Sample Category Title

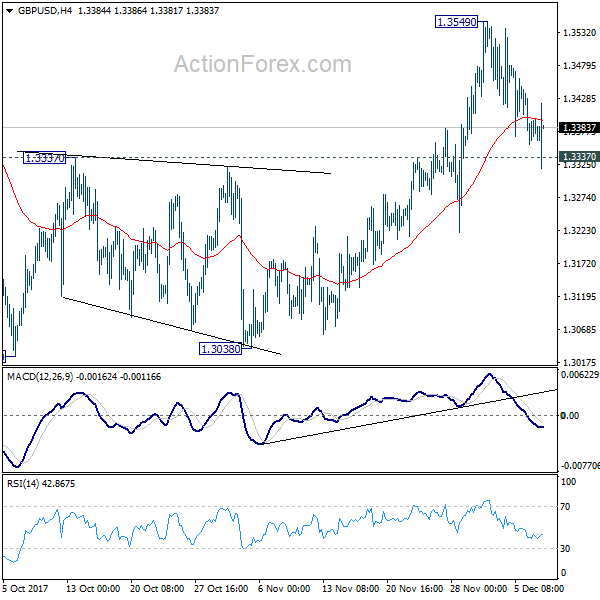

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3351; (P) 1.3397; (R1) 1.3436; More....

GBP/USD breached 1.3337 resistance turned support briefly but quickly recovered. Intraday bias stays neutral first. As long as 1.3337 holds, further rise is expected. Break of 1.3549 will target 1.3651 high and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it's still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

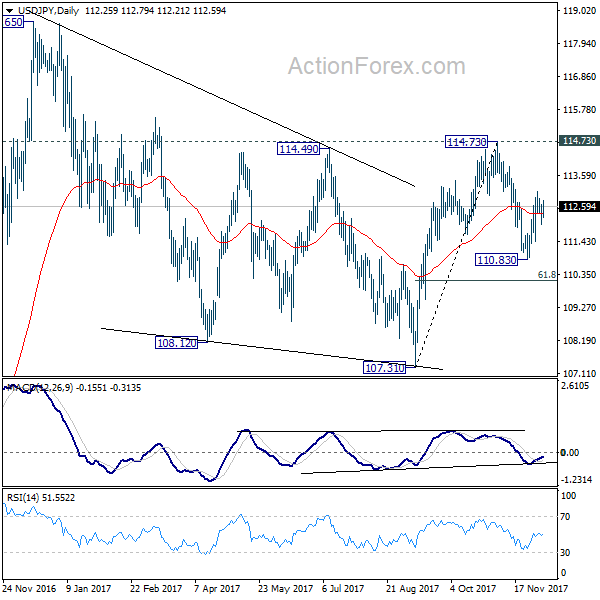

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.97; (P) 112.29; (R1) 112.61; More...

Outlook in USD/JPY remains mixed with neutral intraday bias. On the upside, above 113.08 will extend the rebound from 110.83 to retest 114.73 key resistance. Decisive break there will extend the rally from 107.31 to retest 118.65 high. On the downside, break of 110.83 will resume the decline from 114.73 instead. But in that case, we'll look for bottoming again below 61.8% retracement of 107.31 to 114.73 at 110.14.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

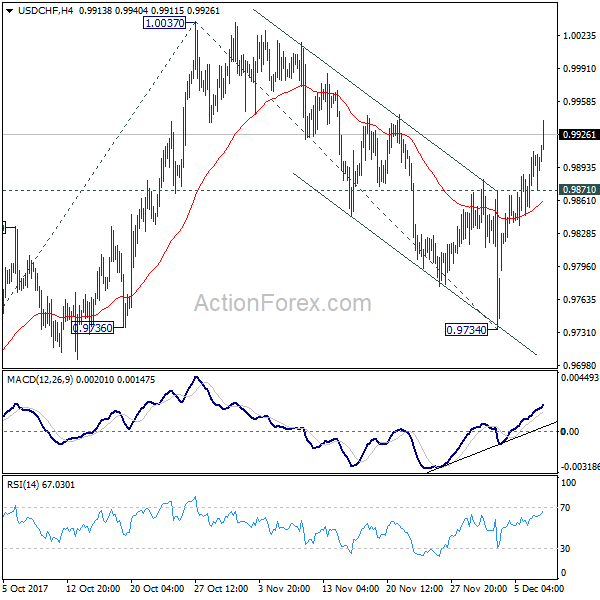

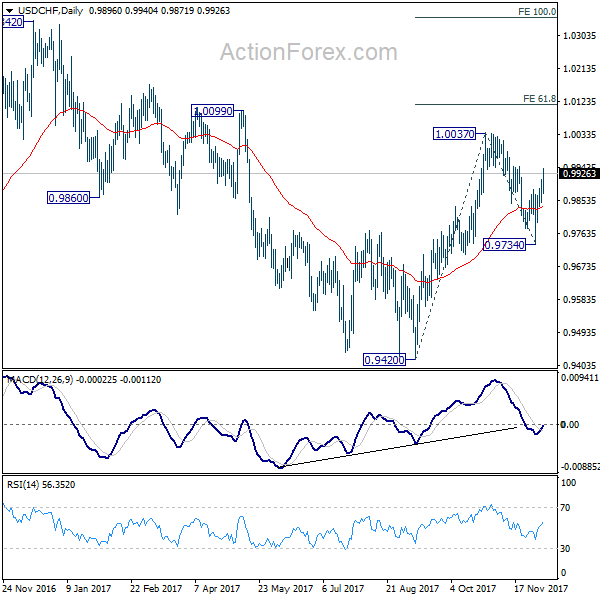

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9844; (P) 0.9865; (R1) 0.9894; More....

USD/CHF's rally from accelerates to as high as 0.9940 so far and intraday bias remains on the upside for 1.0037 resistance. Firm break there will confirm resumption of whole rise from 0.9420 and target 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115 next. On the downside, below 0.9871 minor support will dampen the immediate bullish case and turn intraday bias neutral first.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Dollar Firm as Initial Jobless Claims Dropped to Five Week Low, Extending Rally

Dollar remains the strongest currency in early US session as supported by positive job data. Initial jobless claims dropped 2k to 236k in the week ended December 2, below expectation of 241k. That's also the lowest level in five weeks. Four week moving average dropped from 242.25k to 241.50k. Continuing claims dropped -52k to 1.91m in the week ended November 25. Challenger report, though, showed 30.1% yoy rise in planned layoff in November. Overall, recent job released data point to solid non-farm payroll report to be released tomorrow. And expectation of 200k job growth could easily be matched. But again, the tricky point will remain to be wage growth.

Released elsewhere, Canada building permits rose 3.5% mom in October versus expectation of 1.70%. Eurozone GDP was finalized at 0.6% qoq in Q3, unrevised. German industrial production dropped -1.4% mom in October. Swiss unemployment rate was unchanged at 3.0% in November while foreign currency reserves dropped to CHF 735b. Japan leading indicator dropped 0.3 to 106.1 in October. Australia trade surplus narrowed to AUD 0.11b in October.

In the currency markets, Euro follow dollar as the second strongest one today. Sterling is trading as the third strongest even though there is apparently no breakthrough in Brexit negotiations Commodity currencies are trading generally as the weakest ones.

German Merkel making no progress in grand coalition talks yet

So far, there is no conclusion in the coalition talk between German Chancellor Angela Merkel's CDU/CSU and the SPD. SPD leader Martin Schulz sounded non-committal regarding the idea of grand coalition and said "we don't want to govern at any price, ... but we also shouldn't refuse to govern at any price." According to the latest Spiegel poll, only 27.9% of SPD supporters preferred a grand coalition. 56.5% preferred a minority government while 13% preferred new election. On the other hand, 61.6% of CDU/CSU supports preferred a grand coalition, 25.7% preferred a minority government and 9.7% preferred a new election.

Merkel has been clear that she even preferred a new election than a minority government. But German deputy Finance Minister Jens Spahn said in a CNBC interview that Merkel could still lead a minority government if the negotiation talk with SPD fails. He noted that "if the Social Democrats aren't willing to actually compromise with us on the necessary issues like the question of how we remain a strong economic power … Then there can't be a grand coalition." And still, "we, as Christian Democrats, want to govern even in a minority government, that will be new for Germany, but it's time for new things anyway." Spahn was also sure that "Angela Merkel will lead the next government, no matter if it's a grand coalition again or perhaps a minority government."

UK PM May to announce new Irish board proposal

In UK, under-pressure Prime Minister Theresa May is set to announce a new proposal on the Irish border issue. That's an effort to please pro-Brexit Northern Ireland DUP while May is rushing to complete the three tasks of divorce bill, Irish border and citizens right. Time is getting tight to make sufficient progress before December 14/15 EU summit, to move on to trade talks. But even if the Irish border and divorce bill issues are solved, EU citizens rights in UK will remain a sticky point. It's reported that EU is insisting that UK must stay within European Court of Human Rights, so that EU citizens in UK are protected, or, there will be no talk on trade deal.

BoJ Kuroda hails YCC as sustainable framework

BoJ Governor Haruhiko Kuroda hailed that the central bank's yield curve control is a "sustainable" framework, effective in pushing down long term interest rates. He pointed out that the program has ended deflation in the country and boosted the economy. Also, he noted that "BOJ's bond buying has been conducted in a smooth manner so far. The risk of us facing problems in terms of buying bonds will be small for the time being." Though, he added that "in accordance with changes in the economy, prices and financial conditions, we will consider where our short- and long-term rate targets should be to create an appropriate shape of the yield curve." Kuroda also reiterated that BoJ will continue to "persistently pursue powerful monetary easing".

AUD staying weak as trade surplus shrank

Aussie follow closely as the third weakest for the week. Yesterday's GDP data miss showed weak household consumption and wage growth. Today's trade balance data is not giving any support neither. Trade surplus narrowed sharply to AUD 0.11b in October, missing expectation of AUD 1.41b. The result was driven by a steep -3% slide in exports and 2% jump in imports. Slump in iron ore sales, which tumbled -10% to AUD 7b contributed a large part to the contraction in exports. Coal exports also dropped -3% mom to AUD 4.3b.

China foreign exchange reserves rose for 10 straight month

China's foreign exchange reserves increased for the 10th month in a row to USD 3.1193T at the end of November. That represents an increase of USD 10b from a month early. The State Administration of Foreign Exchange (SAFE) noted that cross-border capital flows were kept stable thanks the strength of the economy and structural adjustments. And in turn, the steady international balance of payments supported gradual rebound in reserves. Meanwhile, there has been concern of capital out flow last year which resulted in China's forex reserves dipping below USD 3T briefly back in January. But a bottomed was formed there as economic outlook improved.

IMF warns of China financial system risks

The International Monetary Fund published as assessment on financial system stability of China today. In the report, IMF warned that "the system's increasing complexity has sown financial stability risks." And it urged that "holding more capital would strengthen the banking system and bolster financial stability." Three tensions in the system are identified. The first one being surge in risk credits as debt-to-GDP ratio jumped from 180% in 2011 to 255.9% by Q2 of 2017. Second tension is that lending has shifted away from traditional banks to the shadow banking sector, the less-regulated part of the system. That makes supervision increasingly difficult. Moral hazard and excessive risk-taking is seen as the third with the expectation that the government with bail out state-owned enterprises and financial institutions in case of troubles. The People's Bank of China responded by disagreeing some points even though the recommendations are "highly relevant in the context of deepening financial reforms" in China.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9844; (P) 0.9865; (R1) 0.9894; More....

USD/CHF's rally from accelerates to as high as 0.9940 so far and intraday bias remains on the upside for 1.0037 resistance. Firm break there will confirm resumption of whole rise from 0.9420 and target 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115 next. On the downside, below 0.9871 minor support will dampen the immediate bullish case and turn intraday bias neutral first.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance Oct | 0.11B | 1.41B | 1.75B | 1.60B |

| 05:00 | JPY | Leading Index CI Oct P | 106.1 | 106.1 | 106.4 | |

| 06:45 | CHF | Unemployment Rate Nov | 3.00% | 3.10% | 3.00% | |

| 07:00 | EUR | German Industrial Production M/M Oct | -1.40% | 1.00% | -1.60% | |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | 735B | 745B | 742B | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 F | 0.60% | 0.60% | 0.60% | |

| 12:30 | USD | Challenger Job Cuts Y/Y Nov | 30.10% | -3.00% | ||

| 13:30 | CAD | Building Permits M/M Oct | 3.50% | 1.70% | 3.80% | 4.90% |

| 13:30 | USD | Initial Jobless Claims (DEC 02) | 236K | 241K | 238K | |

| 15:00 | CAD | Ivey PMI Nov | 63.8 | |||

| 15:30 | USD | Natural Gas Storage | -33B |

Politics to Carry Markets into Year End

US Futures Higher After Wednesday's Tech Rebound

US futures are pointing to a slightly higher open on Thursday, as yesterday's rebound in tech stocks gave the impression that the buy the dip mentality remains in play.

The end of the year is likely to be dominated by political stories, with central banks not looking to rock the boat and a Federal Reserve rate hike next week all but priced in. Any shocks could shake things up in the markets but I think this is unlikely at this stage. A number of central banks have already made their move – ECB extended QE to next September, Bank of England raised interest rates, Bank of Canada raised rates twice – and have signalled an intention to wait and see before making any other changes.

US Tax Reform and Brexit to Dominate into Year End

The political picture has become more interesting, with Donald Trump's pledge on tax reform making progress in Congress. There is some optimism that a plan that could pass in the House and the Senate could be agreed by the end of the year, although time is running out. As ever, there are other political distractions when it comes to Trump – North Korea, Russian links investigation and now Jerusalem – but as it stands these are having minimal impacts on the market, although each have the potential to should they take a negative turn.

Over the next week Brexit negotiations are likely to have an impact on the UK market, as the two sides struggle to find a solution on the Irish border that appeases all involved. The EU has stated that this is one of the three issues that must be resolved before talks progress to trade and transition arrangements but with the self-imposed deadline fast approaching for this to be wrapped up this year, it's going to be very tight.

The pound is under pressure again today and is on course for a fifth consecutive daily decline against the dollar. It previously hit two month highs on the hope that the UK and EU were close to a deal on phase one, but most of these gains have since been given up and we're now closing back in on 1.3350, a level that had previously been a ceiling for the pair.

GBPUSD Daily Chart

To make matters worse, the grumblings within Theresa May's own government are once again getting louder and there are increasingly suggestions that she could be on borrowed time. It's difficult to see how this could be a positive move for negotiations and therefore a deal being reached in time, something the EU is very aware of and may work in her favour, but also another thing the pound is likely to be vulnerable to.

Bitcoin Eyes $15,000 Only a Week After Hitting $10,000 For the First Time

Bitcoin is on the rise once again on Thursday and is poised to hit $15,000 only 8 days after reaching $10,000 for the first time. Bitcoin is now up more than 25% since yesterday morning, a phenomenal climb that continues to baffle most watchers. Prior to hitting $10,000, Bitcoin had been on a remarkable run, rising more than 900% since the start of January, the kind of move that many may never see again. And yet this pales in comparison to what we've seen since then and the last two days has been extraordinary.

Bitcoin Daily Chart

Source – Thomson Reuters Eikon

The cryptocurrency has undoubtedly come on leaps and bounds this year but it's difficult to see anything move as Bitcoin has and not fear a devastating bubble bursting. I don't think it's a coincidence that Bitcoin has been making headlines over the last week or so, during which time it's risen another $5,000, or 50%. If speculation is playing as big a role in the latest moves as some expect, then very interesting times may lie ahead. Although as is always the case, this could rise a lot more before the bubble bursts. It will be interesting to see what happens once Bitcoin futures are launched on CBOE and CME and traders are given the chance to short, should they be brave enough.

Sterling Struggles to Keep Afloat; Gold Tumbles

This is certainly shaping up to be a painful trading week for the British Pound, as fears mount over the lack of progress in Brexit talks.

The lingering disappointment from Prime Minister Theresa May's failure to secure a Brexit deal on Monday, can still beis still reflected in Sterling's depressed price action today. With the E.U's chief Chief negotiatorNegotiator, Michel Barnier, giving the British government only 48 hours to agree on a potential deal, May is under renewed pressure to solve the deadlock over the Irish border. Although some remain cautiously optimistic of May securing a deal with the DUP, Sterling is still at risk of depreciating further, if Britain is unable to achieve a potential agreement by Friday. An unfavourable situation where Brexit talks are delayed until 2018, is likely to translate to further pain for the already vulnerable British Pound.

From a technical standpoint, the GBPUSD is struggling to keep afloat on the daily charts, with prices trading towards 1.3360 as of writing. Although prices are trading above the daily 50 Simple Moving Average, the bullish daily channel is at risk of becoming invalidated below 1.3340. Sustained weakness below the 1.3400 minor resistance level is likely to encourage a further decline towards 1.3350 and 1.3300, respectively.

Global stocks edge higher, but for how long?

Global stocks were under pressure during Wednesday's trading session, as geopolitical risk and falling oil prices eroded investor appetite for risker assets.

Interestingly, Asian equities closed mixed today while European stocks ventured higher, as investors redirected their focus on the U.S tax reforms and Brexit developments. With European markets are back in the green territory, and the positive momentum could trickle down into Wall Street later this afternoon. While stock markets could edge higher as investor sentiment improves, the upside may face some headwinds if participants adopt a cautious approach ahead of Friday's NFP report issuance.

Dollar flexes on U.S tax reform optimism

The Greenback appreciated against a basket of major currencies on Thursday, thanks to a renewed sense of optimism on U.S tax reforms.

With the U.S Senate Republicans agreeing to a discussion with the House of Representatives on a major tax reform bill, some investor anxiety over potential obstacles and complications has dissipated. The growing optimism over lawmakers potentially agreeing on a final bill before the 22nd of22 December deadline, could continue supporting the Dollar.

Taking a look at the technical picture, the breakout above 93.50 on the Dollar Index could encourage an appreciation towards 93.80 and 94.00, respectively.

Commodity spotlight - Gold

Gold found itself under intense selling pressure during Thursday's trading session, amid a strengthening U.S Dollar.

The yellow metal has tumbled to its lowest level in four months at $1255 and may be in store for more punishment, thanks to rising optimism over U.S tax reforms. Bears are currently in the building with further downside on the cards if Friday's NFP report exceeds market estimations. From a technical standpoint, Gold turned bearish on the daily charts after prices secured a daily close below $1267. Previous support at $1267 could transform into a dynamic resistance, that encourages a decline towards $1250.

Canadian Dollar Slide Continues as BoC Holds Steady

The Canadian dollar has posted losses in the Thursday session. USD/CAD is trading at 1.2832, up 0.36% on the day. On the release front, Canada will release Building Permits and the Ivey PMI. The US publishes unemployment claims, which are expected to tick up to 239 thousand. On Friday, the US publishes three key employment indicators – Average Hourly Earnings, Nonfarm Employment Change and the unemployment rate. The week wraps up with the release of UoM Consumer Sentiment.

The Bank of Canada did not pull any surprises on Wednesday, and maintained the benchmark rate at an even 1.00%. The Canadian dollar lost ground after the rate announcement, which was dovish in tone. The Bank said that there was slack in the labor market, and investors took this as a sign that a January rate hike was less likely. Another uncertainty facing the BoC is NAFTA, as a protectionist-minded US administration has threatened to torpedo the free-trade agreement unless Canada and Mexico make major concessions. An additional headache for the BoC is that the Federal Reserve is expected to raise rates in December and January. The BoC will have to follow suit with a raise of its own, or watch the Canadian dollar head lower against the greenback.

The ADP nonfarm employment report came in as expected, with a gain of 190 thousand. Still, this was a soft reading compared to the previous release, which showed a gain of 235 thousand. Attention now turns to the official nonfarm employment change release on Friday. Again, the markets are expecting a soft landing, with a forecast of 200 thousand, down from 261 thousand in the October release. If nonfarm payrolls, one of the most important indicators, is weaker than expected, the US dollar could lose ground.

CAC Inches Lower, Markets Eye Draghi Press Conference

The CAC is unchanged in the Thursday session. Currently, the index is at 5375.50, down 0.11% on the day. On the release front, France's trade deficit climbed to EUR 5.0 billion, higher than the estimate of EUR 4.7 billion. Eurozone Revised GDP for the third quarter posted a respectable gain of 0.6%, unchanged since the first quarter of 2017. ECB President Mario Draghi will host a press conference presented by the Bank for International Settlements in Frankfurt. The markets will be looking for clues regarding future monetary policy moves. On Friday, France releases Industrial Production, with an estimate of -0.1%. The US publishes Nonfarm Employment Change, which is expected to soften to 198 thousand.

France's economy continues to grow in 2017. On Tuesday, French Final Services PMI looked sharp, punching above the symbolic 60-point level. This marked the indicator's highest level since May 2011. The strong reading is indicative of strong expansion, as the service sector has been buoyed by strong customer demand and strong economic conditions. French service providers remain optimistic that activity in the sector will increase in the upcoming 12-month period. The French economy has rebounded in impressive fashion in 2017, and looks to wrap up the year on firm footing, as a strong manufacturing sector has triggered improved job growth.

It's been an excellent 2017 for the eurozone, as the bloc's economy has posted its best growth in years. The manufacturing sector continues to expand, exports have surged and unemployment continues to head lower. The latest ECB economic forecast is predicting GDP of 2.2% in 2017 and inflation of 1.2%. Things are so good that the ECB finally acted and tapered its asset purchase program, although it did extend the program until September 2018. Still, the cautious ECB said on Wednesday that it was concerned about "increased risk-taking behavior in global financial markets" as this could lead to sharp asset price corrections. The ECB is also keeping its eye on political uncertainty in Europe, notably the deadlocked Brexit negotiations and the political vacuum in Germany. In the meantime, European stock markets remain at high levels and the CAC could make further gains if French numbers continue to point upwards.

Dollar Gains on Tax Reforms Momentum; Stocks Climb on Tech Recovery

Here are the latest developments in global markets:

Forex: The dollar index moved higher to a fresh two-week high of 93.73 (+0.13%) as a layer of uncertainty was removed after the US Senate Republicans and the House of Representatives agreed yesterday to continue talks on tax reforms. However, risks remain on the side of the government budget which expires on Friday midnight. Dollar/yen was last seen at 112.70 (+0.37%), dollar/swissie was trading at a two-week high of 0.9922, while dollar/loonie was hovering around 1.2826 (+0.30%). The euro and the pound were pressured by a stronger dollar as readings on the UK house prices and final Eurozone GDP growth figures came in as expected. The kiwi, remained the worst performers of the day.

Stocks: European equity indices surged as tech shares recovered after a strong sell-off in previous days, while a rebound in tech stocks was also noticed in Asian markets and Wall Street earlier. The benchmark STOXX 600 was 0.36% up at 1040GMT, the German DAX 30 performed the best among its European peers, surging by 0.64% and the French CAC 40 gained 0.34%. The British FTSE 100 posted gains for the second consecutive session (+0.09%), driven by telecommunication services, while a weaker pound provided further support. US futures were heading lower.

Commodities: Oil futures climbed during early European trading hours as the market become oversold. WTI crude jumped by 0.35% on the day to $56.20 per barrel and Brent rose by 0.47% to $61.60. Gold tumbled by 0.68% to $1,255.00 per ounce on the back of a rising dollar.

Day ahead: Initial Jobless claims & Canadian PMI watched; US taxes, government budget & Brexit in focus

US and Canadian data will be for once again under the spotlight for the remainder of the day. But any updates on the reconciliation of the US tax bill and the settling of the government budget will be of main importance. In addition, investors will also weigh heavily any news on Brexit developments as the time runs out for the UK Prime Minister, Theresa May, to break the deadlock before the EU summit next week.

Initial Jobless claims out of the US at 1330GMT will likely show that applications for unemployment benefits increased by 240,000 in the week ending December 1, slightly above the 238,000 seen in the preceding week. Besides that, investors will also keep a close eye on the 4-week average gauge which adjusts for volatility, as the measure has been smoothly rising since the beginning of November. October's consumer credit will attract some attention as well at 2000GMT.

In Canada, reports on building permits for the month of October will be available at 1330GMT, with analysts predicting the gauge to halve to 1.5% m/m from 3.8% in September. At 1500GMT, the Richard Ivey School of Business will publish Canadian PMI readings for December. Recall that in November, Ivey PMI hit a 1-½ year-high at 63.8.

In terms of public appearances, the ECB Chief, Mario Draghi, will participate in a press conference by the Bank of International Settlements at the European Central Bank in Frankfurt at 1600GMT.

DAX Punches Above 13,000

The DAX index has recorded slight gains in the Thursday session. Currently, the DAX is at 13,024.50, up 0.20% on the day. On the release front, German Industrial Production declined 1.4%, well off the forecast of a 0.9% gain. Eurozone Revised GDP for the third quarter posted a respectable gain of 0.6%, matching the estimate. Later in the day, ECB President Mario Draghi will host a press conference presented by the Bank for International Settlements in Frankfurt. The markets will be looking for clues regarding future monetary policy moves. On Friday, Germany releases Trade Balance. The US will release key employment numbers, led by Nonfarm Employment Change.

A strong eurozone economy has boosted investor confidence, and European stock markets have responded with strong gains. The manufacturing sector continues to expand, exports have surged and unemployment continues to head lower. The latest ECB economic forecast is predicting GDP of 2.2% in 2017 and inflation of 1.2%. Things are so good that the ECB finally acted and tapered its asset purchase program, although it did extend the program until September 2018. Still, the cautious ECB said on Wednesday that it was concerned about "increased risk-taking behavior in global financial markets" as this could lead to sharp asset price corrections. The ECB is also keeping its eye on political uncertainty in Europe, notably the deadlocked Brexit negotiations and the political vacuum in Germany. In the meantime, European stock markets remain at high levels and the euro is enjoying the view from the 1.18 level.

The US labor market remains strong, and the last thing that investors want to see is a soft reading from Nonfarm Employment Change release. ADP Nonfarm Payrolls came in as expected on Wednesday, with a gain of 190 thousand. Still, this was a soft reading compared to the previous release, which showed a gain of 235 thousand. The markets are keeping a close eye on the official Nonfarm Employment Change report, which will be released on Friday. Again, the markets are expecting a soft landing, with a forecast of 200 thousand, down from 261 thousand in the October release. If nonfarm payrolls, one of the most important indicators, is weaker than expected, global stock markets could respond with losses.