Sample Category Title

Canadian Dollar Slips to 4-Week Low, Current Account Next

The Canadian dollar continues to lose ground in the Thursday session. Currently, USD/CAD is trading at 1.2890, up 0.20% on the day. The Canadian dollar has suffered a rough week, declining 1.4 percent. Currently, the currency is at its lowest level against the greenback since November 1. On the release front, Canada's current account deficit is expected to rise to CAD $20.0 billion. The US releases unemployment claims and Personal Spending. On Friday, the US releases ISM Manufacturing PMI.

The US economy continues to perform well, and there was more good news on Wednesday, as Preliminary GDP for the third quarter posted a sharp gain of 3.3%. This was higher than the initial estimate of 3.0% and marked the fastest growth rate since Q3 of 2014. This was particularly impressive, as the southern US was battered by major hurricanes which caused significant economic damage. Consumer confidence levels are sky-high, but consumer consumption softened in the third quarter. However, business spending improved in the third quarter. Federal Reserve Chair Janet Yellen sounded upbeat about the economy, saying that the expansion was broad-based, across sectors of the economy.

Canadian inflation indicators pointed upwards on Tuesday, but the Canadian dollar couldn't take advantage and lost more ground against the US currency. The Raw Materials Price Index jumped 3.8% in October, rebounding after a decline of 0.1% a month earlier. This marked the indicator's strongest gain in 2017. The Industrial Product Price Index also rebounded after a decline, posting a gain of 1.0%. Elsewhere, Bank of Governor Stephen Poloz sounded upbeat about the stability of the financial system, noting that the labor market was strong and higher interest rates had helped cool the housing market frenzy.

Canadian GDP and Jobs Report Eyed for Rate Clues as Loonie Hits One-Month Low

The Canadian dollar is once again on the verge of breaching the 50% Fibonacci retracement level of its impressive May-September uptrend. The currency has been suffering from the paring back of expectations of additional rate hikes by the Bank of Canada over the coming months, concerns about difficult NAFTA renegotiations and a stronger US dollar.

After several failed attempts in late October/early November to break this retracement level around C$1.2925 to the greenback, the loonie has been stuck in a range. Its uptrend came to a halt in September soon after the Bank of Canada raised rates for a second time this year. BoC officials have been signalling that further rate hikes will be data-dependent, but incoming data since the September policy meeting has been mixed.

Employment growth, particularly in full-time jobs, has been strong but inflation has moderated slightly to 1.4% in October and retail sales disappointed in September. Friday's numbers will therefore be watched closely for a clearer indication as to the strength of the Canadian economy and whether further rate hikes would be warranted in the near term.

GDP expanded by a robust annualized rate of 4.5% in the second quarter, following a similarly solid 3.7% growth in the first quarter. However, this rapid pace is expected to have slowed in the third quarter and consensus forecasts are for the economy to have expanded by 1.6% in the three months to September.

The unemployment rate is expected to dip back to 6.2% in November after increasing by 0.1 percentage points to 6.3% in October. The number of new jobs created though is forecast to ease from 35.3k in October to 10k in November.

An upside surprise to tomorrow's data could bring forward market expectations of the next rate increase by the BoC. Investors are currently pricing the next move to come in April or May 2018, with a rate hike at the next meeting on December 6 having sharply diminished in recent weeks. Weaker than anticipated readings could push back the expectations even further into the future, which would be negative for the loonie.

While a possible output extension deal by OPEC/non-OPEC countries could provide some support for the Canadian currency, the loonie's positive correlation with oil prices hasn't been very strong recently, with rate hike expectations being a bigger driver for the dollar/loonie pair.

If dollar/loonie manages to break above resistance at the 50% Fibonacci level around 1.2925, it could pave the way for additional gains towards the 1.31 handle. But upbeat data tomorrow could push the pair back towards recent support around 1.2660.

Euro Bears in Charge; European Stocks in Green; Eyes on US PCE Inflation Index & OPEC Meeting

Here are the latest developments in global markets:

Forex: The euro dived to a one-week low versus the dollar and approached a one-month low against the pound after flash inflation estimates out of the Eurozone inched below expectations in November, whereas the block's unemployment rate ticked down, hitting fresh multi-year lows. Pound/dollar was on track to post a third straight green daily candle, while the kiwi was the worst performer amid weakening business sentiment.

Stocks: European stocks were posting gains. The STOXX 600 index was 0.57% up, the German Dax jumped by 0.75% while the British FTSE rose by 0.21% around midday. US futures were heading higher – Dow, S&P 500 and Nasdaq 100 contracts traded up by 0.4%, 0.3% and 0.3% respectively.

Commodities: Brent futures broke above $64 per barrel and WTI crude futures recovered more than half of earlier losses, rising to $57.81. Gold retreated by 0.18% on the day to trade at $1,281.20 per ounce.

Day Ahead: US PCE index & consumption in focus; OPEC meeting takes place

Looking at the calendar, readings on the US consumer spending for the month of October, figures on the Fed's preferred inflation measure, the core PCE (personal consumption expenditures) index, and data on initial jobless claims are likely to shake the dollar later in the day.

Personal spending is expected to narrow to 0.3% m/m in October after it posted its highest growth of 0.9% since 2009 in September when motor vehicles sales surged as households replaced their hurricane-damaged cars.

On the other hand, analysts anticipate the core PCE index to pick up by 0.1 percentage points to 1.4% y/y in October, remaining well below the Fed's target of 2.0%.

Turning to initial jobless claims, the Department of Labor forecasts 240,000 individuals to have applied for unemployment benefits in the week ending November 24 compared to 239,000 in the preceding week.

However, the greenback is likely to react more fiercely on any updates on the US tax story as markets are widely expecting to see the outcome of the final tax vote in the Senate probably later this week. Positive results would put Trump's proposed tax overhaul for a vote on a full-Chamber floor, reducing debate periods and raising hopes for taxes turning into law before the year-end.

In oil markets, investors will keep a close eye on the OPEC/non-OPEC meeting in Vienna today, where energy ministers are gathering to decide whether to prolong their output cuts for another nine months. Russia's saying would be in focus as the country has lately shown some reluctance on the strategy and the duration of the extension. Speaking in Vienna, the Saudi Arabian energy minister, Khalid al-Falih said he would back a nine-month extension while adding that an exit from the program would be very gradual.

CAC Posts Slight Gains, French CPI Matches Forecast

The CAC has posted gains in the Thursday session, erasing the losses which marked Wednesday trade. Currently, the CAC is at 5423.30, up 0.46% on the day. On the release front, Eurozone CPI Flash Estimate edged up to 1.5%, missing the estimate of 1.6%. French Preliminary CPI remained unchanged at 0.1% in November, matching the forecast. On Friday, the eurozone and France release Manufacturing Final PMI reports.

Bank stocks have made gains this week, following testimony from Fed Chair Designate Jerome Powell. On the CAC, Credit Agricole has gained 1.41% on Thursday. At a confirmation hearing on Tuesday, Powell, said that he favored tailoring regulations for small banks, leaving the toughest regulations for the largest banks. Powell takes over the helm of the Federal Reserve in February, and is expected to continue the Fed's current monetary policy, which has been marked by small, incremental gains.

French President Emmanuel Macron has big plans for reforming the eurozone, including a parliament, budget and finance minister for the bloc. However, he will need the help of Angela Merkel to realize these aspirations, and Merkel has her hands full on the domestic scene, as she tries to form a new government. Coalition talks fell apart after the Free Democrats pulled the plug, and Merkel has now entered into exploratory talks with its former coalition partner, the social democrats (SPD). However, many SPD members don't want the SPD to be relegated to a junior party in the coalition, as was the case prior to the election. The SPD is likely to take advantage of Merkel's weak hand and press demands for greater government spending and a looser immigration policy, and could demand the powerful finance ministry as their price to enter a Merkel government.

DAX Rebounds As US GDP Sparkles

The DAX index has posted strong gains in the Thursday session, erasing the losses seen on Wednesday. Currently, the DAX is at 13,168.00, up 0.80% on the day. On the release front, German Retail Sales declined 1.2%, well off the estimate of 0.3%. German unemployment change declined by 18 thousand, better than the estimate of -10 thousand. Eurozone CPI Flash Estimate edged up to 1.5%, but this was shy of the forecast of 1.6%. On Friday, manufacturing indicators will be in focus, as Germany and the eurozone release Final Manufacturing PMI reports.

German retail sales remain a concern, and posted a sharp decline of 1.2% in October. This marked the third decline in four months. Germany’s economy is solid and the labor market is strong, so why isn’t the German consumer spending? Strong economic conditions have not translated into higher wages for a large segment of the labor force, and low unemployment numbers have masked the problem of underemployment, ,which of course means lower wages for workers who can’t find full-time work. The lack of inflation in Germany is apparent in the eurozone as well, as inflation levels remain below the ECB’s inflation target of around 2 percent.

There are new developments in the German political saga, as President Angela Merkel continues efforts to form a new government. Coalition talks will now center on Merkel’s conservative bloc (CDU) and the social democrats (SPD). After the election, the SPD announced that it would remain in the opposition. However, coalition talks imploded when the Free Democrats pulled out of the negotiations and there is pressure on the SPD to reconsider in order to avoid elections. The SPD is split on whether to join a coalition with Merkel, as many SPD members don’t want the SPD to be relegated to a junior party in the coalition, as was the case prior to the election. Although the SPD has agreed to exploratory meetings with the CDU, substantial talks of a “grand coalition” are not expected to start before 2018. The SPD is likely to take advantage of Merkel’s weak hand and press demands for greater government spending and a looser immigration policy. The SPD could even demand the powerful finance ministry.

Elliott Wave Analysis: Nasdaq100 Vs BTCUSD And German Dax

We have seen a sharp fall on some US stocks today; a drop come on NASDAQ100 which consists of some very good known technology companies. A drop on NASDAQ100 also caused lower cryptocurrenices which obviously has a lot in common with technology companies because of mining. Correlation is very close, and as you can see NASDAQ100 was the first one that turned lower and then BTCUSD followed the move as well with a slight delay.

Nasdaq100 vs BTCUSD

Well, I warned this week that US market can turn lower, but only if correlation with DAX will hold, which is seen in corrective bounce; ideally making wave C higher now as an ending diagonal.

German Dax, 1h

An ending diagonal is a special type of pattern that occurs at times when the preceding move has gone too far too fast, as Elliott put it. A very small percentage of ending diagonals appear in the C wave position of A-B-C formations. In double or triple threes, they appear only as the final 'C' wave. In all cases, they are found at the termination points of larger patterns, indicating exhaustion of the larger movement.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

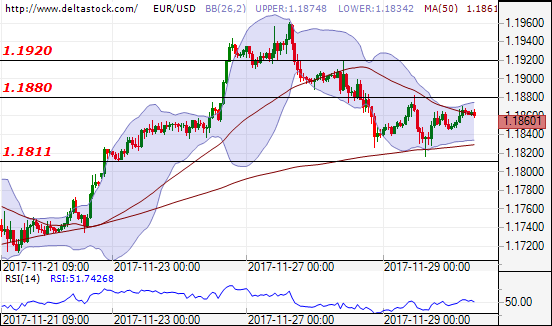

EUR/USD

Current level - 1.1860

The intraday spike to 1.1960 could be a finale of the rise since 1.1710 low and my outlook here is bearish, for a violation of 1.1870 support, towards 1.1770.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1960 | 1.1940 | 1.1870 | 1.1690 |

| 1.2000 | 1.2090 | 1.1770 | 1.1550 |

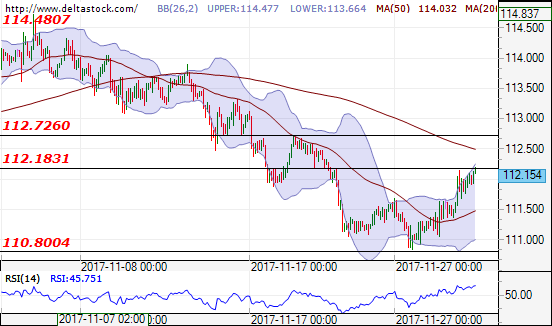

USD/JPY

Current level - 112.15

The trend is positive for breakthrough the level at 112.18 and test at 112.72. If the breakthrough of this level is successful, this might lead to uptrend at the new level 118.60.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

112.72 |

112.72 |

112.00 |

109.50 |

|

112.70 |

114.70 |

109.50 |

107.30 |

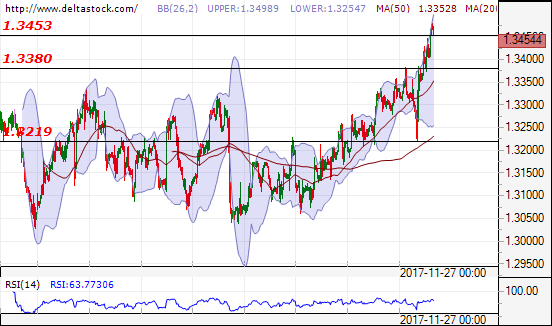

GBP/USD

Current level - 1.3454

The forecast is positive for breakthrough the resistance at 1.3453. In negative direction the support level will be 1.3380 and after that 1.3219.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

|

1.3380 |

1.3460 |

1.3280 |

1.3220 |

|

1.3460 |

1.3660 |

1.3220 |

1.3020 |

Equity Markets Rebound After Tech Sell-Off

- Data to Put Improved Risk Appetite to the Test;

- Oil Edges Higher Ahead of Decision on Output Cut;

- Sterling Adds to Gains on Brexit Progress;

- Bitcoin Back Below $10,000 After Wednesday's Aggressive Rebound.

Data to Put Improved Risk Appetite to the Test

Wednesday's tech sell-off is doing little to weigh on risk appetite ahead of the open on Thursday, with futures on all three major indices around a third of a percentage point higher, tracking broad gains in Europe.

With US indices trading around record highs it seems investors are currently willing to shrug off Wednesday's declines some of the biggest tech names, putting it down to profit taking rather than a sign of any underlying concerns given the already extended levels. With plenty of economic data to come today including income, spending and inflation – the Fed's preferred measure – as well as appearances from Federal Reserve officials, this positive risk appetite may well be put to the test at times.

Oil Edges Higher Ahead of Decision on Output Cut

Oil is trading a little higher today as OPEC and non-OPEC officials meet to discuss extending production cuts, which currently runs until March of next year. An extension of the 1.8 million barrel cut to the end of 2018 is expected to be announced and given the rally in recent months, I would assume this is almost entirely priced in.

With that in mind, anything short of this could trigger a decline in oil prices, as could an extension in line with expectations as we saw when the last one was announced in May. Only a more aggressive cut is likely to provide any substantial upside, although I'm not sure there'll be much appetite for such action given the progress that's already been made and the market share that is being conceded to US shale as a result.

Sterling Adds to Gains on Brexit Progress

Sterling is trading higher again this morning as Brexit negotiators appear to be making steps towards agreeing on the terms of the divorce necessary to progress to future trade and a transition. The pound hit a two month high against the dollar on Wednesday and has now reached a similar high against the euro. The pair may find support around 0.8750 having done so on the last two occasions in September and earlier this month. A break below here could be quite a bearish signal for the pair, with next support coming around 0.8650.

While European equity markets are making decent gains across the board on improved risk appetite, the FTSE is slightly underperforming its peers which is likely being driven by the pounds gains. With the FTSE being a global facing index deriving the vast majority of profits from abroad, a stronger pound is actually negative for the UK index.

Bitcoin Back Below $10,000 After Wednesday's Aggressive Rebound

Bitcoin is as volatile as ever on Thursday, with prices having risen as much as 8% earlier in the session only to trade slightly lower at the time of writing. This comes after reaching new highs above $11,000 on Wednesday before falling almost 20% on reports of exchange outages, a clear sign of how easily Bitcoin traders can be spooked and the risk this poses. I'm sure there'll be plenty of more examples of this as speculation increases.

Still, prices remain extremely elevated, despite dropping back below $10,000. While dips have been frequent and at times aggressive, it is notable that they have until now been viewed as buying opportunities prompting quick rebounds. This is helped by the fact that the foundations of Bitcoin as a tradeable asset are improving but the speculative component can't be ignored and will likely continue to play a major role in the medium term.

Euro Dips As German Retail Slumps

The euro has posted small losses in the Thursday session. Currently, EUR/USD is trading at 1.1819, down 0.25% on the day. On the release front, German Retail Sales declined 1.2%, well off the estimate of 0.3%. German unemployment change declined by 18 thousand, better than the estimate of a drop of 10 thousand. Eurozone CPI Flash Estimate edged up to 1.5%, but this was shy of the forecast of 1.6%. In the US, there are two key events – Personal Spending is expected to dip to 0.2%, and unemployment claims is forecast to edge up to 241 thousand. On Friday, manufacturing indicators will be in focus, as Germany, the eurozone and the US release manufacturing PMI reports.

German retail sales remain problematic, and posted a sharp decline of 1.2% in October. This marked the third decline in four months. Germany’s economy is solid and the labor market is strong, so why isn’t the German consumer spending? Strong economic conditions have not translated into higher wages for a large segment of the labor force, and low unemployment numbers have masked the problem of underemployment, ,which of course means lower wages for workers who can’t find full-time work. The lack of inflation in Germany is apparent in the eurozone as well, as inflation levels remain below the ECB’s inflation target of around 2 percent.

There was more good news for the US economy on Wednesday. Preliminary GDP for the third quarter posted a sharp 3.3%, as expected. This was higher than the initial estimate of 3.0% and marked the fastest growth rate since Q3 of 2014. This was particularly impressive, as the southern US was battered by major hurricanes. Although consumer consumption was softened in the third quarter, business spending improved. The rosy picture of the US economy was summarized by Fed Chair Yellen on Wednesday, who said that the expansion was broad-based, across sectors of the economy.

Jerome Powell, who takes over as Fed chair in February, testified before the Senate Banking Committee on Tuesday. Powell said that he favored tailoring regulations for small banks, leaving the toughest regulations for the big players. Powell was cautious and diplomatic during the hearing, saying that the case is building for a December rate hike, and refused to express an opinion on the Trump tax bill. Powell will replace Janet Yellen, and is widely expected to continue Yellen’s monetary stance of small, gradual rate hikes. Fed policymakers have differing views on what to do about inflation, which remains at low levels. Some members have proposed that the Fed drop its 2 percent target, in favor of a “gradually rising path” for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

USD Reverses Losses In Trendless FX Market

Yellen gives positive outlook on the US economy

Yesterday, Janet Yellen spoke in front of Congressional leaders amid the release of the US GDP data, which as expected, climbed to 3-year high. The end of Yellen’s mandate is near as the current Fed Chair is going to be replaced next year by Jerome Powell.

Janet Yellen said in her speech that the central bank does not want to “let growth get out of hands”. The Fed certainly prefers the debt to get out of hands. That was a very ironic statement from the US private bank’s chair. Yellen also mentioned that while she did not want to promise a rate hike in December, she will continue to act towards a normalization of the monetary policy. Markets are pricing in a rate hike for December.

So Yellen, as usual, keeps on being cautious regarding the rate path. It has been years that Fed officials are either “patient” or in “wait-and-see mode”. Central bankers declare that raising rates too soon could push the economy into recession. We rather believe that the Fed is unable to raise rates above a certain level or the bond bubble will likely burst. This is why we should see the Eurodollar climbing higher. In addition the short-term decline in gold is likely temporary as we believe that the Fed will have a hard time to deliver in 2018 and beyond.

Optimistic on Select EM Currencies

While the market focus is clearly on Crypto currencies conditions are steady improving for EM FX. Constructive global backdrop including improved risk appetite and strong growth will send investors deeper into select EM currencies. Current EM weakness trigger by sudden steepening in US yield curve will provide investors with attractive valuation heading into 2018. Weak US data and dovish comments indicate that the Fed is not positioning for aggressive tightening. India remains a bright spot for EM investors, as 3Q growth should recover and likely surprise to the upside. Domestic conditions including consumer spending and narrowing trade deficit will support acceleration in growth.

The RBI will likely stay on hold as inflation head marginally higher yet tighter monetary policy is a low probability until late 2018 (markets are pricing in a single 25bp hike in 2018). Positive news around the UK /EU negotiations, which indicated that an agreement on exit settlement would be widely positive for CEE. UK is the second higher net contributor to the EU budget therefore a bigger exit bill will likely soften the impact the on EU budget near-term. Further positive news will be bullish for the PLN considering the currencies historical high sensitivity to Brexit related risks.