Sample Category Title

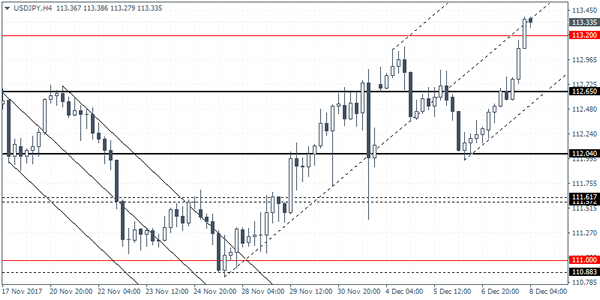

USDJPY Intraday Analysis

USDJPY (113.33): The U.S. dollar posted strong gains following the rebound off the 112.00 level of support. Price action remains biased to the upside especially after breaching the 113.20 level of resistance. In the near term, USDJPY could be seen pushing back lower to retest the support at 112.65 support. Establishing support at this level could signal further upside in price. However, in the event that USDJPY slips below 112.65, we could expect to see the declines pushing lower towards the 112.04 lower support.

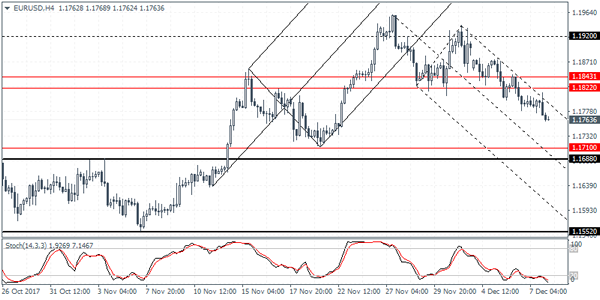

EURUSD Intraday Analysis

EURUSD (1.1763): The EURUSD continued to post declines to the downside for the third consecutive day. Price action is seen nearing the support level at 1.1704. This will see a retest of the support level which previously served as a break out from the descending wedge pattern that was formed. In the near term, EURUSD's gains are limited to the 1.1843 - 1.1822 level where resistance could be formed. To the downside, the declines could see EURUSD push lower towards the support level at 1.1710 - 1.1688.

November Payrolls To Set The Tone For The Markets

The U.S. dollar was seen strengthening on the back of investor optimism that the tax benefits could help boost the economy. The U.S. dollar index rose to a one-month high ahead of the payrolls report that is due to be released later today.

Economists polled expect to see the U.S. unemployment rate staying steady at 4.1% while wage growth is expected to accelerate. The payrolls report comes ahead of next week's Fed meeting where interest rates are widely expected to be hiked.

In the UK, the British pound continued to trade volatile on the Brexit related news. Manufacturing production and construction output data is expected to be released today. Forecasts put the manufacturing production to rise just 0.1% on the month while, construction output is expected to rise 0.2%.

Sterling Soars as Brexit Talks Close to Completing First Phase, Dollar Turns to Non-Farm Payroll for More Strength

Dollar remains generally strong today, but it's over powered by Sterling. The Pound is lifted by optimism that Brexit negotiation is finally close to completing the first phase. It's reported that the Irish border issue is solved with UK Prime Minister Theresa May's new proposal. And she's flying to Brussels again today to complete the talks. Dollar will look into today's non-farm payroll report for the fuel for further rally. Elsewhere in the currency markets, Yen and Swiss Franc are trading as the weakest ones today.

NFP expected to grow 200k, eyes on wage growth

Economists are expecting NFP to show 200k growth in November. Unemployment is expected to be unchanged at 4.1%. Average hourly earnings are expected to rise 0.3% mom. Looking at other employment related data, ADP report showed 190k growth in private jobs, down fro October's 235k. ISM manufacturing employment dropped 0.1 to 59.7. ISM non-manufacturing employment dropped 2.2 to 55.3. Four week average of initial jobless claims rose 11k to 242k. Continuing claims rose 0.01m to 1.91m. Conference board consumer confidence improved to 129.5, hitting the highest level since December 2000.

Overall, job related data pointed to rather healthy underlying growth momentum. And, 200k headline NFP should be easily met. The surprises today could be found in unemployment rate which may dropped further. And more importantly, wage growth would be the key market driver. Considering that average hourly earnings growth was at 0.0% mom back in October, a 0.3% mom growth in November looks achievable.

Technically, Dollar is looking very firm against Aussie, Canadian and Swiss Franc. USD/JPY's break of 113.08 overnight also suggests underlying upside momentum and would likely target 114.73 resistance again. However, GBP/USD managed to rebound strongly after breaching 1.3337 support. And that' should resilience of Sterling. The bigger question lies in EUR/USD which is holding above 1.1712 support and maintains bullishness. However, in case of dollar rally after NFP, firm break of 1.1712 will align EUR/USD with other dollar pairs expect GBP/USD. In that case, we'll likely see Dollar gains broad based momentum.

US Congress passed two week funding extension

US Congress passed two-week extension of federal funding that avoids a partial government shutdown this week. House voted 235 to 193 for the extension while Senate voted 81 to 14. This gives lawmakers a bit more time to finish the work on spending and legislation till December 22. At the same time, they will also be working on the tax reform, rushing to reconcile the differences between House and Senate version, and pass them in respective chambers before year end holidays.

Brexit negotiations close to complete first phase, May to meet Juncker

Quick update: Juncker declared that "sufficient progress has now been made on the three terms of the divorce." And negotiation can move on to trade agreements.

UK Prime Minister Theresa May would likely rush to Brussels today and meet European Commission President Jean-Claude Juncker at around 7am local time to resume Brexit negotiations. It's reported that after a night of intensive talk and phone calls, May is closing on a deal on Irish border, with support from her Northern Ireland partner DUP. The second issue on divorce bill should have been agreed for some time already. Meanwhile, it's believed that UK and EU have also agreed on the third issue, the role of European Court of Justice in British legal cases after Brexit. So, Brexit negotiation should be ready to move on to the next stage of trade talks.

Sterling was given a boost in Asian session today. In particular, EUR/GBP has taken out 0.8732 support to finally resume recent decline from 0.9305. GBP/JPY also broke 152.93 to resume the rise from 139.29. Pound traders will now eagerly await the post meeting press briefing of May and Juncker to confirm this optimism.

Japan GDP grew 0.6% qoq in Q3, doubled initial estimate

Japan GDP growth was finalized at 0.6% qoq in Q3, double the pace of initial estimate of 0.3% qoq. Annualized rate was 2.5%. GDP deflator was finalized at 0.1% yoy, unchanged. The data showed that Abenomics and BoJ's easing have definite boosted growth, but is so far having little impact on lifting inflation. Also from Japan current account surplus widened to JPY 2.44T in October. Labor cash earnings rose 0.6% yoy, below expectation of 0.8% yoy.

China trade surplus widened to USD 40.2b in November, up from USD 38.2b and above expectation of USD 34.9b.Exports rose 12.3% yoy while imports also surged 18% yoy. In Yuan, trade surplus widened to CNY 264b, up fro CNY 254b and beat expectation of CNY 238b. Also from Asia Pacific, Australia home loans dropped -0.6% mom in October. New Zealand manufacturing activity rose 0.5% in Q3.

Looking ahead

UK trade balance, productions and German trade balance are the main features in European session. US will release NFP and U of Michigan sentiment. Canada will release housing starts.

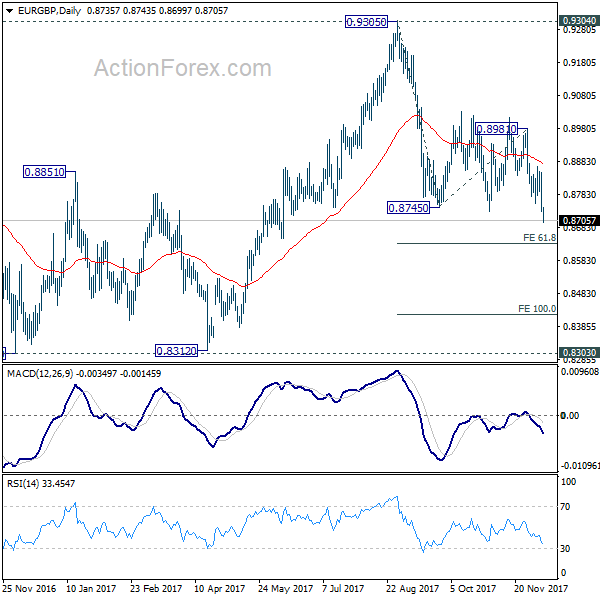

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8696; (P) 0.8773; (R1) 0.8812; More...

EUR/GBP drops sharply to as low as 0.8699 so far. Firm break of 0.8732 support finally confirms resumption of fall from 0.9305. Intraday bias is back on the downside for 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first. Break will target 100% projection at 0.8151 next. On the upside, break of 0.8849 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q3 | 0.50% | 3.90% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) Oct | 2.44T | 1.93T | 1.84T | |

| 23:50 | JPY | GDP Q/Q Q3 F | 0.60% | 0.40% | 0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | 0.10% | 0.10% | 0.10% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Oct | 0.60% | 0.80% | 0.90% | |

| 0:30 | AUD | Home Loans M/M Oct | -0.60% | -2.00% | -2.30% | -2.50% |

| 3:13 | CNY | Trade Balance (CNY) Nov | 264B | 238B | 254B | |

| 3:36 | CNY | Trade Balance (USD) Nov | 40.2B | 34.9B | 38.2B | |

| 7:00 | EUR | German Trade Balance (EUR) Oct | 22.3B | 21.8B | ||

| 9:30 | GBP | Industrial Production M/M Oct | 0.00% | 0.70% | ||

| 9:30 | GBP | Industrial Production Y/Y Oct | 3.50% | 2.50% | ||

| 9:30 | GBP | Manufacturing Production M/M Oct | 0.00% | 0.70% | ||

| 9:30 | GBP | Manufacturing Production Y/Y Oct | 3.80% | 2.70% | ||

| 9:30 | GBP | Construction Output M/M Oct | 0.10% | -1.60% | ||

| 9:30 | GBP | Visible Trade Balance (GBP) Oct | -11.5B | -11.3B | ||

| 13:00 | GBP | NIESR GDP Estimate Nov | 0.40% | 0.50% | ||

| 13:15 | CAD | Housing Starts Nov | 221K | 223K | ||

| 13:30 | CAD | Capacity Utilization Rate Q3 | 85.20% | 85.00% | ||

| 13:30 | USD | Change in Non-farm Payrolls Nov | 200K | 261K | ||

| 13:30 | USD | Unemployment Rate Nov | 4.10% | 4.10% | ||

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.30% | 0.00% | ||

| 15:00 | USD | U. of Mich. Sentiment (Dec P) | 99 | 98.5 |

Forex: Chinese & Japanese Data Impresses, Markets Await US Data

Data released earlier today showed that Chinese trade data beat expectations in November, with strong annual import and export growth as well as a higher trade surplus. Data from China’s General Administration of Customs showed November imports grew, in USD terms, by 17.7% (prev. 17.2%) and November exports grew, in USD terms, to an impressive 12.3% (prev. 6.9%), with both datasets beating market expectations. China’s trade surplus closed out the trio, with the data showing it grew to $40.21B (prev. $38.17B), beating market forecasts for a decline to $35B. The data helped lift the Yuan along with AUD and NZD.

Further impressive data from the region came from Japan, with revised data indicating that Asia’s second-largest economy expanded at an annualized 2.5% in Q3. GDP beat market forecasts of 1.5% due to stronger than expected business investment and rising inventories, while demand perked up. Japanese Prime Minister Shinzo Abe was expected later Friday to outline his plans for longer-term efforts to improve both growth and productivity.

GBP moved higher overnight on reports that an agreement is imminent after it was reported that European Council President Donald Tusk will make a statement on Brexit early on Friday morning, suggesting that Prime Minister May had made progress on the Irish border issue. PM May, European Commission President Jean-Claude Juncker and Irish PM Leo Varadkar have held several calls, with Juncker’s spokesman commenting that “an early morning meeting and press point on Friday was possible” and “We are making progress but not yet fully there. Talks are continuing throughout the night.”

The markets are now waiting in anticipation for today’s US Non-Farm Payrolls Report, Unemployment and Average Hourly Earnings data due out at 13:30 GMT.

EURUSD is little changed overnight, trading around 1.1762.

USDJPY is 0.25% higher in early Friday trading at around 113.36.

GBPUSD is 0.15% higher overnight, trading around 1.3493.

Gold is 0.1% higher in early session trading at around $1,248.5, after trading as low as $1,246.89 earlier on Friday.

WTI is unchanged overnight trading around $56.70.

Major data releases for today:

At 07:00 GMT: Statistisches Bundesamt Deutschland will release German Trade Balance s.a. data for October. The trade balance is forecast to have fallen slightly to €21.5B from the previous reading of €21.8B.

At 09:30 GMT: the UK Office of National Statistics will release Manufacturing Production and Industrial Production (MoM & YoY) for October. Manufacturing month-on-month is forecast to come in at a paltry 0.1% (prev. 0.7%) with the annualized rate expected at 3.9% (from 2.7%). Industrial Production is forecast to come in at 0.1% from the previous 0.7% (MoM) and the annualized rate is forecast at 3.6% from the previous 2.5%. Any significant deviation from forecasts will see GBP volatility.

At 13:30 GMT: the US Department of Labor will release Non-Farm Payrolls, the Unemployment rate and Average Hourly Earnings for November. Unemployment is expected to hold steady at 4.1% and the always impactful NFP is forecast at 200K from the previous 261K. Average earnings were 2.4% previously and are expected to have increased annualized to 2.7%. Any significant deviation from the forecast will result in USD volatility.

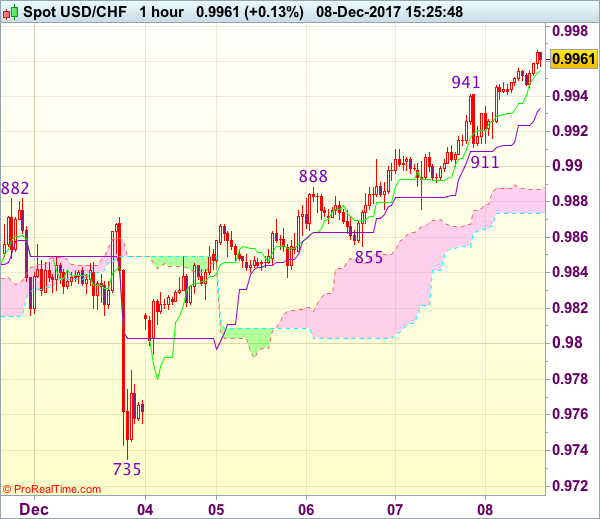

Trade Idea : USD/CHF – Buy at 0.9900

USD/CHF - 0.9961

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9954

Kijun-Sen level : 0.9933

Ichimoku cloud top : 0.9887

Ichimoku cloud bottom : 0.9874

Original strategy :

Buy at 0.9825, Target: 0.9925, Stop: 0.9790

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9900, Target: 1.0000, Stop: 0.9865

Position : -

Target : -

Stop : -

As the greenback has surged again after brief pullback and broke above previous resistance at 0.9947, adding credence to our bullish view that the rise from 0.9735 low is still in progress, hence test of resistance at 0.9987 would be seen, above there would encourage for headway to 1.0000, however, near term overbought condition should limit upside and reckon recent high at 1.0038 would hold from here, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and we are looking to buy dollar on dips as 0.9900 should limit downside and bring another rebound. Below previous resistance at 0.9882-88 (now support) would defer and risk correction towards support at 0.9855 but only break there would signal top is formed instead.

Where To Make Money In 2018

Key points

- We expect the global expansion to continue lending support to profits and risk assets.

- We do not project a bond bear market, though. Rather we look for more US curve flattening.

- Credit spreads are set to narrow further on a search for yield and low default rates.

- In the FX space, we look for strengthening of USD, GBP and NOK in 2018.

As 2017 draws to a close, the question increasingly on investors' minds is where they can make money in 2018. Below is a summary of our key macro and market views.

Strong global macro backdrop. Going into 2018, the global economy is in the best shape it has been in six to seven years. In The Big Picture: Global economy still on a roll, we argue that the global expansion is set to continue, albeit in a slightly lower gear than in 2017, as we expect a slowdown in China to weigh slightly on global activity. Still, the global economy is set to continue growing above the trend rate next year, driven increasingly by fixed investments, which have widely been the missing link in the global recovery until this year.

We look for core inflation in the US and euro area to increase only gradually. The main reason for this scenario is our expectation that wage demands will continue to be fairly moderate and that the Chinese slowdown will reduce the inflationary impact of commodity prices.

The benign inflation picture should allow the central bank exit to take place at a measured pace. Adding to the positive picture is the lack of big risk factors to growth at the current time. On our watch list, though, is the Italian election next year, North Korea and the tensions in the Middle East.

Equities – positive but lower returns and more volatility. The above macro environment is typically favourable for risk assets and, thus, also equities. As long as growth stays above trend and we do not see a big upward inflation surprise forcing central banks to step on the brakes, equities have outperformed bonds historically. Equities will be supported by robust profit growth even if it moderates a bit from this year. A very low level of yields on both corporate and sovereign bonds also continues to drive money into risk assets and push risk premiums even lower. In our view, the expected slowdown in the Chinese manufacturing and construction sector will cause some headwinds for emerging markets but developed markets should benefit from the capex recovery benefiting manufacturing in this area.

With some deceleration in the global cycle and risk premiums lower, we expect to see lower returns in 2018 than in 2017. In our view, volatility is also likely to pick up, as investors may feel they are skating on slightly thinner ice and, thus, are more prone to taking chips off the table if some risk factors flare up.

Euro credit – further tightening of spreads. While credit spreads are generally tight, we believe the macro backdrop points to a further search for yields and even further spread tightening in 2018. We expect defaults to be low in the expected macro environment and the ECB to continue being a buyer of corporate credit until Q4 when the QE programme ends. In our view, the risk-reward is not as good as in 2017 with the current level of spreads and hiccups are likely to happen during the year. However, we expect these to be temporary and recommend using them to buy credit.

Sovereign bonds – no big bear market. As expressed in Strategy – ‘Bond yield conundrum vol. 2’, 30 November, we do not expect a big bond bear market in 2018. While we look for yields in the short end to move higher as the Fed continues to hike rates and an ECB hike is gradually moving closer, the longer ends of the yield curves are set to be supported by a range of factors. These include: (1) inflation expectations being set to stay in check, with commodity prices cooling, (2) the central bank natural rate (the so-called r-star) having come down, (3) bond markets being very rare when the business cycle is cooling off – even when the central bank is tightening and (4) the very low yield level in Japan is the gravity of bond yields putting a cap on how high US and euro yields go as Japanese investors search for yield in global bond markets.

Consequently, we also expect the current flattening of the US yield curve to continue in 2018. It’s one of our fixed income top trades for 2018 (see Danske Bank 2018 Fixed Income Top Trades, 6 December).

FX – higher EUR/USD, lower EUR/GBP, higher NOK/SEK. We keep our longstanding view that EUR/USD will resume the move higher in 2018, as the cross is still undervalued according to our valuation model (MEVA). The bond-related portfolio outflows of the euro area are also set to turn EUR positive, as the market eyes the ECB exit.

For 2018, we also look for EUR/GBP to move lower. In our view, Brexit clarification and valuation will be supportive for GBP relative to EUR.

In Scandinavia, the key theme to play is the weakening of housing markets. The housing market in Sweden is looking fragile and, although the SEK has been beaten up lately, we expect it to trade with a ‘housing risk premium’ for some time and expect growth deceleration and the repricing of the Riksbank to continue weighing on the currency in 2018. In contrast, we see a compelling case for NOK to strengthen versus both EUR and SEK. The macro picture looks solid, the higher oil price is not yet reflected in NOK strength and the NOK is undervalued, judging from both our MEVA model and PPP. Imported inflation is also set to pick up on the back of the recent NOK weakening.

Overall, we see a compelling case for EUR/NOK to move lower in 2018. With our more bearish view on SEK, we also look for upside in NOK/SEK. For more views on the FX market, see FX Top Trades 2018: How to position for the year ahead, 6 December. Overall, we believe the best performance is still to be found in risk markets (both equity and credit) relative to government bonds. We recommend hedging US assets due to our view of a further USD weakening in 2018. In FX markets, we see opportunities in NOK and GBP, while we recommend caution in SEK.

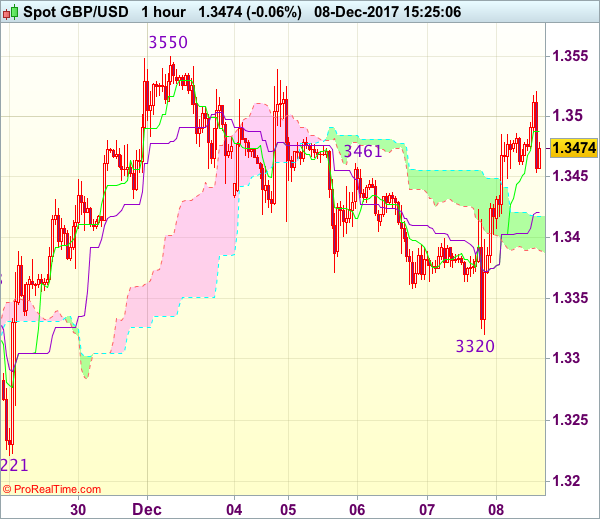

Trade Idea : GBP/USD – Stand aside

GBP/USD - 1.3487

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3488

Kijun-Sen level : 1.3421

Ichimoku cloud top : 1.3417

Ichimoku cloud bottom : 1.3390

Original strategy :

Sold at 1.3440, met target at 1.3340

Position : - Short at 1.3440

Target : - 1.3340

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite yesterday’s anticipated selloff to 1.3320, the subsequent strong rebound on active cross-buying in sterling suggests low has been formed there and further choppy trading would take place, hence gain to 1.3525-30 cannot be ruled out, however, as outlook remains consolidative, reckon upside would be limited and recent high at 1.3550 should hold, bring retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below the Kijun-Sen (now at 1.3421) would bring test of the lower Kumo (now at 1.3390) but downside should be limited to 1.3350-60 and price should stay well above said support at 1.3320, bring another rebound.

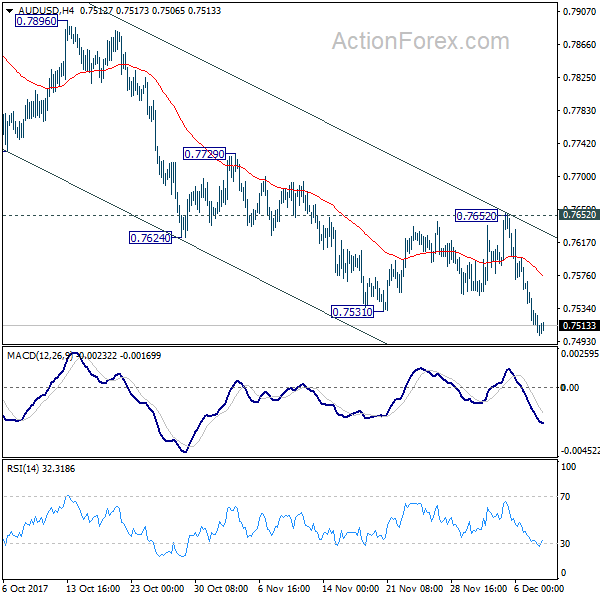

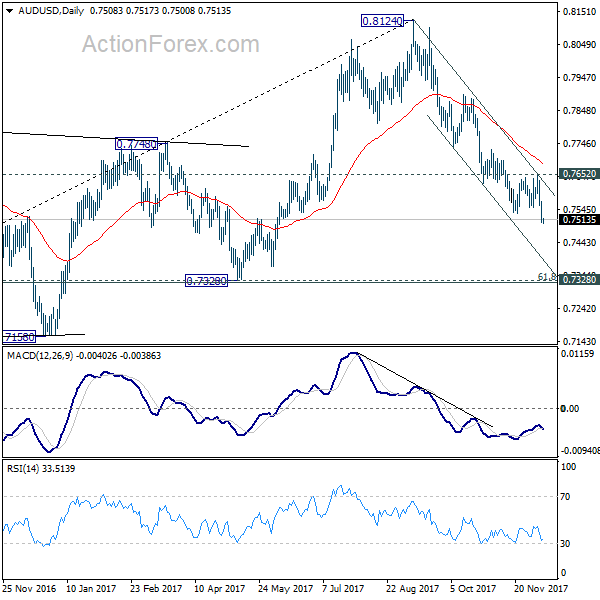

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7537; (P) 0.7584; (R1) 0.7609; More...

Intraday bias in AUD/USD remains on the downside at this point. Whole decline from 0.8124 should now extend to next key cluster level at 0.7322/8. On the upside, break of 0.7652 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8033). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

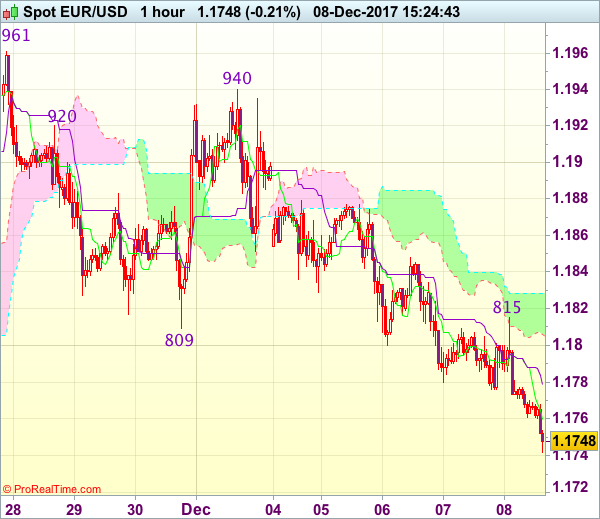

Trade Idea : EUR/USD – Sell at 1.1810

EUR/USD - 1.1749

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1760

Kijun-Sen level : 1.1779

Ichimoku cloud top : 1.1829

Ichimoku cloud bottom : 1.1806

Original strategy :

Sell at 1.1865, Target: 1.1765, Stop: 1.1900

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1810, Target: 1.1710, Stop: 1.1845

Position : -

Target : -

Stop : -

As the single currency has fallen again after brief bounce to 1.1815, adding credence to our bearish view that the erratic decline from 1.1961 top (last week’s high) is still in progress and downside bias remains for further weakness to support at 1.1736, break there would bring a test of previous key support at 1.1713 but break there is needed to retain bearishness for subsequent decline towards 1.1660-70 before prospect of a recovery due to near term oversold condition.

In view of this, we are looking to sell euro on recovery but at a lower level as said resistance at 1.1815 should limit upside and bring another decline. Above 1.1845-50 would defer and suggest low is formed, bring a stronger rebound to 1.1875-80 first.