Sample Category Title

USD/ZAR 1H Chart: Two Channels Prevail

The US Dollar is currently trading in a long-term channel up against the South African Rand. The pair reached a 2017 high of 14.5490 on November 13, breached the previously prevailing ascending channel (drawn with dashed lines) and subsequently initiated a new wave south. If looking at the junior pattern, the Greenback should test its upper line circa 13.85. However, the 55– and 200-hour SMAs which have limited the pair for the past two weeks are located nearby. Even if the pair edges higher, the pressure of the monthly PP, the 200-hour SMA and the weekly S1 near the 13.90 mark is likely to reverse the pair back down. Meanwhile, the bottom boundary of the senior channel is located circa 131.10. The US Dollar could push for this mark during the following two weeks.

EUR/USD Analysis: Trades Near 1.1864 Amid Strong Resistance

The resumption of surge towards the 1.1910 level was halted by the weekly PP with the 55-hour SMA as well as the 61.8% Fibonacci retracement level and the 100-hour SMA. Nevertheless, the general scenario remains the same. In medium perspective the pair is projected to reach the upper boundary of a senior descending channel near the 1.1940 mark. However, during this trading session the above technical indicators are likely to push the rate back to combined support formed by the 200-hour SMA and the bottom edge of a junior ascending channel. But this scenario might be altered due to release of estimate on Euro Zone’s inflation. Even though the event itself does not arouse much volatility but it might create a momentum for easier breakthrough to the top.

GBP/USD Analysis: Breaks From Dominant Channel Down

On the one hand, the cable has reached the forecasted target at the 1.3406 level. On the other hand, the upper boundary of the junior ascending channel that was backed by the weekly S1 could not constrain the further surge. Moreover, the 47 pip jump in the early hours of this trading session allowed the pair to break not only through the monthly R1 but also the upper trend-line of a dominant descending channel. As the pair two times in a raw failed to bypass the 1.3480 mark, a small retreat is expected to follow. However, if traders decide to readjust the above junior channel up, the correction might drag the pair back to 1.3400. Nevertheless, in larger perspective an optimism related to Brexit is likely to continue driving the Pound towards the 1.3600 level.

USD/JPY Analysis: Forms Minor Rising Wedge

Even though there were attempts to push the pair back to the 55- and 100-hour SMAs, anticipation of the upcoming US GDP data release inched the buck higher. Without this fundamental background the pair would unlikely to bypass the 38.2% Fibonacci retracement level at 111.65 and the monthly S1 at 112.05. However, the further surge seems unlikely, as yesterday’s sharp advance led to transformation of new junior ascending channel into the rising wedge formation. In support of this assumption, there is an alleged resistance area between the 112.30 and 112.35 marks that matches with the breaking point of the pattern. In case this assumption is incorrect, a combination of the weekly R1 and the 50% Fibonacci retracement level near 112.45 should temporarily halt the buck from soaring higher

XAU/USD Analysis: Drops By 0.9% As American GDP Grows

An estimated growth of the US GDP expectedly strengthened the buck and reduced demand for the safe haven metal even though the plunge was not expected to be so sharp, as southern side was reliably protected by two moving averages that were moving along the trend-line of a rising wedge formation. As the aggregate market sentiment remains 60% bullish, in medium perspective the pair is expected to continue rising in the one-month long ascending channel. With respect to the current trading session, formation of a minor pennant pattern suggests that the rate is likely to continue moving downwards towards the bottom boundary of the above channel. Nevertheless, a rebound might happen earlier if the pair fails to bypass support zone located between the 1,282.00-1,283.00 levels.

USD/JPY: US Gross Domestic Product

The Greenback was slightly changed against the Japanese Yen, following the preliminary data release on the US economic growth. The USD/JPY exchange rate fell 3 base points to continue fluctuating at a stronger level of 111.95, targeting the 112.0 area.

The US economy expanded at the fastest pace in three years, as businesses invested more in equipment and inventories, offsetting slackening in inflation. The Commerce Department stated in its preliminary report that the US gross domestic product rose at a 3.3% yearly pace in the September quarter. Donald Trump wants diminished taxes to lift yearly GDP growth to 3% on a regular basis. Though, fiscal stimulus is likely to come only when the economy is at full employment.

EUR/USD: German Consumer Price Index

The Euro depreciated against the Greenback, following strong preliminary report on Germany’s consumer inflation in November. The EUR/USD currency pair fell slightly 0.08% or 9 base points to rebound from the 1.1825 mark and changed the direction back to the 1.1870 area, being affected by the US economic reports coming further.

German consumer prices grew more rapidly than anticipated in November, as the costs of fuel and food rose, owing to the Euro zone’s loose monetary policy boosting the country’s economy and job market. Destatis preliminary report for Germany showed that the Consumer Price Index rose 1.8% year-on-year in November, compared with a 1.5% gain in the previous month.

Technical Outlook: AUDUSD – Bears Focus Key Support At 0.7530, Falling Trendline Continues To Cap

The Aussie remains in red for the fifth consecutive day and trend lower, with bear-trendline off 0.8102 (20 Sep high) continuing to cap and maintain bearish pressure.

Limited overnight's corrective action was capped by broken daily Tenkan-sen (0.7592) before bears resumed, pressuring Wednesday's low at 0.7551.

This is the last obstacle ahead of key support at 0.7530 (21 Nov low, the lowest since mid-June), break of which would signal continuation of larger downtrend from 0.8124 (2017 high).

Bearish techs support scenario, however, hesitation at 0.7530 pivot and subsequent consolidation would be likely scenario.

Bear-trendline is expected to cap extended upticks.

Res: 0.7592, 0.7607, 0.7620, 0.7644

Sup: 0.7551, 0.7530, 0.7500, 0.7475

NZDUSD Is Set For Further Downside As Decline Continues

NZDUSD appears to be carving out a lower top after reversing back down from the November 28 high of 0.6945. The recent corrective move from 0.6780 stalled and downside momentum gained speed, turning the focus back to the downside.

Looking at the 4-hour chart, RSI is now in bearish territory below 50, suggesting the downside move still has legs, especially after strong resistance has been met at the 61.8% Fibonacci retracement level (0.6848) of the rise from 0.6780 to 0.6945.

Support is expected at the November 22 low of 0.6819 ahead of 0.6780. A further decline from this 1 ½-year low would bring about a resumption of the downtrend that started from the July peak of 0.7557.

Only a move back above 0.6870 (near 50% Fibonacci) would help weaken downside pressure. But since the market is trading below the 20 and 50-period moving averages, the outlook is quite negative.

Pound Shines On Brexit Hopes, Tech Stocks Decline, OPEC Meeting, US & Eurozone Inflation Take The Stage

Here are the latest developments in global markets:

FOREX: The dollar was firmer against its major peers but headed for a monthly loss as a rising pound and a stronger euro capped gains arising from investors’ positive sentiment on the US economy despite ongoing geopolitical tensions in the Korean peninsula. Against the yen, the greenback hit a fresh one-week high, while it gained the most relative to the kiwi.

STOCKS: The Nikkei 225 closed 0.6% higher and the Hang Seng was down by 1.3%; tech stocks underperformed in Asia following yesterday’s selloff in the US that saw the Nasdaq Composite losing 1.3% on the day; Euro Stoxx 50 futures traded 0.2% higher at 0729 GMT; Dow futures were 0.2% higher with S&P 500 and Nasdaq 100 equivalents little changed.

COMMODITIES: Oil prices edged higher but remained near yesterday’s one-week lows as concerns over the future of the production-cut deal debated today at the OPEC/non-OPEC meeting weighed on the markets. The EIA report showed unexpectedly a sharp decline in US crude inventories, but gasoline inventories increased. WTI crude was 0.30% up at $57.47 per barrel and Brent rose by 0.48% to $63.41. Gold hit a fresh one-week low of $1,281.38 per ounce.

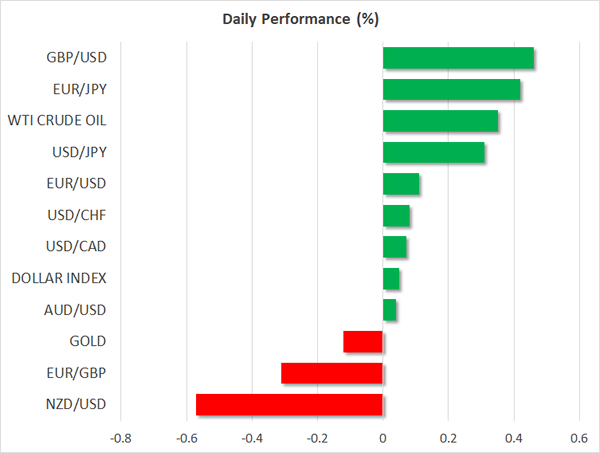

Major movers: Pound at two-month high; kiwi tumbles on weaker business confidence

The pound stretched its uptrend against the dollar, breaking the 1.3400 key level to reach a fresh two-month high of $1.3478 as investors were optimistic that the UK and the EU will reach a compromise on the financial settlement despite British consumer confidence falling back to four-year lows on November according to the Gfk measure.

Euro/dollar gained 0.17% to 1.1869, while euro/yen jumped by 0.46% to a two-week high of 133.29, finding support on Reuters polls showing that a majority of economists are expecting the ECB to terminate its monetary stimulus probably by the end of 2018.

The kiwi sank by 0.55% to a one-week low of $0.6831 after the ANZ business confidence gauge declined to an eight-year low in November, while the aussie posted moderate gains following better than expected readings on October’s building approvals. Australian capital expenditures for the third quarter and private housing credit grew in line with expectations, while Chinese manufacturing and non-manufacturing PMIs showed some improvement in November.

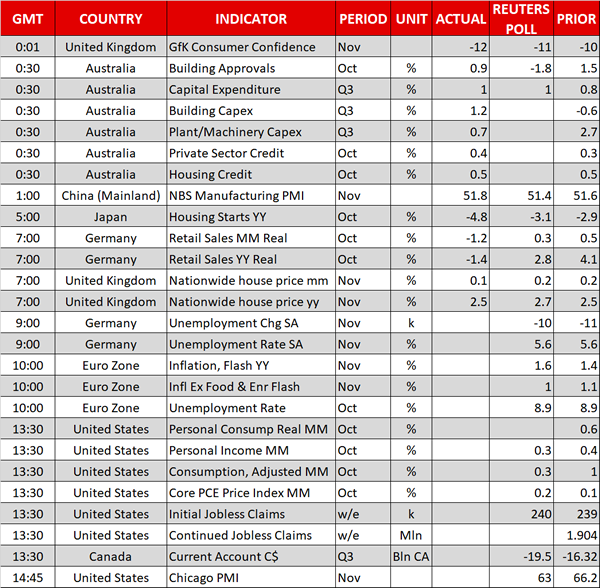

Day ahead: Senate tax bill, consumption & PCE inflation closely watched in US; eurozone flash CPI & unemployment rate attract interest; OPEC meeting coming up

Out of the US, October consumption data and the Federal Reserve’s preferred inflation measure, the core PCE price index, will be at the center of attention in terms of data releases. Those are due at 1330 GMT alongside personal consumption and personal income data, as well as weekly figures for initial and continuing jobless claimants.

A possible Senate vote on the tax bill later today is of course of great significance. If the bill does pass, then it is expected to provide a boost to the greenback as well as spur positive sentiment in stock markets.

The eurozone will see the release of November flash inflation and October unemployment rate figures at 1000 GMT. Headline inflation is expected to grow by 1.6% y/y (October’s reading was at 1.4%) and core inflation by 1.0% annually (October’s reading was at 1.1%). Before that, Germany will see the release of unemployment data (0900 GMT).

OPEC alongside some non-OPEC members including Russia will be meeting today in Vienna. A decision to extend supply cuts beyond March 2018 is expected to provide some support to oil prices.

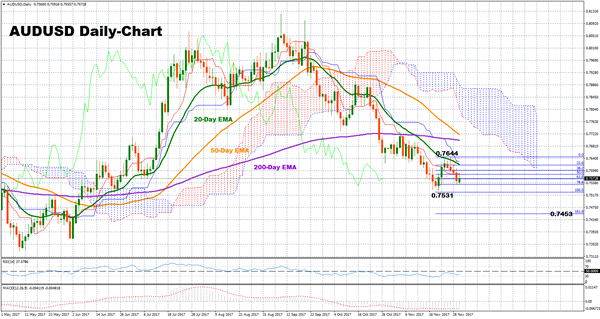

Technical Analysis: AUDUSD in consolidation phase but bearish bias intact

Bears still have the upper hand on AUDUSD as the pair has been posting lower lows and lower highs since early September, with markets pricing no rate hikes this year and only gradual rate rises in 2018. The RSI is below its neutral level (50), suggesting that negative movements are more likely to emerge in the short term, while the Ichimoku analysis also backs this view as market action is currently taking place below the cloud. To the downside, an immediate support could be found at the previous bottom of 0.7531 before the 0.7500 psychological level and the 161.8% Fibonacci of 0.7453 of the upleg from 0.7531 to 0.7644 come into view. Should the pair head up, potential resistance levels could be met between the previous top of 0.7644 and the 0.7700 key level, where the 200-day exponential moving average also lays.