Sample Category Title

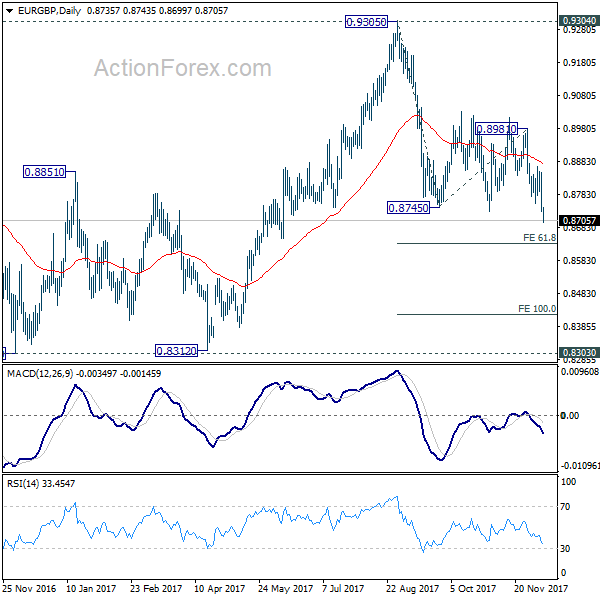

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8696; (P) 0.8773; (R1) 0.8812; More...

EUR/GBP drops sharply to as low as 0.8699 so far. Firm break of 0.8732 support finally confirms resumption of fall from 0.9305. Intraday bias is back on the downside for 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first. Break will target 100% projection at 0.8151 next. On the upside, break of 0.8849 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Elliott Wave View: Nasdaq

Nasdaq Short Term Elliott Wave view suggests that Intermediate wave (3) ended at 6429.5 and Intermediate wave (4) pullback is proposed complete at 6231.75. Subdivision of Intermediate wave (4) is unfolding as a double three Elliott wave structure where Minor wave W ended at 6283, Minor wave X ended at 6391.75, and Minor wave Y of (4) ended at 6231.75. Index still needs to break above Intermediate wave (3) at 6429.5 for this view to gain validity. Until then, we still can’t completely rule out a break below Intermediate wave (4) at 6231.75 in a double correction.

Near term, cycle from 12/5 low (6231.75) is mature and expected to complete soon with Minute wave ((w)). Index should then pullback in Minute wave ((x)) to correct cycle from 6231.75 low in 3, 7, or 11 swing before Index resumes the rally. We don’t like selling the proposed pullback.

NQ_F Nasdaq 1 Hour Elliott Wave Chart

Market Morning Briefing: Dollar-Yen As Predicted

STOCKS

Dow (24211.48, +0.29%) bounced back a bit yesterday. Daily candle support is visible near 24000. A test of 24000 is possible before the index rises back towards 24600.

Dax (13034.88, +0.28%) continues to remain in its sideways consolidation mode and could spend some more time within this region. Another week could be spent in the 13200-12800 region before attempting a rise above 13200.

Nikkei (22772.53, +1.22%) bounced back sharply towards 22800 contrary to our expectation of a test of 22000 on the downside. Overall broad 23000-22000 region is holding well but Nikkei seems to be still confused on the medium term directions. We need to wait for a confirmed break on either side to get some clarity on the directional front.

Shanghai (3271.02, -0.03%) is likely to test 3250-3230 levels while below 3300. Note that 3230 is an interim support which could hold, pushing the price back towards 3300; else a fall towards 3200 or lower would come into picture, if we see a break below 3230.

Nifty (10166.70, +1.22%) bounced back sharply from levels below our mentioned 10050 and has managed a close above 10150 yesterday. Sensex (32949.21, +1.08%) on the other hand rose as expected moving up towards 33000. While important levels of 10000 and 33000 holds on Nifty and Sensex respectively, near term looks bullish.

COMMODITIES

Commodities look mixed just now. Gold and Silver have been falling and could trade low for some more time while crude prices look positive.

Gold (1251.20) has broken below immediate supports and could be headed towards 1200 in the next few sessions. A break below 1240 could take it straight down to 1200. Near term looks bearish.

Silver (15.762) has been steadily and gradually falling from levels near 17.25 since the last session of Novemnber’17. A test of 15.25-15.00 levels seems possible in the near term.

Brent (62.15) moved back to current levels instead of testing 60 on the downside. While below 64.75, the downside scope of testing 61.0-60.0 still remains. WTI (56.63) has held above our mentioned support near 56.6 and could now move up to re-test 58.

Copper (2.9700) has earlier support turned resistance near 3.0 and if that produces a rejection, prices could fall to 2.90 in the near term/

FOREX

Dollar-Index (93.823), as per expectations, has continued its rise towards resistance at 94.00 on the 3 day candles and the daily line charts. There could be a corrective dip after touching 94.00 or else, in case of a breach of 94.00, it will test resistance around 94.4-94.5 on the daily candles, from where a dip would then be likely.

Euro (1.1767) is also swiftly moving towards support on 3 day candles & daily line chart at 1.1760-1.1750 (this was earlier mentioned as 1.1775). If the Dollar Index dips from 94 we might see a hold of support for the Euro at 1.1750-1.1760; whereas if the Dollar Index moves towards 94.50, the Euro could test support at 1.17 on the daily candles.

Dollar-Yen (113.33) as predicted, is on way to test resistance at 113.40-113.50 on the daily line charts, as the Dollar Index and Euro move towards 94 and 1.175 respectively. If the above two move further towards 94.50 and 1.170 respectively, we could see Dollar-Yen rise further to test resistance around 113.80-114.00 on the 3 day and weekly line charts.

Pound (1.3478), as per our prediction, tested support yesterday reaching a low of 1.3320 and bouncing back to close at 1.3472, where it is currently trading. It can now rise towards 1.355 to test resistance on the daily candles, after which there could be another dip.

Dollar Rupee (64.575) looks set to test resistance near 64.60-64.80 as the Euro moves towards crucial support near 1.17. It could dip back towards 64.40 again after testing resistance.

INTEREST RATES

US yields are all trading higher. The 5Yr (2.14%), the 10YR (2.37%) and the 30Yr (2.77%) are back to levels seen last week and have all bounced back from support levels. The 10Yer could test 2.40% while the 5Yr and the 30Yr could be headed towards 2.20% and 2.83% respectively.

The Japan-US 10Y (2.32%) continues to remain ranged within the 2.28-2.37% region, trading along the channel resistance. The sideways movement could continue for some more time before deciding on further direction.

The German-US 10YR (-2.08%) has fallen further and looks bearish for the coming sessions. It has tested our mentioned -2.08% and could move down towards -2.10% and lower in the near term.

GBPUSD – Rallies Off Intra Day Low, Eyes 1.3549 Zone

>

GBPUSD - The pair held of lower prices to close higher on a rally on Thursday. This development has opened the door for more strength in the days ahead. Support lies at the 1.3450 level where a break will turn attention to the 1.3400 level. Further down, support lies at the 1.3350 level. Below here will set the stage for more weakness towards the 1.3300 level. Conversely, resistance stands at the 1.3500 levels with a turn above here allowing more strength to build up towards the 1.3550 level. Further out, resistance resides at the 1.3600 level followed by the 1.3650 level. On the whole, GBPUSD looks to recover higher.

On A Wing And A Prayer

On a Wing and a Prayer

No need to elaborate in detail today as the dollar is firming “on a wing” that White House press corps is correct that the Trump Administration is readying an infrastructure plan for Jan 30 and a “prayer” for a tax bill deal

While the US economy is booming, President Trump’s long-standing pledge may be upon us as infrastructure spending at both a federal and state could be a real game-changer for the dollar as the resulting massive pick up in business investment could propel the US economy to 4% growth,ceteris paribus. The headline boosted stocks and yields in late NY trading and lit a fire under the dollar bulls. The one exception was Sterling which bucked the trend dollar on reports that Prime Minister May and the DUP were close to a deal on the Irish border deadlock.

Looking forward, an extension of the latest dollar churn might all boil down to this evenings wages data with the tail risk for a hawkish inference on the employment headline. The jobs report will play a significant factor in keeping the dollar rally alive and forwarding the view of an early 2018 rate hike

Japanese Yen

The bounce in US yields was convincing enough to propel USDJPY through the 113 level and only held back by the YCC debate after Governor Kuroda recapitulated his Hawkish deterrent overnight.

Also, the long USDJPY trade appears stable as some element of diplomacy enters the NK fray.

The Pound

Apart from digesting the infrastructure stage whispers surrounding Brexit will continue to drive GBP sentiment

Gold

Predictably XAU hastened losses on this infrastructure news – as the sell the recent sell-off gathers speed as bid remain far and few between

Energy Markets

Muted trading despite the boisterous inference from the US tax reform and fiscal spend one-two punch.But perhaps fears that the Trump administration may float a gas tax to pay for infrastructure spending are presenting some headwinds?

Dollar Higher on Tax Cut Optimism Ahead of Jobs Report

The US Economy is expected to add 200,000 jobs in November

The USD is higher against most major pairs ahead of the release of the November U.S. non farm payrolls (NFP) report. Tax reform optimism have benefited the dollar, with only the pound gaining against the American currency due to a high possibility of the UK and the EU finding a way to move forward on the Irish border deadlock. Geopolitics have set the tempo in the market and while the two tax bills await becoming one pice of legislation the threat of a movement shutdown in the US has been minimized as there are signs that the House will approve legislation to prevent a weekend partial shutdown.

The first of the employment release this week dropped with the publication of the ADP private payrolls report. US private employers added 190,000 jobs, 5,000 more than expected. The U.S. Bureau of Labor Statistics will release the non farm payrolls (NFP) report on Friday, December 8 at 8:30 am EST. The economy is forecasted to have added 200,000 positions in November. Once again the emphasis will be on average hourly wages for signs on inflationary pressure. While the market has already priced in a rate hike of 25 basis points in the next Fed meeting doubts remain on what the central bank will do in 2018. Weak inflation is the biggest argument the doves within the FOMC have used to debate waiting before raising rates again. Wages are forecasted to have gained 0.3 percent in the last month after a flat reading in October.

The US job market is expected to have recovered from the effects of hurricane related volatility, but with soft inflation being a point of debate within the FOMC, strong wage growth is needed for the hawks to gain the upper hand. A survey of economists conducted by Reuters already forecasts 3 or more rate hikes in 2018 as Yellen's term as Chair ends and Jerome Powell's begins.

The EUR/USD lost 0.17 percent on Thursday. The single currency is trading at 1.1776 ahead of the release of US U.S. non farm payrolls (NFP). The USD is gaining on the back of tax cuts expectations and the performance of the stock market. With the pro-growth policies of the Trump administration on the eve of becoming a reality the market is pricing back in some of the momentum from earlier in the year. Geopolitics have complicated matters as President Trump's decision to declare Jerusalem as the new site of the US embassy has added unwanted instability to the region.

European Central Bank (ECB) head Mario Draghi was in Frankfurt to agree on the final set of rules on Banking Supervision. The set of rules were aimed at how to avoid bailouts for banks taking lessons from the Great Recession. The ECB will meet next week to announce its rate statement. The rate is expected to remain at 0 percent but given the trend of European growth there could be a surprise in the December meeting or in the first quarter of 2018. Geopolitics will be a big part of the end of the year for the EUR as the Catalan elections will take place on Dec 21.

The GBP/USD gained 0.62 percent on Thursday. The currency pair was one of the best performers on the day thanks to a new draft for the Irish border proposed. There will be a statement tomorrow as negotiations will continue to find a deal that satisfies the DUP and the Irish Government. The DUP rose in prominence thanks to the ill advised snap election called by UK Prime Minister Theresa May than rather than solidify their majority saw it almost slip away. Partnering with the Northern Irish DUP was the only way for the Conservatives to remain in power but as Ireland is part of the EU it brought the issue of the Irish border to a new level.

The EU has backed Ireland on the border dispute. The Brexit negotiations remain deadlocked until this issue is sorted. The UK is eager to move into trade negotiations as there is no current plan B in place when the divorce from the UK is official. There have been some advances as the two parts are closer than they were after the referendum was voted on, but issues like the Irish border need to be sorted before moving on.

Market events to watch this week:

Friday, December 8

- 4:30am GBP Manufacturing Production m/m

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

- 8:30am USD Unemployment Rate

*All times EDT

Gold Falls to 4-Month Low as Jobless Claims Dip Lower

Gold has posted sharp losses in the Thursday session. In North American trade, the spot price for an ounce of gold is $1252.92, down 0.84% on the day. It's been a tough week for gold, which has declined 1.6% and is at its lowest level since August 8. On the release front, unemployment claims dipped to 236 thousand, below the estimate of 239 thousand. On Friday, the US releases three key employment indicators – Average Hourly Earnings, Nonfarm Employment Change and the unemployment rate. We'll also get a look at consumer confidence, with the release of UoM Consumer Sentiment.

US employment numbers have been steady this week, as unemployment claims and ADP nonfarm payrolls both beat their estimates. However, a tough test looms on Friday, with the release of nonfarm payrolls and wage growth. The ADP reading slowed considerably compared to the previous release, and the markets are predicting the same trend for nonfarm payrolls, which is expected to come in at 190 thousand. As one of the most important indicators, nonfarm payrolls could shake up the markets, so traders should be prepared for some movement from GBP/USD in Friday's North American session. Wage growth has been stubbornly, despite a strong labor market and assurances from Fed policymakers that inflation and wages will move upwards. The markets are expecting some good news on Friday, with Average Hourly Earnings expected to gain 0.3%. The October reading of 0.0% was a disappointment, missing the forecast of 0.2%.

The markets are widely expecting the Federal Reserve to continue to raise rates in the near future, and this sentiment continues to weigh on gold prices. The odds on upcoming rate hikes continues to fluctuate. Currently, the CME has priced in December and January hikes at 90% and 88%, respectively. If the US economy continues to perform at its impressive pace into 2018, we could see the Fed raise rates up to three times next year.

Could Americans See Higher Wages Further Ahead?

Markets are widely expecting the Fed to finish the year with a third-rate hike in December as the US economy grows above expectations and the unemployment rate is currently at the lowest tracked since 2000. Hence, the NFP report released this Friday is less likely to change the Fed's mindset at next week's policy meeting. However, what could be worthy of attention are the wage growth numbers which policymakers are closely watching to appraise inflationary pressures and thus whether they are on the right path with interest rate increases.

On Wednesday, the ADP Research Institute released private-sector nonfarm payrolls. These are considered by some as a preview of the more comprehensive government nonfarm payrolls which are due on Friday at 1330GMT. The ADP report showed that the private sector added 190,000 positions in the economy in November – slightly above expectations – compared to an eight-month high of 235,000 seen in the previous month. Nonfarm jobs created published by the Labour Department are also projected to narrow in November, falling from a 16-month high of 261,000 to 200,000. Besides that, average hourly earnings released with the jobs numbers are forecast to grow by 0.3% m/m in the given period after remaining stable in the preceding month, while the unemployment rate will likely stand pat at a 17-year low of 4.1%.

It should be mentioned that the rise in nonfarm payrolls and the slowdown in wage growth in October was mainly attributed to the return of workers to low-paying industries such as leisure and hospitality, as those employees remained temporarily unemployed in September in the face of catastrophic weather phenomena.

The labor market is currently considered to be operating near full-employment conditions. Subsequently, the Federal Reserve is hoping that a tighter jobs market would spur wage growth pressures, translating into higher inflation. Should subdued wages persist though, inflation would likely remain below the Fed's target of 2.0% for longer. Such an outcome is expected to make Fed policymakers rethink delivering three rate hikes in 2018, as they currently forecast.

But still, the Fed remains optimistic that a tighter labour market resulting in higher earnings could be achieved given that GDP growth has overshoot past forecasts this year. The last reading in Q3 showed annualized growth reaching 3.3%, its highest in three years.

In the forex markets, the dollar turned neutral versus the yen after it found support at the 111 key-level. If average hourly earnings surprise to the upside on Friday, immediate resistance could be met at the 113 key-level, which is also the 23.6% Fibonacci of the upleg from 107.31 to 114.72. Any violation of this point would turn the bias from neutral to bullish, opening the scope for a re-test at the 9-month high of 114.72. Alternatively, disappointing wage growth numbers could push prices down to 111.88 (38.2% Fibonacci), with stronger bearish movement shifting focus to the 111 key-level (50% Fibonacci).

Pound Edges Higher on Positive UK Inflation Report

The British pound has posted small gains in the Thursday session. In North American trade, GBP/USD is trading at 1.3413, up 0.15% on the day. On the release front, British Halifax HPI gained 0.5%, beating the estimate of 0.2%. In the US, unemployment claims dipped to 236 thousand, below the estimate of 239 thousand. Friday will be busy, with a host of key events. The UK will publish Manufacturing PMI. The US releases three key employment indicators – Average Hourly Earnings, Nonfarm Employment Change and the unemployment rate. We'll also get a look at consumer confidence, with the release of UoM Consumer Sentiment.

US employment numbers have been steady this week, as unemployment claims and ADP nonfarm payrolls both beat their estimates. However, the stiffer test is on Friday, with the release of nonfarm payrolls and wage growth. The ADP reading slowed considerably compared to the previous release, and the markets are predicting the same trend for nonfarm payrolls, which is expected to come in at 190 thousand. As one of the most important indicators, nonfarm payrolls could shake up the markets, so traders should be prepared for some movement from GBP/USD in Friday's North American session.

Ireland is in the spotlight on both sides of the Channel, as the UK and European Union scramble to find a solution to the vexing question of the status of the Irish border after Brexit. An embattled Prime Minister May is desperate to move on to trade talks with the EU, but the Europeans want to wrap up the non-trade issues first. There had been hopes of a major announcement following a meeting between Prime Minister May and European Commission President Jean-Claude Juckner. However, these expectations were left on hold, as it became apparent that wide gaps remain on two key issues – Northern Ireland and the European Court of Justice. The European Union is willing to let EU rules apply to Northern Ireland, but the small DUP party, which is keeping the May government afloat, is against any steps which could be seen as separating the UK mainland from Northern Ireland. A solution that will satisfy the UK, the EU and the DUP over the Irish border remains elusive. Another thorny issue is whether the European Court of Justice will apply to European citizens in the UK after Brexit. While the EU is in favor of the court having authority over these citizens, many British lawmakers feel that such a move would undermines British sovereignty. The EU holds a key summit on December 12, and all sides are hoping to wrap up the non-trade sticking points before the meeting.

USD Growing in Anticipation of Tax Cut Approvals in the US

The EUR/USD kept falling on the background of hopes linked to successful negotiations on tax cuts in the US. If the bill on fiscal stimulation passes, we are likely to see further strengthening of the USD against other major world currencies. The news on the strong GDP growth in the Eurozone by 0.6% in the fourth quarter was not able to change the mood of traders. Trader activity is also restrained by the expectation of the release of important data on the labor market in the US that will impact the FOMC decision on the rate hike at its next meeting. Positive statistics are likely to raise the bullish sentiment on the market, which will support the EUR/USD bears.

The Canadian dollar has weakened despite the recent hawkish rhetoric of the Bank of Canada during yesterday's statement on monetary policy, according to which the growth in investments and wages are among positive factors that may lead to a rate hike during 2018. In 2017, the key interest rate in Canada was increased twice and is currently at 1.0%.

The AUD/USD remains under pressure from unexpectedly weak trade balance data in the country, according to which the trade surplus was only 0.11 billion in October against the 1.37 billion forecasted. Volatility is likely to remain high due to tomorrow's release of trade balance data in China which traditionally has a significant influence on the AUD/USD quotes. Today we should also pay attention to the reports on the Japanese current account balance and GDP growth at 23:50 GMT.

EUR/USD

The EUR/USD price keeps moving along the upper limit of the local descending channel. The closest targets in case of maintaining the current impulse will be at 1.1730 and 1.1620. In order to change the bearish trend, the price needs to fix above the 1.1800 mark. In this scenario, the closest goals will be located at 1.1825 and 1.1925.

USD/CAD

The USD/CAD quotes are growing fast after an unsuccessful attempt to fix under 1.2665. Gaining a foothold above 1.2000 may be the basis for price growth up to 1.2915 and 1.3000. At the same time, we do not exclude the rollback on the background of profit taking with the fall potential to SMA100 on the 15-minute chart.

AUD/USD

The AUD/USD quotes fell to the strong support at 0.7520 and after a sharp decline, we may see the price rebound to the 0.7550-0.7565 range. The MACD signal line on the 15-minute chart has changed direction to positive, which together with the RSI on the 15-minute chart being near the oversold zone, may result in an upward correction. In case of the price declining lower than 0.7500, the next objective will be at 0.7440.