Sample Category Title

USDJPY Firms Up This Week, Remains Trapped In Medium-Term Range

USDJPY maintains its medium-term trading range between 108 and 114.50 as a result of entering a consolidation phase after a rally to 118.66 in December 2016. The pair is now trading above the mid-point of the range.

USDJPY has been closing above the key 111 in the past two months, making it a strong support level. Breaking below it would shift the focus back to the lower end of the range in the 108 area.

USDJPY firmed up this week after bouncing off the 111 level. The short-term bias improved when prices rose above the 200-day moving average. This level at 111.65 is now expected to provide support.

RSI is ticking higher, suggesting the market has more upside potential in the near term. There is resistance at 112.75 (50-day MA) but pushing above it would help USDJPY see further gains back towards the top of the range at 114.50. This level would be a challenge to break, however, if successful, there is scope to target the 118 level for a re-test of the December 2016 peak.

Forex: US Economy Expanding Faster Than Predicted

Data released on Wednesday showed that the US economy expanded at its quickest pace since 2014 in Q3. The US Commerce Department said that GDP grew at an annualized rate of 3.3% in the July to September period — the highest reading since Q3 2014. The release beat market forecasts of 3.2% growth and was faster than the initial estimate of a 3% expansion. In a tweet, President Trump said GDP would have climbed to 3.9% if not for the storms, citing internal research by his Council of Economic Advisers. The improvement in GDP was led by stronger business investment. Spending on equipment, especially in transportation-related areas, rose 10.4%, beating forecasts of 8.6%. A disappointing data release came with the increase in consumer spending that came in unchanged at 2.3%.

GBP gained against its peers on news that London and Brussels have agreed that the UK will pay between €45 and €55bn ($53-63bn) to leave the European Union, according to media reports. The Financial Times has reported that Britain would cover EU liabilities worth as much as €100bn. EU chief negotiator Michel Barnier refused to confirm the reports, calling them “rumors” commenting in Berlin that “There is a subject on which we are continuing to work – despite the claims or rumors, that's the issue of financial engagements”. An agreement would be significant as the UK prepares for a December EU summit where it hopes to start the next phase of talks on future trade ties with the EU. Whilst this is a major “step-forward” it still leaves 2 critical issues that need to be agreed upon: expatriate citizens' rights after Brexit and the Irish border.

EURUSD is 0.15% higher in early Thursday trading at around 1.1865.

USDJPY is little changed overnight trading at around 112.00.

GBPUSD is 0.45% higher in early session trading at around 1.3464, after reaching an 8+ week high of 1.3479 earlier on Thursday.

Gold is unchanged overnight, currently trading around $1,284.25.

WTI is unchanged in early trading at around $57.45.

Major data releases for today:

All Day: OPEC meeting in Vienna, Austria.

At 09:00 GMT: German Statistics will publish the German Unemployment Rate s.a. and Unemployment Change for November from the Bundesagentur für Arbeit. Seasonally adjusted German Unemployment is expected to be unchanged at 5.6%, with the Change in November expected to be -10K (prev. -11K). If the actual number is significantly different from expectations we are likely to see EUR volatility.

At 10:00 GMT: Eurostat will release Eurozone Consumer Price Index & CPI Core (YoY) for November. CPI is expected to have increased to 1.6% from the previous release of 1.4% and Core is forecast to come in at 1.1% from the previous release of 0.9%. Any significant deviation from the forecast will likely cause EUR volatility.

At 13:30 GMT: the US Bureau of Economic Analysis will release Core Personal Consumption Expenditure – Price Index (MoM & YoY) for October. Month-on-Month is forecast to come in at 0.2%, a slight increase from the previous 0.1%. Year-on-Year PCE is also forecast to come in slightly higher at 1.4% (prev. 1.3%). A release significantly different from forecast will see USD volatility.

At 13:30 GMT: the US Department of Labor will release Initial Jobless Claims for the week ended November 24th and Continuing Jobless Claims for the week ended November 17th. The markets expect to see data that reinforces a strong and resilient labour market in the US, which has been fueling economic growth.

At 18:00 GMT: FOMC board Member and SEO of the Federal Reserve Bank of Dallas is scheduled to speak.

Aussie Dollar Struggles To Recover Vs US Dollar

Key Highlights

The Aussie Dollar remains in a downtrend below the 0.7650 pivot against the US Dollar.

There is a major bearish trend line forming with resistance at 0.7600 on the 4-hours chart of AUD/USD.

The US GDP in Q3 2017 increased 3.3% (Preliminary), more than the forecast of 3.2%.

The US Initial Jobless Claims figure for the week ending Nov 25, 2017 will be released today, which is forecasted to increase from 239K to 240K.

AUDUSD Technical Analysis

The Aussie Dollar recovered recently from 0.7535 against the US Dollar. However, the AUD/USD pair failed near 0.7650 and started a new downside wave.

The pair failed to break a major bearish trend line with current resistance at 0.7600 on the 4-hours chart. Moreover, the 100 simple moving average (4-hour, red) is around 0.7615 to act as a key hurdle on the upside.

The pair is now below the 50% Fib retracement level of the last wave from the 0.7532 low to 0.7644 high. Therefore, there are chances of it extending the current decline back toward the 0.7530-40 levels in the near term.

US GDP

Recently in the US, the Gross Domestic Product Annualized reading for Q3 2017 was released by the US Bureau of Economic Analysis. The market was looking for a rise of 3.2% (Preliminary) in Q3 2017 compared with the last reading of 3%.

However, the actual result was better since the GDP rose 3.3% as per the second estimate.

The report added that:

The price index for gross domestic purchases increased 1.8 percent in the third quarter, compared with an increase of 0.9 percent in the second quarter. The PCE price index increased 1.5 percent, compared with an increase of 0.3 percent.

Overall, the result was positive and it might weigh further on the AUD/USD pair in the near term.

Economic Releases to Watch Today

Swiss Gross Domestic Product for Q3 2017 (QoQ) – Forecast +0.9%, versus +0.3% previous.

Germany's Unemployment Change for Nov 2017 – Forecast -10K, versus -11K previous.

Germany's Unemployment Rate for Nov 2017 – Forecast 5.6%, versus 5.6% previous.

German Retail Sales for Oct 2017 (MoM) – Forecast 0.3%, versus 0.5% previous.

German Retail Sales for Oct 2017 (YoY) – Forecast 2.8%, versus 4.1% previous.

Euro Zone CPI for Nov 2017 (YoY, Preliminary) – Forecast +1.6%, versus +1.4% previous.

US Initial Jobless Claims – Forecast 240K, versus 239K previous.

Trade Idea : USD/CHF – Sell at 0.9885

USD/CHF - 0.9850

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9843

Kijun-Sen level : 0.9845

Ichimoku cloud top : 0.9837

Ichimoku cloud bottom : 0.9816

Original strategy :

Sell at 0.9885, Target: 0.9785, Stop: 0.9920

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9885, Target: 0.9785, Stop: 0.9920

Position : -

Target : -

Stop : -

Dollar has traded narrowly today and near term upside risk remains for the rebound from 0.9778 (this week’s low) to bring retracement of recent decline, hence marginal gain from here cannot be ruled out, however, reckon upside would be limited to 0.9876 (previous support) and bring another decline later, below 0.9815-20 would bring a retest of said support at 0.9778, break there would extend recent decline from 1.1038 top towards 0.9730-37 support area but reckon support at 0.9705 would hold from here, bring rebound later.

In view of this, we are looking to sell dollar again on further subsequent recovery as previous support at 0.9876 should turn into resistance and limit upside. Only break of 0.9895-00 would defer and signal a temporary low is formed instead, bring a stronger rebound to 0.9920 but price should falter well below resistance at 0.9947.

Tax Bill Passes The Senate, Investors Rotate From Tech To Financials

U.S. stock indices ended mixed on Wednesday. While the Dow-Jones industrial average closed at a record high after U.S. GDP showed the economy grew at a revised rate of 3.3%, Tech stocks dragged the Nasdaq down, closing 1.3% lower. There has been a significant rotation from the Tech sector to financials on bets that the giant multinationals willbenefit the least from U.S. tax legislation, whereas the rise in long-dated U.S. bond yields were seen asa positive sign for banks’ profit margins.

As we approach the end of 2017, investors are likely to reassess their portfolios. Few may disagree that stocks are very expensive, but expectations of tax reforms, synchronized economic growth, accommodative monetary policies and robust earnings, were all factors that helped shares surge this year. Given that the tax bill passed the Senate Budget Committee on Wednesday, it looks like we are getting closer to a deal, but this does not necessarily mean that bulls will get overly excited. I think much of the premium for tax reforms has already been priced in, and I won’t be surprised to see the scenario of “buy the rumors and sell the news” when we get the deal done. Monetary policies can only get tighter at the current stage which is another negative factor for risk assets. This leaves us with few factors that may justify further upside in stocks in 2018, so investors might start considering protecting their portfolios from any potential pullback.

Bitcoin: Bull, Bear then Bull!

Bitcoin continued to be the news making headline this week. The cryptocurrency moved from a bull to a bear market (a drop of 20%) then back to a bull market in less than 24 hours. I cannot remember in my career seeing an asset with such volatility. Bitcoin traders blamed the outages and poor execution at exchanges for the pullback, but as the price approached $9,000 new inflows came in, and the price surged again. This scenario has been repeated throughout the year where every sharp pull back attracts new inflows. It’s impossible to predict a price target for the bitcoin at this stage but I can say it’s going to be the most volatile asset class in history. If you are a faint-hearted investor, stay away.

Pound hits two months high

Sterling is the best performing currency early Thursday. GBPUSD hit a new two-month high of 1.3479 on hopes that the U.K. is close to reaching an agreement over the divorce bill. The fall in consumer confidence was totally ignored, and the current move is based on media reports rather than official ones. Although Sterling continues to look cheap from a fundamental perspective, Sterling bulls may be disappointed if no agreement is reached in the EU Summit in mid-December. However, if positive news continues to flow, I think the pound may be headed towards 1.36 – 1.38 in the next couple of days.

US Government Bond Yield Curve Steepening Around 3bp

Market movers today

After some quiet days (at least in terms of economic data releases) , we have a more act ion packed day ahead of us. We estimate euro area HICP core inflation rose to 1.1% y/y in November from 0.9% in October, as we estimate a rebound in volatile components such as package tours and services related to transport. Here and now, it should not matter much for the ECB after its decision to extend QE to September 2018.

In the US, we est imate PCE core index rose 0.2% m/m in October, as indicated by the CPI figures released already. This would push the PCE core inflation rate up to 1.4% y/y from 1.3%, still well below t he Fed's 2% target . Note that the Fed has seemed a bit more concerned about the persistently low inflation in recent weeks although this should not change that the Fed is on track to hike in December.

Also, a lot is going on in the Scandies. In Sweden, the government may decide on t he FSA's amort isat ion proposal. In Norway, retail sales data is due. In Denmark, the second release of Q3 GDP growth is also due.

Selected market news

Yesterday in the US, we saw yields climbing higher across the curve with the 2Y-10Y on the US government bond yield curve steepening around 3bp after a period of a flattening trend in the US yield curve. Similarly, we saw a decent sell-off across curves in the EUR fixed income market with the 2Y-10Y (on the German government bond yield) curve steepening around 2bp. The fixed income sell-off in the US and the euro area came on the back on positive news on the data front , the advance in the US tax bill, Fed Chair Janet Yellen calling the economic expansion ‘increasingly broad based' and possibly some profit taking by investors.

According to Bloomberg, the US Senate took a step towards the passage of the tax bill, with a l ikely vote later this week, after the US Senate Budget Committee passed the tax bill on Tuesday. However, this is a complicated process, as the Republicans can only afford to lose two votes.

German November HICP inflation came out at 1.8% y/y yesterday, which was slightly above consensus. This supports our call for euro area HICP core inflation today at 1.1% y/y. In addition, the European Commission's euro area sent iment indicator is continuing to climb, reaching the highest level since 2000.

In the US, both GDP and core PCE figures for Q3 17 were revised up from 3.2% y/y to 3.3% y/y and 1.3% y/y to 1.4% y/y, respectively.

In Sweden, we saw generally strong confidence numbers from NIE with no evidence that households have been affected by signs of a slowdown in the Swedish housing market. Consumer confidence rose to its highest since 2011. In all, a st rong report with some signs of a slowdown in construction. Swedish Q3 17 GDP came out weaker than expected, printing 2.9 % y/y compared to our call for 3.3 % y/y and consensus of 3.5 y/y. Note that Q1 17 and Q2 17 figures were revised down by 0.1pp.

Market Update – Asian Session: BOK Raises Rates, First Policy Move In 6-Yrs, Tech Names Remain Under Pressure, China...

Headlines/Economic Data

General Trend Themes: Asian markets trade mostly lower

Technology names track weakness seen in NY session; Tencent -2%

Chipmakers weaker, Taiwan Semi down over 3%; Bank of Korea Gov Lee said the memory chip boom to stay for now. (Recall: On Monday, shares of chip-related firms declined amid a cautious US broker note on Samsung Electronics)

China Nov PMIs rise

GBP trades higher

Japan

Nikkei 225 opened flat; closed

TOPIX Iron & Steel Index +1.9% (follow-through strength in steelmakers)

Mega banks track earlier outperformance in US financials: Mitsubishi UFJ +2%; TOPIX Securities brokers Index +1.4%

Fast Retailing +1.7%

Tech names track declines in US: Softbank -3%

Chip-related companies remain weak ; Tokyo Electron -2.4%, Toshiba -2%, SUMCO -1.5%,

BoJ's Harada: USD/JPY is stable at about ¥110 since QQE started; Labor shortages have been insufficient

JAPAN OCT PRELIM INDUSTRIAL PRODUCTION M/M: 0.5% V +1.8%E; Y/Y: 5.9% V 7.1%E

(JP) JAPAN OCT HOUSING STARTS Y/Y: -4.8% V -2.8%E; ANNUALIZED HOUSING STARTS: 933K V 952KE

JGB (JP) Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.1% 2-yr JGBS; avg yield -0.166%; bid-to-cover 4.76x

JGB (JP) Japan MoF sells ¥4.39T v ¥4.4T indicated in 3-Month Bills; avg yield -0.1995%

Looking Ahead: Oct CPI, Household spending , unemployment and Q3 Capex to be released on Friday.

Korea

Kospi opened -0.4%

Continued weakness in chipmakers: Samsung Electronics -2.5%, Hynix -5.5%

Woori Bank +1% (raises deposit rates following rate hike by BoK)

BANK OF KOREA (BOK) RAISES 7-DAY REPO RATE BY 25BPS TO 1.50%, AS EXPECTED, the first policy move in 6 years. Gov Lee said that the BOK does NOT have forecasts for future rate hikes and rate policy is based on mid-term inflation. Policy to remain accommodative and will judge carefully if further adjustments needed.

USD/KRW rises 1% on Gov Lee comments where he affirmed stance that FX rate is determined in market not benchmark rate only, FX authorities can respond to FX if volatility is extreme

Oct Data weakens: SOUTH KOREA OCT INDUSTRIAL PRODUCTION SA M/M: -1.1% V 0.2%E; Y/Y: -5.9% V 3.0%E (sharpest decline since 2013 on holiday distortions)

(KR) South Korea Oct Retail Sales m/m: -2.9% v 3.1% prior; y/y: -0.2% v 8.4% prior

(KR) South Korea Oct Cyclical Leading Index Change: -0.3 v -0.2 prior

(KR) On Wed, UN held emergency meeting following most recent North Korea launch: US Ambassador to -UN Haley: North Korean regime will be utterly destroyed if war comes

(US) Pres Trump tweets: to announce major new sanctions on North Korea

Looking Ahead: South Korea Q3 GDP revision and Nov Trade Balance due for release on Friday

China/Hong Kong

(CH) CHINA NOV OFFICIAL GOVT MANUFACTURING PMI: 51.8 V 51.4E, NON-MANUFACTURING PMI: 54.8 V 54.3 PRIOR

Markets opened lower: Hang Seng opened -1%, Shanghai -0.3%

Hang Seng Info Technology Index -2.2%, Materials -1.2%, Consumer Goods index -1.2%, Energy -1%, Financials -0.9%, Property -0.9%

(CN) PBoC sets yuan reference rate at 6.6034 v 6.6011 prior

(CN) China Oct Swift Global Payments (CNY): 1.46% v 1.94% prior

(CN) China FX Regulator SAFE Vice Head Lu Lei: China should manage FX reserves from economic stability view; FX reserves important part of macro prudential management

(CN) PBoC OMO: Injects CNY280B in 7, 14-day, 63-day reverse repos v CNY240B injected in 7,14 and 63-day reverse repos prior; Net: nil v nil prior (4th consecutive net nil)

(HK) 1-month HK$ HIBOR falls below 1% (halting 5 days of consecutive increases); 3-month -1bps to 1.18179%; 1-week -14bps to 0.75036%

(HK) China press looks at recent surges in HIBOR rates and how 95% of mortgages in Hong Kong are linked to Hibor and its possible negative impact

(CN) China Beijing sells 3-yr special bond at 3.79%; 10-yr special bond at 3.96%

China corporates continue to cancel yuan denominated bond offerings: China Datang Corp cancels planned CNY5B bond sale on ‘market fluctuation’

(CN) China Premier Li: China is willing to expand cross border trade with Russia

(CN) Japan, US and Europe reportedly plan to push China for action on steel overcapacity - Nikkei

(CN) China coal prices may fall in 2018 - China Info Daily

Looking Ahead: China Nov Caixin Manufacturing PMI expected on Friday

Australia/New Zealand

ASX 200 opened -0.4%; close -0.6%

Resources Index -1.3%

Financials Index -0.8% ; Australia Government releases draft terms of reference for financial services Royal Commission; (AU) Australia PM Turnbull: Uncertainty about the banking inquiry is weighing on the economy, need to resolve it

Aussie (AUD) trades higher amid domestic and China data releases

(AU) AUSTRALIA Q3 PRIVATE CAPITAL EXPENDITURE (CAPEX) Q/Q: 1.0% V 1.0%E ( Equipment, plant, machinery investment +0.7% q/q; Buildings, structures investment +1.2% q/q)

(AU) AUSTRALIA OCT BUILDING APPROVALS M/M: +0.9% V -1.0%E; Y/Y: 18.4% V 14.1%E

(AU) Australia Oct Private Sector Credit M/M: 0.4% v 0.4%e; Y/Y: 5.3% v 5.3%e

AWE Ltd (oil & gas company) +19% (received takeover offer from China Energy Reserve and Chemical Group

Kiwi (NZD) trades lower on session: (NZ) New Zealand Nov ANZ Business Confidence: -39.3 v -10.1 prior (8-yr low); Activity Outlook: 6.5 v 22.2 prior

(NZ) NEW ZEALAND OCT BUILDING PERMITS M/M: -9.6% V -2.5% PRIOR

APX.AU Completes A$25M institutional placement priced at at A$5.80/shr; +32%

Looking Ahead: New Zealand Q3 Terms of Trade tomorrow

Other Asia

(SG) Singapore Central bank (MAS): Will continue to monitor property market developments and where necessary take appropriate action to maintain stable and sustainable market

North America

US equities ended mixed: Dow Jones +0.4%, S&P 500 flat, Nasdaq -1.3%, Russell 2000 +0.4%

S&P500 Tech Sector -2.2%, Financials Sector +1.7%

Costco SSS above est: Reports Nov Total SSS (ex-gas) 7.9%; US SSS (ex-gas) 8.4% v 5.7%e; E-commerce sales +39%

Tax Reform: (US) Tax reform bill passes in procedural hurdle in US Senate (as expected); Vote 52 v 48; Allows for debate to begin on the Senate floor with a final vote likely by Friday

(US) Trump sends nomination of Marvin Goodfriend for Fed to Senate; - We have contingencies in place but hope it doesn't come to that

Fed Speak: (US) Fed Chair Yellen: Strengthening US economy will warrant continued interest rate increases - prepared remarks before joint economic committee; Weak inflation likely to prove "transitory"; don't think it's a mystery why inflation was so low in past years; this year's low inflation is puzzling; Fed is keeping an eye on recent low inflation trends

(US) Fed Williams (moderate, non-voter): failing to raise rates to more normal levels could risk recession; should continue to raise rates slowly over coming year; Four rate hikes between now and end of 2018 makes sense

(US) Fed's Dudley (dove, FOMC voter): There are not a lot of excesses currently in US economy

Energy: (US) DOE CRUDE: -3.4M V -2ME

(SA) Saudi Oil Min al-Falih: not concerned about market reaction to OPEC discussions today - comments in Vienna

(KW) Kuwait Oil Min: ministerial committee has recommended 9-month cut agreement extension

(RU) Russia Energy Min Novak: we have had a constructive dialogue; oil market has yet to balance; everyone agrees oil production cutting agreement should be extended; Specific details on production cuts will be discussed at Thurs OPEC meeting

(IA) Iran Oil Minister Zangeneh: will go along with 6 or 9 month extension if it is majority decision at OPEC

Looking ahead: OPEC Meeting, US Nov Chicago PMI

Europe

(EU) ECB's Knot: inflation outlook poses no threat to price stability; ECB communications should shift away from net purchases

(EU) ECB’s Weidmann (Germany): remain skeptical about need for ECB QE

(EU) ECB reportedly may postpone separate proposals to deal with both new and old non-performing loans – press

GBP/USD: In Asia trades at highest level since Sept, above 1.3460

(UK) EU Parliament Brexit committee: have not made enough progress in the Brexit talks on citizens rights or Ireland

(UK) PM May: We are still in negotiations with the EU. For the current budget plan, I also said that we would honour our commitments and we are still in negotiations with the EU. I want to see us able to move forward together into the next stage of the talks when we can look in detail at the deep and special partnership we want to have with the EU once we leave." - Sky News interview

(UK) Britain reportedly nearing deal on Northern Ireland border; officials on both sides reportedly predict agreement within weeks - Times UK

*(UK) NOV GFK CONSUMER CONFIDENCE: -12 V -11E

M&A: Nokia [NOKIA.FI]: Responds to media reports: Says not in talks with Juniper Networks [JNPR] nor is it preparing an offer

(PT) Hearing Italy will back Portugal Fin Min Centeno to be next Eurogroup chairman - financial press

SBM Offshore NV [SBMO.NL]: Said to pay $238M to settle US bribery case

Looking Ahead: Swiss Q3 GDP, EZ Nov Prelim CPI

Levels as of 01:00ET

Nikkei225 +0.7%, Hang Seng -1.4%; Shanghai Composite -0.4%; ASX200 -0.7%, Kospi -1.1%

Equity Futures: S&P500 -0.0%; Nasdaq100 -0.1%, Dax -0.0%; FTSE100 -0.2%

EUR 1.1871-1.1846; JPY 112.13-111.89; AUD 0.7593-0.7557;NZD 0.6889-0.6833

Dec Gold +0.1% at $1,283/oz; Jan Crude Oil +0.3% at $57.47/brl; Mar Copper +0.2% at $3.07/lb

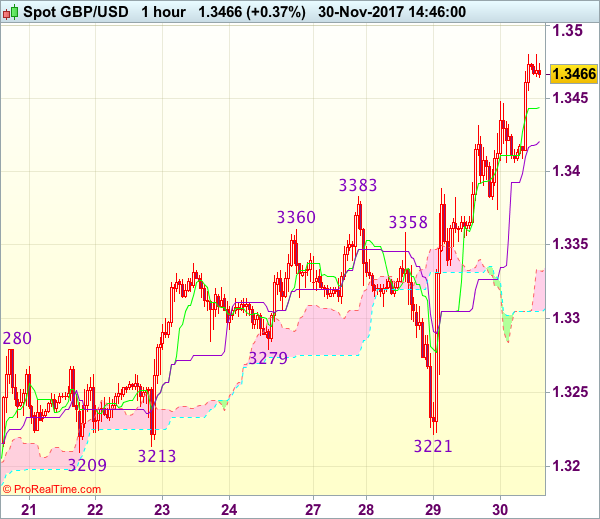

Trade Idea : GBP/USD – Buy at 1.3385

GBP/USD - 1.3458

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3445

Kijun-Sen level : 1.3423

Ichimoku cloud top : 1.3332

Ichimoku cloud bottom : 1.3305

New strategy :

Buy at 1.3385, Target: 1.3485, Stop: 1.3350

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after recent rally above previous resistance at 1.3383 (now support), adding credence to our bullish view that the erratic rise from 1.3027 low is still in progress, hence upside bias remains for this move to extend further gain to 1.3480-85, however, overbought condition should prevent sharp move beyond 1.3500-10 and price should falter below 1.2475-80, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy sterling on subsequent pullback as 1.3383 (previous resistance turned support) should limit downside and bring another rise. Below 1.3355-60 would suggest top is formed instead, bring weakness to 1.3330, then towards 1.3300 but reckon downside would be limited to 1.3260-65.

Trade Idea : EUR/USD – Buy here

EUR/USD - 1.1864

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1860

Kijun-Sen level : 1.1850

Ichimoku cloud top : 1.1894

Ichimoku cloud bottom : 1.1859

New strategy :

Buy at market level, Target: 1.1965, Stop: 1.1835

Position : -

Target : -

Stop : -

Although the single currency fell to as low as 1.1817 yesterday, the subsequent rebound suggests low is possibly formed there and consolidation with upside bias is seen for gain to 1.1895-00, however, break of indicated resistance at 1.1920 is needed to signal the pullback from 1.1961 has ended at 1.1817, bring further gain towards this level, break there would extend recent upmove to 1.1990-00 which is likely to hold from here.

In view of this, we are looking to buy euro again on dips. Below 1.1830-35 would risk retest of 1.1817 but only break there would signal the retreat from 1.1961 is still in progress for retracement of recent rise to 1.1805-10 (61.8% Fibonacci retracement of 1.1713-1.1961) and possibly towards 1.1770 but price should stay well above support at 1.1736, bring rebound later.

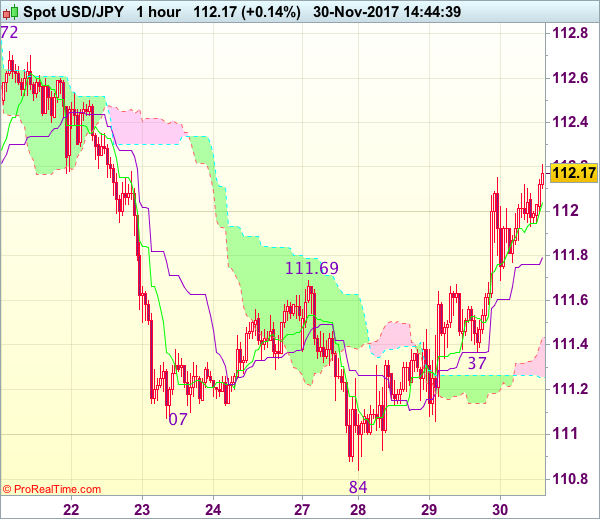

Trade Idea : USD/JPY – Buy at 111.40

USD/JPY - 112.18

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.04

Kijun-Sen level : 111.79

Ichimoku cloud top : 111.44

Ichimoku cloud bottom : 111.26

Original strategy :

Buy at 111.40, Target: 112.40, Stop: 111.05

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.40, Target: 112.40, Stop: 111.05

Position : -

Target : -

Stop : -

As the greenback has risen again after brief pullback, adding credence to our view that low has been formed at 110.84 earlier this week, hence consolidation with upside bias remains for this rebound to bring retracement of recent decline and further gain to 112.40-50 would be sen, however, near term overbought condition should limit upside and price should falter below resistance at 112.72, bring retreat later this week.

In view of this, we are still looking to buy dollar on dips as 111.35-40 would limit downside. Below 111.05-10 would abort and signal the rebound from 110.84 has ended, bring retest of this level, break there would signal recent decline has resumed and extend weakness to 110.70 and possibly towards 110.50.