Sample Category Title

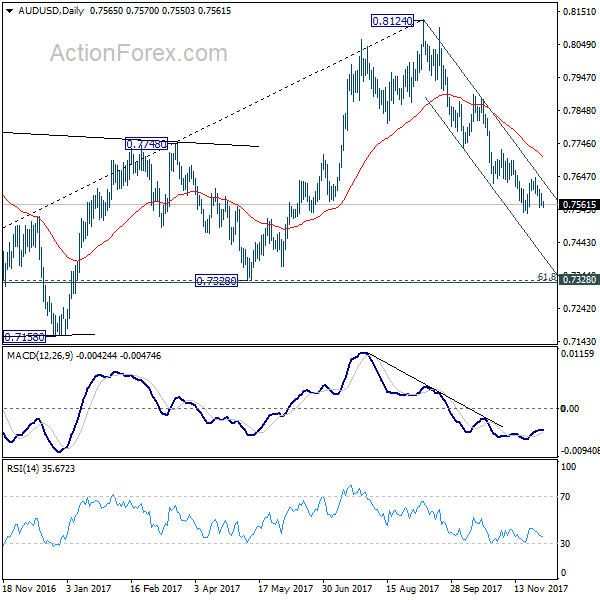

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7549; (P) 0.7572; (R1) 0.7587; More...

Intraday bias remains neutral as consolidation from 0.7531 is in progress. Near term outlook stays bearish with 0.7729 resistance intact and deeper decline is expected. Break of 0.7531 will resume whole decline from 0.8124 and target next key cluster level at 0.7322/8. However, considering bullish divergence condition in 4 hour MACD, break of 0.7729 will indicate near term reversal and bring stronger rebound back to 0.7896 resistance and above.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8049). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7729 near term resistance holds.

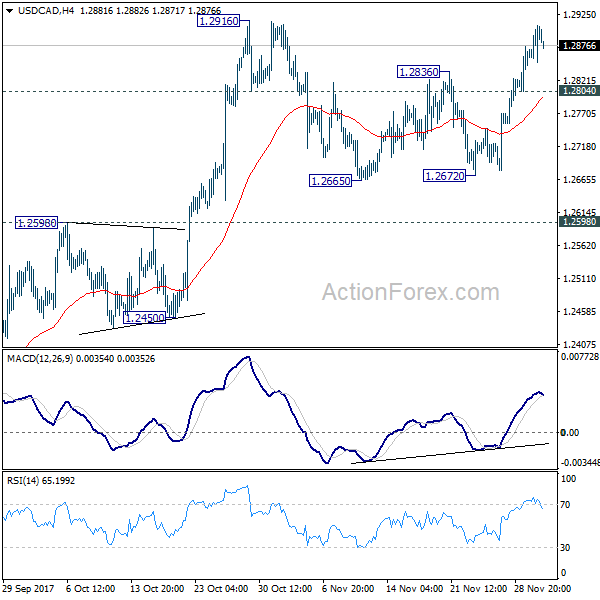

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2822; (P) 1.2847; (R1) 1.2890; More....

USD/CAD's rise is still in progress and intraday bias remains on the upside for 1.2916 high. Decisive break there will confirm resumption of whole rally from 1.2061. In that case, USD/CAD should target 1.3065 medium term fibonacci level next. On the downside, though, below 1.2804 will argue that consolidation from 1.2916 is extending with another falling leg. And intraday bias will be turned back to the downside for 1.2672 support. But still, we'd expect downside to be contained by 1.2598 resistance turned support and bring rise resumption.

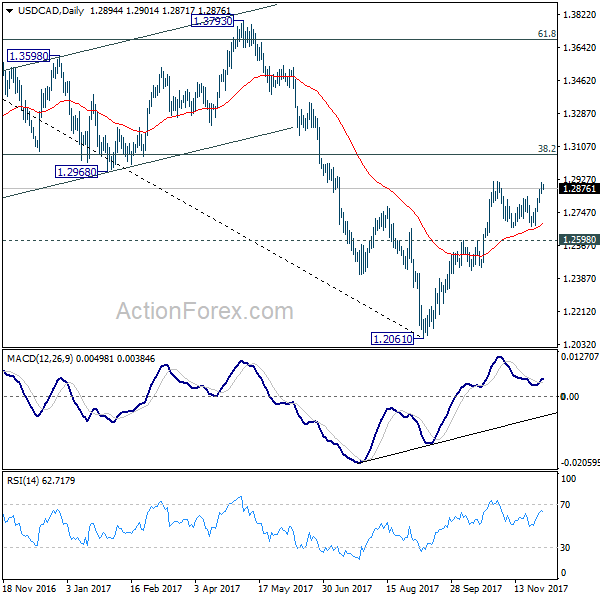

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

US Equities Continued Record Runs on Tax Hope, Yields Rebounded, Dollar Ties With Euro Following Sterling

US stocks were once again boosted by optimism on Senate passing the tax bill. DOW gained 331.67 pts or 1.39% to close at 24272.35. S&P 500 rose 21.51 pts or 0.82% to end at 2647.58. Both were at record highs. NASDAQ lagged behind but still gained 49.58 pts or 0.73%. Though, Asian markets don't follow and are trading mixed at the time of writing. It should also be pointed out that treasury yield also staged strong rally. 10 year yield closed up 0.041 at 2.417 and looks very safe from key near term support at 2.273. More positive news on tax bill could push 10 year yield through near term resistance at 2.475, which will give support to Dollar, in particular USD/JPY.

In the currency markets, Sterling remains the strongest one for the week. News about agreement on Brexit divorce bill and Irish border raised optimism that there will be sufficient progress made before December 14/15 EU summit. That is, UK and EU could be very ready to move on to trade talks soon. Dollar and Euro follow closely, competing to be the second strongest. Canadian Dollar is trading as the weakest one for the week so far and will look into GDP and employment data for a little help.

Senate to continue marathon debate on tax bill on Friday

The Senate didn't vote on the bill on Thursday and the marathon debate will continue on Friday. There was some jitters in the markets after Susan Collins expressed that she's still noted "committed" to the bill. However, sentiments were then lifted as John McCain, a wild card, expressed his support. There was call for a trigger to raise tax if growth induced rise in revenue couldn't cover the loss. That was raised by Bob Corker, Jeff Flake and James Lankford to avoid ballooning deficit. But the idea was rejected and Republicans are left to find other ways, including raising some taxes down the road to help offset the costs. Developments in the Senate will continue to catch attention during the weekend.

As coalition talks started, SPD Gabriel pleaded "not to put pressure on us"

German Chancellor Angela Merkel and Social Democratic Party leader Martin Schulz met at the presidential palace for more than two hours, kicking the grand coalition talks. President Frank-Walter Steinmeier, who arranged the meeting, said before that "I expect everyone to be willing to negotiate and to make it possible to form a government in the foreseeable future". But the negotiation could take more than just a few weeks.

SPD Foreign Minister Sigmar Gabriel, who was not at the meeting, emphasized that "we're now in a process orchestrated by the president, in which we first need to look at what the possibilities are but no one can expect it to go quickly." Gabriel pointed out that "the conservatives, Greens and FDP took months to get nothing off ground so I'd ask people not to put pressure on us." Latest poll by Allensbach found that nearly two-thirds of Germans, surveyed between November 22/27, wanted SPD to start coalition talks with CDU/CSU.

China economy may come under pressure in 2018

China Caixin PMI manufacturing dropped to 50.8 in November, down from 51.0 and below expectation of 51.0. That's also the lowest level in five months. In the statement, Zhengsheng Zhong, director of macroeconomic analysis at CEBM Group, a subsidiary of Caixin, said that "for the most part, the manufacturing sector remained stable in November, although some signs of weakness emerged." And, "in the fourth quarter, the economy is likely to maintain the stability observed since the start of the second half of the year" and "economic growth in 2017 is expected to be higher than last year". However, he also warned that "it may come under downward pressure in 2018."

Elsewhere

Japan national CPI rose to 0.8% yoy in October, Tokyo CPI was unchanged at 0.6% yoy in November. Inflation stays well below the 2% target and justify BoJ's massive stimulus. Also from Japan, unemployment rate was unchanged at 2.8% in October, household spending rose 0.0%. Japan capital spending rose 4.2% in Q3. PMI manufacturing was revised down to 50.8 in November. Also released, New Zealand terms of trade index rose 0.7% qoq in Q3, below expectation of 0.7% qoq.

Looking ahead: PMI manufacturing will be main focus in European session. UK and Swiss will release PMI manufacturing while Eurozone will release PMI manufacturing revision. Later in the day, Canada will release GDP and employment. US will release ISM manufacturing and construction spending.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2822; (P) 1.2847; (R1) 1.2890; More....

USD/CAD's rise is still in progress and intraday bias remains on the upside for 1.2916 high. Decisive break there will confirm resumption of whole rally from 1.2061. In that case, USD/CAD should target 1.3065 medium term fibonacci level next. On the downside, though, below 1.2804 will argue that consolidation from 1.2916 is extending with another falling leg. And intraday bias will be turned back to the downside for 1.2672 support. But still, we'd expect downside to be contained by 1.2598 resistance turned support and bring rise resumption.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q/Q Q3 | 0.70% | 1.30% | 1.50% | 1.40% |

| 23:30 | JPY | Unemployment Rate Oct | 2.80% | 2.80% | 2.80% | |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | 0.00% | -0.30% | -0.30% | |

| 23:30 | JPY | National CPI Core Y/Y Oct | 0.80% | 0.80% | 0.70% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 0.60% | 0.60% | 0.60% | |

| 23:50 | JPY | Capital Spending Q3 | 4.20% | 3.20% | 1.50% | |

| 0:30 | JPY | PMI Manufacturing Nov F | 53.6 | 53.8 | 53.8 | |

| 1:45 | CNY | Caixin PMI Manufacturing Nov | 50.8 | 51 | 51 | |

| 8:30 | CHF | PMI Manufacturing Nov | 62.5 | 62 | ||

| 8:45 | EUR | Italy Manufacturing PMI Nov | 58.3 | 57.8 | ||

| 8:50 | EUR | France Manufacturing PMI Nov F | 57.5 | 57.5 | ||

| 8:55 | EUR | Germany Manufacturing PMI Nov F | 62.5 | 62.5 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Nov F | 60 | 60 | ||

| 9:30 | GBP | PMI Manufacturing Nov | 56.5 | 56.3 | ||

| 13:30 | CAD | GDP M/M Sep | 0.10% | -0.10% | ||

| 13:30 | CAD | Net Change in Employment Nov | 10.0k | 35.3k | ||

| 13:30 | CAD | Unemployment Rate Nov | 6.20% | 6.30% | ||

| 14:30 | CAD | Manufacturing PMI Nov | 54.3 | |||

| 14:45 | USD | Manufacturing PMI Nov F | 53.8 | 53.8 | ||

| 15:00 | USD | ISM Manufacturing Nov | 58.3 | 58.7 | ||

| 15:00 | USD | ISM Prices Paid Nov | 67.8 | 68.5 | ||

| 15:00 | USD | Construction Spending M/M Oct | 0.50% | 0.30% |

GBP/JPY Higher Out Of Support

We've been watching this key GBP/JPY support/resistance level for a while, and enjoying having a clear zone like this to manage our risk around.

'GBP/JPY Daily:

'These types of setups really are a risk manager's dream and I hope that you're taking advantage of the opportunities that are continuing to be gifted to you by the markets.

Find your levels, trade your levels and manage your risk.'

Find your levels and trade your levels indeed!

Just another example of price pulling back into a zone where buyers are waiting to soak up the supply and price rocketing off it as a result:

GBP/JPY Daily:

Being in a major bullish trend, a bounce at support was always the preferred option from a day trading perspective.

With price now approaching the previous swing high again, you're essentially able to give yourself a free ride. If price can break higher again, it's a nice early Christmas present now we're into December.

OPEC + Extends Cuts – June Review Frets Market

- OPEC+ agreed to extend output cuts by 9M with Libya and Nigeria joining the deal, which is set to be reviewed in June.

- The oil market was left disappointed by the risk of OPEC+ ending cuts prematurely by mid next year.

OPEC+ (the 30 oil producing countries in OPEC and outside OPEC) today agreed to extend the deal from last November to cut output by another nine months; hence, until the end of 2018. In addition, Libya and Nigeria joined the deal and agreed to freeze output at 2017 highs. Finally, the group announced that it plans to review the deal in June next year. In relation to the latter part, it is worth noting that the group was said to have discussed a potential exit strategy from cuts yesterday.

The announcement was about as expected in terms of the extension of production cuts and the addition of Libya and Nigeria to the mix. The latter two are already producing close to full capacity; hence, the caps put on their respective output are more of a symbolic character. The latter part of the agreement today, the plan to review cuts in June next year, took the market by surprise. OPEC+ has effectively only committed to cutting production until the June review, which means it has only committed to three months of additional cuts in practice.

The fact that the focus around the OPEC meeting has now turned towards the timing and content of an exit strategy caused the oil market to sell off on the announcement with the price on Brent crude falling to USD62/bbl from USD64/bbl before the meeting. That is a significant price drop for the oil market and could be a signal of what to come. Positioning is stretched long crude and the USD has stopped depreciating. The geopolitical risk factor is looming in the background though to provide some support. Overall, we look for the price on Brent crude to average USD63/bbl next year, while OPEC+ could be more of a downside risk factor if it starts to market an exit strategy.

OPEC and Non-OPEC Group Agrees to Extend Production Cuts Until the End of 2018

At the 173rd Meeting of the OPEC Conference, OPEC members agreed that the global crude oil market is moving in the right direction. Production adjustments to date are having their desired effect, with inventories falling by half their target amount in 2017.

This reduction in inventories has resulted from a combination of stronger-than-expected demand and high rates of compliance among the OPEC and non-OPEC group with respect to their production quotas.

The pace of inventory reduction is expected to slow (or even reverse course) as we move through a period of seasonally weaker demand, but OPEC anticipates inventories to fall to their 5-year average by the end of 2018 with the extension of supply cuts.

Accordingly, both OPEC and the group of non-OPEC producing countries agreed today to extend the production cuts until the end of 2018. The group intends to assess market conditions next June to consider whether any further adjustments are needed.

Third-party media reports indicate that today's extension of supply cuts includes Libya and Nigeria for the first time, with an agreed upon collective cap higher than current combined production levels. As such, the inclusion - which will take effect in January - will not have an impact on current production levels.

Prior to today's meeting, Russia had been intent on discussing the exit strategy in order to gain some clarity on what comes after the market is in a more balanced position. Meanwhile, the Saudi Oil Minister indicated that it is too early for those discussions given that there is still a large amount of inventory that must be eliminated. As of yet, there has been no mention of how these output cuts will be phased out once the market is in balance.

Key Implications

An agreement on extending the production cuts through the end of 2018 was largely priced in. Once the decision had been finalized, market reaction was subdued with prices holding relatively steady.

The WTI benchmark has been sitting in the US$55-59 per barrel range in recent weeks. Given the supply-demand fundamentals, it appears as though oil prices have been bid up too much and are unlikely sustainable in their current range. Now that the extension of production cuts has been confirmed, there is likely to be some profit taking, taking prices back below US$55 per barrel. Barring any significant supply disruptions, prices are likely to sit in the US$50-55 per barrel range until the market moves into a more balanced position.

A key risk for 2018 remains the evolution of U.S. shale production, as it is still a challenge for OPEC. Production there is sitting near record levels and hedging activity has been on the rise. U.S. output could continue to surprise on the upside going forward, acting to delay OPEC's goal of bringing inventories down to the 5-year average by the end of next year.

You’re Fired or Maybe Not

Its been a year to remember in Global politics and by all accounts, December looks like it will be chalk full of political goodies. The stakes are enormously high for both Brexit and tax reform resolutions, but questions continue to swirl around the Trump administrations as 'Rexit" (Rex Tillerson Firing ) reports, rumours and innuendos emanating from the Foggy Bottom brings the administrations credibility into question once again. Well you know what they say where there's smoke, there's fire and nothing could be more accurate about the Trump administration record. Even if nothing definitive emerges from 'Rexit, not that it should be a long-lasting dollar negative, the real question is who's next on the firing line??

Prospects for tax reform are convincing with the market pricing in a 75 % chance it will go through. Senate Majority Leader McConnell says passage is likely Thursday night or Friday. If indeed the case, that would lay the first stone for a Republican joint Conference to arbitrate the variances between the House and Senate versions

On the Brexit front, reports citing an EU official who claims that the EU and UK have agreed to a financial settlement keeps the momentum rolling for a market-friendly parting of the ways.

Economic Data

Core PCE data has come out at 0.2%MoM and 1.4%YoY – precisely in line with expectation and generated dollar selling as hope for future uptick does little to support the cause of the dollar.

Eurozone inflation data missed the market slightly but was inconsequential as far as the market was concerned.

G-10 FX

Overnight price action was practically incomprehensible given month end rebalance mayhem where the greenback gained in some wallets and weighed in others despite 10Year US bond yields nudging higher overnight.

The Japanese Yen

The path of least resistance appears higher as US yields rise and tax reform risk unwinds. Provided there are no significant unexpected risk catharsis or the BoJ backs off the YCC program, USDJPY should remain well supported on dips. Overnight saw risk aversion creep into the equation when the market sold off on the "Rexit " headline but dollars were hoovered up as risk appeal for the US tax reform is too loud to ignore

The Euro

As EU political risk fades, the Euro will continue to take cues from economic data. The EU CPI data registered a small insignificant miss as Eurozone's booming economy foreshadows an ECB policy showdown. The Euro should remain firm on strong data flow. The Euro made an astonishing move overnight based traders pervasive apprehension about missing out on a possible shift in ECB rate policy. But with the Brexit bluster lessening the EU is riding the wave of progress.

The British Pound

Brexit positivity has underpinned GBP even with the dollar catching a broader bid. But we should expect the pound to remain embroiled in the Brexit bluster suggesting a limited top side until the dust settles later in December when divorce talks should reach a crescendo.

The New Zealand Dollar

The Kiwi continues to sag on weak business confidence while the political overhang continues to weigh on broader sentiment.But with the market looking for political risks to abate we could see a reversal of fortunes sooner than later.

Australian Dollar

Some recently engaged tactical year-end longs are packing it in as the Aussie continues to gain little traction in the face of diminishing yield advantage. With little support offered on the domestic front, the AUD should remain pressured by the stronger US dollar and firmer US dollar yields with the US 10 year treasuries breaching the 2.40 level.

Energy Markets

OPEC had extended production deal by 9m and agreed to review those cuts in June (6m) rather than the 3m ( April ) hawked about on Wednesday. Indeed, a better result than what could have been and should underpin oil prices through year-end.But oil traders were slow off the mark suggesting that either position is too heavy long in their view or that that the agreement is not constructive enough to inspire a significant push higher.

Local EM Fx traders are in price discovery mode given the pro and con susceptibility various regional currencies will have to higher oil prices. INR vulnerable while MYR resilient pointing to some interesting regional cross trade nuances

Asia FX

The Malaysian Ringgit

It's a Malaysia public holiday in observance of the Prophet Muhammad' s birthday so trading should be rather muted.

The Bank of Korea offered up a dovish rate hike which caused a wave USD short covering. The Won has been a proxy for the regional currencies of late, so it dulled the Ringgits sharp-edged momentum.

US yields are rising but rates remain rangebound and only sustained a break of 2.4 % in the 10 Year US Treasuries would push USD dollar significantly higher. However, this is unlikely to happen unless there are some definite signs of inflation

Month-end activity tends to be very messy on the USD as there is more rebalancing activity than actual market momentum flow, tends to cloud the big picture.

Expect 4.07 4.11 range early next week as we may enter a consolidation phase with investors optimism waning as holiday season thin liquidity is creeping into the picture

Rising US yields present the most significant obstacle to a stronger Ringgit next week so investors will continue to monitor the US yield curve in earnest

The Korean Won

The widely expected BOK dovish rate hike:

- The Won was appreciating too rapidly which unwinded any momentum for a hawkish expectation

- IRS market is still implying a little under two more rate hikes over the next 12 months, so not much change there

- The BoK remains the most assertive regional central bank regarding future normalisation

- The USDKRW bounced aggressively higher but likely compounded by equity outflows as the global tech sector rout weighed on Samsung shares.

- The US ten-year yields were moving higher adding to the positive USD momentum

There's a balancing act when it comes to monetary policy as the CB can choose to tighten financial conditions through a stronger currency or higher interest rates. To prevent " financial imbalances" from the stronger Won, the BoK tacked dovish but left the door wide open for further rate hikes down the road.

The market continues to price in a shallow rate hike cycle, but the Won should continue to benefit from a strong economy supported by the global growth storyline and long-standing sizeable current account surplus. But more significantly, the BoK may be more supportive to a pace of gradual appreciation of the Won as opposed to monetary policy to ward off inflation.

Given the market will continue to express a bullish Asia view through the KRW, the market will likely try to add dollar shorts. Korean Asset should remain in high demand, after all, when is a dovish rate negative for equity or bond markets? Also, any significant move lower on USDKRW should attract exporter and corporate need to convert dollars. Also

The primary risk to the bullish Korean Won storyline comes not from the BoK dovish rate hike but rather a sudden meltdown in global equities or an unexpected hawkish shift from the Federal Reserve Board.And of course, traders will continue to monitor the North Korea escalation as the market continues to sidestep Korean Peninsula risk after the latest missile test.

Market Musing

The US Dollar

While tax headlines are dominating, the market remains tacitly focused on US inflation which suggests a tax reform victory in the Senate may have a muted dollar reaction as subdued inflation could ultimately weigh on US yields.

Canadian Dollar Falls with US Tax Reform in Final Stretch

The Canadian dollar depreciated on Thursday on the back of the divisive US Tax reform gaining traction after receiving the backing of Republican Senator John McCain. The Canadian current account deficit grew to 19.35 billion Canadian dollars in the third quarter. The third largest deficit resulted from a drop in exports of goods and motor vehicles with services remaining unchanged.

The USD/CAD remains close to the 1.29 price level ahead of the release of the monthly Canadian GDP numbers and the change in jobs data to be released at 8:30 am EST on Friday, December 1. The US jobs data will be released next week leaving the Canadian jobs data to steal the spotlight, but there are concerns after the new ADP report showed the economy losing 5,700 positions in October versus the 35,000 added jobs reported by Statscan. The official figure released by Statscan will be followed by investors on a quiet data release Friday with a forecast that calls for a gain of 10,000 positions in November.

The USD/CAD gained 0.26 percent on Thursday. The currency pair is trading at 1.2896 as the USD moved higher against commodity currencies on the back of the progress on US tax reform. The Senate bill has gained backing from some undecided Republican Senators, most notably Sen John McCain. The White House needs 52 senators to back the bill to pass it given the unified opposition from Democrat Senators.

The loonie has been on the back foot this week with the USD gaining 1.53 percent in the last 4 days on the market optimism that the Trump Administration could score a victory. Expectations of a rate hike by the U.S. Federal Reserve in December are high, and already priced into the pair, but the Bank of Canada (BoC) is seen more dovish by the minute. A new Reuters survey of 30 economists shows that there is little expectation of a rate move by the Canadian central bank in December, and a third see April at the earliest.

Factors such as the precarious state of the NAFTA renegotiations and evidence of the economy slowing down have cooled the BoC's desire to reduce further stimulus worried about the effect of higher interest rates on borrowers that hold record high levels of debt. The two data releases on Friday could confirm the headwinds facing the loonie, or in case they over perform expectations give the currency a boost against the US dollar.

Oil was volatile on the eve of the Organization of the Petroleum Exporting Countries (OPEC) announcement of a production cut agreement extension. West Texas Intermediate is trading at $57.23 after oil producers agreed to extend the duration of their production reduction by 9 months. The 1.8 million cut in daily barrels will continue until the end of 2018. The market had already priced in such a move after numerous statements and comments from Energy Minister from OPEC and non-OPEC alike. Despite the united front there are various calls within the bloc to look for an exit strategy. Russia in particular is keen to get back to full production, but for now will seek stability than profits.

Nigeria and Lybia who were exempt from the original production cut have now been limited to not exceed the levels from this year as compliance within the group will be a challenge.

US shale producers continue to ramp up production and free from weather disruptions will put pressure on crude prices that have been boosted by the effort put forth by the OPEC. The technology advances that made oil extraction cheaper created a sudden drop in prices as the OPEC sought to price them out of the market in a strategy that backfire by exchanging market share for profits.

Diplomatic stability within the producers organization will prove to be difficult as Saudi Arabia has taken a more aggressive role in domestic and regional politics which could pit it against number two and three producers Iraq and Iran.

Market events to watch this week:

Friday, December 1

- 4:30am GBP Manufacturing PMI

- 8:30am CAD Employment Change

- 8:30am CAD GDP m/m

- 10:00am USD ISM Manufacturing PMI

*All times EDT

Gold Slips to 14-Day Low as Jobless Claims Beats Estimate

Gold has posted considerable losses for a second straight day. In Thursday's North American session, the spot price for an ounce of gold is $1274.06, down 0.75% on the day. In the US, unemployment claims edged lower to 238 thousand, below the estimate of 241 thousand. Personal Spending dropped to 0.3%, marking a 4-month low. Still, this beat the estimate of 0.2%. On Friday, the US releases Manufacturing PMI.

There was more good news for the US economy on Wednesday. Preliminary GDP for the third quarter posted a sharp 3.3%, as expected. This was higher than the initial estimate of 3.0% and marked the fastest growth rate since Q3 of 2014. This was particularly impressive, as the southern US was battered by major hurricanes. Although consumer consumption was softened in the third quarter, business spending improved. The rosy picture of the US economy was summarized by Fed Chair Yellen on Wednesday, who said that the expansion was broad-based, across sectors of the economy.

Gold prices are inversely linked to interest rate hikes, and with the markets expecting rate hikes in December and January, traders should be prepared for some movement from gold. As well, there are major changes taking place at the Federal Reserve, as Jerome Powell is set to replace Janet Yellen as Fed chair in February. Powell didn't make any waves at his confirmation hearing on Tuesday, although his comments on relaxing regulations for smaller banks did send global stock markets higher. Powell inherits a strong US economy, and this could mean several rate hikes in 2018, if the economy maintains its current pace. Still, inflation remains stubbornly low, and with Fed policymakers divided on whether to keep the 2 percent inflation target, the markets will be keeping close tabs on how Powell deals with inflation when he takes over the helm of the Fed.

Swiss Economy Remains on Solid Footing in Q3

Executive Summary

Growth in the Swiss economy strengthened in Q3, up 2.5 percent on an annualized basis. While GDP growth in Switzerland has been more muted over the past few quarters, today's print affirms broad-based growth in both domestic and external demand. Amid solid economic growth, Switzerland has faced low inflation over the past several years, pushing the Swiss National Bank (SNB) to move its policy rate into negative territory and actively manage its exchange rate to avoid additional deflationary pressures from a strengthening Swiss franc. The SNB's easing policies have contributed to growth in bank lending that pushed up levels of household debt. However, today's GDP print points to positive economic growth that will likely push inflation slowly higher over time and allow the SNB to gradually reverse its accommodative stance. Higher future interest rates could weigh on leveraged Swiss households by increasing debt-servicing costs, but, in the near term, inflation still has room for significant improvement before the SNB will likely move to raise rates.

Broad-Based GDP Growth Registered in the Third Quarter

Data released today showed that real GDP in Switzerland grew 0.6 percent (2.5 percent annualized) on a sequential basis in Q3-2017 (Figure 1). Today's print affirms broad-based strength in domestic demand across multiple sectors of the Swiss economy. Investment spending was solid for equipment and software products, up 2.9 percent on a year-ago basis. A drawdown in inventories in the third quarter supports strength in the private sector and is promising for future expansion, as firms will likely need to rebuild inventory stock in the coming quarters. Swiss consumers also saw solid economic growth in the third quarter. Household consumption was up 0.4 percent on a sequential basis (1.2 percent year over year), likely boosted by solid employment growth as the unemployment rate has edged lower in recent months (Figure 2).

Switzerland also enjoyed a pickup in external demand in Q3 that was additive to topline GDP growth. Swiss exports were particularly strong, with exports of goods up 2.1 percent for the quarter after the slower 0.7 percent rate of growth registered in Q2. Stronger export growth is consistent with the pickup in global demand seen more broadly and reaffirms the broad-based economic growth in the quarter, especially as the private sector continues to expand to meet global demand. Imports saw a retrenchment in Q3, with both imports of goods and services declining over the quarter. However, after particularly strong growth in imports in Q2 and solid consumer and business demand in Q3, we should see imports bounce back in the future. While we do not forecast Swiss GDP explicitly, the consensus expects solid economic growth to continue in the coming quarters, with GDP growth forecasted to be between 1.5 percent and 2.0 percent in 2018, likely supported by solid domestic and external demand.

Mild Deflation = Extraordinary Monetary Accommodation

The Swiss economy has been more or less expanding for eight consecutive years, but inflation in Switzerland remains essentially non-existent. The economy experienced mild deflation in 2012- 2013 and again in 2015-2016, which has brought the consumer price index at present nearly 3 percent below the level that prevailed in mid-2011. Inflation has returned to positive territory in recent months, but the overall and core rates both remain well below 1 percent (Figure 3). As CPI inflation weakened and then turned negative, the SNB cut its target rate for 3-month Swiss LIBOR, its main policy rate, to zero percent and then eventually to -0.75 percent, where it remains today (Figure 4).

In addition, the SNB turned to exchange rate policy to try and combat the deflationary forces that were buffeting the economy. Imports of goods and services are equivalent to about 50 percent of nominal GDP, and the sharp appreciation of Swiss franc between early 2008 and mid-2011 - it strengthened more than 40 percent on a trade-weighted basis - contributed to the deflationary pressures in Switzerland. Consequently, the SNB announced in September 2011 that it would no longer tolerate an exchange rate stronger than 0.83 euros per Swiss franc (Figure 5). To prevent the exchange rate from strengthening beyond this line in the sand, the SNB had to buy euros and sell Swiss francs in the foreign exchange (FX) market.1 The SNB's buying of euros and selling of its own currency led to a sharp increase in its FX reserves and a corresponding rise in the growth rate of the Swiss money supply (Figure 6).

The Challenges for the SNB Going Forward

These easing steps by the SNB likely prevented deflation from becoming even worse. However, the policy steps may have had some side effects that could potentially prove to be a bit problematic. Specifically, low interest rates and ample bank liquidity fueled solid growth in bank lending, especially in mortgages. The ready availability of mortgage financing helped to push up home prices, which have risen about 25 percent on a nationwide basis since 2010. House prices in some of the country's more densely populated cities such as Zurich and Geneva rose even more, although they are now starting to edge lower.

Despite the deceleration in mortgage lending over the past few years, the debt-to-GDP ratio of the Swiss household sector has continued to trend higher and is closing in on 130 percent (Figure 7), which gives Switzerland one of the highest ratios among advanced economies. Although mortgage lending in Switzerland has grown only 3 percent or so per annum over the past few years, nominal income growth in the economy has been anemic during that period due to the deflationary forces that have taken hold. Fortunately, the low level of interest rates in Switzerland has kept the debt service ratio (DSR) of the private sector contained (Figure 8).

As Figure 8 makes clear, the DSR rose markedly between 2006 and 2009 when the SNB was hiking rates. With the household debt-to-GDP ratio about 25 percentage points higher than it was when the SNB commenced its last tightening cycle, the DSR has potential to move up significantly. That said, the SNB is not likely to hike rates anytime soon. However, if the economy strengthens further in the coming year, as is widely expected, the CPI inflation rate likely will trend higher, if only slowly. Sooner or later the SNB will begin to tighten monetary policy, which could eventually lead to a noticeable rise in debt-servicing costs for households as mortgage rates reset. Higher debt-servicing costs for households could then weigh on growth in consumer spending.

Conclusion

Solid economic growth in Switzerland in Q3 has likely put the economy on track to tackle the challenges of lackluster inflation and an upward trend in household debt seen over the past few years. While the SNB will likely need to see significant improvement in inflation before beginning to hike rates, in our view CPI inflation will likely trend slowly higher. Today's positive GDP print and solid domestic demand will likely support a gradual acceleration in prices, allowing the SNB to reverse its accommodative stance at a gradual pace. Slowly increasing inflation could exert upward pressure on wage growth, potentially counteracting higher debt-service costs as the SNB eventually begins to raise rates. In the near term, the consensus expects the broad-based strength in the Swiss economy to continue in the coming quarters.