Sample Category Title

EURUSD Turning Bearish Below 1.1828 Level

The euro is struggling to move higher against the U.S dollar, with price-action moving closer to the 1.1800 technical level, which represents the pairs 100-day moving average. The EURUSD again moved into selling pressure during the European trading session, creating a third bearish lower swing price-high. An overall lack of euro demand above the 1.1875 level has hurt EURUSD sentiment, with traders now selling upside rallies. Traders now look to the release of the U.S ADP job report for November, and news coming from the pending U.S government shutdown.

The EURUSD pair remains intraday bearish while trading below the 1.1828 level, further downside towards the 1.1800 and 1.1770 levels appears likely.

Should EURUSD price-action move above the 1.1828 technical level, further buying towards 1.1845 and 1.1875 levels seems possible. Extended intraday resistance is found at the 1.1900 level.

GBPUSD Strongly Bearish Below 1.3400 Level

The British pound has moved to a new weekly price-low against the U.S dollar, hitting 1.3360, as the Brexit stalemate weighs on the pound. The GBPUSD fell through the 1.3400 support level during the European session, sparking a technical sell-off in the pair. Brexit Secretary David Davis has confirmed that the UK and EU have yet to make any further progress, while Theresa May has yet to agree a border deal with the Irish Democratic Union Party. Traders now await the release of the ADP private sector jobs report from the United States economy.

The GBPUSD pair is strongly bearish while trading below the 1.3400 technical level, with sellers likely to test the 1.3303 level if price-action break below the 1.3360 level.

Should buyers push the GBPUSD pair above the 1.3400 technical level again, price-action may gravitate back towards the 1.3450 resistance level.

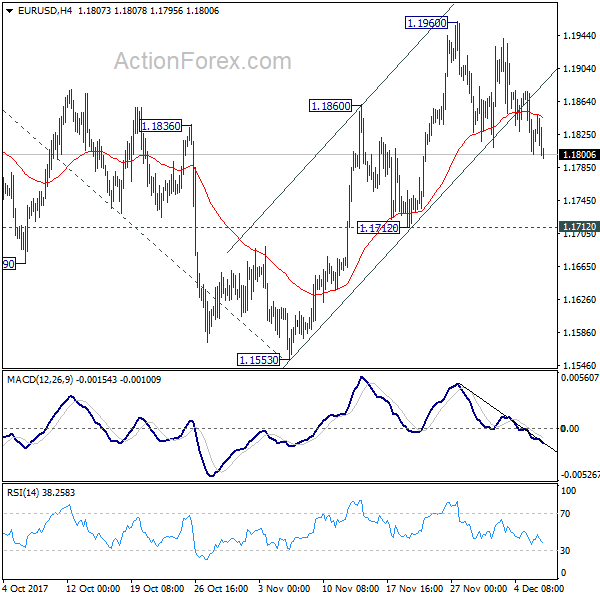

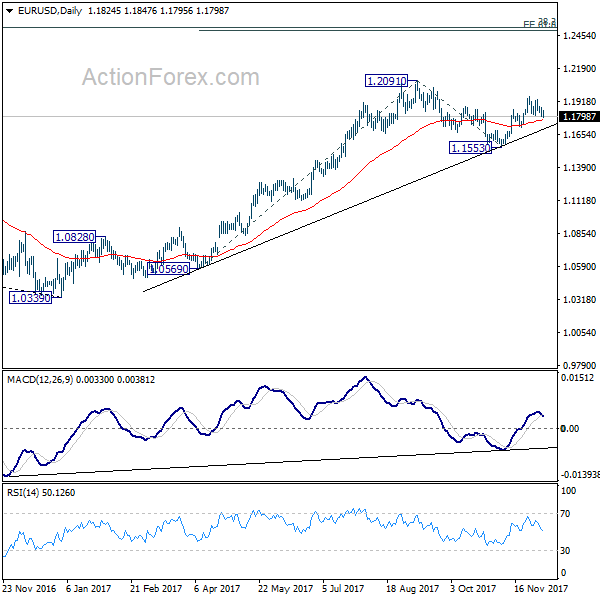

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1792; (P) 1.1834 (R1) 1.1868; More....

EUR/USD's pull back from 1.1960 continues today but it's staying well above 1.1712 support so far. Intraday bias remains neutral first and another rise is still mildly in favor. On the upside, break of 1.1960 will resume the rise from 1.1553 and target 1.2091 high first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 will indicate completion of the rise from 1.1553 and turn near term outlook bearish.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

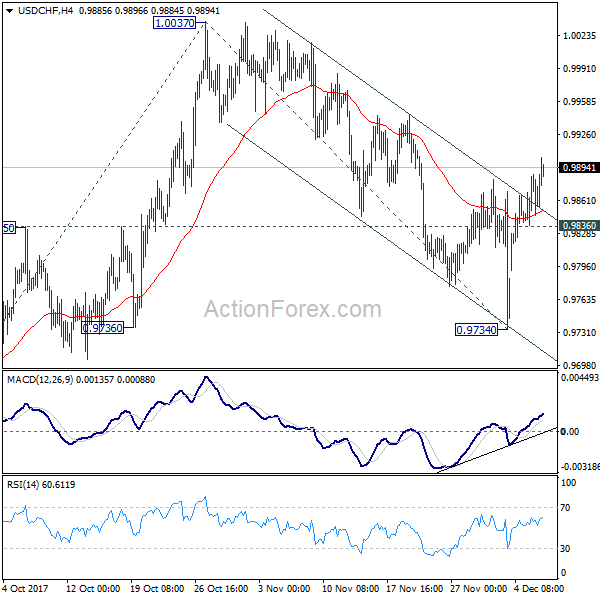

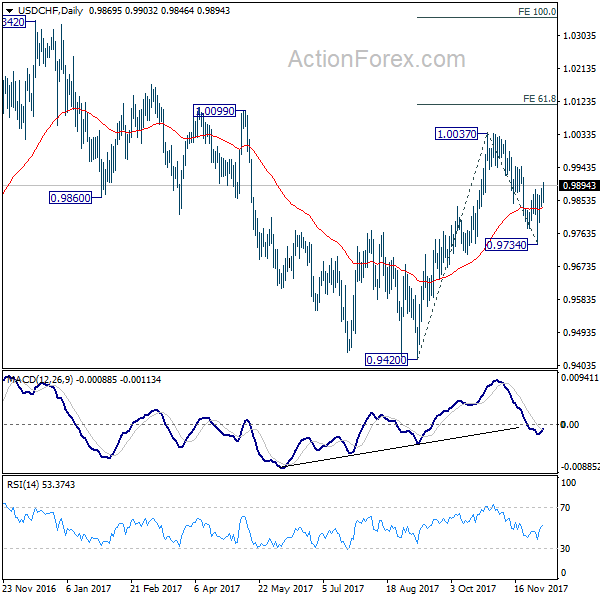

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9844; (P) 0.9865; (R1) 0.9894; More....

USD/CHF's break of 0.9881 resistance now suggests that pull back from 1.0037 has completed at 0.9734 already. Intraday bias is back on the upside for retesting 1.0037 first. Break there will resume whole rise from 0.9420 and target 61.8% projection of 0.9420 to 0.9734 from 1.0047 at 1.0115. On the downside, below 0.9836 minor support will dampen the bullish case and turn bias back to the downside for 0.9374 instead.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

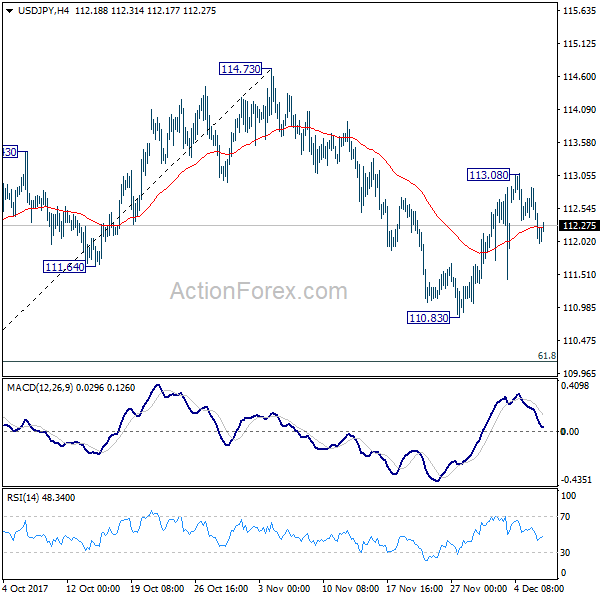

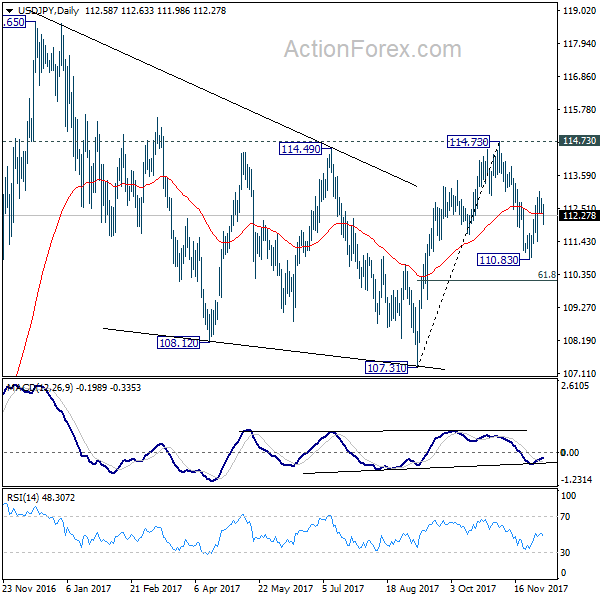

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.35; (P) 112.60; (R1) 112.84; More...

Intraday bias in USD/JPY remains neutral and outlook is a bit mixed. On the upside, above 113.08 will extend the rebound from 110.83 to retest 114.73 key resistance. Decisive break there will extend the rally from 107.31 to retest 118.65 high. On the downside, break of 110.83 will resume the decline from 114.73 instead. But in that case, we'll look for bottoming again below 61.8% retracement of 107.31 to 114.73 at 110.14.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

Canadian Dollar Steady Ahead of BoC Rate Decision

The Canadian dollar continues to have a quiet week. In the Wednesday session, USD/CAD is trading at 1.2667, down 0.16% on the day. On the release front, both Canada and the US release Trade Balance, and the US will also publish ISM Non-Manufacturing PMI. On Wednesday, the Bank of Canada will set the benchmark rate and the US releases ADP Nonfarm Employment Change.

The Bank of Canada is expected to remain on the sidelines and leave the benchmark rate at an even 1.00% on Wednesday. Although some analysts don't expect the BoC to raise rates before next April, that timetable could change if last week's sparkling numbers continue. On Friday, employment change soared to 79.5 thousand, crushing the estimate of 10.2 thousand. This marked 12 straight months of job gains and helped drive the unemployment rate down to 5.9%. As well, September GDP rebounded with a gain of 0.2%, edging above the estimate of 0.1%. The impressive numbers boosted the Canadian dollar by some 1.6% on Friday, its strongest 1-day gain in 2017. On Tuesday, the Canadian dollar climbed to its highest level since October 24. If today's BoC rate statement sounds optimistic about the Canadian economy, the loonie rally could continue. Another factor which the BoC must take into account is expected rates hikes in the US in December and January. If the Fed does raise rates at its next two policy meetings, the BoC would have to follow suit with a raise of its own, or watch the Canadian dollar head lower.

The US labor market has been red-hot, but the markets are bracing for some weak November numbers. ADP Nonfarm Employment Change is expected to slow to 189 thousand, compared to 235 thousand in the previous release. Investors are, of course, much more interested in the official nonfarm employment change release, which takes place on Friday. Again, the markets are expecting a soft landing, with a forecast of 200 thousand, down from 261 thousand in the October release. If nonfarm payrolls, one of the most important indicators, is weaker than expected, the US dollar could lose ground.

Trade Idea: USD/CAD – Sell at 1.2800

USD/CAD - 1.2677

Trend: Near term up

Original strategy :

Sell at 1.2800, Target: 1.2600, Stop: 1.2860

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2800, Target: 1.2600, Stop: 1.2860

Position: -

Target: -

Stop:-

As the greenback recovered after falling to 1.2623, suggesting consolidation above this level would be seen and corrective bounce to 1.2720-30 cannot be ruled out, however, as top has been formed earlier at 1.2917, reckon upside would be limited to 1.2790-00 and bring another decline later, below said support at 1.2623 would extend the fall from 1.2917 to 1.2570-75 but loss of near term downward momentum should prevent sharp fall below 1.2550 and price should stay well above 1.2500-10.

In view of this, we are looking to sell on recovery as 1.2790-00 should limit upside and bring another decline later. Above 1.2850-60 would risk test of 1.2890-00 but only break of said resistance at 1.2917 would revive bullishness and extend recent upmove to 1.2975-80 (61.8% Fibonacci retracement of 1.3547-1.2061), then towards psychological resistance at 1.3000.

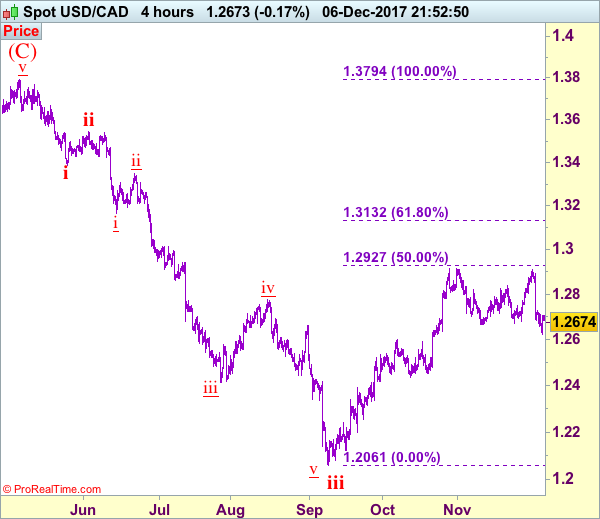

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

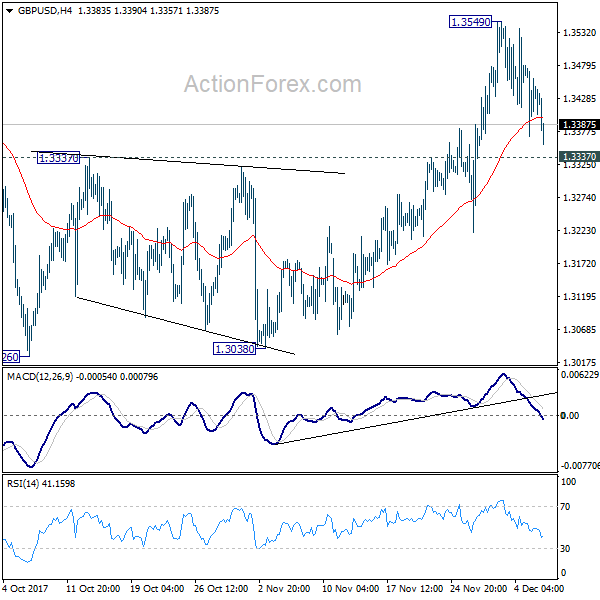

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3381; (P) 1.3429; (R1) 1.3489; More....

GBP/USD's pull back from 1.3549 extends to as low as 1.3357 so far today. But the pair is still staging above 1.3337 resistance turned support. Intraday bias remains neutral and another rise is still expected. Break of 1.3549 will target 1.3651 high and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it's still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Dollar Unmoved after ADP Grew 190k, Sterling and Aussie Staying Weak

Mid-Day Report: Dollar Unmoved after ADP Grew 190k, Sterling and Aussie Staying Weak

Quick update: CAD is sold off after BoC said in the statement that Governing "Council will continue to be cautious, guided by incoming data in assessing the economy's sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation." The language suggests BoC will stay in wait-and-see mode in near term, practically rule out a hike in January.

Dollar continues to trade with a mixed today as economic data released from US provide little inspiration. Sterling weakness remains the main theme in rather directionless markets. Misalignment within UK politicians remain the key issue in Brexit negotiation and Prime Minister Theresa is still struggling to put things back under control. Meanwhile, Australian Dollar stays as the second weakest one after today's GDP mixed. On other hand, Yen is extending its rebound, in particular against Europeans. Canada Dollar follow closely as markets await BoC rate decision. The Loonie would be given a boost if BoC signals that it's back in tightening path again.

Release from US, ADP report showed 190k growth in private sector jobs in November, just 1k below expectation of 191k. Non-farm productivity was finalized at 3.0% in Q3, unit labor costs at -0.2%. From Canada, labor productivity dropped -0.6^ qoq in Q3. Release earlier today, Eurozone retail PMI rose to 52.4 in November. German factory orders rose 0.5% mom in October. Swiss CPI was rose to 0.8% yoy in November.

UK PM May insist on making very good progress after talking to DUP leader

In UK, Prime Minister Theresa May finally had a phone call with North Ireland DUP leader Arlene Foster today. Foster, who interrupted May's talk with European Commission President Jean Claude Juncker, initially refused to answer the call. May said afterwards that "very good progress" was made in Brexit negotiation, but a DUP spokesman sounded indifferent and said that there was "more work to be done". May is expected to go back to Brussels to resume the negotiation with EU and targets to complete "sufficient" progress by Sunday at most. But so far, the issue of Irish border remain a key showstopper and there isn't any positive development seen yet.

ECB Mersch urged to plan for QE exit

ECB Executive Board member Yves Mersch urged the central bank to start planning for ending the asset purchase program. He said that "while a too quick end to the buying program could lead to excessive market reactions, we should not forget that the longer the programme lasts, ... the greater the risks will become." And, "a credible perspective for an exit from QE is therefore key in curbing risks."

Greek 10 year yield dropped to 8 year low

Greece 10 year government bond year drops to as low as 4.802% today, hitting the lowest level in eight years since November 2009. This is partly a reflection on the preliminary agreement with Eurozone regarding the reforms of the bailout program. That kept Greece on course for ending financial aids next year in August. Also, it reflects general optimism within Eurozone as investors are back taking more risks and yields. It's also seen as a factor keeping the Swiss Franc soft.

Australia GDP showed weak spending growth

Australian Dollar tumbles broadly today as weighed down by disappointing GDP data. Q3 GDP rose 0.6% qoq 2.8%, below expectation of 0.7% qoq, 3.0% yoy. Despite the miss, the headline numbers are not bad at all. Treasurer Scott Morrison described the figures as indicating "solid" economic growth. And he said that "this is above the OECD average and puts Australia back up towards the top of the pack for major advanced economies around the world." However, weak household consumption is seen as the most worrying part of the details. Consumer spending grew just 0.1% qoq and was at the lowest rate in more than a decade since 2005. Sluggish wage growth, as pointed out by RBA rate statement released yesterday, was a key factor and would likely continue to be.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3381; (P) 1.3429; (R1) 1.3489; More....

GBP/USD's pull back from 1.3549 extends to as low as 1.3357 so far today. But the pair is still staging above 1.3337 resistance turned support. Intraday bias remains neutral and another rise is still expected. Break of 1.3549 will target 1.3651 high and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it's still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.60% | 0.70% | 0.80% | 0.90% |

| 07:00 | EUR | German Factory Orders M/M Oct | 0.50% | -0.20% | 1.00% | 1.20% |

| 08:15 | CHF | CPI M/M Nov | -0.10% | 0.00% | 0.10% | |

| 08:15 | CHF | CPI Y/Y Nov | 0.80% | 0.80% | 0.70% | |

| 09:10 | EUR | Eurozone Retail PMI Nov | 52.4 | 51.1 | ||

| 13:15 | USD | ADP Employment Change Nov | 190K | 191K | 235K | |

| 13:30 | CAD | Labor Productivity Q/Q Q3 | -0.60% | -0.40% | -0.10% | -0.20% |

| 13:30 | USD | Nonfarm Productivity Q3 F | 3.00% | 3.30% | 3.00% | |

| 13:30 | USD | Unit Labor Costs Q3 F | -0.20% | 0.30% | 0.50% | |

| 15:00 | CAD | BoC Rate Decision | 1.00% | 1.00% | 1.00% | |

| 15:30 | USD | Crude Oil Inventories | -5.6M | -3.2M | -3.4M |

Are US Equity Markets Losing Their Sparkle?

- No Tax Reform May Mean No Santa Rally This Year;

- GBP Stutters as Irish Border Issue Goes Unresolved;

- Bitcoin Surges Again as CBOE and CME Prepare to Offer Futures.

No Tax Reform May Mean No Santa Rally This Year

It's been a rocky few days for US equities and that may be starting to take its toll, with US futures pointing to a weaker open on Wednesday, as Europe and Asia post similar losses.

It would appear some of the sparkle has disappeared from the markets at the start of December after what has been another impressive performance since the middle of November. The prospect of tax reform in the US, which has made progress, has aided the rally in recent weeks but clearly a number of significant hurdles remain and this is likely to continue to impact investor sentiment this month. A failure to deliver tax reform may well ensure the santa rally eludes us this year.

The pound is trading around half a percentage point lower against the dollar and the euro this morning as optimism around Brexit negotiations fades. The DUP's decision to scupper a deal on phase one of the talks late in the day has raised serious questions regarding whether one can now be achieved by the EU summit next week when progress is expected to be discussed. If the Irish border issue remains unresolved, it's unlikely that the EU will sign off on negotiations progressing to future trade and transition deal.

GBP Stutters as Irish Border Issue Goes Unresolved

Sterling had previously rallied to two month highs against the greenback on the prospect of a deal being achieved, as both parties appeared to have closed in on a financial settlement being agreed, at least in theory. As it turns out, what had been touted as being the largest stumbling block has turned out to be nothing in comparison to finding a solution to the border problem that satisfies all involved. The next week could get very tense for Theresa May and questions over her leadership are already once again being asked, providing more downside pressure on the currency.

Bitcoin Surges Again as CBOE and CME Prepare to Offer Futures

Bitcoin is surging once again on Wednesday in a fashion that has become all too familiar this year. The cryptocurrency was up almost 10% on the day at one stage, reaching a new high above $12,800 in the process, and continues to trade close to these highs at the time of asking. The moves we've seen over the last week or so have been quite remarkable even for Bitcoin and while there has been fundamental factors supporting the rise this year, the speculative contribution to the rise can't be overlooked.

CBOE and CME Group are preparing to offer Bitcoin futures over the next couple of weeks and perhaps this has played a major role in the surge. That said, the increased media coverage we've seen around Bitcoin recently may have actually fed the frenzy, with fomo traders piling in to avoid missing out on a rare opportunity to make these kinds of gains. The danger here of course is that this kind of action leaves traders very vulnerable to bubbles bursting and significant losses due to a lack of understanding of what is being traded.

While political stories are currently dictating market sentiment at the moment, there are a number of key data points still to come this week that will have an influence. Today we'll get ADP employment numbers for November, ahead of Friday's official jobs report, as well as unit labour costs and productivity numbers. The Bank of Canada will also make its latest interest rate decision, although no change is expected with the central bank having already raised interest rates twice in recent meetings.