million barrels in the week ending December 1 compared to a fall of 3.42 million in the preceding week. On the other hand, gasoline inventories and distillate stocks are anticipated to increase though not by much.

CAC Dips as Financial Stocks Falter

The CAC is in red territory on Wednesday. Currently, the index is at 5352.00, down 0.45% on the day. On the release front, the sole eurozone release is Retail PMI, which improved to 52.4. This marked a seven-month high. On Thursday, France will release Trade Balance, with the trade deficit expected to remain unchanged at EUR 4.7 billion.

On Tuesday, French Final Services PMI looked sharp, punching above the symbolic 60-point level. This marked the indicator's highest level since May 2011. The strong reading is indicative of strong expansion, as the service sector has been buoyed by strong customer demand and strong economic conditions. French service providers remain optimistic that activity in the sector will increase in the upcoming 12-month period. The French economy has rebounded in impressive fashion in 2017, and looks to wrap up the year on firm footing, as a strong manufacturing sector has triggered improved job growth.

The eurozone economy has enjoyed a strong rebound in 2017, marked by steady growth and lower unemployment. The ECB has projected GDP of 2.2% and inflation of 1.2% for 2017. The economic recovery pushed the ECB into action, which tapered its asset purchase program, although it did extend the program until September 2018. Still, the cautious ECB said on Wednesday that it was concerned about "increased risk-taking behavior in global financial markets" as this could lead to sharp asset price corrections. The ECB is also keeping its eye on political uncertainty in Europe, notably the deadlocked Brexit negotiations and the political vacuum in Germany. In the meantime, European stock markets remain at high levels and the euro is enjoying the view from the 1.18 level.

GBPUSD: Weakens On More Bear Threats

GBPUSD: The pair failed to follow through lower on Wednesday causing to decline further. This leaves GBPUSD weak and vulnerable to the downside with eyes on the 1.3300 zone. Support lies at the 1.3350 level where a break will turn attention to the 1.3200 level. Further down, support lies at the 1.3150 level. Below here will set the stage for more weakness towards the 1.3100 level. Conversely, resistance stands at the 1.3400 levels with a turn above here allowing more strength to build up towards the 1.3450 level. Further out, resistance resides at the 1.3500 level followed by the 1.3550 level. On the whole, GBPUSD looks to decline further.

GOLD Retest of Cont. SHS Bearish Pattern is Possible

Gold might be going through a revaluation phase, where Cryptocurrencies like Bitcoin are now rivaling it as the preferred risk-off asset or when such inflation risks persist. This crypto hype has potentially weakened some demand for Gold. Furthermore, there is the possibility that the US Fed may hike rates three times over the next 12 months, and this shifts further investments from Gold into Bonds.

Technically Gold is showing Bearish SHS continuation pattern (Head and Shoulders at support) and the price might retest a neckline that is a part of POC zone. The POC 1271-1274.50 (Bearish SHS neckline, order block, EMA89, D H4, 78.6) could potentially reject the price towards 1264.23 , 1261.28 and 1256.87. Break of 1281.80 and 4h close above it, might possibly negate bearish scenario.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

DAX Slides As Banking, Tech Stocks See Red

The DAX index has posted sharp losses in the Wednesday session. Currently, the DAX is at 12,939.50, down 0.84% on the day. On the release front, German and European indicators were positive, but this was not enough to keep the DAX from moving into red territory. German Factory Orders gained 0.5%, above the estimate of -0.2%. There was more positive news, as Eurozone Retail PMI improved to 52.4 points in November, its highest level since June. On Thursday, German releases Industrial Production and ECB President Mario Draghi holds a press conference hosted by the ECB.

There is little to cheer about on the Frankfurt exchange on Wednesday, as almost all of the DAX listings are in red territory. Financial stocks are down sharply, with Commerzbank and Deutsche Bank posting losses of 1.82% and 1.60% respectively. Technology stocks are also down, led by Infineon Technologies, which has declined 1.28% on the day.

The eurozone has enjoyed a strong 2017, marked by steady growth and lower unemployment. The ECB has projected GDP of 2.2% in 2017 and inflation of 1.2%. Things are so good that the ECB finally acted and tapered its asset purchase program, although it did extend the program until September 2018. Still, the cautious ECB said on Wednesday that it was concerned about increased risk-taking behavior in global financial markets” as this could lead to sharp asset price corrections. The ECB is also keeping its eye on political uncertainty in Europe, notably the deadlocked Brexit negotiations and the political vacuum in Germany. In the meantime, European stock markets remain at high levels and the euro is enjoying the view from the 1.18 level.

Euro Shrugs Off Sharp German Industrial Report

The euro has inched lower in the Wednesday session. Currently, EUR/USD is trading at 1.1814, down 0.10% on the day. On the release front, German Factory Orders gained 0.5%, above the estimate of -0.2%. There was more positive news, as Eurozone Retail PMI improved to 52.4 points in November, its highest level since June. In the US, today's highlight is ADP Nonfarm Employment Change, which is expected to slow to 189 thousand. On Thursday, German releases Industrial Production and ECB President Mario Draghi holds a press conference hosted by the ECB. The US will release unemployment claims.

The eurozone has enjoyed a strong 2017, marked by steady growth and lower unemployment. The ECB has projected GDP of 2.2% in 2017 and inflation of 1.2%. Things are so good that the ECB finally acted and tapered its asset purchase program, although it did extend the program until September 2018. Still, the cautious ECB said on Wednesday that it was concerned about increased risk-taking behavior in global financial markets” as this could lead to sharp asset price corrections. The ECB is also keeping its eye on political uncertainty in Europe, notably the deadlocked Brexit negotiations and the political vacuum in Germany. In the meantime, European stock markets remain at high levels and the euro is enjoying the view from the 1.18 level.

Will we see a slowdown in the US labor market? The markets are predicting that ADP Nonfarm Employment Change will slow to 189 thousand, compared to 235 thousand in the previous release. Investors are, of course, much more interested in the official nonfarm employment change release on Friday. The key release is expected to slow to 200 thousand, down from 261 thousand in the previous release. If nonfarm payrolls is weaker than expected, the dollar could lose ground against the euro and other rivals.

Loonie Strengthens Ahead Of January Rate Hike

Loonie strengthens ahead of January rate hike

Later today the Bank of Canada (BoC) will announce its December interest-rate decision: we think it will remain unchanged, but a climb is likely in January. USD/CAD has tracked front-end yield spreads tightening in the last six months. With a US Federal Reserve December rate hike priced-in and a hawkish BoC, a USD/CAD reversal from 1.29 resistance presages a deeper correction towards 1.2566 (100-day moving average).

Q3 economic data surprised to the upside. Labour markets exceeded expectations, demand was strong, and the prospect of US tax reform could accelerate Canadian growth and reduce risk of the North American Free Trade Agreement falling apart. The BoC is likely to hike rates steadily, in a gradual process.

Brazilian real to weaken

As Brazil’s central bank is expected to drop its prime lending rate to an all-time low of 7%, and demand for the USD rises with the US Federal Reserve’s impending rate hike, the real should continue to weaken against the greenback. Since the start of the year, the USD/BRL has been trading between 3.1 and 3.4. Brazilian rates have fallen by half in the past year, and 2018 might see further cuts. Capital outflows are likely to accelerate, as the interest-differential to the USA narrows.

The interest rate cut is driven by inflation, which surprisingly stands way below the official target. Banco Central do Brasil is targeting inflation at 3-6%, yet consumer prices have dived from double digit to less than 2% growth. Inflation for November is expected to print at 2.88% annually.

CRUDE OIL Losing Steam

Crude oil continues its consolidation phase and should not challenge the 60-dollar level. Expected to show continued sideways move. Support is given at a distance at 54.81 (14/11/2017 low)

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

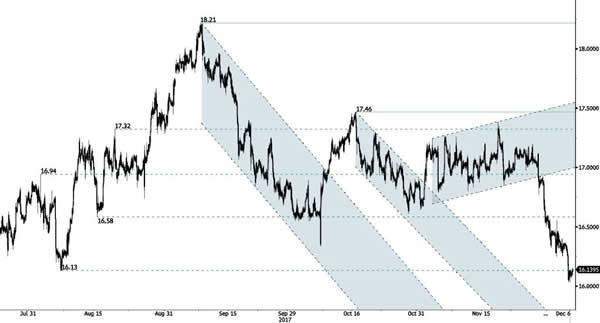

SILVER Collapsing

Silver is heading lower. Hourly support can be found at 16.13 (07/08/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Expected to keep pushing lower.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

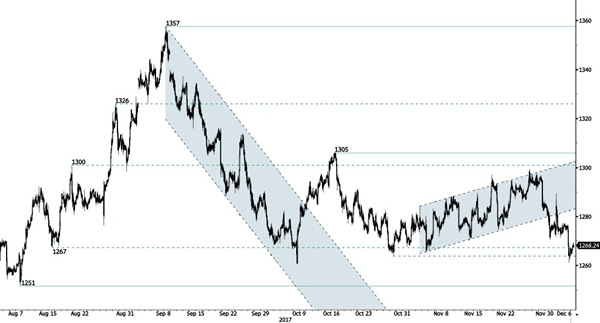

GOLD Ready For Further Downside

Gold is pushing lower. The technical structure confirms the end of the consolidation phase. Support lies at a distance at 1251 (08/08/2017 high). Resistance is located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).