Sample Category Title

Forex: No Surprises From BoC & ADP But GBP Comes Under Pressure

In an unsurprising move, the Bank of Canada decided to hold its benchmark lending rate at 1%, after two small hikes earlier in 2017. The BoC stated on Wednesday that it has decided to keep its target for the overnight rate right where it is, while rate hikes in July and in September continue to work their way through the economy. The central bank commented, 'While higher interest rates will likely be required over time, the bank will continue to be cautious, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation.' The markets had expected the BoC to keep the rate steady but the news saw CAD come under selling pressure, with USDCAD trading up from 1.2660 to just above 1.2800 where it has steadied overnight.

The US ADP report also provided few surprises, with private sector jobs in the US increasing by 190K from October to November as forecast by the market. The ADP Research Institute commented that 'The labor market continues to grow at a solid pace' and 'Notably, manufacturing added the most jobs the industry has seen all year. As the labor market continues to tighten and wages increase it will become increasingly difficult for employers to attract and retain skilled talent. The markets look at the ADP report for clues on the 'always impactful' NFP report due to be released on Friday.

GBP came under selling pressure on news that Michel Barnier, the EU's chief Brexit negotiator, has told member states that the British government has just 48 hours to agree terms on a potential deal or it will be told that negotiations will not move on to the next stage. If talks do not move on to the next stage of discussions in December then the terms of a transition period will likely be pushed back until the next European council summit of leaders in March, by which time many businesses in the UK will have had to make decisions over their location and investments in the country. Prime Minister May told the UK Parliament, 'We're leaving the European Union, we're leaving the single market and the customs union but we will do what is right in the interests of the whole United Kingdom,' and 'nothing is agreed until everything is agreed.' GBP gave back many of its gains to trade as low as 1.3375 overnight.

EURUSD is little changed overnight, currently trading around1.1795.

USDJPY is 0.2% higher in early Thursday trading at around 112.48.

GBPUSD is 0.15% lower in early session trading at around 1.3373.

USDCAD is 0.15% higher overnight, trading around 1.2805.

Gold is little changed overnight, trading around $1,262.50.

WTI is 0.15% higher in early trading at around $56.12.

Major data releases for today:

At 10:00 GMT: Eurostat will release Eurozone Gross Domestic Product s.a. (QoQ) and (YoY) for Q3. Both releases are expected unchanged with Quarter-on-Quarter GDP forecast at 0.6% and Year-on-Year GDP forecast at 2.5%. Any significant deviation from the forecast is likely to see EUR volatility.

At 13:30 GMT: The US Department of Labour will release Initial Jobless Claims for the week ended December 1st and Continuing Jobless Claims for the week ended November 24th. Initial Claims are forecast to show a slight increase to 240K from the previous reading of 238K. Continuing Claims are forecast to come in slightly lower at 1.915M from the previous reading of 1.957M. Any significant deviation from expectations will see USD volatility.

At 16:00: European Central Bank President Mario Draghi is scheduled to speak in his capacity as Chair of the Group of Governors and Heads of Supervision (GHOS) in a press conference by the Bank for International Settlements, hosted at the European Central Bank in Frankfurt, Germany.

USDJPY Remains In Broad Range, Positive Undertone In Near Term

USDJPY has not had a clear trend since January this year as the pair has been trading in a broad range between 108 – 114. In the short term, prices have moved to the upper half of the range, having firmed up this week.

USDJPY has made an astounding recovery after bouncing from the 108 area in September. But the pair failed to break out of the range and found strong resistance at the top of the range, consequently reversing back down. The market found strong support in the 111 area, which is around the mid-point of the range.

Technical indicators are pointing to more consolidation in the near term, as the RSI is flat and hugging the 50 level, while the 50 and 200-day moving averages are moving sideways. USDJPY is expected to remain supported on dips to 111 and capped in the zone below the key 113 level and the 50-day MA at 112.80.

Overall, risk remains on the upside despite the pullback from 113 this week. The undertone in the near term is expected to remain positive as long as the USDJPY remains above 111.

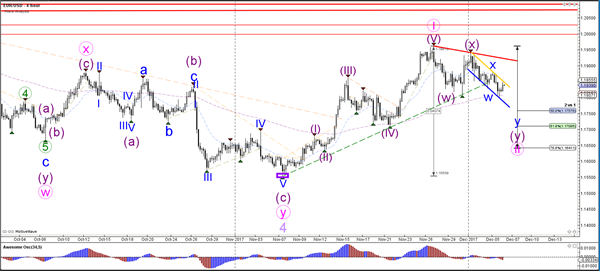

Daily Wave Analysis: EUR/USD Bearish Channel Aiming At 1.17 And 50-61.8% Fibonacci

Currency pair EUR/USD

The EUR/USD is building a bearish correction as expected. The choppy and corrective price action is making a wave 1-2 (pink) pattern more likely. The bearish channel could take price down lower to the Fibonacci levels of wave 2. A break below the bottom (purple box) invalidates this wave pattern.

The EUR/USD broke below the support trend line (dotted green) and fell below 1.18 but is a sturdy pullback. This could be part of a wave B (green) within a larger bearish ABC zigzag.

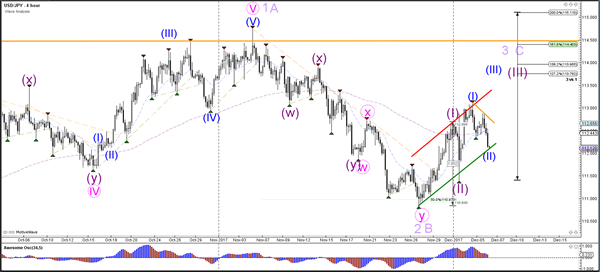

Currency pair USD/JPY

The USD/JPY is testing the bottom / support (green) of the uptrend channel. An impulsive bullish bounce could indicate that price is building a wave 2 (blue) whereas a sideways movement could mean a bear flag pattern and more downside.

The USD/JPY will need to bounce at support first of all and later on break above the resistance (red/orange) to confirm the wave 3 pattern (purple). For the moment, price could have built a bearish ABC pattern within wave 2 (blue) and the Fibonacci levels and the support trend line could stop price from falling.

Currency pair GBP/USD

The GBP/USD is building a bearish correction which is probably part of a larger a wave 1-2 (green). This is invalidated if price breaks below the 100% Fibonacci level of wave 2 vs 1.

The GBP/USD is showing a triangle chart pattern (orange/blue). A break below or above the triangle could indicate a potential breakout.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD continued its bearish momentum yesterday slipped below 1.1800 support area, bottomed at 1.1780. Although price is now still struggling around 1.1800 region, I think the bullish phase is no longer valid. The bias remains bearish in nearest term testing 1.1690 support area. Immediate resistance is seen around 1.1850. A clear break back above that area could lead price to neutral zone in nearest term as direction would become unclear. Overall I remain neutral.

GBPUSD

The GBPUSD had a bearish momentum yesterday bottomed at 1.3357. The bias is bearish in nearest term testing 1.3330 support area. A clear break and daily close below that area could trigger further bearish pressure testing 1.3220 and the trend line support as you can see on my daily chart below which is a good place to buy with a tight stop loss. Immediate resistance is seen around 1.3420. A clear break above that area could lead price to neutral zone in nearest term testing 1.3480 or higher. Overall I remain bullish.

USDJPY

The USDJPY had a bearish momentum yesterday bottomed at 111.99 but closed higher at 112.28 and hit 112.48 earlier today in Asian session. The bias is neutral in nearest term but as long as stay below 113.20 I still prefer a bearish scenario at this phase as a part of the bearish pin bar scenario on daily chart (November 06). Immediate resistance is seen around 112.63 (yesterday’s high). A clear break above that area could trigger further bullish pressure testing 113.00/20 region which remains a good place to sell with a tight stop loss. Immediate support is seen around 112.00. A clear break below that area would expose 111.65 region. Overall I remain neutral.

USDCHF

The USDCHF had a bullish momentum yesterday, broke above 0.9875 resistance area. The bias is bullish in nearest term testing 0.9940 region. Immediate support is seen around 0.9875. A clear break back below that area could lead price to neutral zone in nearest term as direction would become unclear testing 0.9850 – 0.9818 support area. On the upside, a clear break and daily close above 0.9940 would expose 1.0000 – 1.0037 region. Overall I remain neutral.

EUR/USD Broke Below 1.18

Market movers today

In Germany, industrial production is set to show a decent increase for October after a drop in September. A rise in factory orders yesterday continued to point to a robust recovery, as does a high level of German manufacturing confidence.

Headlines regarding German politics could come back into focus, as the three-day SPD party conference kicks off today, where SPD members will decide whether to enter renewed coalition negotiations for a ‘grand coalition' with Angela M erkel's CDU p arty.

US initial jobless claims is the last piece of input on the US job market ahead of the payrolls report tomorrow. Initial claims have hovered around 240k recently, pointing to a strong labour market (see our US Labour Market Monitor: Expect strong November report, 5 December).

In the late afternoon, ECB President Mario Draghi will participate in a press conference by the Bank for International Settlement in his role as Chair of the Group of Governors and Heads of Supervision, but this is unlikely to provide material news ahead of the ECB meeting next week.

Some interesting Scandi data is due today. Norway is due to release manufacturing production and in Sweden, household consumption and not least average house prices will be followed closely to gauge the temperature of the Swedish housing market (see page two for more).

Selected market news

Asian shares hovered near two-month lows this morning as softer oil and copper prices and uncertainty over US foreign p olicy , following Trump 's announcement to recognise Jerusalem as Israel's cap ital, kep t many investors on the sidelines. Oil prices are trading near two-week lows after a big fall on Wednesday, when a sharp rise in US inventories suggested demand may be flagging, while US crude production hit another weekly record. Eonia remains elevated past the Greek bond swap on Tuesday and the ECB's weekly MRO allotment yesterday and hence the higher fixings can no longer be deemed temporary.

Markets are also still focused on the US tax reform and a potential US government shutdown, although we deem the lat ter unlikely. It now looks increasingly likely that the corporate tax rate will end up at 22% and not 20%, supporting our view that the final tax bill will be a watered down version of what is already on the table, as Republicans struggle to find a common ground on tax revenue raisers in order to finance tax cuts. Yesterday, the Senate also voted in favour of going to conference and Republicans still hope to send a bill to Trump 's desk before y ear-end, although that is still ambitious in our view. Nevertheless, EUR/USD broke below 1.18 yesterday, also helped by growing US tax-reform optimism.

Regarding Brexit, PM Theresa May is still under siege from her own party and the Northern Irish DUP to forge a deal on the Irish border issue. May is said to submit another proposal to Ireland within 24 hours, while the EU has indicated willingness to be flexible on the Brexit deadline ahead of the key summit next week.

Market Update – Asian Session: China Drafts New Rules Impacting Liquidity

Headlines/Economic Data

General Trend: Nikkei rebounds from largest drop seen in 2017, but Asian indices are overall mixed

Profit warning from Samsung Heavy continues to weigh on shipbuilders

Shares of Tencent rebound

Japan

Nikkei 225 opened +0.6% (declined 2% on prior session), driven by tech names; closed +1.5%

Chip-related shares gain: Tokyo Electron +3%, SUMCO +2.5%

Fast Retailing +1.7% (declined 4.9% prior session)

(JP) BoJ Gov Kuroda: Reiterates long way to go to reach 2% price target, will 'persistently' continue 'powerful' easing; reiterates current yield curve appropriate for now; Prices and financial system are two most vital BoJ targets

(JP) Japan MoF sells ¥800B (incl non-competitive bids) v ¥800B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.848% v 0.789% prior; Bid to cover: 4.38x v 3.43x prior

(JP) Japan Nov Official Reserve Assets: $1.26T v $1.26T prior

(JP) Moody's affirms Japan's sovereign rating at A1; outlook stable

(JP) Japan Chief Cabinet Sec Suga: Progress achieved on maritime communications with China

Looking Ahead: Japan Q3 GDP revision and Oct avg cash earnings due for release on Friday

Korea

Kospi opened +0.2%, has since moved lower

Samsung Heavy -3.5% (follow-through selling from Wed’s session); Fellow shipbuilder Hyundai Heavy -5%

Posco Steel -1%; Vale CEO commented: High prices attract inefficient producers which later hamper the market; ready to sell 50Mt of iron ore if prices get too high - financial press

Samsung Electronics +0.5%, analysts positive on shipments of 3D-sensing adopted smartphones

Korean Won (KRW) +0.2%

(KR) North Korea: nuclear war on the Korean Peninsula has become a matter of when, not if - KCNA

(KR) South Korea and Russia to step up economic cooperation - Korean press

(KR) South Korea said to be considering VAT and corporate tax on cryptocurrency

(KR) South Korea financial stability review: S. Korea urged to strengthen regulations on non-bank financial institutions

015760.KR President Cho Hwan-eik announced will resign later this week (~3-months ahead of the end of his term) - Korean press

China/Hong Kong

Markets open mixed with China drafting regulation to curb liquidity: Hang Seng +0.5%, Shanghai -0.3%

Hang Seng Materials Index -2%, Property/Construction -1.4%, Energy -0.5% Consumer Goods -0.5%; Information Technology Index +0.9% (Tencent +1.5%)

(CN) China Banking Regulatory Commission (CBRC) drafts new requirements on banks to curb liquidity risks, to go into effect March 1st, 2018 with grace period – Xinhua

PBOC conducts first open market operation (OMO) in 5 sessions; PBOC Open Market Operations (OMO): injects combined CNY270B in 7, 14 and 28-day reverse repos v skips prior; Net injection nil

(CN) PBoC sets yuan reference rate at 6.6195 v 6.6163 prior

(CN) China foreign exchange reserves likely to have risen in November (would be 10th straight increase) – press (Note: The data could be released during the European session)

(CN) IMF Review of China Financial System: Banks reported non-performing loans (NPLs) may be 'understated'; Chinese banks may have insufficient capital to weather potential losses from the nation’s rapidly mounting credit risks

(CN) PBOC disputes IMF comments on stress tests for Chinese banks

(CN) Fitch: China 2018 GDP growth seen slowing to 6.4% from 6.8% (*Note: In June, Fitch said China's economic growth 'to fall slightly below 6.0% in 2018 and 2019)

(CN) China Commerce Ministry Gao: Plans WTO case against US ‘3rd country approach; China does not view US trade probes as appropriate; China and Canada have expressed willingness to seek FTA talks

(CN) China National Petroleum Corp (CNPC): China gas consumption expected to increase by 16.4% in 2017 to a fresh record high

Looking Ahead: China Nov Trade Balance data tentatively scheduled for Friday

Australia/New Zealand

ASX 200 opened flat, banks stronger and miners impacted by metal prices; ASX then moved higher to close +0.5%

ASX 200 REIT Index +1%, Financials +0.6%, Consumer Discretionary Sector +0.5%

Gold miner Newcrest +1%

Aussie declines following trade data

(AU) AUSTRALIA OCT TRADE BALANCE: $105M V $1.4BE; Exports M/M: -3.0% v 3.0% prior; Imports M/M: +2.0% v 0.0% prior

(NZ) RBNZ: Economy continues to perform well; Some evolution of decision-making may be appropriate; Governing committee should continue with consensus decision; Governor should have final decision if no consensus; Developing depositor protection proposal; Proposal to protect deposits up to NZ$10,000 - briefing to incoming ministers dated in Oct

(AU) Australia Nov Foreign Reserves: A$85.8B v A$78.1B prior

(NZ) New Zealand sells NZ$100M in 2.5% Sept 2040 inflation-indexed bonds, avg yield 2.1110%, implied bid to cover 2.14x

FCG.NZ Reports Q1 (NZ$) Rev 4B. +4% y/y, sales volumes 3.9B LME, -20% y/y; Cuts FY18 Farmgate milk price $6.40 (prior $6.75)

AIR.NZ Due to Rolls Royce engine issues will be some cancellations to international flights in the coming weeks; no change to guidance at the time

Other

Fitch sees 2018 global growth 3.3% (vs 3.1% in June) vs 3.2% (2.9% prior) expected for 2017 - 2018 Outlook Emerging Asia Sovereigns report

North America

US equity markets ended mixed: Dow -0.2%, S&P 500 flat, Nasdaq +0.2%, Russell 2000 -0.5%

S&P 500 Energy Sector -1.3%; Technology +0.6%

Government Funding/Debt Ceiling: (US) House Rules Committee passes rule for two-week stopgap spending bill until Dec 22nd; full floor debate seen occurring as early as Thurs – press

(US) Pres Trump: govt shutdown could happen; Don't see a reason we can't get to 4, 5 or 6% GDP growth

(US) Earlier on Wed, the White House said that President Trump would sign stop-gap spending measure advanced in the House that funds government through Dec 22nd

(US) US House Republicans said to seek to link debt ceiling increase to spending bill – US financial press; Republicans are said to be likely to increase the debt limit enough to last at least through the midterm elections due to be held in Nov of 2018, says the article; The government is expected to have to act by March on the debt ceiling in order to avoid a default.

(US) On Wed, Treasury Sec Mnuchin sent a letter to congressional leaders in order to tell them that the Treasury would begin taking extraordinary measures on Friday and urged politicians to raise the debt limit at the first opportunity; The Treasury's extraordinary measures will enable it to continuing paying bills into next Spring.

Tax Reform: (US) S&P sovereign rating head: GOP tax plan will increase deficit and could prompt the Fed to raise rates further; fiscal policy could lead to negative rating action unless long-term challenges are addressed

(US) House Speaker Ryan: believe we can make the tax bill better in reconcillation process and Senators will support a better bill; Confident that the bill will be ready for Pres Trump to sign by Christmas

(US) Senate Majority Leader McConnell: Named Senate GOP tax bill conferees (**Note: On Dec 4th, McConnell confirmed that the Senate and House would go to conference over their tax bills)

(US) GOP congressional leaders reportedly mulling 22% corporate tax rate level (vs 20%) as bill deadline nears - Wash Post; GOP may need to find new revenue to fund last minute modifications to the bill

(US) Sen Maj Leader McConnell (R-KY): remains open to tweaking state and local tax provisions in GOP tax reform bill

(US) Sen Hatch (R-UT): doesn't look like the corporate alternative minimum tax (AMT) will be in final tax bill

Other Politics: (US) Sen Franken (D-MN) to announce resignation on Thursday - local press

Energy: (US) DOE CRUDE: -5.6M V -2.5M

(RU) Russia Energy Min: too soon to discuss exiting oil production deal; process should be gradual; exit could take up to six months, depending on oil market recovery and oil demand

Lululemon:+7% in the afterhours (Q3 results above ests, midpoint of Q4 guidance above est, raised FY17 outlook)

Chevron: Announces FY18 Capex $18.3B, down ~7.6% vs planned spending for FY17

VALE CEO Schvartsman: High prices attract inefficient producers which later hamper the market; ready to sell 50Mt of iron ore if prices get too high - financial press

Europe

(UK) EU parliament details UK concessions on rights - financial press

(IE) Ireland PM Varadkar: had a good phone call with UK PM May, and willing to look at any proposals from the UK side; PM May did not suggest any new wording on the Irish border today; Any new wording on the Irish border must be consistent with the substance of the text that was agreed upon on Monday

(IE) Ireland PM Varadkar and UK PM May agree on the 'paramount importance' of no hard border in Ireland - joint statement

(UK) Govt spokesperson Slack: UK govt wants to make progress on Brexit as quickly as possible; UK cabinet to discuss the desired end state for Brexit by the end of the year

(UK) DUP Party spokesperson: Irish govt is playing a dangerous game over border issue; longer delay on border deal, the higher likelihood of no deal

(UK) Fin Min Hammond: UK and Ireland are absolutely committed to keeping an open border on the island of Ireland; Likely to get more clarity in next year or two on when UK budget will be in balance

(UK) Allies of Brexit Min Davis reportedly have launched attempt to replace Prime Min May - UK press

(DE) Germany Deputy Fin Min: govt said to focus refinancing its 30-year bonds and maybe 50yr; Gov't spent €1.6B more than planned in Oct/Nov - German press; Jutta Doenges to be named as head of the finance agency.

Fitch sees 2018 global growth 3.3% (vs 3.1% in June) vs 3.2% (2.9% prior) expected for 2017 - 2018 Outlook Emerging Asia

M&A: Sky plc: CNBC's Faber: Disney aims to own all of Sky as part of any Fox asset deal (not just the stake in Sky that is owned by Fox)

Looking ahead: Euro Zone Final Q3 GDP; UK 30-year Gilt Auction; ECB Draghi due to speak during NY morning

Levels as of 01:00ET

Nikkei225 %, Hang Seng +0.5%; Shanghai Composite -0.4%; ASX200 +0.5%, Kospi -0.4%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.4%, Dax +0.1%; FTSE100 +0.3%

EUR 1.1809-1.1793; JPY 112.51-112.22; AUD 0.7569-0.7542;NZD 0.6889-0.6850

Feb Gold-0.1% at $1,264/oz; Jan Crude Oil +0.1% at $56.02/brl; Mar Copper +0.0% at $2.97/lb

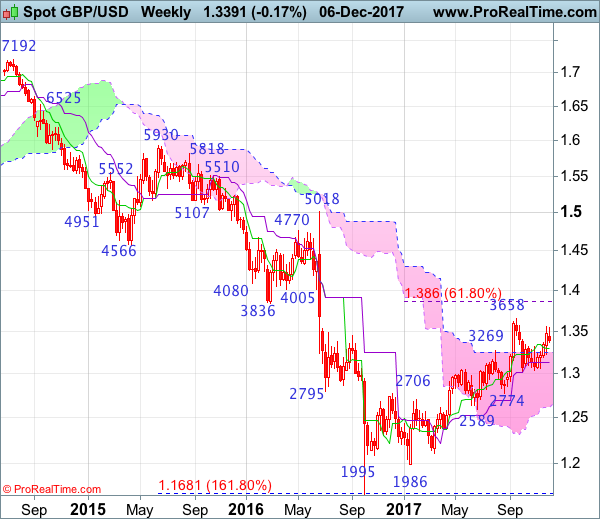

GBP/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 31 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Morning star

• Time of formation: 25 Aug 2017

• Trend bias: Near term up

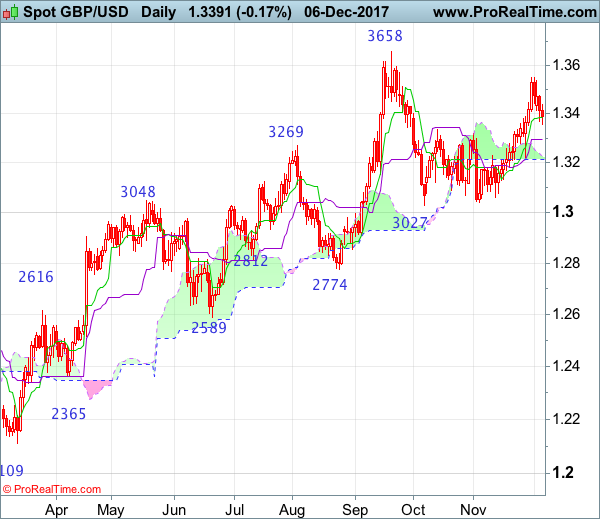

GBP/USD – 1.3372

Although the British pound rose to as high as 1.3550 late last week, the subsequent retreat from there suggest top is possibly formed there and consolidation with mild downside bias is seen for weakness to the Kijun-Sen (now at 1.3295), however, a daily close below support at 1.3221 is needed to add credence to this view, bring further fall to 1.3185-90 and later towards 1.3130 but near term oversold condition should prevent sharp fall below there and price should stay above previous support at 1.3062, risk from there has increased for a rebound later.

On the upside, whilst recovery to 1.3450-60 cannot be ruled out, reckon upside would be limited to 1.3500 and bring another decline to aforesaid downside target. Only break of said last week’s high at 1.3550 would abort and signal the rise from 1.3027 is still in progress, then test of resistance at 1.3596 and price should falter below recent high at 1.3658. Looking ahead, a breach above this level is needed to retain bullishness and confirm medium term upmove has resumed and bring subsequent headway to 1.3770-80.

Recommendation: Sell at 1.3460 for 1.3260 with stop below 1.3560.

On the weekly chart, sterling ran into strong resistance around 1.3550 late last week and has retreated in part due to dollar;s broad-based rebound, suggesting consolidation below this level would be seen and mild downside bias is for a test of the Tenkan-Sen (now at 1.3295), a weekly close below this level would suggest top has possibly been formed, bring further fall to support at 1.3221, once this level is penetrated, this would add credence to this view, bring further fall to 1.3130 and later towards strong support at 1.3062. Looking ahead, only a drop below 1.3027 support would revive bearishness and signal top has indeed been formed at 1.3658, bring a stronger correction of early rise to 1.3000, then towards support at 1.2909.

On the upside, expect recovery to be limited to 1.3450-60 and 1.3500 should hold, bring another retreat later. Above 1.3550 (last week’s high) would shift risk back to the upside and extend the rise from 1.3027 to 1.3600, then test of last month’s high at 1.3658, break there would confirm medium term rise from 1.1986 low has resumed for headway to 1.3750-60 and 1.3800 but anticipated overbought condition should prevent sharp move beyond 1.3860 (61.8% Fibonacci retracement of 1.5018-1.1986).

Gold Price Turns Bearish Versus US Dollar

Key Highlights

- Gold price made a U-turn and declined below the $1275 support against the US Dollar.

- There was a break below an important ascending channel with support at $1282 on the 4-hours chart of XAU/USD.

- The US ADP Employment Change in Nov 2017 was 190K, better than the forecast of 185K.

- Today, the US Initial Jobless Claims for the week ending Dec 2, 2017 will be released, which is forecasted to increase from 238K to 240K.

Gold Price Technical Analysis

Gold price struggled a lot to hold the $1280-1282 support area against the US Dollar. The price started a downside move and is currently well below the $1275 support.

Looking at the 4-hours chart of XAU/USD, there was a downside break below an important ascending channel with support at $1282. The price moved down sharply below $1280 and is currently well below both 100 simple moving average (red, 4-hour) and 200 simple moving average (green, 4-hour).

The price traded as low as $1260.99 recently and started a minor correction. It tested the 23.6% Fib retracement level of the last decline from the $1289.31 high to $1260.99 low.

The upside correction seems to be limited by the $1270 and $1275 levels. Should the price fail to move higher, it could even break $1260 for more declines.

US ADP Employment Change

Recently in the US, the Employment Change for Nov 2017 was released by the Automatic Data Processing, Inc. The forecast was slated for a change of 185K, compared with the last 235K.

The actual result was on the higher side, as the Private Sector employment increased by 190,000 jobs in November 2017, on a seasonally adjusted basis.

Commenting on the report, the vice president and co-head of the ADP Research Institute, Ahu Yildirmaz, stated:

The labor market continues to grow at a solid pace. Notably, manufacturing added the most jobs the industry has seen all year. As the labor market continues to tighten and wages increase it will become increasingly difficult for employers to attract and retain skilled talent.

The outcome was positive and helped the US Dollar in gaining bids versus all major currencies in the short term.

Economic Releases to Watch Today

Euro Zone Gross Domestic Product Q3 2017 (QoQ) – Forecast 0.6%, versus 0.6% previous.

Euro Zone Gross Domestic Product Q3 2017 (YoY) – Forecast 2.5%, versus 2.5% previous.

US Initial Jobless Claims – Forecast 240K, versus 238K previous.

Australia’s Trade Surplus Narrowed Sharply In October

For the 24 hours to 23:00 GMT, the AUD declined 0.55% against the USD and closed at 0.7564.

LME Copper prices declined 1.6% or $106.0/MT to $6539.0/MT. Aluminium prices declined 1.2% or $23.5/MT to $2028.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7549, with the AUD trading 0.2% lower against the USD from yesterday's close, after latest data showed that Australia's trade surplus slumped in October.

Data showed that Australia seasonally adjusted trade surplus narrowed more-than-anticipated to A$105.0 million in October, hitting its lowest level in six months, amid a sharp fall in exports and a rise in imports. The nation had registered a revised surplus of A$1604.0 million in the previous month, while markets were anticipating for a surplus of A$1400.0 million.

On the other hand, the nation's AiG performance of construction index climbed to a level of 57.5 in November, notching a four-month high level and following a reading of 53.2 in the prior month.

The pair is expected to find support at 0.7528, and a fall through could take it to the next support level of 0.7507. The pair is expected to find its first resistance at 0.7584, and a rise through could take it to the next resistance level of 0.7619.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Germany’s Factory Orders Posted An Unexpected Rise In October

For the 24 hours to 23:00 GMT, the EUR declined 0.2% against the USD and closed at 1.1805, after Germany's Markit construction PMI fell to a ten-month low level of 53.1 in November, hinting that the nation's construction sector is losing momentum. In the preceding month, the PMI had recorded a level of 53.3.

On the contrary, the nation's seasonally adjusted factory orders surprisingly advanced 0.5% on a monthly basis in October, rising for the third straight month, thus suggesting that the nation's industrial sector would continue to remain on a strong growth path in the last quarter of 2017. Factory orders had registered a revised rise of 1.2% in the prior month, while markets expected for a drop of 0.2%.

The greenback gained ground against its key counterparts, after ADP's private sector employment in the US advanced by 190.0K in November, meeting market expectations. ADP private sector employment had recorded a gain of 235.0K in the prior month.

Additionally, the nation's mortgage applications rebounded 4.7% in the week ended 01 December 2017. In the previous week, mortgage applications had recorded a drop of 3.1%.

In the Asian session, at GMT0400, the pair is trading at 1.1804, with the EUR trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.1774, and a fall through could take it to the next support level of 1.1744. The pair is expected to find its first resistance at 1.1841, and a rise through could take it to the next resistance level of 1.1878.

Going ahead, traders would await a speech by the European Central Bank (ECB) President, Mario Draghi, due later in the day. Moreover, the Euro-zone's final 3Q GDP figures as well as Germany's industrial production data for October, will be on investors' radar. Also, the US initial jobless claims data, followed by consumer credit change for October, will garner a lot of market attention.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.