Sample Category Title

EUR/USD Continued Short-Term Consolidation Before Another Leg Higher

EUR/USD is consolidating lower. Hourly resistance is now given at 1.1961 (27/11/2017 high). Hourly support is given at a distance at 1.1554 (07/11/2017 low). Expected to show renewed increase.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

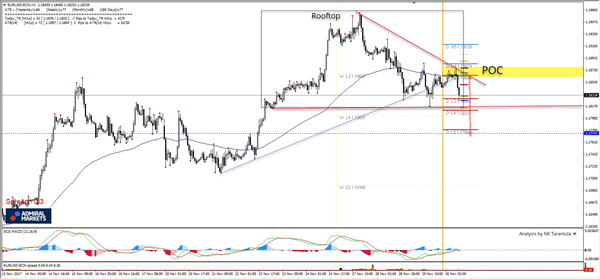

EUR/USD Continuation Of The Rooftop Pattern Below 1.1800

The EUR/USD has formed a huge bearish rooftop pattern with a clear support within.1810-00 zone. 1.1865-85 is the POC zone where now moment sellers might be waiting for. Month-end demand can usually be volatile and EUR/USD seem to be offered withing the POC zone. Break below 1.1800 and the pair could target 1.1775 and 1.1750. For counter trend trades watch for reversal patterns and/or regular bullish divergence only IF 1.1800 zone holds.

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

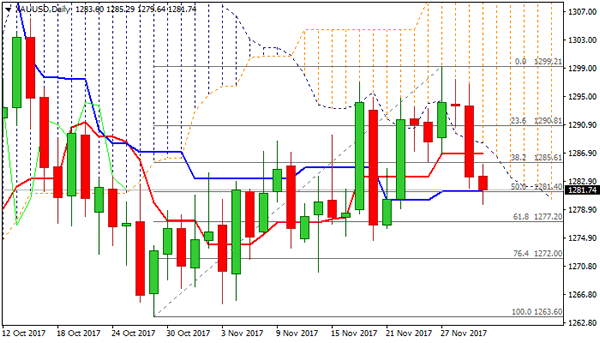

Technical Outlook: SPOT GOLD Extends Weakness Under Widening Daily Cloud

Spot Gold remains in red on Thursday and hit one-week low at $1279, extending strong fall on Wednesday after data showed the US economy has regained traction. US Gross Domestic Product rose by 3.3% in Q3, showing economy expanding in the fastest pace in three years.

Another hit for gold price came from Fed chair Janet Yellen’s Congressional testimony, as Yellen pointed at expanding economy which would warrant continued interest rate increases.

The yellow metal is waiting for another set of releases from the US, which includes personal income and spending and personal consumption expenditures, to get more clues about likely trajectory of US monetary policy.

Technical studies are turning to bearish mode on daily chart after the price repeatedly failed to sustain break into daily cloud that kept widening cloud as solid resistance and continuing to weigh on gold’s price.

Today’s dip cracked support at $1281 (daily Kijun-sen) but firm break lower is needed to open pivot at $1277 (Fibo 61.8% of $1263/$1299).

Falling cloud base ($1288) is expected to cap upticks.

Res: 1286, 1288, 1290, 1296

Sup: 1281, 1279, 1277, 1274

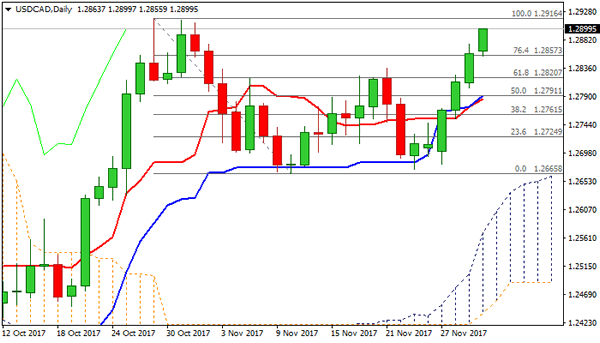

Technical Outlook: USDCAD – Key Barriers At 1.2916/25 Under Increased Pressure

The pair extends steep ascend from 1.2670 base and pressures key barrier at 1.2916 (27 Oct recovery peak, the highest since mid-July).

Strong recovery extended after double-bottom was formed (1.2665/70) and showing scope for eventual break above 1.2916 peak and nearby Fibo barrier at 1.2625 (50% retracement of larger 1.3789/1.2061 descend).

Bullish techs are supporting positive sentiment, with OPEC meeting also being focused for fresh signals.

Strongly overbought slow stochastic on daily chart warns of consolidative / corrective action preceding break higher.

Rising thick hourly cloud (spanned between 1.2831 and 1.2773) is expected to contain extended dips.

Res: 1.2916, 1.2925, 1.3000, 1.3071

Sup: 1.2856, 1.2831, 1.2791, 1.2773

Market Update – European Session: Euro Zone Flash CPI Misses Expectations While Regional Unemployment Remains At Multi-Year Lows

Notes/Observations

Euro Zone flash CPI misses expectations and still well below the ECB target

Unemployment remains improving trend for Europe (Italy at 5-year lows, Euro Zone at 8-year lows)

OPEC bi-annual meeting seen keeping current level of production cuts intact for another 9 months

Odds of seeing a US tax cut seem above 60%

Asia:

Bank of Korea (BOK) raised the 7-Day Repo Rate by 25bps to 1.50% for its 1st rate hike since 2011

China Nov Official Govt Manufacturing PMI: 51.8 v 51.5e v 51.6 prior, Non-manufacturing PMI: 54.8t v 54.3 prior

Japan Oct Preliminary Industrial Production M/M: 0.5% v 1.8%e; Y/Y: 5.9% v 7.1%e

BoJ's Harada: Wages and prices to rise as BOJ continued with its easing policy; Labor shortages had been insufficient. Current policy sufficient for 2% price target; more easing might be needed if external shocks occur. Would start to reduce easing if price momentum strengthened

Europe:

ECB's Knot (Netherlands): inflation outlook posed no threat to price stability. Despite undershooting its inflation aim in the near term, the ECB was fulfilling its mandate. Full phasing out of net asset purchases from Sept 2018 onwards is warranted

ECB’s Weidmann (Germany): remained skeptical about need for ECB QE. Strong data signaled the ECB growth outlook could be raised

Britain reportedly nearing deal on Northern Ireland border; officials on both sides reportedly predict agreement within weeks. UK officials this week tabled proposals to avoid a hard border in Ireland that could remove the last major obstacle to a deal

Italy said to back Portugal Fin Min Centeno as the next Eurogroup chairman

SNB Vice President Zurbruegg: reiterates the Swiss Franc remains highly valued. Safe haven aspect of Swiss Franc was still out there, but situation remained fragile

Americas:

Tax reform bill passes in procedural hurdle in US Senate (as expected) in a 52-48 vote. Allowed for debate to begin on the Senate floor with a final vote likely by Friday

President Trump sent nomination of Marvin Goodfriend for Fed to Senate

Fed Williams (moderate, non-voter): failing to raise rates to more normal levels could risk recession; should continue to raise rates slowly over coming year. Would like to get rates to new normal level around 2.5% over next two years

Fed's Kashkari (dove, voter): if inflation keeps falling, there's no reason to tap the brakes. If we needed more stimulative policy we could cut rates back to zero, use forward guidance and balance sheet policy. Negative rates would likely come after those if ever

Fed’s Beige Book: Price pressures have strengthened since last report. Economy ws growing at modest to moderate pace. Wage growth modest or moderate despite tight labor market

Energy:

Iraq Oil Min: reiterates would prefer 9-month oil agreement extension

Iran To go along with 6 or 9 month extension; expects OPEC meeting to go very well

Economic Data:

(CH) Swiss Q3 GDP Q/Q: 0.6% v 0.6%e; Y/Y: 1.2% v 0.8%e

(DE) Germany Oct Retail Sales M/M: -1.2% v +0.3%e; Y/Y: -1.4% v +2.8%e

(UK) Nov Nationwide House Prices M/M: 01% v 0.1%e; Y/Y: 2.5% v 2.7%e

(DK) Denmark Q3 Preliminary GDP Q/Q: -0.6% v -0.2%e; Y/Y: 1.3% v 1.7%e

(NO) Norway Oct Credit Indicator Growth Y/Y: 5.7% v 5.6%e

(NO) Norway Oct Retail Sales W/Auto Fuel M/M: -0.2% v +0.7%e

(TR) Turkey Oct Trade Balance: -$7.3B v -$7.4Be

(FR) France Nov Preliminary CPI M/M: 0.1% v 0.1%e; Y/Y: 1.2% v 1.2%e

(FR) France Nov CPI EU Harmonized M/M: 0.1% v 0.1%e; Y/Y: 1.3% v 1.2%e

(ES) Spain Q3 Final GDP Q/Q: 0.8% v 0.8%e; Y/Y: 3.1% v 3.1%e

(CH) Swiss Nov KOF Leading Indicator: 110.3 v 109.7e

(AT) Austria Q3 Final GDP Q/Q: 0.8% v 0.6% prelim; Y/Y: 3.2% v 2.6% prelim

(DE) Germany Nov Unemployment Change: -18K v -10Ke; Unemployment Rate: 5/6% v 5.6%e

(IT) Italy Oct Unemployment Rate: 11.1% v 11.1%e (matches low from 2012)

04:00 (PL) Poland Q3 Final GDP Q/Q: 1.2% v 1.1% prelim; Y/Y: 4.9% v 4.7% prelim

(NO) Norway Dec Central Bank Norges Bank Daily FX Purchases (NOK): -900M v -650Me

(EU) Euro Zone Nov Advance CPI Estimate Y/Y: 1.5% v 1.6%e; CPI Core Y/Y: 0.9% v 1.0%e

(EU) Euro Zone Oct Unemployment Rate: 8.8% v 8.9%e. (lowest since 2012)

(IT) Italy Nov Preliminary CPI (NIC incl. tobacco) M/M: % v 0.0%e; Y/Y: % v 1.1%e

(IT) Italy Nov Preliminary CPI EU Harmonized M/M: % v 0.0%e; Y/Y: % v 1.2%e

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2024, 2027, 2034 and 2046 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.3% at 389, FTSE -0.3% at 7373, DAX +0.6% at 13134, CAC-40 +0.4% at 5417, IBEX-35 +0.5% at 10314, FTSE MIB +0.8% at 22508, SMI +0.2% at 9324, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes:

European Indices trade higher with the FTSE once again the under performer trading lower on the back of a stronger Sterling as the GBPUSD pair approaches $1.35.

On the corporate front Credit Suisse provided initial 2019 and 2020 guidance, with shares reacting positively, while Daily Mail General Trust trades over 20% lower after a fall in profits and guiding 2018 margins lower y/y.

Equitie

Consumer discretionary [Daily Mail General [DMGT.UK] -24% (Earnings), GreeneKing [GNK.UK] -3% (Earnings), Marston [MARS.UK] +10.7% (Earnings), Go-Ahead [GOG.UK] - 1.3% (Trading update)]

Financials: [Credit Suisse [CSGN.CH] +2.5% (Outlook), Aviva [AV.UK] +2.4% (Outlook)]

Technology: [Altran [ALT.FR] -4.5% (Acquisition), Rocket Internet [RKET.DE] -3.6% (Earnings)]

Energy: [Norsk Hydro [NHY.NO] -3.5% (Capital market day)]

Speakers

Various oil ministers’ comment as OPEC holds semi-annual meeting in Vienna:

Saudi Arabia Energy Min Al Falih: In perfect alignment with all OPEC countries; preference was for 9 month as not reached comfortable levels on oil inventories. Non-Opec members must do more because overhang remained. Too early to talk of exit strategy; exit to be gradual. Believed that global oil demand would absorb shale

Kuwait Oil Min Almarzooq: Agreement on production caps for both Libya and Nigeria totaling 2.8M bpd. Kuwait was currently exporting around 2M bpd

Iran Oil Min Zanganeh: Longer duration extension would aid market stability. No discussion to raise production cuts beyond the 1.8M bod

UAE Oil Min Mazrouei: Markets were in a better position compared to a year ago. Opec job was not yet done; looking for wider group of countries to join production cuts

Nigeria Oil Min Kachikwu: Expected to reach 1.8M B/D crude output by year-end

Other Speakers in session:

ECB’s Praet (Belgium, chief economist): Width of economic upturn is notable but too early to signal the all-clear signal

Norway Stats Agency (SSB) Quarterly forecasts raised its 2018 Mainland GDP from 2.1% to 2.5% and 2018 Underlying CPI from 1.7% to 1.8%. It saw the Repo Rate at current level well into 2019

Russia PM Medvedev: Economy has entered a growth phase

Turkey Central Bank Financial Stability Report: Banking sector preserves sound asset quality

Turkey President Chief Adviser Ertem: Targeting inflation, not the FX rate. Central bank could act on rates; had instrument independenceto do so. Expected a rapid drop in inflation in Q1. Import price increase to slow down due to FX impact

South Africa Dep President Ramaphosa: Reject possibility of IMF helping the country. South Africa needed an economic plan

India Fin Min Jaitley: 10% GDP growth is a challenging figure; would require a global economic boom

Thailand Central Bank: Have intervened to slow the THB currency (Baht) rise. Reiterated view that THB currency is moving in line with regional peers

Japan LDP Tax Panel Member Miyazawa: have not decided to raise tobacco taxes at the moment; would make sense to make new category for heat/burn tobacco

Currencies

USD unable to must much upside momentum even as US tax bill advances but did muster some strength just ahead of the NY morning.

GBP currency (Sterling) continued to build upon gains as optimism on the Brexit negotiations continued. After the UK govt said to agree on a financial settlement bill reports circulated that a deal on the Irish border could result in EU leaders offering a two-year transition agreement. GBP/USD at 2-month highs after testing the 1.,3480 level. Dealers see the 1.36 area as the key resistance.

EUR/USD was softer after Nov advance CPI came in below expectations. The 1.5% annual pace was a slight improvement from the Oct level but still distance from the ECB target.

EUR/NOK rises to test 9.9017 for its highest level since Dec 2008. the retail sales data brought some uncertainty over the country's economic recovery. The NOK moved off its worst level after the central bank (Norges) increased its planned daily purchases of FX in Dec

Fixed Income

Bund futures trade 162.74 up 12 ticks, following softer inflation data out of the Euro Zone. Continued downward pressure sees 162.10 followed by 161.50. A reversal targets 163.40 then 163.75.

Gilt futures trade at 124.21 down 17 ticks, following yesterday’s 10-year gilts biggest daily fall since June on Brexit progress. Continued upside eyeing 125.15 then 125.65. Downside targets include 124.01 then 123.75.

Thursday’s liquidity report showed Wednesday's excess liquidity fell to €1.858T from €1.863T. Use of the marginal lending facility fell to €286M from €291M prior.

Looking Ahead

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

06:00 (BR) Brazil Oct National Unemployment Rate: 12.2%e v 12.4% prior

06:00 (PT) Portugal Q3 Final GDP Q/Q: 0.5%e v 0.5% prelim; Y/Y: No est v 2.5% prelim

06:00 (PT) Portugal Oct Industrial Production M/M: No est v -6.7% prior; Y/Y: No est v 2.8% prior

06:00 (PT) Portugal Oct Retail Sales M/M: No est v 0.8% prior; Y/Y: No est v 4.1% prior

06:00 (IT) Italy Oct PPI M/M: No est v 0.3% prior; Y/Y: No est v 2.0% prior

06:00 (ZA) South Africa Oct Electricity Production Y/Y: No est v 1.1% prior; Electricity Consumption Y/Y: No est v 0.2% prior

06:00 OPEC holds closed door session)

06:30 (IN) India Oct Eight (Key) Industries: No est v 5.2% prior

06:40 (EU) ECB's Hakkarainen (SSM member) in London

07:00 (IN) India Q3 GDP Y/Y: 6.5%e v 5.7% prior, GVA Y/Y: 6.3%e v 5.6% prior

07:00 (ZA) South Africa Oct Budget Balance (ZAR): No est v -3.5B prior

07:00 (ZA) South Africa Oct Trade Balance (ZAR): -5.5Be v +4.0B prior

07:00 (CL) Chile Oct Unemployment Rate: 6.6%e v 6.7% prior

08:00 (PL) Poland Nov Preliminary CPI M/M: 0.4%e v 0.5% prior; Y/Y: 2.3%e v 2.1% prior

08:00 (RU) Russia Gold and Forex Reserve w/e Nov 24th: No est v $427.6B prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Oct Personal Income: 0.3%e v 0.4% prior; Personal Spending: 0.3%e v 1.0% prior, Real Personal Spending (PCE): 0.2%e v 0.6% prior

08:30 (US) Oct PCE Core M/M: 0.2%e v 0.1% prior; Y/Y: 1.4%e v 1.3% prior

08:30 (US) Oct PCE Deflator M/M: 0.1%e v 0.4% prior; Y/Y: 1.5%e v 1.6% prior

08:30 (US) Initial Jobless Claims: 240Ke v 239K prior; Continuing Claims: 1.89Me v 1.904M prior

08:30 (CA) Canada Q3 Current Account: -$20.0Be v -$16.3B prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (BE) Belgium Q3 Final GDP Q/Q: No est v 0.3% prior; Y/Y: No est v 1.7% prior

09:00 OPEC and Non-Opec members ministerial meeting

09:00 (BR) Brazil to sell 2023 LFT

09:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills LTN

09:45 (US) Nov Chicago Purchasing Manager: 63.0e v 66.2 prior

10:00 (CO) Colombia Oct National Unemployment Rate: No est v 9.2% prior, Urban Unemployment Rate: 9.8%e v 10.5% prior

10:00 (MX) Mexico Oct Net Outstanding Loans (MXN): No est v 3.895T prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (NZ) New Zealand Nov QV House Prices Y/Y: No est v 3.9% prior

12:00 (IR) Iran Foreign Min Zarif in Rome

12:30 (US) Fed's Quarles (FOMC voter) in Cleveland

13:00 (US) Fed's Kaplan (moderate, voter) in Dallas

13:10 (UK) BOE FPC member Sharp

14:00 (DE) German Chancellor Merkel and SPD leader Schultz meet with President Steinmeier

14:00 (AR) Argentina Oct Industrial Production Y/Y: 5.0%e v 2.3% prior

15:00 (US) Oct Agriculture Prices Received: No est v 6.3% prior

15:30 (MX) Mexico Oct YTD Budget Balance (MXN): No est v 63.2B prior

16:45 (NZ) New Zealand Q3 Terms of Trade Index Q/Q: 1.3%e v 1.5% prior

17:00 (AU) Australia Nov Manufacturing PMI: No est v 55.5 prior

17:30 (AU) Australia Nov AiG Performance of Manufacturing Index: No est v 51.1 prior

18:00 (AU) Australia Nov CoreLogic House Prices M/M: No est v 0.0% prior

18:00 (KR) South Korea Nov CPI M/M: 0.0%e v -0.2% prior; Y/Y: 1.8%e v 1.8% prior; CPI Core Y/Y: 1.7%e v 1.3% prior

18:00 (KR) South Korea Q3 Final GDP SA Q/Q: 1.4%e v 1.4% prelim; Y/Y: 3.6%e v 3.6% prelim

18:30 (JP) Japan Oct Jobless Rate: 2.8%e v 2.8% prior; Job-To-Applicant Ratio: 1.52e v 1.52 prior

18:30 (JP) Japan Oct Overall Household Spending Y/Y: -0.3%e v -0.3% prior

18:30 (JP) Japan Oct National CPI Y/Y: 0.2%e v 0.7% prior; Ex Fresh Food (Core) Y/Y: 0.8%e v 0.7% prior, CPI Ex Fresh Food and Energy (core core): 0.2%e v 0.2% prior

18:30 (JP) Tokyo Nov CPI Y/Y: -0.1%e v -0.2% prior; Ex-Fresh Food Y/Y: 0.6%e v 0.6% prior, CPI Ex Fresh Food and Energy Y/Y: 0.2%e v 0.1% prior

18:50 (JP) Japan Q3 Capital Spending Y/Y: 3.2%e v 1.5% prior; Capital Spending (Ex-Software) Y/Y: 3.0%e v 0.6% prior

19:00 (KR) South Korea Nov Trade Balance: $8.5Be v $7.3B prior; Exports Y/Y: 10.3%e v 7.1% prior; Imports Y/Y: 13.3%e v 7.4%e

19:30 (JP) Japan Nov Final Manufacturing PMI: No est v 53.8 prelim

19:30 (MY) Malaysia Nov Manufacturing PMI: No est v 48.6 prior

19:30 (PH) Philippines Nov Manufacturing PMI: No est v 53.7 prior

19:30 (KR) South Korea Nov Manufacturing PMI: No est v 50.2 prior

19:30 (TW) Taiwan Nov Manufacturing PMI: No est v 53.6 prior

19:30 (TH) Thailand Nov Manufacturing PMI: No est v 49.8 prior

19:30 (VN) Vietnam Nov Manufacturing PMI: 50.9e v 51.6 prior

20:45 (CN) China Nov Caixin Manufacturing PMI: No est v 51.0 prior

22:30 (TH) Thailand Nov CPI M/M: No est v 0.2% prior; Y/Y: 1.0%e v 0.9% prior; Core Y/Y: 0.6%e v 0.6% prior

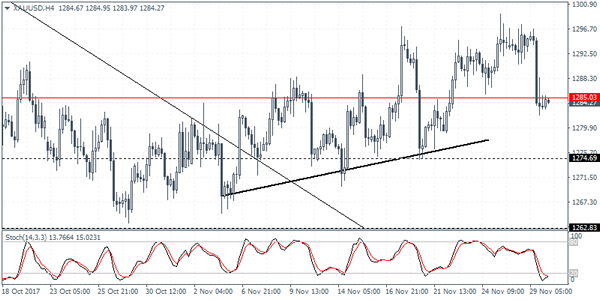

XAUUSD Intraday Analysis

XAUUSD (1284.27): Gold prices gave up the gains as price action fell sharply back to retest the previously breached resistance level. Gold prices are currently trading slightly below the 1285 handle. Failure to trim the losses could see gold prices extending the weakness down to 1275 region where the support level has been firmly established. However, the Stochastics oscillator is currently oversold and could signal a hidden bullish divergence with the higher low in price and lower low on the Stochastics.

USDJPY Intraday Analysis

USDJPY (111.99): The USDJPY closed on a bullish note yesterday following the inside bar pattern that was formed on Tuesday. The upside momentum could continue but price action is seen testing the resistance level at 112.00. In the near term, USDJPY could be seen giving up the short-term gains. Support is found at 111.61 - 111.57 region. USDJPY will need to form a higher low around this level and breakout above the resistance area of 112.00 to target the next main resistance level of 113.00. For the downside, in the event that the USDJPY slips below 111.61 - 111.57 we expect a deeper test back to the previous support level near 111.00.

EURUSD Intraday Analysis

EURUSD (1.1863): The euro stalled its two day decline yesterday, as price action closed with a spinning bottom candlestick pattern. Current attempts to minimise losses could see a short term rebound in price action to the upside. The reversal comes as EURUSD was seen testing the support area near 1.1843 - 1.1822. This could mean a short-term retracement towards 1.1920 where a short-term support was formed. Establishing resistance here could signal further declines. While the support area of 1.1842 - 1.1822 remains, the initial downside target a break down below this level will send EURUSD lower to testing the support area around 1.1710 - 1.1688. The bearish bias will shift if price manages to close above 1.1920.

Upbeat Data Fails To Push U.S. Dollar Higher

The U.S. dollar was broadly muted on Wednesday despite strong economic releases. Starting with the second revised estimates for the GDP, data from the commerce department showed that the U.S. economy advanced 3.3% in the quarter ending in September. This was above the forecast of a 3.2% increase.

Separately, pending home sales data showed a 3.5% increase on the month, beating estimates of a 1.1% increase for October. However, September's data was adjusted down to show a decline of 0.4%. The Fed Chair Janet Yellen testified in her prepared remarks that the central bank will be hiking interest rates this December.

Across the pond, the British pound surged following the news reports that the EU and the UK were likely to reach a settlement that was akin to progressing Brexit talks. No firm commitment has been made just yet but the British PM, Teresa May, is expected to visit Brussels on Monday to engage with her EU counterparts.

Looking ahead, economic data today will see the flash inflation estimates from the Eurozone. Both headline and core CPI rates are expected to rise higher following their weakening in the previous month. The U.S. core PCE data is also expected to be released later in the day.

EUR/SEK 1H Chart: Pair Moves Away From 2017 High

The common European currency has appreciated substantially against the Swedish Krona within the past three months. During this time, an ascending channel was guiding the pair up until a 2017 high of 9.9929 was reached on November 21. The Euro has likewise formed a two-week junior channel. Its bottom boundary has had three confirmations, while the upside its currently being tested for the second time. As apparent on the chart, the pair has been reluctant to move past the 9.9260 area for the last week. The same situation occurred in this session, as well, as the Euro has significantly diminished its trading range. This suggests that the rate could go for the senior channel circa 9.89 today. However, the combined support of the 55-, 100– and 200-hour SMAs is likely to hinder further decline. Meanwhile, technical indicators suggest that the pair could respect the junior channel and thus breach the senior one in a week.