Sample Category Title

Dollar Lifted by Data and Yellen, Focus Turns to Senate Tax Plan and PCE

Sterling and Dollar remain the two strongest currencies for the week. The greenback was supported by better than expected GDP data overnight, as well as Fed Chair Janet Yellen's upbeat comments. Positive sentiments in the US also sent DOW to record high at 23940.68, up 103.97 pts or 0.44%. NASDAQ, though, dropped -1.27% as investors dumped tech for bank stocks. That was in response to Fed Chair nominee Jerome Powell's hints on easing regulations. An important development to note is the rebound in treasury yields. 10 year yield closed up 0.038 at 2.376, keeping the near term bullish trend. The focus will now turn to Senate tax plan vote and PCE inflation data from US today.

Senate to open debate on Republican tax plan

Senate voted to open the debate on Republican tax plan yesterday, moving another step to a final vote possibly today or tomorrow. President Donald Trump said in his usual tone said in a rally in Missouri that it's a "once in a liftetime opportunity" and urged the Congress to deliver. And he added that "this week's vote can be the beginning of the next great chapter for the American worker." It's widely know that the Republicans got slim 52 majority in the Senate. All 48 Democrats and independents are expected to vote no. So, Republicans could only afford to lose two if they want to pass the bill this week. Then, they can move on to the next stage of reconciling the House and Senate versions.

Fed Yellen: Economic expansion is increasingly broad based

Outgoing Fed Chair Janet Yellen sounded upbeat in her last Congressional testimony overnight. She told the Joint Economic Committee that "the economic expansion is increasingly broad based across sectors as well as across much of the global economy." She acknowledged that "we are not seeing undue inflationary pressure in the labor market, so our policy remains accommodative." However, she also emphasized that " it's important to gradually move our policy rate toward what I'll call a neutral level, which would be consistent with sustainably strong labor market conditions." She maintained that Fed would want to remove stimulus "gradually" to avoid "overheating" and cause a "boom-bust" condition.

Fed Williams: Inflation will pickup in 2018

San Francisco Fed President John Williams also said "as long as the data continue to show steady growth and we see the uptick in inflation that we're expecting, my own view is that we should continue to raise interest rates slowly over the coming year." He also sounded unconcerned with the low inflation. He noted that inflation would usually take around 12 months to pick up after growth accelerates. He added that "the next time you see a headline about stubbornly low inflation, you can smile to yourself, knowing that the mystery isn't all that mysterious after all." And, "with the economy doing so well this year and based on the historical pattern, I expect to see a rise in inflation in 2018."

Fed's Beige Book economic report noted that "price pressures have strengthened since the last report." Labor market also tightened as "most districts reported employers were having difficulties finding qualified workers across skill levels." Nonetheless, "wage growth was modest or moderate in most districts."

ECB Knot urged full phase out of QE from September onwards

ECB Governing Council member Klaas Knot said that "with deflation risk clearly off the radar, the main rationale for employing the APP (asset purchase program) has therefore ceased to exist." He added that "fear of relapse owing to an allegedly premature discontinuation of net purchases seems rather overdone." Hence, he urged a "full phasing" out of the program "from September onwards". Back in October, ECB extended the asset purchase program to September next year, but halved the purchase size to EUR 30b a month starting January.

SPD Schulz want bold vision in coalition talk with Merkel

German Chancellor Angela Merkel will meet with Social Democratic Party head Martin Schulz and President Frank-Walter Steinmeier today on talk of reforming the grand coalition. Ahead of the meeting, Schulz said that "I can't tell you what the outcome of the talks will be, but I can assure you of one thing: that I will argue in favor of the best solutions for our country and that my party is aware of its political responsibility." And, he emphasized that "you can't just wing it. You need a bold vision". Schulz also called fro a euro-area budget, a Eurozone finance minister and a "European framework for minimum wages".

On the data front

Japan industrial production rose 0.5% mom in October versus expectation of 1.8% mom. Australia private capital expenditure rose 1.0% in Q3, meeting consensus. Australia building approvals rose 0.9% mom in October, above expectation of -1.0% mom. New Zealand building permits dropped -9.6% mom in October. ANZ business confidence dropped sharply to -39.3 in November. China manufacturing PMI rose 0.2 pt to 5.18 in November, non-manufacturing PMI rose 0.5 to 54.8. UK Gfk consumer confidence dropped to -12 in November.

Looking ahead, the calendar is very busy today. Swiss GDP, KOF and retail sales will be featured in European session. Germany will release unemployment. Eurozone will release CPI and unemployment rate. Later in the day, US PCE is the main focus while jobless claims and Chicago PMI will be featured.

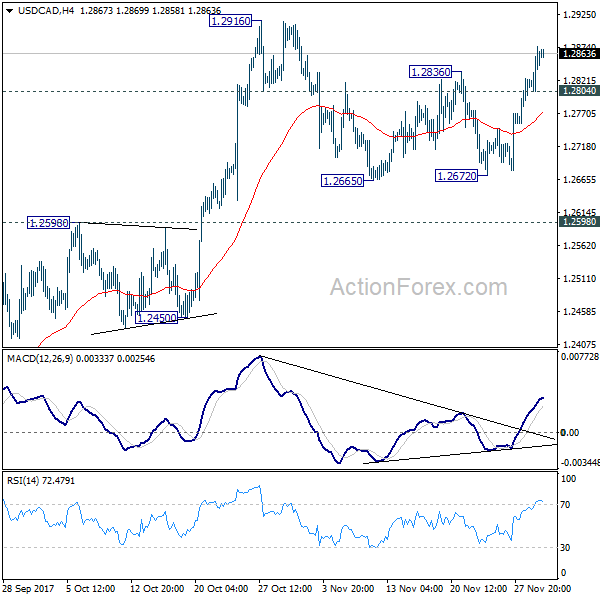

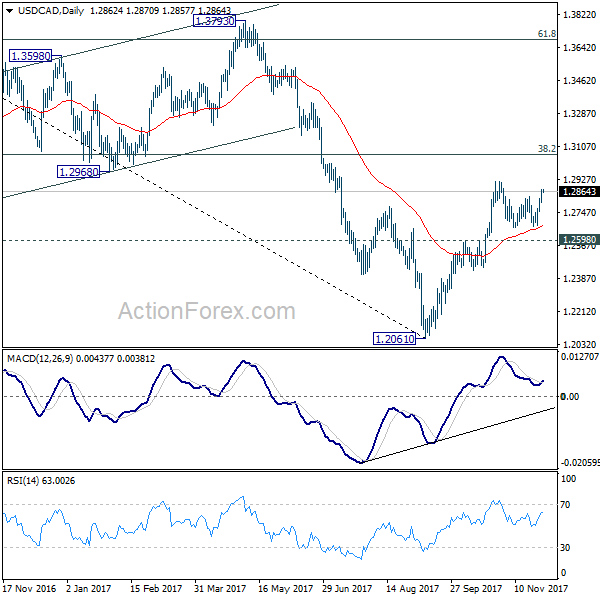

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2822; (P) 1.2847; (R1) 1.2890; More....

Intraday bias in USD/CAD remains on the upside for 1.2916 resistance. As noted before, corrective pattern from 1.2916 could have completed at 1.2672 already. Break of 1.2916 will resume whole rise from 1.2061 and target 1.3065 medium term fibonacci level. On the downside, below 1.2804 minor support will delay the bullish case and extend the correction from 1.2916 with another fall. But still, we'd expect downside to be contained by 1.2598 resistance turned support and bring rebound.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Oct | -9.60% | -2.30% | -2.50% | |

| 23:50 | JPY | Industrial Production M/M Oct P | 0.50% | 1.80% | -1.00% | -1.00% |

| 00:00 | NZD | ANZ Business Confidence Nov | -39.3 | -10.1 | ||

| 00:01 | GBP | GfK Consumer Confidence Nov | -12 | -11 | -10 | |

| 00:30 | AUD | Private Capital Expenditure Q3 | 1.00% | 1.00% | 0.80% | 1.10% |

| 00:30 | AUD | Building Approvals M/M Oct | 0.90% | -1.00% | 1.50% | 0.60% |

| 01:00 | CNY | Manufacturing PMI Nov | 51.8 | 51.5 | 51.6 | |

| 01:00 | CNY | Non-manufacturing PMI Nov | 54.8 | 54.3 | ||

| 05:00 | JPY | Housing Starts Y/Y Oct | -2.80% | -2.90% | ||

| 06:45 | CHF | GDP Q/Q Q3 | 0.60% | 0.30% | ||

| 08:00 | CHF | KOF Leading Indicator Nov | 109.5 | 109.1 | ||

| 08:15 | CHF | Retail Sales Real Y/Y Oct | 0.30% | -0.40% | ||

| 08:55 | EUR | German Unemployment Change Nov | -10K | -11K | ||

| 08:55 | EUR | German Unemployment Claims Rate Nov | 5.60% | 5.60% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 8.90% | 8.90% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Nov | 1.60% | 1.40% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov A | 1.00% | 0.90% | ||

| 13:30 | CAD | Current Account Balance (CAD) Q3 | -20.3B | -16.3B | ||

| 13:30 | USD | Initial Jobless Claims (NOV 25) | 241K | 239K | ||

| 13:30 | USD | Personal Income Oct | 0.30% | 0.40% | ||

| 13:30 | USD | Personal Spending Oct | 0.30% | 1.00% | ||

| 13:30 | USD | PCE Deflator M/M Oct | 0.10% | 0.40% | ||

| 13:30 | USD | PCE Deflator Y/Y Oct | 1.50% | 1.60% | ||

| 13:30 | USD | PCE Core M/M Oct | 0.20% | 0.10% | ||

| 13:30 | USD | PCE Core Y/Y Oct | 1.40% | 1.30% | ||

| 14:45 | USD | Chicago PMI Nov | 62.3 | 66.2 | ||

| 15:30 | USD | Natural Gas Storage | -46B |

GBP/USD Reaches Resistance Within Daily Channel

We've been watching this GBP/USD channel as price moves up between horizontal support/resistance zones.

Price has found some bullish legs following the last tap that we spoke about on the blog last week, but has now reached previous swing high resistance and stalled.

GBP/USD Daily:

How price behaves around this horizontal resistance level will be key as to whether we reach the upper band of the channel, or whether we just head back down again. Either way, this is the level that traders can manage their risk around.

Now zoom into an intraday chart and take a look at the hourly below.

GBP/USD Hourly:

These are the sorts of short term support turned resistance (and vice versa) that we want to look for. Especially on the short side if the above daily level does in fact hold.

Beige Book Indicates Price Pressures Firming in Q4

Today's Beige Book indicated that economic activity across all twelve Federal Reserve Districts increased at a modest to moderate pace between October and mid-November. The outlook improved slightly from the previous report that highlighted hurricane-related setbacks.

Retailers reported optimistic views on holiday spending, with pre-holiday consumption reports largely being mixed as consumers held off on purchases in many cases in anticipation of Black Friday promotions. Retailers expect holiday spending to bolster revenue in the fourth quarter, with auto dealers also expecting a boost. Some retailers have implemented technology upgrades in order to entice shoppers back into stores, providing a streamlined shopping experience between the digital and brick-and-mortar worlds.

Price pressures intensified relative to the previous report, with moderate increases in non-labor input costs being passed onto selling prices. Building material price increases were magnified by strong demand as hurricane rebuilding efforts progressed. Moreover, input costs increased in the transportation and manufacturing sectors, with the inflation largely passed through to consumers.

Residential real estate inventories remained tight, leading to consistent growth in prices with the low inventories resulting in multiple-offer scenarios that have magnified affordability concerns. Some contacts reported increased interest in remodeling services, as homeowners hold on to their properties longer due to tight market conditions. At the same time, a scarcity of labor also limited construction activity. These effects will be amplified by rebuilding following hurricanes Harvey and Irma in the coming quarters. Additionally, builders are concerned about passing through the quickly rising input costs, including land, building materials, as well as labor, to consumers, potentially preventing first-time homebuyers from purchasing property. Non-residential construction increased slightly, extending trends reported last month. Industrial and warehouse space is in high demand, while retail space development remains weak amid a continuing shift to online shopping.

Employment growth picked up relative to the prior report, with hiring progressing at a modest to moderate pace, resulting in universally tight labor markets. Employers continue to report difficulty in recruiting and retaining workers of various skill levels, with this issue posing a threat to expansion. Wage increases were modest or moderate, emulating last month's report, with the most substantial increases being reported for professional, technical and production positions where workers are in especially short supply. Increasingly, firms are using sign-on and mid-year bonuses, over-time, and other non-wage efforts in order to retain and attract workers.

Manufacturers remain optimistic and expect a pickup going forward, with business having expanded moderately during the reporting period. The expansion in shipments kept the transportation industry busy, which was reported to have expanded in all Districts with the exception of New York. Additionally, the recent California wildfires prevented some shipments, as reported by the San Francisco Federal Reserve Bank staff.

Key Implications

This Beige Book confirms that economic activity continues to advance in the fourth quarter, with hurricane-related setbacks having quickly faded. Business optimism will continue to support investment over the remainder of the year, with the largest constraint on growth currently related to widespread labor shortages. However, firms are counteracting this by investing more heavily in equipment to support expansion, boding well for productivity. Additionally, producers remain upbeat, and expect global economic strength to support continued expansion going forward. These growth prospects should strengthen further as the GOP tax reform plans come closer to materializing, with a slashing of the corporate tax rate potentially lifting investment previously held back by policy uncertainty.

Labor markets are extremely tight and will continue to bolster household incomes and solidify the consumer as an important driver as growth in the fourth quarter. The residential property market will likely remain undersupplied as rising input costs, related to land and labor shortages, hold back new construction, leading prices of new homes higher and holding back purchases.

The report suggested that businesses are increasingly passing on increases in their own input costs to consumers, with these moves likely to show up in inflation in the near future. These dynamics, alongside strong economic growth, will continue to support the case for a December rate hike, something we see happening with near-certainty at this point.

A Brave New Bubble

The overnight focus was on the upswing in global yields which offered the greenback no clear channel as traders found themselves confined to the stationary bike, peddling fast but going nowhere quickly while regurgitating the same narratives in very prosaic detail.

On the Fed front, Yellen's testimony, unlike the markets take away from the recent FOMC minutes, continued to emphasise transitory factors in subdued inflation while suggesting the US economic recovery was "increasingly broad-based". By default, the market views this hawkish, but from my seat, the comments are little more than December rate hike window dressing.

Tax reform bill passed the procedural hurdle in US Senate as expected.But rik positivity should continue to underpin the USD into the final tally.

The Japanese Yen

Don't get overly complacent with USDJPY nearing the 112 level as trading JPY remains as intense a dogfight as ever with competing narratives contributing to the choppy price action.

Downside momentum stalled after investors sidestepped the North Korea escalation.However, it may have provided a false sense of bravado suggesting that all that ills the world are cured. But nothing could be further from the truth as risk aversion is waiting in the wings ready to pounce on the first sign of weakness.

But for today at least, improving prospects for tax reform should carry the day.

Long USDJPY remains one of the more crowded trades as short-term speculators have piled in suggesting this will be the best vehicle to sell on any signs of dollar weakness.

The Euro

The single currency continues to underperform versus the markets lofty expectations entering the week. At the core, the USD has gone tacitly bid across G-10 on as the US yields pop and equity market continue to froth on improving tax reform sentiment. But as mentioned yesterday it's more to do with EURGBP crater dampening sentiment as GPB continues to march to the beat of its own drummer after the Bullish Brexit headlines.

Australian Dollar

AUDUSD rate differential touched below the 0 mark for the first time in ages triggering machine driven sell orders based on Aussies diminishing carry advantage.

However, most of the Aussie pressure is coming from GBPAUD cross as the market continues to add to longs.

The Chinese Yuan Pre Fix

The markets are awaiting Chinese PMI

Energy Prices

The market continues to trade the OPEC headlines, but the only one that counts Russia signalled it was leaning towards a nine-month extension. As usual, this whole OPEC fiasco is a complex event. Even if a nine-month extension is agreed to in principle, the entire debate is open for review in April anyway. Moving on ………

Korean Won

There will be of massive interest in the Bank of Korea( BoK) rate decision as the BoK is now viewed as the proxy for regional monetary policy.

The Malaysian Ringgit

The Market continues to express its bullish Asia FX views through the Ringgit which rallied again yesterday pushing through a 52-week high

The unexpected arrival of interest normalisation is taking hold of sentiment. And with Malaysia investors already riding the wave of a robust global demand, the higher interest rate scenario as adding to the Ringgit's appeal. Since the market has still not fully priced in a January rate hike nor the real prospects of a follow-up interest rate hike in Q2 or Q3, the rally could extend well into year-end as traders set sights on the critical 4.00 level.

MYR may be less susceptible to adverse shifts in the global growth narrative as the Ringgit remains under-owned by investors But the near-term risks are a collapse in Oil prices post OPEC meeting or a deterioration in risk sentiment from China Bond and Equity markets souring into year-end potentially destabilising regional markets.

From the macro perspective, the export sector continues to flourish, and by that alone, and despite the Ringgit trading at a 52 week high, the MYR remains undervalued relative to some of its high flying regional peers

Speaking of which; the market continues to view the KRW as a broader proxy for local FX risk as well as rates normalisation. With the BoK set to raise interest rates as the domestic economy continues to soar, expect the MYR to ride any buoyant Won sentiment. And with the Ringgit posied to do some serious catch up to regional peer currency valuations, the MYR should remain one of the go-to trades for Asia FX investors heading into year-end.

A Brave New Bubble

But with all the commotion on Bitcoin, it offered some distraction to a listless trading day on forex desks. However, with the new wave of so-called "Crypto Strategist" hitting the airwaves overly long on theory and conjecture but lacking any structural blueprint or trading narrative, it might be time for some reflection, in case the masses forget to come up for air before it's too late.

These are extraordinary times in the market. The primary drivers of bitcoin momentum in my view 1) The CME's acceptance that seems to have lit a fire under wall street. Cryptocurrencies will gain more credibility as CME Group Inc. starts selling bitcoin futures and other mainstream institutions get involved 2) Intense media coverage supporting the current rally which leads to 3) Investors pervasive apprehension that they're missing the party or the underlying fear of losing out of a quick profit.

It's not just your average retail Joe champing at the bit, high net worth investors are starting to view Bitcoin as an asset class in the same light as investing in other higher-risk debt and are gradually accepting it as a legitimate asset class.

Bitcoin will continue to broaden its legitimacy and credibility as more of the more significant well known Primary Market Makers enter the field.Provided Bitcoin has a favourable lift off on the CME later this year Bitcoin could surge higher from credibility perspective alone.

Of course, Government agencies will likely clamp down on excessive margin given the hyper-volatility as the potential loss to non-sophisticated investors is enormous. After all, risk management continues to run weak in the retail space.

Canadian Dollar Drops on Oil Price Setback

The Canadian dollar depreciated on Wednesday after conflicting comments out of Vienna ahead of the meeting between Organization of the Petroleum Exporting Countries (OPEC) and non-OPEC members no Thursday. The production cut deal which has stabilized prices for more than a year is set to expire in March of 2018, but there is a case for extending the timeline by 9 months. Crude has already priced in an announcement tomorrow, but there is still room for disappointment as Russia could get cold feet and ask for a shorter commitment.

The US economy expanded by 3.3 percent in the third quarter as per the second estimate released today. The gap between the pace of growth in Q3 and the slowdown of the Canadian economy favours the greenback. On Friday the monthly Canadian GDP will be released with the market expecting an improvement over the 0.1 percent contraction last month.

Canadian Prime Minister Justin Trudeau will visit China on December 3 with the intention to build a plan B on trade in case NAFTA ends up disappearing. While not exactly a perfect replacement a deal with China could diversify Canada's reliance on its neighbour to the south, but given the long negotiation periods for this type of deals it could be a decade before it is signed.

The USD/CAD gained 0.37 percent on Wednesday. The currency pair is trading at 1.286 due to strong economic indicators in the US against zero releases on the Canadian front. The US followed yesterday's strong consumer confidence numbers with a preliminary GDP improvement of 0.3% in the third quarter. The US economy is now expected to have gained 3.3 percent in Q3. The figure came in right at the forecast, but it did help the USD regain some of the lost momentum from last week.

Politics will remain a thorn in the dollar's side as the tax reform bills are facing rising opposition from crowdsourced efforts. The Trump's Administration decision to once again try to do too much with the bill could end up being its undoing.

The loonie was impacted by lower oil prices as the correlation between the commodity and the currency has increased after it had decoupled earlier in the year. The news out of Vienna tomorrow will decide the path of the black stuff as OPEC members and non-members are expected to prolong the production cut agreement that has stabilized prices. For the Canadian currency the focus will be on Friday's release of jobs and gross domestic product (GDP) data released at 8:30 am EST.

The price of oil fell in the last 24 hours. West Texas Intermediate is trading at $57.27 after conflicting headlines about the Organization of the Petroleum Exporting Countries (OPEC) meeting in Vienna forced the price of crude under the $57 price level despite the release of US crude weekly inventories showing a larger than expected drawdown.

The market is already pricing in a 9 month extension that will push the production cut agreement between OPEC and non-OPEC until the end of 2018. Russia has been rumoured to be more eager to push for a 3 to 6 month extension, which is why the technical committee that met earlier this week is offering a compromise. A 9-month extension with the possibility of a review at the 6 month mark. When the OPEC announces the extension anything lower than 9 months could cause a drop in prices.

US crude stocks were lower by 3.4 million barrels, but it was the unexpected gasoline and distillate inventories that had a negative impact in the price of oil just as the OPEC meeting is set to wrap up on Thursday.

US production has increased and with the Keystone pipeline restarted operations, but still at reduced capacity. Disruptions in North America due to weather and forest fires has kept production lower than otherwise expected with the OPEC doing the heavy lifting on price stability. The market will be watching for developments in Vienna as the floor of energy pricing has been put in place by the OPEC production cut, and once it reaches its end crude prices will be vulnerable if global demand for energy has not recovered at the same rate as production.

Market events to watch this week:

Thursday, November 30

- 8:30am USD Unemployment Claims

Friday, December 1

- 4:30am GBP Manufacturing PMI

- 8:30am CAD Employment Change

- 8:30am CAD GDP m/m

- 10:00am USD ISM Manufacturing PMI

*All times EDT

Pound Climbs as Britain Sweetens Brexit Pot

The British pound has posted considerable gains in the Wednesday session. In North American trade, GBP/USD is trading at 1.3443, up 0.77% on the day. On the release front, British Net Lending to Individuals dropped to GBP 4.8 billion, above the forecast of GBP 4.3 billion. Bank of England Governor Mark Carney spoke at an event in London. In the US, Preliminary GDP for the third quarter came in at 3.3%, matching the forecast. Pending Home Sales jumped to 3.5%, crushing the estimate of 1.1%. As well, Fed Chair Janet Yellen testifies before a congressional committee. On Thursday, the US releases Personal Spending and unemployment claims.

British Prime Minister Theresa May has blinked first, going a long way to meeting the European demands on Britain's bill for leaving the European Union. The Europeans had demanded EUR 60 billion, while the UK had countered with EUR 20 billion. However, the UK has upped its offer significantly, and the final amount could be as high as EUR 50-60 billion. The British government is anxious to start talks on a trade deal with the EU, and this offer should placate Brussels and pave the way for trade talks to begin in December. Another thorny issue is the border between Northern Ireland and Ireland. Britain has ruled out having the north remain in a customs union with the EU after Brexit, but Ireland is insisting that there not be a hard border.

There was positive news from the banking sector on Tuesday, as all seven major UK banks passed the BoE's stress tests. This is a reliable indication that the banking sector is in decent shape, despite nagging concerns about the toll that Brexit could take the British economy. Still, investors were quick to seize on negative comments from BoE Governor Mark Carney, who warned that in the case of a "disorderly" Brexit, the financial sector would face "some quite material economic costs". Carney's warning briefly sent the pound lower, but it managed to recover.

Minor Slowdown Expected in Chinese Manufacturing Activity; Aussie also in Spotlight

Chinese official manufacturing and services PMIs for the month of November are due on Thursday at 0100 GMT, while Caixin's respective measure for the manufacturing sector is scheduled for release on Friday at 0145 GMT.

According to analysts' projections, the official manufacturing PMI will decline to 51.4 in November from October's 51.6. Despite the ongoing rebalancing in the Chinese economy resulting in the services sector playing an ever more prominent role in terms of contribution to economic activity, the bulk of attention still remains on the release of manufacturing PMI figures, with no polls for services PMI being released. The Caixin manufacturing PMI, which compared to the official figure focuses more on small and mid-size businesses, is also expected to reflect a minor slowdown, falling to 50.9 from October's 51.0. A reading of 50 reflects zero sectoral growth.

Should manufacturing activity indeed decline, then this is not necessarily a negative sign - at least not in its entirety - for the world's second largest economy as it would be partially attributed to the government's efforts to curb pollution in its attempts to shift focus to the quality of growth rather than merely the quantity. Along similar lines, a clampdown of financial risks could also act as a drag on activity by virtue of higher borrowing costs. It is not just government efforts for better quality expansion that are weighing on manufacturing growth though, as weaker export orders are adding downward pressure on Chinese factories' activity as well.

It should be noted that if the official gauge of manufacturing activity comes below October's as expected, this would mark the second straight month of declining activity, though, in a sign of resilience, it would also constitute the 16th consecutive month of growth (i.e. a reading above 50).

Besides movements in the yuan, the Australian dollar will be closely watched by forex market participants when the above data become public, as the Australian currency is considered a liquid proxy for China's economy due to the two nations' strong trade ties.

An upside surprise in the figures, could push aussie/dollar higher. In such an event, the pair might meet resistance around the two-week high of 0.7644 recorded earlier in the week. Should the slowdown in activity be sharper than anticipated, then aussie/dollar is likely to head lower. In this case, the pair could find support around 0.7529, this being the five-and-a-half-month low recorded on November 21.

It should also be taken into account that Australian data that have the capacity to generate movements in the aussie will also hit the markets tomorrow. Those include building capital expenditure and private new capital expenditure due at 0030 GMT.

Yen Dips as US GDP Accelerates in Q3

The Japanese yen has posted considerable gains in the Wednesday session. In North American trade, USD/JPY is trading at 111.84, up 0.34% on the day. On the release front, Japanese Retail Sales disappointed with a decline of 0.2%. This missed the estimate of a 0.1% gain. Later in the day, Japan releases Preliminary Industrial Production, with an estimate of 1.9%. In the US, Preliminary GDP for the third quarter came in at 3.3%, matching the forecast. Pending Home Sales jumped to 3.5%, crushing the estimate of 1.1%. As well, Fed Chair Janet Yellen will testify before a congressional committee. On Thursday, the US releases Personal Spending and unemployment claims, and Japan publishes Tokyo Core CPI.

Fed Chair Designate Jerome Powell testified before the Senate Banking Committee on Tuesday. Powell said that he favored tailoring regulations for small banks, leaving the toughest regulations for the big players. Powell was cautious and diplomatic during the hearing, saying that the case is building for a December rate hike, and refused to express an opinion on the Trump tax bill. He will replace Janet Yellen in February, and is widely expected to continue Yellen's monetary stance of small, gradual rate hikes. Fed policymakers have differing views on what to do about inflation, which remains at low levels. Some members have proposed that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Is the Bank of Japan rethinking its massive stimulus program? With the Japanese economy showing moderate growth, there has been speculation that the Bank of Japan is giving some thought to tapering stimulus. Any tapering to the program could give a significant boost to the yen, so the markets are closely monitoring BoJ statements and comments from BoJ policymakers, looking for clues. However, a stronger yen would hurt exports, which has been a catalyst for the stronger economy. Inflation and wage growth remain low, and if we are to take BoJ Governor Haruhiko Kuroda at his word, the Bank will not taper stimulus before inflation moves closer to the BoJ's target of around 2 percent.

USD Off Eecent Lows, But Gains Remains Modest

- European equities had a strong run today, surfing on the risk-on sentiment triggered by increased hopes of the Congressional adoption of the US tax reform. US equities opened mixed with S&P building out yesterday's gains and Nasdaq showing modest losses.

- Britain has bowed to EU demands and agreed to fully honour its financial commitments as identified by Brussels, removing one of the biggest obstacles to a Brexit divorce settlement. UK would assume EU liabilities worth up to €100 bln although net payments, discharged over many decades, could fall to less than half that amount.

- Prices in Germany rose faster than expected in November, in an encouraging sign of the resilience of inflation trends in the eurozone as the central bank prepares to start withdrawing its quantitative easing programme. Consumer prices rose 1.8% Y/Y in November, a sharp jump from last month's disappointing 1.5% Y/Y.

- US GDP grew at an annualised rate of 3.3% in Q3, the highest reading since Q3 of 2014. The improvement reflected increases in business investment, exports and private inventories. However, consumer spending expanded at a slower pace of 2.3%, down from the 3.3 per cent growth notched in Q2.

- In a prepared testimony to Congress, Fed chair Yellen gave a positive health check on the economy's recent performance and stuck with her existing line on gradual rate rises, but warned that deeper reforms would be needed to generate a "sustained boost" in economic growth without causing inflation that is too high.

- Economic recovery across the eurozone has eased pressures on its financial system according to the European Central Bank's financial stability review, but concerns over greater risk-taking by investors hunting for returns in low-volatility markets still linger.

Rates

Core bonds under moderate downward pressure

Core bonds were under pressure from the start of the European trading. A first down-leg coincided with a strong opening of equity trading. German inflation data were slightly higher-than-expected preventing any noticeable return action. A second down-leg was triggered by the publication of Yellen's written testimony before the JEC. She sees the recent low inflation due to transitory factors and calls the expansion increasingly broad-based. Financial risks are muted. She concludes that gradual further tightening is appropriate. So a third rate hike this year in December is baked in the cake. While she won't be chair anymore in 2018, she looks favourable to more rate increases in 2018.

At the time of writing, the German yield curve steepened with yields up to 4 bps higher. The US yield curve steepened too with yields up between 1.6 bp (2-yr) and 5.6 bps (30-yr). On intra-EMU bond markets, peripherals profited from the risk on climate and narrowed 2-to-4 bps.

Currencies

USD off recent lows, but gains remains modest.

Today, the dollar gained slightly further ground as yesterday's progress on a tax bill caused some USD shorts to reduce exposure. The dollar received some breathing space as its trades off its recent lows against the euro and the yen. However, US political risk isn't out of the way and the technical picture didn't improve in a profound way yet.

Overnight, Asian equities couldn't fully copy strong WS gains, trading mixed to slightly higher. Rising tensions on North Korean and uncertainty on the impact of measures to prevent excessive leverage in China, amongst others, might have played a role. Yesterday's USD rally stalled. USD/JPY touched an intraday top early in Asia, but the dollar eased slightly as the Asian trading evolved. USD/JPY traded in the 111.50 area going into the start of European dealings. EUR/USD changed hands in the 1.1860 area.

Early in Europe, interest rate differentials narrowed temporary in favour of the euro. EUR/USD touched an intraday top in the 1.1880, but the gained could not be sustained. EMU data were mixed. French spending data disappointed. EC economic confidence rose to a multi-year peak. First EMU inflation data also gave a diffuse picture. The ECB in its stability report said that EMU stability risks are contained, but mentioned a series of vulnerabilities, including a sudden re-pricing in risk premia. During the morning session, EUR/USD gradually reversed the initial uptick as the dollar found a better bid across the board. However, rising risk on a US government shutdown after Democrats didn't show up in a meeting with president Trump prevented more pronounced USD gains.

Early in US dealings, the text of Yellen's written statement before the JEC of Congress was released. Yellen sees the economic expansion as increasingly broad based. It will support faster growth in wages and incomes. Yellen expects the Fed to continue to gradually raise interest rates and reduce its balance sheet. The headlines from Yellen's speech were less soft than markets expected/feared. US bond yields and the dollar extended their intraday rise. The US Q3 GDP was revised marginally higher to 3.3% Q/Qa, but was largely ignored. USD/JPY took the lead in the USD rebound and tries to regain the 112 big figure. EUR/USD dropped to the 1.1820 area and is currently changing hands in the 1.1835 area. Later today, the Fed will publish its Beige Book, preparing the December 13 Fed meeting. Pressure on the dollar eased as it drifted somewhat further away from the recent lows. That said, the gap is still not big, given the US political risks (Tax bill and potential government shutdown) that are still not yet out of the way.

Sterling extends gradual rebound on Brexit progress

Today, sterling kept a cautiously positive bias, building on yesterday's gains. The preliminary EU/UK agreement on a divorce bill raises chances that negotiations on the future relationship start after the December EU summit. Ireland's EU commissioner also suggested that a break-through on the issue of the Irish border could follow soon. Earlier this morning, the UK money supply and lending data came out on the softer side of expectations. EUR/GBP trades currently in the 0.8830 area. Cable trades in the 1.34 area and tries to extend gains beyond the 1.3350 range top, even as the dollar is also better bid. So, sentiment on sterling improved. However the gains are not spectacular indicating that markets still see a lot of Brexit work to be done.

Dollar and Pound March Higher; Euro Extends Declines

The US dollar and the British pound remained the day's biggest winners in European trading on Wednesday on increased hopes of big tax cuts in the United States and the UK and the EU edging closer to a deal on the Brexit divorce terms. Most majors came under pressure from the stronger greenback, including the euro, which headed for a third straight day of losses, but the resurgent pound capped the dollar index's gains.

European equities headed higher after another record close on Wall Street overnight, with investors shrugging off a fresh threat by North Korea, which yesterday conducted another missile test. The UK's FTSE 100 bucked the trend as it was hurt by a firmer sterling, while gold drew no interest from safe-haven flows, dropping 0.5% to $1287 an ounce.

The euro hit a session low of $1.1816, retreating further from Monday's two-month peak of $1.1960. Another set of solid business survey release out of the Eurozone failed to lift the single currency. The European Commission's economic sentiment index rose to a 17-year high of 114.6 in November, in line with forecasts. Its business climate index was also up, climbing from 1.44 to 1.49 to a 10-year high, though this was below estimates of 1.53. In an encouraging sign for the European Central Bank, inflation expectations strengthened, with the index increasing from 14.7 to 16.0 in November.

There was little reaction to the ECB's bi-annual Financial Stability Review but the euro found some support from stronger-than-expected German inflation data. Germany's harmonized measure of the consumer price index rose from 1.5% to 1.8% year-on-year in November's flash reading, beating expectations of 1.7%. The data helped the euro recover to around $1.1835 in late session.

Sterling hit a two-month high of $1.3430 on reports that the UK and the EU have agreed the outlines of a deal on the Brexit divorce bill, thought to be around €50 billion. The issue of the Northern Irish border remains a sticking point, but hopes are high that the EU's chief negotiator, Michel Barnier, will recommend to EU leaders that there has been sufficient progress on the divorce terms for the talks to move on to the next phase at the December summit.

The pound eased a little however, after Bank of England lending figures showed consumer credit growth in the UK hit an 18-month low in October. Sterling was last trading around $1.34, up 0.5% on the day, while the euro was down a similar amount at 0.8830 pounds.

The greenback moved towards one-week highs, with dollar/yen flirting with the 112 level and the dollar index hitting a session high of 93.435. The US currency got a boost yesterday after the Senate Budget Committee gave the go-ahead for a full Senate vote on the tax bill on Thursday. Senators will be debating the bill today with further amendments expected given that several Republican Senators are still opposed to the legislation in its current form.

Uncertainty about tomorrow's vote, as well as concerns about a possible US government shutdown on December 8 after senior Democrats cancelled a meeting with President Trump to discuss a deal on a new spending bill, have been limiting the dollar's advance. However, the greenback got an added boost from an upward revision to US GDP. Annualized GDP growth in the third quarter was revised up from 3.0% in the preliminary estimate to 3.3% in the second reading, beating expectations of 3.2%. The figure is the highest quarterly growth since 2014 and is up from 3.1% in the second quarter.

Fed Chair Janet Yellen's prepared remarks for her semi-annual testimony before the Joint Economic Committee in Congress didn't attract the usual fanfare as the outgoing Fed chief didn't add anything new to the monetary policy outlook. Yellen repeated that the recent fall in inflation is likely to be due to "transitory factors" and reiterated that "additional gradual rate hikes" will be appropriate, but avoided specifically mentioning December as the timing for the next increase.

Commodity-linked currencies underperformed today, with the Australian dollar sliding to a one-week low of $0.7552 and the New Zealand dollar dropping to around $0.6885. The Canadian dollar was also down, weighed by weaker oil prices, with dollar/loonie hitting a 4-week high of 1.2859.

Crude oil prices remained under pressure amid doubts about whether major oil producers will agree to an extension of the output cut deal at Thursday's meeting in Vienna between OPEC and some non-OPEC countries. OPEC sources today suggested that an expected extension of nine months beyond March 2018 could be accompanied by an interim review in June, meaning the deal may end sooner, according to Reuters.

Both WTI and Brent crude stood slightly down on the day at $57.89 and $63.56 a barrel respectively, ahead of the EIA's weekly US inventory report.