Sample Category Title

Japanese Core CPI Could Justify Monetary Stimulus

It's been almost two years since the Bank of Japan decided to adopt an aggressive monetary stimulus using negative interest rates to end deflation and force price growth up to the central bank's stability target of 2.0%. However, the BOJ's preferred inflation measure, the core CPI index which excludes volatile items, showed a slow reaction since the policy implementation, turning positive only in early 2017. Yet, the index was last still well below the target at 0.7% y/y, persuading policymakers to maintain the current ultra-easy monetary strategy, while price weaknesses have forced them to downgrade inflation forecasts in their last meeting in October.

Friday's readings on the core CPI index will be now in main focus, with analysts anticipating the gauge to edge up by 0.1 percentage points to 0.8% y/y in October, while they also expect the headline CPI index to retreat from 0.7% y/y to 0.2%. Moreover, the jobs-to-applications ratio and the unemployment rate released alongside the above data will be also in the spotlight given that the central bank predicts an improving labour market to drive prices higher. Particularly, October's jobs-to-applications ratio is estimated to rise slightly by 0.1 points to a fresh 43-year high of 1.53, while the unemployment rate is projected to remain steady at a 23-year low of 2.8%.

In other releases, Japanese household spending is expected to decline by 0.4% y/y in October after a contraction of 0.3% in the previous month, signalling weaker inflationary pressures. In contrast, business spending is expected to expand at twice the previous mark in the third quarter - at 3.3% y/y.

If indeed the data verify the BOJ's optimism on the economy and supports the efficiency of the current monetary policy, then the yen will likely post gains, pushing dollar/yen down to test the 200-day exponential moving average at 111.68. From here, the 50% Fibonacci retracement level of the upleg from 107.31 to 114.72 (September 8 - November 11) at 111 might come into view. Any close below this point would further increase risk to the downside, shifting focus towards the 61.8% Fibonacci of 110.14. If this occurs, then the bias will turn bearish from neutral in the short-term as the pair will break below the Ichimoku cloud. Alternatively, disappointing readings could work for the dollar, leading dollar/yen up to the area between the 38.2% and the 23.6% Fibonacci (111.90 - 113.00).

Pound Rally Continues as US Consumer Spending Slows

The British pound continues to post gains in the Thursday session. In North American trade, GBP/USD is trading at 1.3531, up 0.90% on the day. On the release front, British Nationwide HPI came in at 0.1%, shy of the estimate of 0.2%. In the US, unemployment claims edged lower to 238 thousand, below the estimate of 241 thousand. Personal Spending dropped to 0.3%, marking a 4-month low. Still, this beat the estimate of 0.2%. On Friday, manufacturing numbers will be in focus, as the US and UK release manufacturing PMIs.

Britain wants to kick-start the languishing Brexit talks and talk trade with the Europeans. This may have been the catalyst for Prime Minister May to sweeten the pot and going a long way to meeting the EU demands on Britain's divorce bill. The Europeans have demanded EUR 60 billion, while the UK had countered with EUR 20 billion. However, the UK has upped its offer significantly, and the final amount could be as high as EUR 50-60 billion. May is hoping that her improved offer will placate Brussels and pave the way for trade talks to begin in December. Another thorny issue on the Brexit plate is the status of the border between Northern Ireland and Ireland. Britain has ruled out having the north remain in a customs union with the EU after Brexit, but Ireland is insisting that there not be a hard border, and wants written guarantees from London as to the nature of the border after Brexit.

The US economy continues to perform well, and there was more good news on Wednesday, as Preliminary GDP for the third quarter posted a sharp gain of 3.3%. This was higher than the initial estimate of 3.0% and marked the fastest growth rate since Q3 of 2014. This was particularly impressive, as the southern US was battered by major hurricanes which caused significant economic damage. Consumer confidence levels are sky-high, but consumer consumption softened in the third quarter. However, business spending improved in the third quarter. Federal Reserve Chair Janet Yellen sounded upbeat about the economy, saying that the expansion was broad-based, across sectors of the economy.

Dollar Turns Cautious as Senate Tax Vote Eyed, Euro Shrugged Off CPI Miss

Mid-Day Report: Dollar Turns Cautious as Senate Tax Vote Eyed, Euro Shrugged Off CPI Miss

Quick update:

- Dollar tumbles after Republican Senator Susan Collins said "I am not committed to voting for this bill", referring to the tax bill.

- Pressure on dollar eased abit after John McCain said he supports

Dollar stays firm in early US session, except versus Sterling and Euro. Forex traders are turning a bit cautious as economic data from US provide little inspiration. Focus will turn to the Republican's tax plan debate and vote in Senate. Meanwhile, Euro reversed earlier dip on disappointing inflation data as buyers emerged. Sterling, on the other hand, remains the start performer this week as more positive Brexit news come out. In other markets, WTI crude oil recover mildly and is back above 57.7 after OPEC agrees to extend production cut. Gold, on the other handle is pressured and breaches 1280 handle. Stocks traders are still partying with DOW futures pointing to another record high today.

Released from US, personal income rose 0.4% in October, above expectation of 0.3%. Personal spending rose 0.3%, in line with consensus. Headline PCE slowed to 1.7% yoy but beat expectation of 1.5% yoy. Core PCE was unchanged at 1.4% yoy. Initial jobless claims dropped 2k to 238k in the week ended November 25. Continuing claims rose 42k to 19.6m in the week ended November 18. From Canada, current account deficit widened to CAD -19.4b in Q3.

UK-EU close to an Irish border agreement

Positive Brexit development continues to support Sterling. It's reported that UK and EU are close to agreement on the topic of Irish border. Ireland's EU commissioner Phil Hogan was quoted "in the same way as we have seen movement in the last 24 hours in relation to the financial settlement, I expect that we will see movement in this regard in the next few days as well." Earlier this week, it's reported that UK and EU have already agreed on the divorce bill at EUR 45-55b. The negotiation teams now look more likely than ever to make sufficient progress for EU leaders to approve moving on to trade talks in the December 14/15 summit.

Euro dipped briefly after CPI miss

Euro is weighed down by inflation data today, but it quickly recovered. CPI flash rose to 1.5% yoy in November, up fro 1.4% but missed expectation of 1.6% yoy. CPI core was unchanged at 0.9% yoy, below expectation of 1.0% yoy. Nonetheless, Eurozone unemployment rate dropped to 8.8% in October, down from 8.9% and hit the lowest level since 2009. From Germany, unemployment dropped -18k in November, better than expectation of -10k. German unemployment rate was unchanged at 8.8%.

ECB officials delivered upbeat comments

Comments from ECB officials were upbeat. Bundesbank head Jens Weidmann said that "evidence is mounting the economic outlook will be at least as good as previously forecast, if not even better." He added that "the development of domestic price pressures shown in the forecasts is in line with a path to our definition of price stability." And he also emphasized that "even after the end of net purchases, monetary policy in the euro area will continue to be very expansionary."

ECB Governing Council member Klaas Knot said yesterday that "with deflation risk clearly off the radar, the main rationale for employing the APP (asset purchase program) has therefore ceased to exist." He added that "fear of relapse owing to an allegedly premature discontinuation of net purchases seems rather overdone." Hence, he urged a "full phasing" out of the program "from September onwards". Back in October, ECB extended the asset purchase program to September next year, but halved the purchase size to EUR 30b a month starting January.

Swiss KOF indicates increasing growth momentum

Swiss KOF economic barometer rose to 110.3 in November, up from 109.8 and beat expectation of 109.5. That's the third straight months of gains in the indicator and stayed comfortably above long term average at 100. It also indicates that the economy continues to gain momentum towards the end of the year. Manufacturing continued to be responsible a "substantial part of the increase". However, banking slowed down the positive developments. Also from Swiss, GDP grew 0.6% qoq in Q3, in line with expectations. However, retail sales dropped sharply by -3.0% yoy in October versus consensus of 0.3% yoy rise.

New Zealand confidence tumbled

New Zealand Dollar suffered selling pressure as ANZ Business Confidence tumbled to -39.3 in November, down from -10.1. That's also the worst reading in 8 years. ANZ noted that "uncertainty around changing Government policy, a softer housing market, and difficulty getting credit are likely culprits." Also, "the economy is at a delicate juncture as migration, construction and housing run out of steam as growth drivers. Commodity prices are strong and a fiscal boost will come through in time, but at such times of transition, sentiment is more vulnerable." Separately released, building permits dropped -9.6% mom in October.

Elsewhere, Australia private capital expenditure rose 1.0% in Q3, building approvals rose 0.9% mom. Japan industrial production rose 0.5% mom in October, housing starts dropped -4.8% yoy. China manufacturing PMI rose 0.2 pt to 5.18 in November, non-manufacturing PMI rose 0.5 to 54.8.

OPEC to extend production cut to end of 2018

Oil price strengthens mildly today as OPEC agreed to extend its production cut to the end of next year. The current agreement to cut supply by around 1.8 bpd originally expires in March. Saudi Energy Minister Khalid al-Falih said before the meeting that it's premature to talk about exit. But "when we get to an exit, we are going to do it very gradually ... to make sure we don't shock the market." Iraq, Iran and Angola also expressed willingness to review the cut again at next OPEC meeting in June.

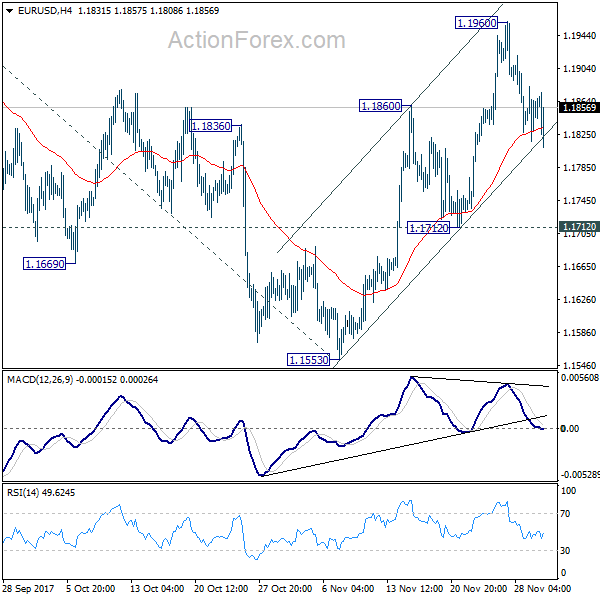

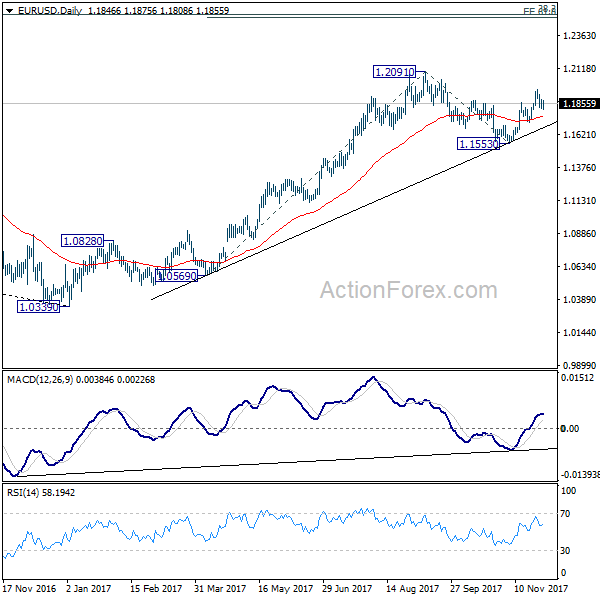

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1814; (P) 1.1849 (R1) 1.1881; More....

EUR/USD is staying in consolidation from 1.1960 and intraday bias remains neutral. With 1.1712 support intact, rise from 1.1553 is expected to resume later. Break of 1.1960 will turn bias to the upside for retesting 1.2091 high first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 will indicate completion of the rise from 1.1553 and turn near term outlook bearish.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Oct | -9.60% | -2.30% | -2.50% | |

| 23:50 | JPY | Industrial Production M/M Oct P | 0.50% | 1.80% | -1.00% | -1.00% |

| 00:00 | NZD | ANZ Business Confidence Nov | -39.3 | -10.1 | ||

| 00:01 | GBP | GfK Consumer Confidence Nov | -12 | -11 | -10 | |

| 00:30 | AUD | Private Capital Expenditure Q3 | 1.00% | 1.00% | 0.80% | 1.10% |

| 00:30 | AUD | Building Approvals M/M Oct | 0.90% | -1.00% | 1.50% | 0.60% |

| 01:00 | CNY | Manufacturing PMI Nov | 51.8 | 51.5 | 51.6 | |

| 01:00 | CNY | Non-manufacturing PMI Nov | 54.8 | 54.3 | ||

| 05:00 | JPY | Housing Starts Y/Y Oct | -4.80% | -2.80% | -2.90% | |

| 06:45 | CHF | GDP Q/Q Q3 | 0.60% | 0.60% | 0.30% | 0.40% |

| 08:00 | CHF | KOF Leading Indicator Nov | 110.3 | 109.5 | 109.1 | 109.8 |

| 08:15 | CHF | Retail Sales Real Y/Y Oct | -3.00% | 0.30% | -0.40% | |

| 08:55 | EUR | German Unemployment Change Nov | -18K | -10K | -11K | -12K |

| 08:55 | EUR | German Unemployment Claims Rate Nov | 5.60% | 5.60% | 5.60% | |

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 8.80% | 8.90% | 8.90% | |

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Nov | 1.50% | 1.60% | 1.40% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov A | 0.90% | 1.00% | 0.90% | |

| 13:30 | CAD | Current Account Balance (CAD) Q3 | -19.4B | -20.3B | -16.3B | -15.6B |

| 13:30 | USD | Initial Jobless Claims (NOV 25) | 238K | 241K | 239K | 240K |

| 13:30 | USD | Personal Income Oct | 0.40% | 0.30% | 0.40% | |

| 13:30 | USD | Personal Spending Oct | 0.30% | 0.30% | 1.00% | 0.90% |

| 13:30 | USD | PCE Deflator M/M Oct | 0.10% | 0.10% | 0.40% | |

| 13:30 | USD | PCE Deflator Y/Y Oct | 1.60% | 1.50% | 1.60% | 1.70% |

| 13:30 | USD | PCE Core M/M Oct | 0.20% | 0.20% | 0.10% | 0.20% |

| 13:30 | USD | PCE Core Y/Y Oct | 1.40% | 1.40% | 1.30% | 1.40% |

| 14:45 | USD | Chicago PMI Nov | 62.3 | 66.2 | ||

| 15:30 | USD | Natural Gas Storage | -46B |

Cable Surges above 1.3500

Cable surged through 1.3500 barrier on Thursday, hitting the highest level since 25 Sep. The pair extends acceleration, driven by strong bullish sentiment over Brexit talks and month-end dollar selling.

Eventual break through 1.3500 obstacle (1.3506 - Fibo 76.4% of 1.3655/1.3026 descend) opens way for final push towards key barrier at 1.3655 (20 Sep recovery high, the highest since Brexit vote).

Cable is up nearly 1% for the day so far and also on track for strong monthly bullish close that marks firm bullish signal.

Daily studies are overbought and suggest some corrective easing in the near-term, but without firmer signal for now.

Broken Fibo 61.8% at 1.3415 is expected to hold extended dips.

Res: 1.3570; 1.3600; 1.3618; 1.3655

Sup: 1.3506; 1.3476; 1.3415; 1.3404

Yen Shrugs Off Soft Japanese Data, Inflation Reports Next

The Japanese yen has ticked lower in the Thursday session. In North American trade, USD/JPY is trading at 111.79, down 0.12% on the day. On the release front, Japanese Preliminary Industrial Production slowed to 0.5%, well below the estimate of 1.9%. Japanese Housing Starts declined 4.8%, compared to the forecast of a 2.8% decline. Later in the day, Japan releases Tokyo Core CPI, with an estimate of 0.6%. In the US, unemployment claims edged lower to 238 thousand, below the estimate of 241 thousand. Personal Spending dropped to 0.3%, marking a 4-month low. Still, this beat the estimate of 0.2%.

Bank of Japan Governor Haruhiko Kuroda has insisted that the BoJ will not taper its massive stimulus program before inflation moves closer to the BoJ's target of around 2 percent. However, the BoJ has recently sent out subtle hints that it could tweak stimulus by allowing long-term interest rates to move higher. With Japanese investors holding JPY 450 trillion overseas, any rise in interest rates could reverse the flow of investment, resulting in massive amount of funds being repatriated back to Japan. Such a move would have a profound effect on global markets and would likely boost the Japanese yen. Investors are keeping a close eye on the BoJ, as any hints regarding tapering stimulus or raising rates could trigger gains for the Japanese currency.

The US economy continues to perform well, and there was more good news on Wednesday, as Preliminary GDP for the third quarter posted a sharp gain of 3.3%. This was higher than the initial estimate of 3.0% and marked the fastest growth rate since Q3 of 2014. This was particularly impressive, as the southern US was battered by major hurricanes which caused significant economic damage. Consumer confidence levels are sky-high, but consumer consumption softened in the third quarter. However, business spending improved in the third quarter. Federal Reserve Chair Janet Yellen sounded upbeat about the economy, saying that the expansion was broad-based, across sectors of the economy.

US: Just in Time: Income to the Rescue of Consumers But…

Personal income increased 0.4 percent in October, just in time for the holidays while spending growth slowed down but remained strong, up 0.3 percent, after a downwardly revised increase of 0.9 percent in September.

Finally Some Help from Income Growth

After a recent relatively long spell of weak income growth, the October release of personal income pointing to, perhaps, an improving path for income growth is a refreshing sign. Of course, a month does not make a trend, so we remain cautiously optimistic regarding the last two months of the year. Furthermore, we believe that income growth has to continue to improve for the right reasons in the next several quarters due to the still strong showing from the labor market.

Nominal disposable personal income was up 0.5 percent in October while real disposable personal income was up 0.3 percent, a notable improvement after a sequence of -0.1 percent, 0.1 percent, -0.1 percent, and 0.0 percent, during the June-September period, respectively. October marks the highest monthly rate since May of this year. Still, the increase in real disposable personal income has not come from much stronger wages and salaries. In fact, personal income increased by $65.1 billion in October versus an increase of $69.1 billion in September, with much of the weakness coming from wages and salaries of private industry workers. Wages and salaries of private industries increased $23.0 billion in October versus $33.7 billion in September. At the same time, Americans got higher income from receipts on assets, up $19.2 billion in October versus only $10.3 billion in September. But perhaps the largest help for disposable personal income was the fact that Americans paid $14.3 billion in personal current taxes in September while having a "tax rebate" of $1 billion in October. That is, all what was good for personal income but especially disposable personal income seem to have been one-off rather than something that will continue in the next several months.

Thus, it is clear that income is still constrained and our expectation that income is going to start increasing has not yet materialized. Thus, we remain cautiously optimistic for the holiday season.

Spending Growth Weakens in October

On the spending side, we were expecting some weakness because of the strong showing in September. Personal spending increased 0.3 percent in nominal terms but only 0.1 percent in real terms after increases of 0.9 percent and 0.5 percent, respectively in September.

This may indicate trouble ahead for consumption during the last quarter of the year; however, we believe that conditions remain positive for a strong showing in consumer demand during the final quarter. Positive conditions are supported by the strong showing in consumer confidence, a very strong labor market, this past month's improvement in real disposable income, plus the slight improvement in the savings rate. Thus, we are still positive on the spending picture going into the holiday sales season.

Euro Withstands Soft EMU Inflation Data

- European equities eke out decent gains after yesterday's setback. US equities opened with good gains (+/-0.5%) as fears about yesterday's Tech sell-off eased.

- The world's biggest oil producers are close to extending a deal to curb oil production throughout 2018, OPEC ministers said on Thursday, with more work needed to shrink swollen stockpiles and underpin prices above $60 a barrel. Brent oil rose over $64/barrel

- India's economy grew at a 6.3 per cent annualised pace in Q3, reversing five quarters of slowing growth and up from 5.7% Y/Y in Q2. The improved figures should prove some relief for Mr Modi as he heads in to the next round of regional elections towards the end of the year.

- Inflation in the eurozone hit 1.5% this month, up from 1.4% in October, but was weaker than the 1.6% reading economists had expected. Core inflation came in at 0.9%, the same as last month. Unemployment rate fell to 8.8% last month, from 8.9% in September. Unemployment is now at its lowest level since the beginning of 2009.

- The Swiss Kof economic barometer climbed further in November from last month's seven-year high, topping the highest estimates in a Reuters poll. It came in at 110.3 points, the third consecutive increase and up 0.5% up from October.

Rates

Core bonds trade narrowly mixed

Core bonds traded listless in a tight range, ending narrowly mixed (Germany) to marginally higher (US). On intra-EMU bond markets, peripherals 10-yr yield spreads narrowed 1 to 2 bps. The weaker-than-expected euro area inflation for November was behind the only intra-day movement of significance.

The Bund opened little changed (162.52) and eased slightly in the first couple of hours (162.24 low). A "turnaround" occurred mid-morning when euro area inflation was reported at 1.5% Y/y and 0.9% Y/Y (core) That was weaker than expected and pushed the Bund again above the starting line (162.75 high). However, there was no follow through buying and sideways trading dominated till the closure of our report (range 162.75-162.55). Equities eked out modest gains and oil price went higher, but impact on core bonds was minimal.

During the US session, personal spending and income were in line with expectations and the deflators were close to expectations. As also initial claims were near recent outcomes, the eco data had no noticeable impact on US Treasuries. The T-Note future opened at 124-10+ and trades now at 124-09 with intra-day wiggles negligibly small. At the time of writing, the German yields were flat (5-yr) to 0.9 bp (10-yr) lower. The US yields rose between 0.4 (10-yr) and 0.8 bp (2/5-yr).

Currencies

Euro withstands soft EMU inflation data

Trading in the major USD cross rates showed no clear pattern today. The euro suffered temporary from soft EMU inflation data, but the decline slowed soon. US data were too close to expectations to kick-start a meaningful USD move. USD/JPY (112.40 area) extends its rebound as equities find their composure after yesterday's setback. EUR/USD is going nowhere in the mid 1.18 area.

Overnight, Asian equities traded with substantial losses as tech shares suffered from the Nasdaq correction. The November China PMI (both manufacturing and services) improved, but didn't help sentiment. Japanese equities decoupled from the broader correction supported by yesterday's USD/JPY rebound. The pair traded in the low 112 area. EUR/USD showed no clear trend and traded in the 1.1860/70 area.

European equities started hesitant, but soon decoupled from the Tech correction. The constructive open in Europe prevented a further decline in core yields and also supported the dollar. Mid-morning, USD strength was temporary replaced by euro softness as the EMU November inflation data printed again below consensus at 1.5% Y/Y for the headline figure and 0.9% Y/Y for core CPI. EUR/USD touched an intraday low in the 1.1810 area.

Early in US dealings, the EUR/USD reversed part of the earlier losses as investors counted down to the US data. October spending (0.4%) and income (0.3%) were close to expectations as were the jobless claims. However, markets were mostly interested in the price data of the report. The headline PCE deflator was slightly higher than expected at 1.6% Y/Y. The core PCE was as expected (1.4%Y/Y). The deviations from consensus were too small to trigger a meaningful market reaction. EUR/USD hovers in the mid 1.18 area. USD/JPY trades near 112.30/40, awaiting how (US) equities will perform after recent gyrations.

In a broader perspective, USD/JPY is gradually moving further away from the recent low. A bottoming out process might be developing if equities maintain their composure. EUR/USD also trades off the correction top but the decline still has no strong momentum, despite today's low EMU inflation data.

Sterling maintains constructive bias

Today, sterling extended the gradual rise that started earlier this week as the UK and the EU are said to have reached a provisional agreement on the Brexit divorce bill. Since yesterday, there also plenty of rumours that progress has been made on the delicate issue of the border between Northern Ireland and the Irish Republic. There was not much of additional positive news today. As usual, there were even some headlines downplaying recent progress. However markets are hopeful that a meeting of UK PM May and EU's Juncker on Monday will yield more good news, maybe even an outright breakthrough on the conditions the EU wants to be fulfilled to start negotiations on the future EU/UK relationship. EUR/GBP dropped temporary below the 0.88 barrier. Soft EMU inflation data reinforced this move, but the euro rebounded later in the session. EUR/GBP trades currently in the 0.8815 area. Cable also returned part of the early session gains but still trades comfortably above 1.34 level (mid 1.34).

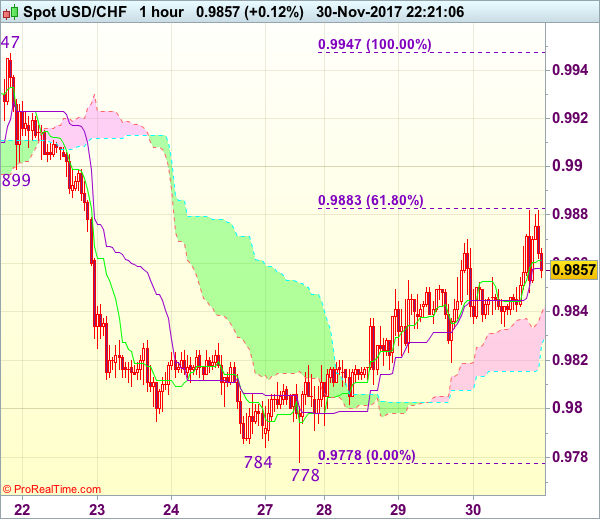

Trade Idea Update: USD/CHF – Sell here

USD/CHF - 0.9857

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9861

Kijun-Sen level : 0.9858

Ichimoku cloud top : 0.9839

Ichimoku cloud bottom : 0.9826

Original strategy :

Sell at 0.9885, Target: 0.9785, Stop: 0.9920

Position : -

Target : -

Stop : -

New strategy :

Sell at market level, Target: 0.9760, Stop: 0.9890

Position : -

Target : -

Stop : -

Dollar only edged higher to 0.9882 before retreating again (just missed our short entry at 0.9885), suggesting consolidation with downside bias would be seen and test of support at 0.9819 is likely, however, a firm break below there is needed to signal the rebound from 0.9778 has ended, bring a retest of this support, break there would extend recent decline from 1.1038 top towards 0.9730-37 support area but reckon support at 0.9705 would hold from here.

In view of this, we are looking to sell dollar here. Only break of 0.9895-00 would defer and signal a temporary low is formed instead, bring a stronger rebound to 0.9920 but price should falter well below resistance at 0.9947.

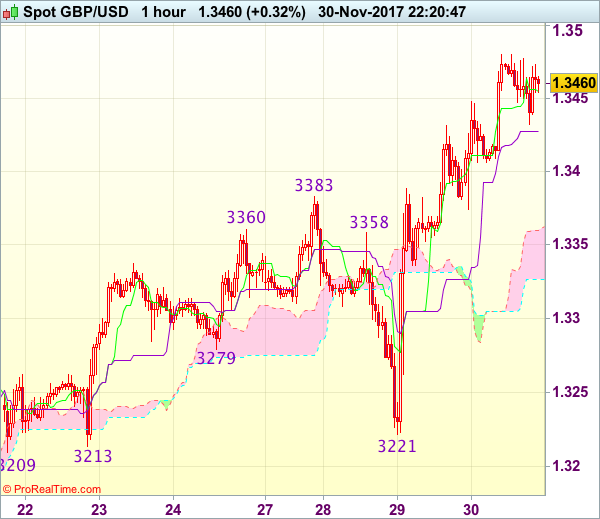

Trade Idea Wrap-up: GBP/USD – Buy at 1.3385

GBP/USD - 1.3468

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3464

Kijun-Sen level : 1.3435

Ichimoku cloud top : 1.3360

Ichimoku cloud bottom : 1.3326

Original strategy :

Buy at 1.3385, Target: 1.3485, Stop: 1.3350

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3385, Target: 1.3485, Stop: 1.3350

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after recent rally above previous resistance at 1.3383 (now support), adding credence to our bullish view that the erratic rise from 1.3027 low is still in progress, hence upside bias remains for this move to extend further gain to 1.3480-85, however, overbought condition should prevent sharp move beyond 1.3500-10 and price should falter below 1.3525-30, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy sterling on subsequent pullback as 1.3383 (previous resistance turned support) should limit downside and bring another rise. Below 1.3355-60 would suggest top is formed instead, bring weakness to 1.3330, then towards 1.3300 but reckon downside would be limited to 1.3260-65.

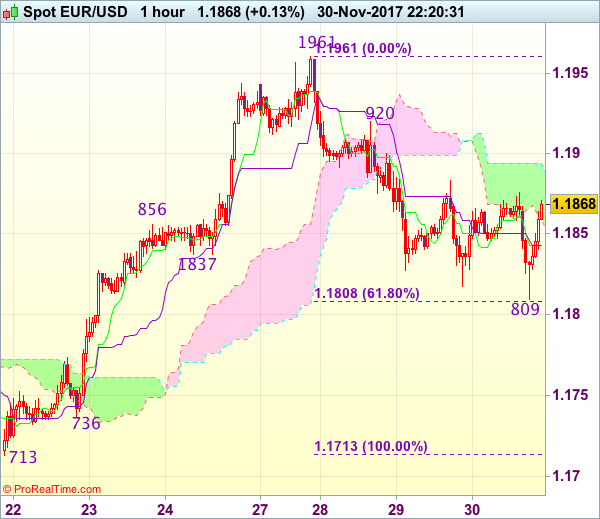

Trade Idea Wrap-up: EUR/USD – Buy here

EUR/USD - 1.1868

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1860

Kijun-Sen level : 1.1850

Ichimoku cloud top : 1.1894

Ichimoku cloud bottom : 1.1859

Original strategy :

Bought at 1.1864, stopped at 1.1835

Position : - Long at 1.1864

Target : -

Stop : - 1.1835

New strategy :

Buy at market level, Target: 1.1965, Stop: 1.1835

Position : -

Target : -

Stop : -

Although the single currency slipped again to 1.1809, as euro found renewed buying interest there and has staged another rebound, suggesting an intra-day low is formed there and consolidation with upside bias is seen for gain to 1.1895-00, however, break of indicated resistance at 1.1920 is needed to signal the pullback from 1.1961 has ended at 1.1817, bring further gain towards this level, break there would extend recent upmove to 1.1990-00 which is likely to hold from here.

In view of this, we are looking to buy euro again on dips. Below 1.1830-35 would risk retest of 1.1809 but only break there would signal the retreat from 1.1961 is still in progress for retracement of recent rise towards 1.1770 but price should stay well above support at 1.1736, bring rebound later.