Sample Category Title

XAU/USD Analysis: Ready To Test Strength Of Dominant Pattern

In essence, the buck is actively appreciating against the gold the third day in a row. A short-term bullish movement towards the 38.2% Fibonacci retracement level at 1,268.00 was the only exception and was attributed to beginning of drills on the Korean peninsula. But, in general, the pair is driven by optimism over the progress of tax bill. Accordingly, today the rate is expected to continue heading downwards until it makes a rebound from the bottom boundary of a currently active two-month long descending channel near 1,255.00. However, the above market sentiment has a good chance to push the rate even more down. If this breakout happens and the pair gains a foothold below the weekly S2, this might be a sign of existence of another unconfirmed four-month long descending channel.

USD/CAD: Bank Of Canada Interest Rate Decision

The Canadian Dollar marked a solid depreciation against the US Dollar, as the country's Central Bank announced its interest rate decision. The USD/CAD currency pair added almost 100 base points in total, trying to offset the losses made during the last week.

The Bank of Canada kept ist cautious mode over the next rate increase, even in the presence of the first signs of healthy recovery. The Bank's polycimakers led by the Governor Stephen Poloz left the key interest rates unchanged at 1% on Wednesday, in line with expectations. The BoC is set to remain dovish, evaluating the economy's sensitivity to higher interest rates, assesing the economic capacity and the growth trends of both wages and inflation.

EUR/USD: ADP Non-Farm Employment Change

The Greenback fell modestly against the Euro on the ADP report revealing some weakening in the employment change in November. The EUR/USD lost 5 base points to return ito 1.1810 area and declined further to be seen trading below the 1.1800 area, as the next release was not strong enough to bring the pair back to stronger levels.

The US private sector created 190K jobs in November, down strongly from the prior month, but in line with projections, the ADP report indicated, ahead of more comprehensive the US Labour Departments figures to be issued on Friday. Meanwhile, another data showed the revision of the US unit labour costs, which was at an annualised 0.2% rate in the Q3, compared to the initially reported 0.5% rise.

GBP/CAD 1H Chart: Pound pressured by resistance

GBP/CAD has been trading in a channel down since mid-August. The pair, however, has failed to reach the bottom boundary of this pattern several times, thus resembling more an ascending wedge. In the short term, the Pound bounced off the upper channel boundary last week and began trading lower. Given that solid Canadian GDP data release on December 1 strengthened the Loonie, the rate failed to form a proper pattern. Meanwhile, the Pound has lost its strong momentum during the past trading hours, as the combined resistance of the weekly and monthly PPs, the 200– and 100-hour SMAs pressure the given currency near the 1.7150 mark. This might force the pair into a period of consolidation, but nevertheless guide it towards the upper boundary of the short-term channel circa 1.72. In case bears prevail, the nearest support is the weekly and monthly S1s at 1.6860.

CAD/JPY 1H Chart: Descending Channel Dominates

The Canadian Dollar has weakened against the Japanese Yen during the past two-and-a-half months, thus forming a descending channel. This pattern is a part of a long-term falling wedge which was formed mid-December, 2016. After bouncing off the bottom boundary of the medium-term channel, the Loonie managed to push up to the weekly R1 at 89.15 within a couple of sessions and thus reach the northern boundary of this pattern. From technical point of view, the pair should continue its movement south down to the bottom channel boundary located in the 86.00/86.50 territory. This scenario is likewise confirmed by weekly technical indicators. However, the pair found resistance at the 200-hour SMA in this session. Thus, it might still edge slightly higher before allowing bears to take the upper hand

Swiss Data And SNB Preview: FX Reserve Fell From Record High As SNB Unless Less Pressure To Intervene

SNB's FX reserve slipped to 738.17B franc, from a record high of 741.96B franc (revised from previous estimate of 741.32B franc), in November. The drop is in contrast with consensus of an increase to 745B franc and marks the first drop since June this year. Meanwhile, the sight deposit fell to 576.78B franc in the week ended December 1. Subsequent decline from the August peak has sent sight deposit to the lowest level since June 2017. The movements of both FX reserve and sight deposit have suggested that the SNB is not in a hurry to intervene with the recent weakness in Swiss franc. Separately, the country's unemployment rate stayed unchanged at 3% (seasonally adjusted) in November, compared with expectations of a rise to 3.1%. For the quarterly SNB meeting scheduled on December 14, we expect policymakers to maintain the status quo, i.e. keeping 3-month LIBOR target range unchanged, at between -1.25% and -0.25%, maintaining the interest rate on sight deposits with the SNB at -0.75% and reaffirming that the central bank is committed to intervene in the FX market as necessary. We believe the domestic economic developments since the September meeting have shown gradual improvements, leaving policymakers more room to wait and see.

GDP Growth

Swiss GDP growth picked up to+1.11% y/y in 3Q17, from +0.68% in 2Q17 and +0.48% in 1Q17. While it is true that the most of the growth was driven by the increase in the volatile “net acquisitions of valuables”, other indicators are underpinning the strong growth momentum. For instance, the KOF indicator jumped to a 6-year high of 11.89 in November, after drifting modestly lower in the prior month. The Markit manufacturing PMI jumped to 65.1, the highest since July 2010, in November from 62 in the prior month. The market had anticipated a modest increase to 62.5.

Inflation

Subdued inflation has remained the key reason to leave the policy rate at historical low. Headline CPI steadied at +0.8% in October and averaged at +0.5% y/y in 3Q17. SNB's measure of 6-12 month inflation expectations had risen from +0.3% to +0.5%. Consumer expectations on inflation outlook have also improved. As the latest SECO survey suggested, consumers expectations of positive price developments has risen to 56% in the three months through October, from 45% in the three months though July. However, all measures still suggest the Swiss price levels has remained soft and far below the +2% target.

Exchange Rate

Swiss franc has depreciated -1.8% against the euro and -2.6% against the greenback. Just like what it did at the September meeting, we expect the SNB to soften its complaint over Swiss franc's strength, but reiterate that the franc is still “overvalued” and pledge vigilance over the exchange rate movement. As Governor Thomas Jordan noted in Basel on November 23, the country's' high current account surplus “is not a reflection of an overly weak Swiss franc”. Rather it is driven by several reasons including statistical distortion - overstatement, structural reasons – aging population and the skew towards pharmaceuticals and merchanting industries which are relatively insensitive to exchange rate fluctuations. Jordan reiterated in his speech that “the Swiss franc remains highly valued” and “inflation is still low and production capacity is not yet fully utilized”.

Mint Ratio Signals Gold’s Moment Of Truth

Gold has finally broken 1260.00 long-term support in early Europe as the gold/silver (mint) ratio hits new highs suggesting a much more substantial down move could now occur.

GOLD

Gold attempted a comeback rally after Tuesday's calamitous sell-off, but it was quickly snuffed out and failed ahead of 1270.00. Instead, the yellow metal ended the day with a whimper, closing near its lows at 1263.70 and appearing to be preparing itself for a severe test of critical long-term support. Gold traders will face a nervous end to the week as gold fails to rally even as the U.S. yield curve continues to flatten and ahead of crucial payroll data tomorrow evening.

With Asian shares solidly in the red and a general risk-off mood permeating the markets, it is significant that gold cannot find any support. The safe-haven bid that would typically appear in times such as these has disappeared from the market's thoughts. It is yet another black market against the yellow metal.

Gold has now closed two days in a row under its 200-day moving average at 1267.30 and now intra-day resistance. This is followed by 1270.00 and then 1273.30.

The downside looks far more ominous, with gold breaking the critical long-term support at 1260.00 in early Europe, trading to a low of 1256.00 as stop losses set in. We have had a small rebound to 1259.00 but have been unable to recapture 1260.00. A daily close below this level could set of structural unwinding of long positioning, and the technical picture shows no meaningful support for gold until the 1200.00 regions.

While it is still too soon to suggest a significant sell-off is on the cards, the charts do imply that gold may well be about to break out of its three-month trading range.

Silver

Silver has led gold lower over the last week. The break of its five-month trendline support at 17.0000 also took out it's 100 and 200-day moving averages. Silver has since plunged over the past week to the 15.8900 lows we have seen today. Resistance is at 16.2360 and 16.5380, but the charts have no meaningful support until 14.9200, still another dollar away.

Temporary salvation may be at hand though. The daily Relative Strength Index (RSI) is now at very oversold levels. This is an excellent short-term indicator when used with precious metals and commodities. It suggests that Silver may have done enough for now and that a bounce could be on the cards in the short-term at least

Gold/Silver (Mint) Ratio

The mint ratio has hit six-month highs overnight, moving to the 79.00 regions. Traders should note that the ratio's daily RSI is at extreme overbought levels. This implies that either silver is hugely oversold (see above), or that gold is not yet at fair values, ie overbought versus silver. (see gold above)

Whichever way you chose to cut it, the mint ratio and its RSI are telling us that that gold could go lower and or that silver should remain unchanged or move higher.

The mint ratio also has interim resistance just above at 79.35 will strong resistance at 81.80. Support is at 75.75 and then 74.00 which is a massive level, being multiple daily lows over the last six months.

The fact that support is so far away as compared to resistances again reinforces the case that the mint ratio could be signalling more downside for gold.

NZDUSD Sees Strengthening Bearish Momentum In Near Term

NZDUSD has a negative undertone as the flow is back to the downside following a break below the key 0.6900 level.

On the 4-hour chart, the RSI is bearish while the 20 and 50-period moving averages are negatively aligned.

The rapid pullback from yesterday’s 0.6916 high suggests NZDUSD does not have enough momentum to resume the uptrend from 0.6780 to 0.6945 (November 17-28 rise).

As long as NZDUSD remains above the 0.6816 low then the pair is expected to remain neutral and to consolidate the recent gains. A move back above 0.6900 would shift focus back to the upside to target 0.6916 and set the market on a path towards 0.7000.

Meanwhile, breaking below the 0.6816-0.6800 zone could see a re-test of the 0.6780 low and likely see the start of a new downtrend.

The fact that the market has retraced more than 61.8% of the 0.6780 to 0.6945 upleg keeps the NZDUSD vulnerable to additional weakness.

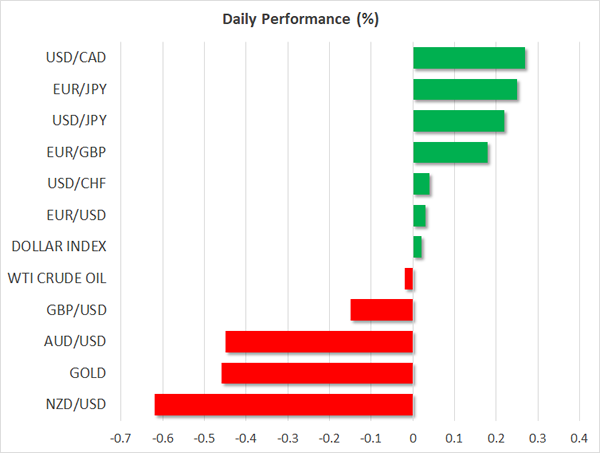

Dollar At 2-Week Highs, Nikkei Rebounds

Here are the latest developments in global markets:

FOREX: The dollar hit a two-week high against a basket of currencies as optimism on US tax reform continued to support the currency, though concerns over a possible government shutdown restricted steeper upside movement. The euro and the pound were on track to post the third day of consecutive losses versus the greenback, while the loonie tumbled to a one-week low after the BOC expressed caution for further rate hikes. The aussie tumbled in the wake of worse-than-expected Australian trade data.

STOCKS: The Nikkei rebounded after yesterday’s sharp fall, closing 1.45% higher; stocks in mainland China recorded losses though. Euro Stoxx 50 futures traded 0.2% higher at 0751 GMT. Dow and S&P 500 futures were up by 0.1% and Nasdaq 100 equivalents traded higher by 0.4%.

COMMODITIES: Oil prices were trading near three-week lows touched yesterday following the release of the EIA report on US crude inventories. US crude stocks fell more than expected but gasoline and distillate inventories surged past forecasts. WTI crude and Brent were flat at $56.00 and $61.35 per barrel respectively. Gold retreated to a four-month low of $1,256.02 an ounce (-0.47%).

Major movers: Loonie loses ground on perceived BOC dovishness; antipodeans also down after Australian trade data drag

The loonie was on the backfoot during Asian trading, pushing dollar/loonie to a one-week high of 1.2824 (+0.30%) after the Bank of Canada held interest rates unchanged on Wednesday at 1.0% but remained cautious on future rate increases despite upbeat evidence on employment the previous day. The monetary policy statement following the decision stated that “while higher interest rates will likely be required over time”, upcoming data will determine the path of monetary policy, giving no clue about when the central bank will further normalize policy. Hence, investors priced that a hike in January will be less likely.

Meanwhile in the US, Senate Republicans and House policymakers agreed on Wednesday to extend talks on the tax overhaul, raising hopes that differences between them could be resolved soon. Dollar/yen climbed to 112.60, while euro/dollar was hovering around a two-week low of 1.1790, pressured by disappointing German data on industrial production released earlier today. Pound/dollar was close to one-week lows at 1.3338, being weighed by weakening momentum for a breakthrough in Brexit talks.

The aussie and the kiwi dipped into losses after Australia’s October trade surplus narrowed to A$0.105 billion compared to the forecasted A$1.410bn. Exports fell by 0.3% m/m after a rise of an equivalent percentage in September, and imports increased by 2.0%. The aussie dived to a six-month low of 0.7522 (- 0.54%) to $0.7522 and the kiwi sank to a one-week low of $0.6833 (-0.64%).

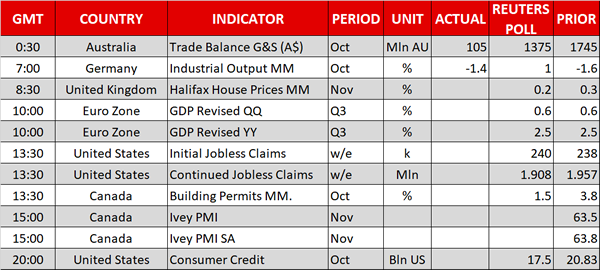

Day ahead: Beyond politics, eurozone GDP, US jobless claims and Canadian building permits on today’s calendar

The eurozone will see the release of revised third quarter GDP growth figures at 1000 GMT. The numbers are expected to remain unchanged relative to the initial estimates of growth which pointed to quarterly growth of 0.6% and annual expansion in the order of 2.5%.

Out of the US, weekly jobless claims – initial and continued – due at 1330 GMT will be gathering attention. The number of initial benefits claimants for the week ending December 1 is anticipated to be 240k, little changed from the preceding week’s 238k. The world’s largest economy will also see the release of October consumer credit data at 2000 GMT.

Canadian building permits for the month of October and the country’s November Ivey PMI due at 1330 GMT and 1500 GMT respectively are also considered of relative importance and could spur movements in the loonie.

Halifax house price data out of the UK will be released within minutes. Month-on-month, prices are expected to rise by 0.2% in November. This compares to October’s rise by 0.3%.

In politics, President Trump’s action to recognize Jerusalem as the capital of Israel could generate some uncertainty; developments will be watched. US lawmakers’ efforts on tax reform will also be closely watched. Senate Republicans yesterday agreed to engage in discussions with the House of Representatives in an attempt to reconcile the two versions of the tax bill they voted in favor of; a December 22 self-imposed deadline is in place. Attempts by Congress on averting a partial government shutdown by week-end will be generating interest as well. Lastly, UK PM Theresa May might also take some initiatives to move beyond the seeming impasse in Brexit talks.

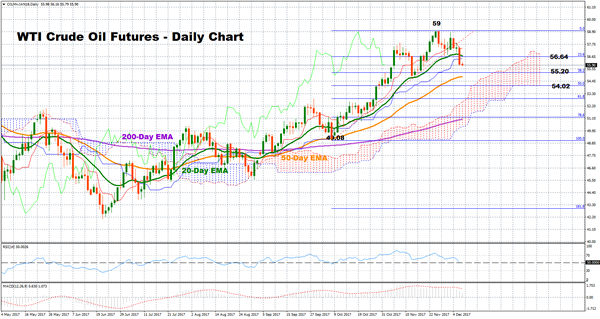

Technical Analysis: WTI crude oil futures bearish in short-term, bullish medium-term outlook intact though

WTI crude oil futures maintain a bullish picture in the medium-term but in the short-term, the market turned bearish after the price moved off the 2-½-year high of 59.0 on November 27. The RSI is currently at the 50 neutral-perceived level but is heading lower. The MACD is below its signal line and the price has crossed below the 20-day exponential moving average, hinting that negative movements might occur in the near-term.

In the dips, the market might find support at the 38.2% Fibonacci of 55.20 of the upleg from 49.08 to 59.0. From here, the 50-day EMA at 54.85 and the 50% Fibonacci mark at 54.02 could also act as barriers to downside movements.

On the upside, prices could find resistance at the 20-day EMA at 56.72, which is also the 23.6% Fibonacci level. Steeper increases could also open scope for a test at the 2 ½-year high of 59.0, while a breach of this point would paint a bullish picture in the short-term as well.

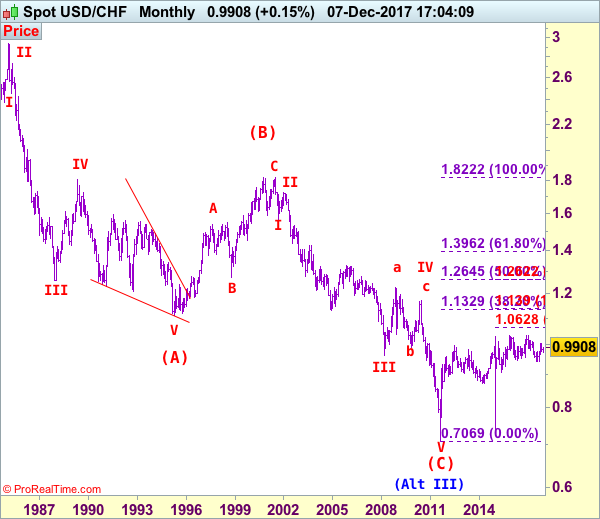

USD/CHF Elliott Wave Analysis

USD/CHF – 0.9908

Although the greenback extended recent fall from 1.0039 to as low as 0.9735 late last week, as dollar found decent demand there and has staged a strong rebound, suggesting low has been formed there and consolidation with upside bias is seen for gain to 0.9947 resistance, however, a daily close above 0.9987 is needed to add credence to this view and signal entire correction from 1.0039 has ended at 0.9735, then retest of this level would follow. Looking ahead, a break of 1.0039 would confirm early upmove from 0.9421 low has resumed and extend headway to previous resistance at 1.0100.

Our preferred count on the daily chart is that early selloff to 0.9630 is an end of the larger degree wave III and major correction is unfolding from there with a leg ended at 1.2298 (Nov 2008 with (a): 1.0625, (b):1.0011 and (c):1.2298), wave b ended at 0.9910 with (a): 1.0370, (b): 1.1967, (c): 0.9910. The rise from there to 1.1730 is the wave c which also marked the end of wave IV and wave V has possibly ended at 0.7068.

On the downside, whilst pullback to 0.9840-50 cannot be ruled out, downside would be limited and support at 0.9794 should contain weakness, bring another rise later. Only a drop below said support at 0.9735 would abort and signal the erratic decline from 1.0039 top is still in progress for retracement of early upmove to 0.9705 support, then towards 0.9640-45 but reckon previous support at 0.9589 would hold from here, bring rebound later.

Recommendation: Buy at 0.9850 for 1.0050 with stop below 0.9750.

Dollar's long-term downtrend started from 2.9343 (Feb 1995) and it was unfolding as a (A)-(B)-(C) with (A): 1.1100, (B): 1.8310 (26 Oct 2000), then followed by another impulsive wave (C) with wave III ended at 0.9630 (Mar 2008). Under this count, correction in wave IV has possibly ended at 1.1730 and wave V already broke below support at 0.9630 and met indicated downside target at 0.7500 and 0.7400. The reversal from 0.7068 suggests the wave V has possibly ended and the breach of resistance at 0.9595 add credence to this view and indicated upside target at 1.0000 had been met, however, the sharp retreat from 1.0296 to 0.7401 suggests choppy trading would be seen but price should stay above said record low at 0.7068.