Sample Category Title

BOC Kept Powder Dry, Warned of Slack Capacity Despite Falling Jobless Rate

The BOC left the policy rate unchanged at 1% in December. While acknowledging the strength in the employment situation, it warned of the slack in the labor market. While upgrading GDP growth forecast, it noted that it does not necessarily imply a narrower output gap. While admitting the policy rate would have to increase over time, it reiterated caution over any monetary decision. All in all, the central bank attempted to deliver a neutral to dovish message, so as not to cripple the recovery path – a lesson learnt after two consecutive rate hikes in July and September. Canadian dollar plunged after the announcement, with USDCAD jumping to as high as 1.2777, highest level in three days.

Canada's unemployment rate plunged to almost a decade low of 5.9% in November. The number of payrolls added was +79.5K, beating consensus of only a +10K addition. BOC acknowledged the improvement. However, it added that "despite rising employment and participation rates, other indicators point to ongoing - albeit diminishing - slack in the labour market".

Inflation has remained subdued, offering the central bank the strongest reason to stay on hold. Despite modest pickup, core CPI stayed below +1% (at +0.9%) in November. Meanwhile, all of BOC's inflation measures stayed way below the +2% target. The central bank noted the recent improvement on inflation, noting that it "has been slightly higher than anticipated and will continue to be boosted in the short term by temporary factors, particularly gasoline prices". It also noted that "measures of core inflation have edged up in recent months, reflecting the continued absorption of economic slack". Regarding to the upgrade of the GDP growth estimate, policymakers attributed it to "revisions to past quarterly national accounts" and stressed that it "is unlikely to have significant implications for the output gap because the revisions also imply a higher level of potential output".

BOC omitted the October references related to the loonie's strength. In October, the members pushed back the timing that inflation would rise to +2%, suggesting that this was driven by "recent strength in the Canadian dollar". They also noted that "projected export growth is slightly slower than before, in part because of a stronger Canadian dollar. These references disappeared in December, as Canadian dollar has remained under pressure during the intermeeting period.

On the monetary policy outlook, the BOC hinted the next move would likely be a rate hike. As noted in the accompanying statement, "while higher interest rates will likely be required over time, Governing Council will continue to be cautious". It affirmed that "the current stance of monetary policy remains appropriate".

BoC: Poloz Holds for Now With Caution Ruling the Day

As widely expected, the Bank of Canada held its key monetary policy interest rate at 1.00% this morning, with the accompanying statement striking a dovish tone.

The economic backdrop appears to be evolving in line with the Bank's expectations at the time of the October Monetary Policy Report, although 'considerable uncertainty' still clouds the global outlook.

The Canadian economy is also seen as falling in line with their expectations, with 'very strong' employment growth noted, as well as robust consumer spending, ongoing contributions from business investment, and more evidence that public infrastructure spending is having a rising impact on growth. Although exports disappointed in the third quarter, the Bank noted that the latest trade data supports the view that exports are likely to make a positive contribution to growth going forward.

On the inflation front, slightly higher than anticipated price pressures are seen as being helped by temporary factors (notably gas prices), but core inflation has also ticked up in line with 'continued absorption of economic slack'.

On the downside, the Bank continues to see "ongoing - albeit diminishing - slack in the labour market", while noting that employment continues to rise alongside participation rates.

The final section of the statement struck a somewhat dovish tone. It was noted that higher rates will likely be required over time, but the Governing Council will be 'cautious, guided by incoming data", pointing again to the key areas of the Bank's focus in recent quarters: the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of wage growth and inflation.

Key Implications

If it weren't for the final section of the statement, this would have looked like a central bank getting ready to hike. With developments since their October Monetary Policy Report in line with their expectations, by their own assessment the economy is likely entering excess demand, which would typically call for a monetary policy response.

Indeed, most, if not all of the tick-boxes that the Bank has identified appear to be getting ticked: employment growth remains robust, wages continue to accelerate by almost all measures, and consumer spending has remained healthy despite rising borrowing costs with the most recent aggregate employee compensation data reported the strongest quarterly gain since late 2014. This latter point should help reduce the sensitivity of the economy to rising rates - it's easier to deal with a potential rise in debt service costs if you're also making more money. It is also becoming increasingly difficult to identify the labour market slack that once again seems to be a key factor in the Bank's decision making.

Ultimately, it is the Bank's risk management framework that appears to have ruled the day. Despite things seeming to line up for further near-term tightening, Governor Poloz has chosen to maintain his optionality. With economic growth appearing likely to exceed the Bank's 2.5% expectation for the fourth quarter of this year, things continue to point to a hike sooner rather than later. However, as today's statement shows, nothing is a done deal until the day of the decision.

Yen Dips as US Employment Report Meets Expectations

The Japanese yen has edged lower in the Wednesday session. In North American trade, USD/JPY is trading at 112.17, down 0.31% on the day. On the release front, there are no major Japanese indicators. In the US, ADP Nonfarm Employment Change slowed to 190 thousand, a shade above the forecast of 189 thousand. On Thursday, the US releases unemployment claims and Japan releases Final GDP for the third quarter.

Bank of Japan Governor Haruhiko Kuroda remains the model of consistency, at least as far as its monetary policy. On Monday, Kuroda reiterated that the BoJ would maintain its ultra-accommodative monetary policy in order "to achieve the 2 percent inflation target as soon as possible". The BoJ has been forced to constantly lower its inflation projections, yet the Bank has stubbornly stuck to its 2 percent target. Although the labor market remains tight, this has not translated into higher wages for workers, and nervous consumers have held tight to their purse strings, further contributing to a lack of inflation. Kuroda noted that global economic growth had improved, although he sounded a note of concern about President's Trump isolationist policy, saying that he hoped that global trade would be conducted under the multilateral trading system.

The ADP nonfarm employment report came in as expected, with a gain of 190 thousand. However, this was a substantial drop compared to the previous reading of 235 thousand. Investors are, of course, much more interested in the official nonfarm employment change release, which takes place on Friday. Again, the markets are expecting a soft landing, with a forecast of 200 thousand, down from 261 thousand in the October release. If nonfarm payrolls, one of the most important indicators, is weaker than expected, the US dollar could lose ground. The US will also release a wage growth report on Friday, with the markets expecting a gain of 0.3%.

Euro Slides, Big Questions

The euro tested the 100-day moving average as the market sorts through political and central bank questions. The New Zealand dollar was the top performer while the euro lagged. The Bank of Canada is due shortly. Earlier in Asia, Australian Q3 GDP grew by less than expected, promptinng broad AUD selloff. The BOC decision later, with less than 20% chance of rate hike expected, but expect an optimistic spin. US ADP weakened to 190K as expected. The Premium CAD trade remains in the green.

Economic data on Tuesday featured the ISM non-manufacturing index. It slipped to 57.4 from a 12-year high of 60.1. The reading was below the 59.0 expected but the market hardly moved on the results because hurricane effects were the likely driver.

More broadly, the market is pondering three big questions. The first is what is next for global central banks. A series of decisions are due in the next 9 days and that will clarify the path for rates next year. The second is the US tax reform bill. The details are what matter now and small changes are driving the US equity market, with sentiment also swinging back and forth, with the usual pre-Santa rally selloff in view. Thirdly, even if those questions are answered, year-end flows could swamp fundamentals and leave the market vulnerable.

On the central banking front, the RBA offered some hints at what coming. Lowe talked about improving global growth and how that is an upside risk for inflation.

The BOC is up next to weigh in on the global outlook. The market is pricing in a 17% chance of a hike. That's high but understandable given past BOC surprises. If they hold, a CAD rally can't be ruled out if they signal a more hawkish stance in 2018. Currently a hike is 70% priced in for March.

Dollar Resists Risk-off Correction

- European equities lose up to 0.5% with the German Dax underperforming (-1%). US stock markets opened with marginal losses. The Nasdaq underperforms again (-0.3%).

- The US economy added 190 000 jobs in the private sector in November according to payroll processor ADP, down from 235k in October. The outcome confirms ongoing strength on the US labour market and was bang in line with expectations.

- Britain has not conducted formal sector-by-sector analyses of the impact that leaving the EU will have on the economy, Brexit minister Davis said, arguing they were not necessary yet. The comments inflamed critics of the government's handling of the complex divorce process.

- ECB officials risk limiting their options for dealing with any unexpected acceleration in inflation if they make policy promises that extend too far into the future, Executive Board member Mersch said.

- German industrial orders increased unexpectedly in October (0.5% M/M & 6.9% Y/Y) thanks to domestic and non-euro zone demand, suggesting this sector of Europe's biggest economy is likely to gain steam in the coming months.

- U.S. unit labor costs were lower than initially thought, declining both in the second and third quarters of this year. The price of labor per single unit of output dropped at a 0.2% annualized rate in the last quarter (initially reported at 0.5%). ULC in de second quarter even declined at an annualized rate of 1.2%, previously reported as a 0.3% rise.

Rates

German 10-yr yield tests 0.3% support

Global core bonds traded mixed today with the US Note future slightly outperforming the German Bund. The Bund opened higher in a catch-up move, but traded sideways afterwards while the US Note future extended gains. Yesterday's commodity sell-off (industrial materials like copper) didn't continue today and losses on European equity markets were limited to the ones recorded in the opening. So risk sentiment turned neutral following risk aversion in Asia. The eco calendar added little spirit to trading with US ADP employment bang in line with forecasts at a strong 190k.

Interesting comments from ECB Mersch didn't resonate in dealings either. Mersch joins the German-Franco hawkish camp which is currently in the minority at the ECB, but could gain traction in coming months as ultradovish ECB heavyweights (Constancio, Praet and Draghi) will be replaced between mid-2018 and the end of 2019. Mersch warned about risks from pre-committing monetary policy for too long in a context of a booming economy: "If our forward guidance is reaching too far into the future, beyond the point at which reasonable predictions about the economy can be made, there's a risk that our hands will be tied needlessly. When the time comes in the course of next year when we reconsider our monetary-policy course, we should think carefully how much we pre-commit." He also openly suggested whether current monetary policy is too accommodative, arguing that the difficulty of measuring inflationary pressures might mean that the ECB is "running behind developments without being aware of it." He concludes that a drastic correction in monetary policy will be necessary in coming years in that scenario.

At the time of writing, the German yield curve bull flattens with yields 0.6 bps (2-yr) to 1.9 bps (30-yr) lower. Technically, the German 10-yr yield is currently testing important support at 0.30%. Changes on the US yield curve vary between declines of 2 to 2.5 bps across the curve. On intra-EMU bond markets, 10-yr yield spread changes versus Germany widen up to 2 bps.

Currencies

Dollar resists risk-off correction

Global market were captured by a global risk-off correction today. However, the spill-overs to the interest rate and FX markets were modest. The dollar held up well despite the decline in core/US yields. USD/JPY is holding north of 112. EUR/USD even drifted to the low 1.18 area.

The US equity slide accelerated in Asia overnight, with commodity related stocks taking the lead after a sell-off of copper yesterday. Losses varied across markets, but mounted up to 2% (Japan/Hong Kong). The equity decline pressured US yields, but the damage for the dollar was contained. USD/JPY dropped to the low 112 area. EUR/USD held relatively stable near 1.1840.

The trends from Asia basically continued in Europe. European equities joined the risk-off correction from Asia. Strong German order data didn't change sentiment. As was often the case of late, changes in global risk sentiment had only a modest impact on other markets. Core yields (in the US and Europe) ceded a few basis points, but remained in well-known territory. Changes in interest rate differentials were also too small to guide FX trading. The dollar continued to perform rather well, given the circumstances. USD/JPY held north of 112 despite the decline of equities and lower core yields. EUR/USD even trended lower in the 1.18 big figure. The pair trades currently near the 1.18 big figure. The US ADP labour market report showed net 190 000 job growth in the US private sector last month, perfectly in line with consensus. Yesterday, we suggested that there were tentative signs that the big (ST) interest rate differential is gradually giving the dollar some additional downside protection. At least for now, this hypothesis survives.

Sterling resilient even as Brexit headline stay negative

Brexit headlines continued steering sterling trading today. Sterling showed some brisk swings this week as initial hope on a separation deal didn't prove justified. The UK currency trades off the recent highs reached before the press conference of UK PM May and EC head Juncker on Monday evening. In a broader perspective, the losses of sterling remain modest given the negative news flow. Today's headlines still brought little evidence that a deal could be reached anytime soon. There were renewed indications that part of PM May's party were questioning her leadership. UK Brexit minister Davis faced questions in Parliament whether the government had accurately investigated the potential consequence of Brexit. Last but not least, the DUP, supporting May's minority government, sees a deal on the Irish border as unlikely this week, the EU deadline. EUR/GBP (currently 0.8835) settled well north of 0.88, but no important technical level was broken. Cable declined back below the 1.34 barrier, but part of this move was due to cable mirroring the intraday decline of EUR/USD. So, sterling holds up quite well, suggesting that markets still see a decent change of a last minute solution ahead of next week's EU summit.

(BOC) Bank of Canada Maintains Overnight Rate Target at 1 Per cent

The Bank of Canada today maintained its target for the overnight rate at 1 per cent. The Bank Rate is correspondingly 1 1/4 per cent and the deposit rate is 3/4 per cent.

The global economy is evolving largely as expected in the Bank's October Monetary Policy Report (MPR). In the United States, growth in the third quarter was stronger than forecast but is still expected to moderate in the months ahead. Growth has firmed in other advanced economies. Meanwhile, oil prices have moved higher and financial conditions have eased. The global outlook remains subject to considerable uncertainty, notably about geopolitical developments and trade policies.

Recent Canadian data are in line with October's outlook, which was for growth to moderate while remaining above potential in the second half of 2017. Employment growth has been very strong and wages have shown some improvement, supporting robust consumer spending in the third quarter. Business investment continued to contribute to growth after a strong first half, and public infrastructure spending is becoming more evident in the data. Following exceptionally strong growth earlier in 2017, exports declined by more than was expected in the third quarter. However, the latest trade data support the MPR projection that export growth will resume as foreign demand strengthens. Housing has continued to moderate, as expected.

Inflation has been slightly higher than anticipated and will continue to be boosted in the short term by temporary factors, particularly gasoline prices. Measures of core inflation have edged up in recent months, reflecting the continued absorption of economic slack. Revisions to past quarterly national accounts have resulted in a higher level of GDP. However, this is unlikely to have significant implications for the output gap because the revisions also imply a higher level of potential output. Meanwhile, despite rising employment and participation rates, other indicators point to ongoing – albeit diminishing – slack in the labour market.

Based on the outlook for inflation and the evolution of the risks and uncertainties identified in October's MPR, Governing Council judges that the current stance of monetary policy remains appropriate. While higher interest rates will likely be required over time, Governing Council will continue to be cautious, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.

Information note

The next scheduled date for announcing the overnight rate target is January 17, 2018. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.

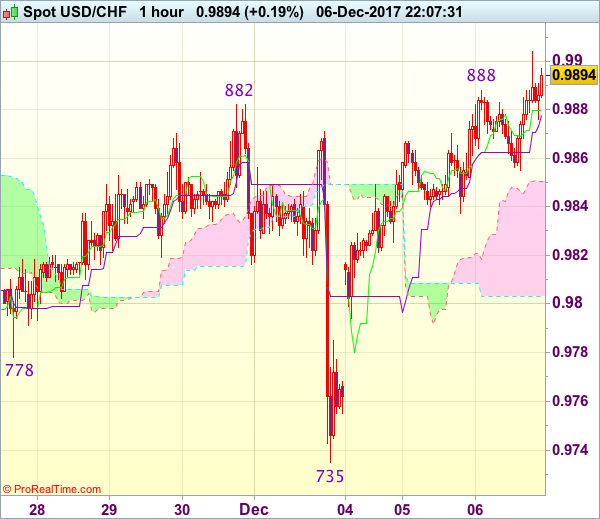

Trade Idea Wrap-up: USD/CHF – Buy at 0.9825

USD/CHF - 0.9888

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9880

Kijun-Sen level : 0.9878

Ichimoku cloud top : 0.9851

Ichimoku cloud bottom : 0.9803

Original strategy :

Buy at 0.9820, Target: 0.9920, Stop: 0.9785

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9825, Target: 0.9925, Stop: 0.9790

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone after staging a strong rebound from 0.9735 (last Friday’s low), adding credence to our view that a temporary low has been formed there and consolidation with upside bias remains for this move to bring at least a strong retracement of recent decline to 0.9920 and later towards resistance at 0.9947 but reckon 0.9990-00 would hold from here due to near term overbought condition.

In view of this, we are looking to buy dollar on dips as 0.9820-25 should limit downside and bring another rebound. Below 0.9790 would defer and risk weakness to 0.9755-60 but still reckon said last week’s low at 0.9735 would remain intact.

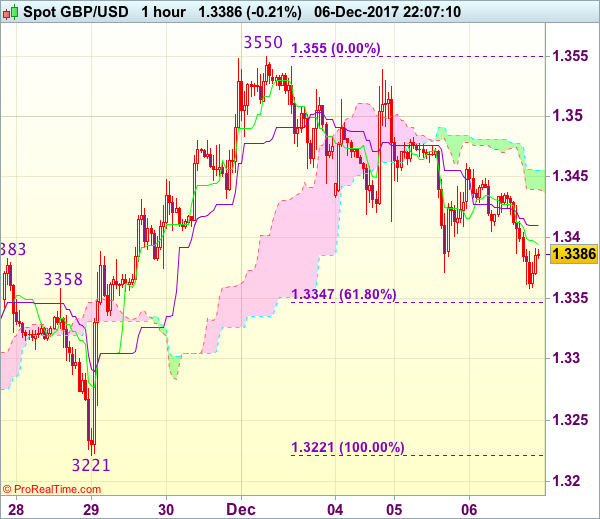

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.3440

GBP/USD - 1.3377

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3394

Kijun-Sen level : 1.3410

Ichimoku cloud top : 1.3455

Ichimoku cloud bottom : 1.3439

Original strategy :

Sold at 1.3440, Target: 1.3340, Stop: 1.3465

Position : - Short at 1.3440

Target : - 1.3340

Stop : - 1.3465

New strategy :

Hold short entered at 1.3440, Target: 1.3340, Stop: 1.3455

Position : - Short at 1.3440

Target : - 1.3340

Stop : - 1.3455

Cable met renewed selling interest at 1.3461 and has fallen again, adding credence to our bearish view that top has been formed at 1.3550 and downside bias remains for the erratic fall from there to bring retracement of recent rise to 1.3340-50 (61.8% Fibonacci retracement of 1.3221-1.3550) but near term oversold condition should prevent sharp fall below 1.3300 and reckon 1.3260-65 would hold, bring rebound later.

In view of this, we are holding on to our short position entered at 1.3440. Only above said resistance at 1.3461 would defer and risk test of resistance at 1.3483 but break there is needed to signal an intra-day low is formed instead, bring another bounce to 1.3530-35 first.

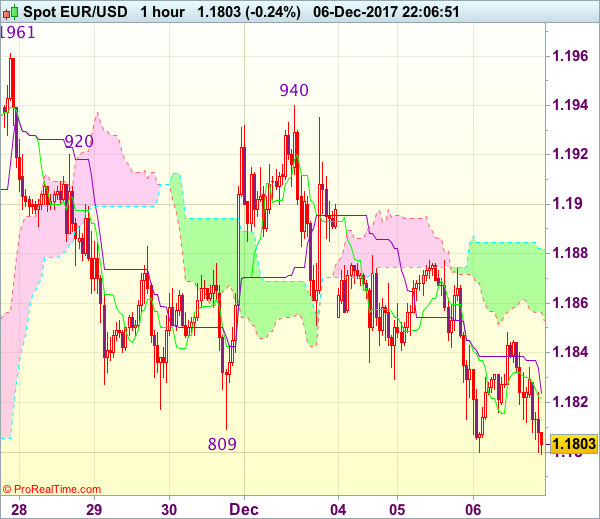

Trade Idea Wrap-up: EUR/USD – Sell at 1.1865

EUR/USD - 1.1805

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1820

Kijun-Sen level : 1.1822

Ichimoku cloud top : 1.1856

Ichimoku cloud bottom : 1.1820

Original strategy :

Sell at 1.1900, Target: 1.1800, Stop: 1.1935

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1865, Target: 1.1765, Stop: 1.1900

Position : -

Target : -

Stop : -

As the single currency has fallen again after brief recovery, adding credence to our bearish view that the erratic decline from 1.1961 top (last week’s high) is still in progress and downside bias remains for further weakness to to 1.1770 and possibly towards support at 1.1736 but near term oversold condition should limit downside and price should stay above previous key support at 1.1713.

In view of this, we are looking to sell euro on recovery as 1.1870-75 should limit upside and bring another decline. Above 1.1900 would risk test of last Friday’s high at 1.1940 but only break there would revive bullishness, bring retest of 1.1961 later.

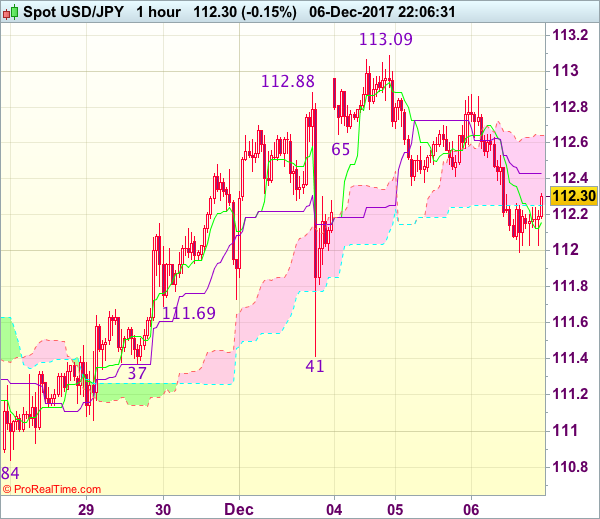

Trade Idea Wrap-up: USD/JPY – Hold long entered at 112.10

USD/JPY - 112.28

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 112.16

Kijun-Sen level : 112.43

Ichimoku cloud top : 112.64

Ichimoku cloud bottom : 112.25

Original strategy :

Bought at 112.10, Target: 113.30, Stop: 111.75

Position : - Long at 112.10

Target : - 113.30

Stop : - 111.75

New strategy :

Hold long entered at 112.10, Target: 113.30, Stop: 111.75

Position : - Long at 112.10

Target : - 113.30

Stop : - 111.75

Although the greenback slipped again earlier today and marginal weakness from here cannot be ruled out, reckon downside would be limited and 111.80 should hold, bring rebound later, above 112.90 would signal the retreat from 113.09 has ended, bring retest of this level, break there would extend recent rise to resistance at 113.33 but loss of upward momentum should prevent sharp move beyond 113.60-70.

In view of this, we are holding on to our long position entered at 112.10. Below 111.80 would defer and risk weakness to 111.60 but only break of said support at 111.37-41 would abort and signal top is formed instead.