Sample Category Title

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7537; (P) 0.7584; (R1) 0.7609; More...

AUD/USD's break of 0.7550 minor support argues that consolidation from 0.7531 has completed with three waves up to 0.7653 already. Intraday bias is back on the downside. Break of 0.7531 low will resume whole fall from 0.8124 and target next key cluster level at 0.7322/8. In any case, outlook will remain bearish as long as 0.7729 resistance holds and further fall is expected.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8033). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

Dollar Broadly Higher But Outlook Stays Mixed, CAD and AUD Weak

Dollar is trading broadly higher today as its shrugged off negative news. US President Donald Trump announced to recognize Jerusalem as Israel's capital could unsettle the region and triggered a dip in USD/JPY. But the pair quickly recovered as the impact faded. Markets are also ignoring the risk of partial government shut down after money runs out on December 8 if no spending bill is agreed by the Congress. Also, news regarding special counsel Robert Mueller subpoena on Trump's Deutsche Bank records was also disregarded by traders.

Nonetheless, it's hard to tell whether Dollar's rise this week is impulsive or corrective. AUD/USD's break of 0.7550 support today clearly suggests resumption of the fall from 0.8124 that started back in September. USD/CAD also looks completed the consolidation from 1.2916 and is ready to resume rise from 1.2061, also the September low. But the pull-backs in EUR/USD and GBP/USD are so far corrective looking. And the direction is USD/JPY is rather unclear since it failed to take out 114.49 key resistance back in November. Dollar traders would probably need to wait for non-farm payroll report tomorrow before making up their minds.

UK PM May's Brexit plan in chaos

In UK, Prime Minister Theresa May faced objections from Tory MPs on backing North Ireland DUP's opposition to the Brexit proposal on Irish border. Nineteen of them urged May not to allow Eurosceptic to "impose their own conditions" and that is "highly irresponsible" for someone to dictate the terms that could ruin a deal. Many business leaders are also dissatisfied that the Brexit negotiation is turning into chaos with time ticking. A CBI survey showed that 10% of companies have already started planning or a "no-deal" scenario on Brexit, and that would jump to as much as 60% by March. European Commission President Jean-Claude Juncker also expressed his concern that the UK government would collapse if the Brexit talk fails. May would be going back to Brussels later this week to secure support from EU team for approval to move on to trade talk during next EU summit on December 14/15.

BoJ Kuroda hails YCC as sustainable framework

BoJ Governor Haruhiko Kuroda hailed that the central bank's yield curve control is a "sustainable" framework, effective in pushing down long term interest rates. He pointed out that the program has ended deflation in the country and boosted the economy. Also, he noted that "BOJ's bond buying has been conducted in a smooth manner so far. The risk of us facing problems in terms of buying bonds will be small for the time being." Though, he added that "in accordance with changes in the economy, prices and financial conditions, we will consider where our short- and long-term rate targets should be to create an appropriate shape of the yield curve." Kuroda also reiterated that BoJ will continue to "persistently pursue powerful monetary easing".

CAD trading as second weakest on cautious BoC

Canadian Dollar is trading as the second weakest one for the week. The Loonie was sold off after BoC left interest rate unchanged at 1.00% and issued a "cautious statement". While acknowledging the strength in the employment situation, it warned of the slack in the labor market. While upgrading GDP growth forecast, it noted that it does not necessarily imply a narrower output gap. While admitting the policy rate would have to increase over time, it reiterated caution over any monetary decision. All in all, the central bank attempted to deliver a neutral to dovish message, so as not to cripple the recovery path - a lesson learnt after two consecutive rate hikes in July and September. More in BOC Kept Powder Dry, Warned of Slack Capacity Despite Falling Jobless Rate.

AUD staying weak as trade surplus shrank

Aussie follow closely as the third weakest for the week. Yesterday's GDP data miss showed weak household consumption and wage growth. Today's trade balance data is not giving any support neither. Trade surplus narrowed sharply to AUD 0.11b in October, missing expectation of AUD 1.41b. The result was driven by a steep -3% slide in exports and 2% jump in imports. Slump in iron ore sales, which tumbled -10% to AUD 7b contributed a large part to the contraction in exports. Coal exports also dropped -3% mom to AUD 4.3b.

IMF warns of China financial system risks

The International Monetary Fund published as assessment on financial system stability of China today. In the report, IMF warned that "the system's increasing complexity has sown financial stability risks." And it urged that "holding more capital would strengthen the banking system and bolster financial stability." Three tensions in the system are identified. The first one being surge in risk credits as debt-to-GDP ratio jumped from 180% in 2011 to 255.9% by Q2 of 2017. Second tension is that lending has shifted away from traditional banks to the shadow banking sector, the less-regulated part of the system. That makes supervision increasingly difficult. Moral hazard and excessive risk-taking is seen as the third with the expectation that the government with bail out state-owned enterprises and financial institutions in case of troubles. The People's Bank of China responded by disagreeing some points even though the recommendations are "highly relevant in the context of deepening financial reforms" in China.

Looking ahead

Swiss will release unemployment rate and foreign currency reserves in European session. Eurozone will release Q3 GDP final and German industrial production. Canada will release building permits and Ivey PMI. US will release jobless claims on a Thursday as usual.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7537; (P) 0.7584; (R1) 0.7609; More...

AUD/USD's break of 0.7550 minor support argues that consolidation from 0.7531 has completed with three waves up to 0.7653 already. Intraday bias is back on the downside. Break of 0.7531 low will resume whole fall from 0.8124 and target next key cluster level at 0.7322/8. In any case, outlook will remain bearish as long as 0.7729 resistance holds and further fall is expected.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8033). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Trade Balance Oct | 0.11B | 1.41B | 1.75B | 1.60B |

| 5:00 | JPY | Leading Index CI Oct P | 106.1 | 106.1 | 106.4 | |

| 6:45 | CHF | Unemployment Rate Nov | 3.10% | 3.00% | ||

| 7:00 | EUR | German Industrial Production M/M Oct | 1.00% | -1.60% | ||

| 8:00 | CHF | Foreign Currency Reserves (CHF) Nov | 745B | 742B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 F | 0.60% | 0.60% | ||

| 12:30 | USD | Challenger Job Cuts Y/Y Nov | -3.00% | |||

| 13:30 | CAD | Building Permits M/M Oct | 3.80% | |||

| 13:30 | USD | Initial Jobless Claims (DEC 02) | 241K | 238K | ||

| 15:00 | CAD | Ivey PMI Nov | 63.8 | |||

| 15:30 | USD | Natural Gas Storage | -33B |

Market Morning Briefing: Dollar-Yen Had Dropped Yesterday

STOCKS

Dow (24140.91, -0.16%) is falling as expected and could test 24000-23750 levels on the downside before again resuming its rise towards 24500.

Dax (12998.85, -0.38%) rose sharply from levels near 12900. Sideways consolidation is likely to continue for the week before the index decides on further direction.

Nikkei (22457.74, +1.27%) tested levels below 222000 and is trading higher just now. 22000 would be the initial target for Nikkei.

Thereafter, we need to see if it rises back towards 22800 or come off towards 21800. Preference is for the downside.

Shanghai (3277.73, -0.49%) is likely to test 3250-3200 levels while below 3300. Near term looks bearish.

Nifty (10044.10, -0.73%) fell yesterday too and closed at levels below 10050. While below 10050, the index could test 10000-9950 soon. Near to medium term view remains bearish.

Sensex (32597.18, -0.63%) has support at current levels and in case that holds, Sensex can move up towards 33000 or higher; else a sharp fall is in place and could extend to some more levels on the downside.

COMMODITIES

Surprising fall in crude prices seen overnight. News suggests that the fall came after a report by the American Petroleum Institute that showed a 9.2mln barrel rise in gasoline stocks in the week and an increase of 4.3mln barrels in inventories of distillates. This increase in the fuel stocks lead to a fall in crude prices as this points out to weak demand.

Brent (61.38) surprised by falling sharply, breaking below the support at 62 instead of moving higher towards 65-67 levels. If the current fall continues, it may extend towards 60 before rising back from there.

WTI (56.13) has also come off sharply but could face immediate support near 55.6 which if holds could prevent further fall just now. The fall in WTI has been exactly in line with our expectation, pulling down Brent also with itself.

Gold (1263.35) is down to 1260 support levels. The downside momentum seems to have gathered steam and while that dominates, Gold could well break below 1260 in the next few sessions. Failure to bounce back from current levels could take it down to 1250-1240 in the medium term.

Copper (2.9750) could trade within 2.95-3.05 region in the near term and is likely to remain stable just now. 2.90 is an important support on the downside.

FOREX

Dollar-Index (93.57) is well on its way to test resistance on the 3 day charts at 93.75-94.00, which is also seen as resistance on daily line charts. This could prove to be a crucial level, from where a corrective dip back towards 93 could be expected.

With a rising Dollar Index, Euro (1.18) is also moving swiftly towards support at 1.1775 on the 3 day candles. The same support is also seen on the daily and 3 day line charts, thereby indicating the possibility for a bounce, once 1.1775 is reached.

Dollar-Yen (112.42) had dropped yesterday due to a rise in Japanese 10 year yields, but with some consolidation in the same (see Interest Rates below), it has once again resumed its move towards levels near 113. A dip from near resistance levels (113.5) on the daily line chart could be seen with simultaneous dip of the Dollar Index (see Dollar Index above).

Pound (1.3382), as per our expectations, is close to testing support at 1.335 on the daily charts, from where a bounce could be seen, taking it back towards 1.35 in a week’s time.

Dollar Rupee (64.525) has stayed well above support at 64.20 and looks likely to rise to 64.60-64.80 in the next couple of sessions.

INTEREST RATES

The US yields are all bouncing from support just below current levels. The 5Yr (2.13%), the 10YR (2.35%) and the 30Yr (2.74%) are almost stable and could rise in the coming sessions.

The German-Japan 10Yr (0.23%) yield spread has fallen sharply and while it moves lower, it can pull down EUR-JPY to much lower levels in the near term.

The Japan-US 10Y (2.28%) has paused for now and unless it come down further, we cannot negate a scope of rising back to test 2.35%.

The German-US 10YR (-2.05%) is down again and looks bearish towards -2.08% in the near term.

Tricky Year End Markets

Tricky Year End Markets

It's not getting any easier deciphering the continually shifting market sentiment in the currency markets as the USD has gone bid across nearly every currency.While some are hanging their hat on possible year-end repatriation flows others suggest it has more to do with the year-end' turn” positioning. But the bottom line, currency traders are desperately seeking guidance.

It's a bit of a mixed bag for the USD in my view as all the good news seems to be priced in on the tax reform bounce, yet the Federal Reserve will hike this month and continue to do so next year. Speaking of which, discussions are heating up on the street about the Feds 2018 path and more so should we start baking in more reflation risk for the dollar given the boisterous US economy( employment) and the likely massive increase in US fiscal spending in 2018.But it remains a struggle being long dollars as the Fed debate will be tested out of the gate in 2018 as the market tries to decipher if we've priced in or yet to factor in the full extent of the Fed's normalisation cycle. Ultimately, it all boils down to whether the US data support or not.

ADP National Employment Report modestly beat forecasts and managed to underpin the US dollar, but ADP has been notoriously unreliable predicting non-farm payrolls. Relying on this forerunner is like looking for love in all the wrong places.

After an equity meltdown in Asia, with all the major indexes closing deep in the red, Europe and the US markets were far more temperate overnight.But don't get too complacent as risk aversion remains barefaced in bond markets with 10-year yields falling as U.S. President Donald Trump's recognition of Jerusalem is igniting a global political storm of protest and at the same time, Tax Reform uncertainty remains in the backdrop.

Asia equity investors found themselves standing in a sea of pain at yesterday's market close and are likely breathing a sigh of relief that both EU and US equity investors appear a bit more level-headed for the time being. Likewise for local currency markets which traded in the red. The regional equity market meltdowns triggered a wave of USD short covering on outflows, and as usual, $KRW was the most notable mover given the markets more massive weighted positioning. Besides the tax reform uncertainty narrative, and wobbly commodity markets, geopolitical risk wobbled after headlines scrolled that US B-1B bombers flew over the peninsula and that South Korea is set to build s unit of swarming drones in the latest Pyongyang staredown.

The Japanese Yen

The USDJPY is holding up well despite the lack of encouragement from ten-year yields but we did eventually test the 112 after the Nikkei closed in a sea of red.

Battle lines are forming with half the street looking to own JPY near term as the USD positivity from tax reform fades while dip buyer remains entrenched in the repatriation flow speculation and or the more aggressive Fed narrative.

I for one certainly prefer calling plays from the booth on this curious trade as far too much ambiguity persists, and choose to wait for Friday NFP and AHE data before playing the hand.

The Australian Dollar

The bears pounced on the weaker Aussie GDP data which showed no growth in consumption, complimented by no increase in income. The song remains the same in that Australian consumer are in a world of pain drowning in a sea of debt. Despite the better jobs growth, it's all moot without collecting a better paycheck. Any tactical long Aussie dollar asperations dealers were holding onto entering year-end vaporised on the data.

Energy markets

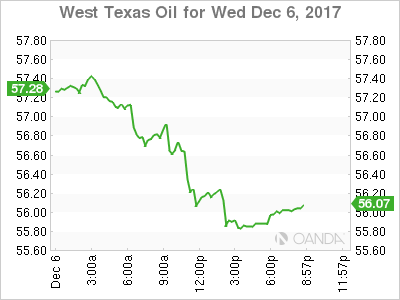

In the topsy-turvy oil markets. WTI prices cratered despite the Energy Information Administration reporting a 5.6 million barrel drop in weekly crude inventories. Indeed, traders were more concerned about the steep rise in gasoline inventories. WTI dropped from $57.19/barrel to below 56.00/barrel. Naturally, any gasoline supply shocker will stoke fears of lower demand and a sagging global economy. We saw this play out in other commodity markets when copper plummeted this week as the market infers any deluge of supply as a China wobble hence a global economic stumble.

Asia FX

The market should be able to pike up the pieces after yesterdays regional currency tumble.

Currency markets can be inexplicable at times and at this time of year, EM Asia FX tends to overshoot directionally.

The Korean Won

USDKRW gained 8 won yesterday on short covering, and the then nervous year-end corporate dollar demand stoked the fires. The regional risk sentiment is opening more stable this morning, but global investor sentiment remains pedestrian awaiting tax reform resolution, And this wary risk appetite should keep the KRW trading defensively but rangebound given medium-term bullish sentiment.

The Malaysia Ringgit

Despite the regional currency upheaval yesterday, the USDMYR remained relatively stable through the brawl. However, the Ringgit will likely trade steady to slightly weaker given the global investor's chary point of view as a sprinkle of risk-off sentiment is inducing some moderate headwinds to counter medium-term bullish sentiment.

Also, the fall in oil prices overnight is marginally weighing on MYR risk, but prices remain well above any significant negative trigger level.

On the data front, Malaysia exports came in better than anticipated printing at 18.9% (highest since August) while imports printed at 20.9% also better than expected. * (Reuters Eikon)

Usually, a positive export print would trigger a broader rally in the ringgit, but the market had already factored in the volatile crude oil component as Brent prices have been on the ups since September. So the Ringgit reaction to the export print was somewhat muted.

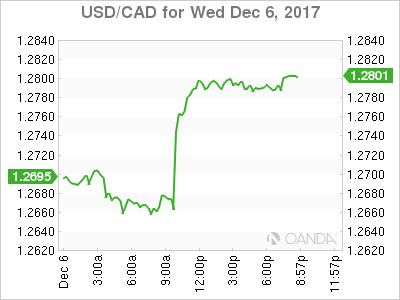

USD/CAD Canadian Dollar Drops After BoC Keeps Rate Unchanged Signals Caution

The Canadian dollar depreciated on Wednesday after a wait-and-see statement from the Bank of Canada (BoC) and falling oil prices. The BoC kept its benchmark interest rate unchanged at 1.00 percent. The central bank did mention a strong job growth and rising inflation signalling that the next move could be a rate hike, but the timing of the monetary policy decision is up in the air. The fate of the NAFTA negotiations is still uncertain and with such a large portion fo the economy tied to the outcome it would be premature for the BoC to speculate on something so outside its control, but very much a factor on its mandate.

The statement from the BoC acknowledges that higher rates will be required over time, but its commitment to caution was read by the market as dovish and the loonie paid the price. The Canadian economy has slowed down from its blistering pace in the second quarter, but still posted a decent 1.7 percent growth in GDP in the third quarter but with rising headwinds NAFTA and the fragility of the OPEC led production cut agreement Governor Poloz is keeping his options open until more unknowns become knowns until a decision had to be made. The most likely scenario from analysts is that NAFTA will continue even if a renegotiation does not bear meaningful fruit and oil prices will remain rangebound which would leave the BoC decision to rely on fundamental data.

The US Tax reform optimism remains as Congress and the Senate will work together to reconcile the two versions that have already passed. Geopolitics remain a big driver of market sentiment with the Trump Administration finally nearing a win since so many previous setbacks.

The USD/CAD gained 0.80 percent on Wednesday. The currency pair is trading at 1.2787 after the Bank of Canada (BoC) kept rates unchanged at 1.00 percent and communicated it would remain cautious going forward. The first of the employment release this week dropped with the publication of the ADP private payrolls report. US private employers added 190,000 jobs, 5,000 more than expected on the way to Friday’s U.S. non farm payrolls (NFP) which is forecasted to add 198,000 jobs in November.

The decision by the BoC to keep the benchmark rate at 1.00 percent and their dovish language was reflected in the drop in rate hike probabilities in the January meeting. The chances fell from 41 percent to 26 after the statement was released. The Canadian economic calendar has little on offer for the remainder of the week. Building permits and the purchasing mangers index (PMI) on Thursday will be highlights but the majority of market moves will be dictated by geopolitics (Washington and Brexit developments) and US employment data with an emphasis on wage growth ahead of the U.S. Federal Reserve December monetary policy meeting next week.

Oil prices fell 3 percent in the last 24 hours. The price of West Texas Intermediate is trading at 55.84 after the Energy Information Administration (EIA) weekly inventory data confirmed the API numbers. Crude stocks fell by more than expected at 5.6 million barrels, but it was the rise of gasoline inventory to 6.8 million barrels that sent a signal to the market that demand for energy might not be as strong as estimated. Despite the seasonal rise in gasoline inventories the data is pointing to a higher than average hoarding in the last five years.

With the Organization of the Petroleum Exporting Countries (OPEC) meeting in the rearview the softening of energy demand in the US knocked prices back down. The showdown between rising US production and the coordinated efforts of the OPEC and other major producers will continue in 2018 as prices are more stable, but the downside risk remains if there is no improvement for the global appetite for the black stuff.

Market events to watch this week:

Thursday, December 7

8:30am USD Unemployment Claims

11:00am EUR ECB President Draghi Speaks

Friday, December 8

4:30am GBP Manufacturing Production m/m

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

8:30am USD Unemployment Rate

Gold Ticks Lower As ADP Report Meets Forecast

Gold continues to lose ground this week. In Wednesday’s North American session, the spot price for an ounce of gold is $1264.42, down 0.14% on the day. On the release front, ADP Nonfarm Employment Change slowed to 190 thousand, just above the forecast of 189 thousand. On Thursday, the US releases unemployment claims.

The ADP nonfarm employment report came in as expected, with a gain of 190 thousand. Still, this was a soft reading compared to the previous release, which showed a gain of 235 thousand. Investors are, of course, much more interested in the official nonfarm employment change release, which takes place on Friday. Again, the markets are expecting a soft landing, with a forecast of 200 thousand, down from 261 thousand in the October release. If nonfarm payrolls, one of the most important indicators, is weaker than expected, the US dollar could lose ground. The US will also release a wage growth report on Friday, with the markets expecting a gain of 0.3%.

The markets are widely expecting the Federal Reserve to continue to raise rates in the near future, and this sentiment continues to weigh on gold prices. The odds on upcoming rate hikes continues to fluctuate. Currently, the CME has priced in December and January hikes at 90% and 88%, respectively. If the US economy continues to perform at its impressive pace into 2018, we could see the Fed raise rates up to three times next year.

Pound Slide Continues as US Jobs Report Beats Forecast

The British pound has posted slight losses in the Wednesday session, continuing the downward movement we've seen for most of the week. In North American trade, GBP/USD is trading at 1.3384, down 0.44% on the day. On the release front, there are no British events on the schedule. In the US, ADP Nonfarm Employment Change slowed to 190 thousand, just above the forecast of 189 thousand. On Thursday, the US releases unemployment claims.

The ADP nonfarm employment report came in as expected, with a gain of 190 thousand. Still, this was a soft reading compared to the previous release, which showed a gain of 235 thousand. Investors are, of course, much more interested in the official nonfarm employment change release, which takes place on Friday. Again, the markets are expecting a soft landing, with a forecast of 200 thousand, down from 261 thousand in the October release. If nonfarm payrolls, one of the most important indicators, is weaker than expected, the US dollar could lose ground. The US will also release a wage growth report on Friday, with the markets expecting a gain of 0.3%.

The Brexit talks are back in the spotlight, but unsurprisingly, there remain plenty of bumps on the road. There had been hopes of a major announcement following a meeting between Prime Minister May and European Commission President Jean-Claude Juckner. However, these expectations were left on hold, as it became apparent that wide gaps remain on two key issues – Northern Ireland and the European Court of Justice. The European Union is willing to let EU rules apply to Northern Ireland, but the small DUP party, which is keeping the May government afloat, is against any steps which could be seen as moving the north and the republic of Ireland closer to unification. A solution that will satisfy the UK, the EU and the DUP over the Irish border remains elusive. Another thorny issue issue is whether the European Court of Justice will apply to European citizens in the UK after Brexit. While the EU is in favor of the court having authority over these citizens, many British lawmakers feel that such a move would undermines British sovereignty. The EU holds a key summit on December 12, and May, who is facing pressure at home over her handling of Brexit, is anxious to wrap up the non-trade issues and move on to trade negotiations as quickly as possible.

Australian Q3 GDP Results Just Shy of Expectations

Yearly GDP growth picked up in the third quarter but was a bit below market expectations. Consumer spending was soft, reflecting spotty retail sales during the quarter.

Rise in Investment, But Where is the Consumer?

The Australian economy expanded 0.6 percent over the quarter (not annualized), just shy of market expectations of 0.7 percent. That said, it still marked an improvement in yearly growth to 2.8 percent, which points to the continued expansion of the Australian economy.

A lead driver of third quarter growth was the improvement in investment spending. Increasing 1.8 percent on the quarter (not annualized), this rise in fixed investment is encouraging for the sector as it continues to improve this year. This print marks the second-fastest growth rate going back to 2012. Fixed investment contributed 1.8 percentage points to the headline quarterly figure, positioning it as a lead driver of the third quarter growth rate in Australia. Third quarter growth also was boosted by a modest buildup in inventories, contributing 0.7 percentage points to headline GDP.

The weak print in private consumption could reasonably have been expected given the muted retail sales figures over the quarter. Having grown at 0.1 percent, this marks the weakest growth rate in household spending since 2008. Although Australian households are strapped with high levels of debt, which could restrain spending going forward, we do not expect such low levels of household spending to persist in the fourth quarter. October retail sales figures jumped 0.5 percent, signaling potential improvement into the fourth quarter. Weak retail figures are, in part, a continued reflection of subdued wage growth within Australia. Although we have seen a continuous decline in the unemployment rate, the tightening of labor market conditions are not being transferred to an increase in income.

RBA Still on Hold…For Now

As was broadly expected, the Reserve Bank of Australia kept its cash rate on hold at its December meeting. RBA Governor Philip Lowe noted improvement in the labor market and as well as his expectation for the soft wage growth dynamic to eventually give way to a lift in wages and broader inflation over time. The text of the accompanying statement was upbeat on the economy, particularly the outlook for the non-mining sector. "The outlook for non-mining business investment has improved further, with the forward-looking indicators being more positive than they have been for some time."

A rate increase is not yet in the cards in Australia, but if inflation firms in the manner describe by Governor Lowe, signals of eventual tightening may creep into the discussion in 2018. In the meantime, a measured but broad improvement in global growth and higher commodity prices should be supportive of the Australian currency. Meanwhile, as we get into 2018, renewed trend weakness in the greenback and eventual signals from the RBA on rate hikes should signal moderate gains for the Aussie dollar.

Lack of Progress in Brexit Talks Puts Sterling Under Pressure

The common currency price is falling today against the US dollar. Even with positive data releases out of the Eurozone today, traders were in no mood to buy up the euro. German factory orders in October rose by 0.5% against the forecasted decline of 0.2% and the retail PMI in the Eurozone rose to 52.4 in November compared to 51.1 in the previous period. However, the political crisis in the US over the investigation of Donald Trump's ties with Russia and ongoing discussions on tax cuts will restrain the dollar bulls.

The British pound is losing positions due to lack of progress in negotiations between the UK and the European Union on the Brexit terms. The British Prime Minister is trying to reach an agreement on the key conditions of the Brexit, but at the center of attention remains lack of support for Mrs. May among her ministers and unsolved questions on the border between Northern Ireland and the Republic of Ireland.

The Australian dollar has fallen today after the release of disappointing statistics, according to which the Australian economy expanded by only 0.6% in the third quarter against the 0.7% expected and 0.9% in the previous period. Trading tomorrow is likely to be influenced by the release of the trade balance at 00:30 GMT and by the new home sales release in Australia published at 22:30 GMT later today.

Investors are waiting for the labour market data in the US, which will be released on Friday which may provoke a volatility spike as it is a key indicator on the Fed's decision for an interest rate hike in December.

EUR/USD

The EUR/USD quotes were not able to leave the limits of the local descending channel and currently are located near 1.1825. The signal to buy in case of the price breaking through 1.1850 will be the overcoming of the local high at 1.1850. In this case, the targets will be at 1.1925 and 1.2000. On the other hand, within the limits of the channel, quotes may reach the closest objective at 1.1730.

GBP/USD

The GBP/USD quotes have broken through the lower boundary of the ascending channel. Fixing under the local support at 1.3350 may lead to the fall acceleration and within this impulse, the price may reach the immediate goals at 1.3250 and 1.3150. In case of correction, the quotes may return to SMA100 on the 15-minute chart.

AUD/USD

The aussie quotes have shown a strong descending movement but were not able to reach the strong support at 0.7565. During the rising price correction, the AUD/USD may return to 0.7600 and its breaking may force the bulls to push the price higher to 0.7660. Volatility is likely to remain high.

Bank of Canada Has No More Surprises for 2017

Highlights:

- The overnight rate was left unchanged at 1%, continuing a pause following back-to-back rate hikes in July and September.

- Recent domestic data, including a 1.7% annualized increase in Q3 GDP, have been roughly in line with the bank's forecast laid out in October.

- Gradual firming in core inflation was attributed to shrinking economic slack. Headline inflation has been a bit higher than expected though the bank seemed to chalk that up to temporary factors.

- They continued to note higher rates will be required over time but maintained quite a bit of flexibility in their tightening bias.

Our Take:

The Bank of Canada's tone was little changed after their final meeting of the year, once again serving up vague forward guidance with a side of caution. They noted firmer growth in a number of advanced economies, higher oil prices and easier financial conditions but continued to flag uncertainty surrounding the global outlook. Domestically, recent trends in investment, trade, infrastructure spending and housing were close enough to prior expectations. The bank may have been a bit surprised by the strength of consumer spending in Q3, which was attributed to robust employment growth. They didn't get overly excited about last week's labour market report though, noting some improvement in wages but still pointing to lingering, albeit diminishing, labour market slack.

Our forecast assumes the bank's cautious mindset will keep them on the sidelines until April. That will give them some time to evaluate the impact of this summer's two rate hikes. They'll also (hopefully) have a better idea of how one of the most significant risks facing the economy, the Nafta renegotiation, is evolving. Last week's jobs report had markets flagging potential for an earlier move, but with the central bank not sounding overly excited, we remain comfortable with our call.