Sample Category Title

Bitcoin Blasts Through $10,000

- Investors Shrug Off North Korean Threat;

- Oil Edges Lower as Oil Producers Meet to Discuss Extension;

- Bitcoin Blasts Through $10,000.

US equity markets are on course to build on Tuesday's gains as we near the open on Wall Street, with the latest North Korea missile launch doing little to deter investors.

Not so long ago, the threat of escalation caused by such action would send investors fleeing for safe havens but as time has gone on and nothing has escalated beyond tough talk, investors have become less sensitive to the tests. Even Gold, the traditional safe haven, has seen only minor flows on the back of the launch and continues to trade below $1,300 which has been a notable resistance level for the yellow metal.

Sterling is trading at a two month high against the dollar this morning, after reports that the UK has agreed a divorce settlement with the EU following months of negotiations. While nothing has been explicitly confirmed and is unlikely to be given the tight political spot Theresa May finds herself in, if this is correct then this would be a major step towards moving negotiations on to transition deals and a future trade agreement.

Progress has come at a snail's pace so far and this agreement, if true, comes as May is put under substantial pressure by businesses demanding assurances on the future relationship with the EU and how it will impact them. While an agreement will come as a relief, as reflected in the rise in the pound, there's still a long way to go and there's likely to be many many more difficulties faced along the way. This is the first of many large hurdles on the way to Brexit, but it's a very important first step.

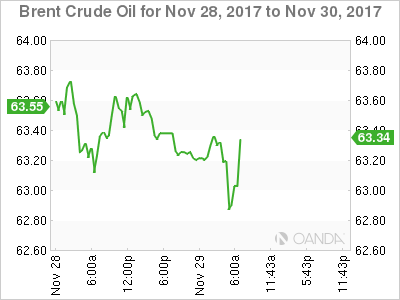

Brent and WTI crude are heading for a third consecutive daily loss on Wednesday as OPEC and non-OPEC officials preparing to meet in Vienna to discuss a possible extension to production cuts. The current cuts expire in March and there appears to be a broad agreement that more needs to be done in order to bring the market back into balance.

The next 12 months is going to continue to be challenging for oil producers and the higher oil prices get, the more we may see US shale companies turning on the taps and undoing the hard work. Still, oil prices have recovered strongly since the cuts were initially agreed and should producers agree to a nine month extension, it should keep prices at these more sustainable levels. That said, with an extension looking almost entirely priced in, I wonder if we'll see a similar response to last time when oil plummeted in the aftermath of the announcement.

Bitcoin is tearing higher once again on Wednesday, having broken through the much talked about $10,000 level for the first time ever earlier in the day and is already closing in on $11,000, only hours later. The move takes Bitcoins gains to more than 30% since Saturday morning and more than 900% since the start of the year. It's no wonder why people are questioning whether this is a bubble.

That said, people have been calling this a bubble for months, if not years, and that hasn't stopped it making record after record. Clearly widespread acceptance and even adoption has aided the rally but the moves we've seen in recent days suggest there's been a substantial speculative component. Perhaps the additional coverage Bitcoin has received on its approach to $10,000 has fuelled the rally and speeded up the process. Whatever the cause, I fear a substantial correction is not far away and this could be the true test of the correct value of the cryptocurrency.

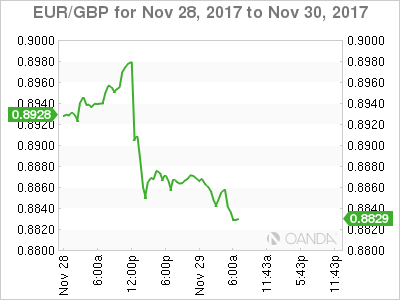

Technical Outlook: EURGBP – Bears Eye 200SMA Target After Completion Of H&S Pattern On Daily Chart

The cross extends steep descend into third consecutive day and generated bearish signals on completion of asymmetric H&S pattern on daily chart (broken neckline lies at 0.8868) and break below 0.8840 (Fibo 61.8% of 0.8732/0.9013 ascend).

Strong bearish acceleration from 0.8981 (right shoulder) eyes target at 0.8791 (200SMA / 07 Nov trough) and could extend towards key s/t support at 0.8732 (01 Nov low).

Broken daily Kijun-sen / H&S neckline mark solid resistance at 0.8870 zone which is expected limit corrective attempts.

Res: 0.8840, 0.8870, 0.8903, 0.8916

Sup: 0.8811, 0.8791, 0.8745, 0.8732

Will Russia Get Onboard The OPEC Train?

Wednesday November 29: Five things the markets are talking about

Global equities continue to find support as investor optimism over U.S tax reform trumps concerns about North Korea's latest missile launch.

In FX, the pound (£1.3422) has jumped to a two-month high as Brexit negotiators seem to have agreed to an outline divorce deal worth around €50B. The 'mighty' dollar remains on the back foot, while the EUR (€1.1864) advances as data from Germany's regions showed inflation and consumer confidence accelerating.

Note: The U.S Senate tax bill is headed for a marathon debate later this week after the budget committee voted yesterday along party lines to send the Republican plan to the floor.

In commodities, crude oil prices fall for a third consecutive day as U.S inventory data expanded ahead of tomorrows OPEC meeting to decide on prolonging supply cuts past the end of March, 2018. However, there is 'radio silence' from non-OPEC member Russia, which could be a stumbling block to a potential new agreement.

Also yesterday, new Fed Chair nominee, Jerome Powell, has assured the market of a “steady, responsible hand” and the case for a December rate hike “is coming together.”

This morning, the second print of Q3 U.S GDP is expected to be revised a tad higher (+3.3% vs. +3%) on the back of stronger consumer spending and inventory accumulation.

1. Stocks find strong support

In Japan, stocks rallied overnight as banks and financial shares tracked Wall street higher, shrugging off another N. Korean missile launch. The Nikkei share average ended +0.5% higher, while the broader Topix advanced +0.8%.

Note: Global financial and securities shares are taking the sector lead, supported mostly by new Fed Chair nominee Powell's defending the need to potentially lighten regulation on the financial sector.

Down-under, Australia's S&P/ASX 200 Index rose +0.5%, while S. Korea's Kospi index dropped less than -0.1%.

In Hong Kong, shares ended the session lower despite other regional gains, with investors' risk appetite curbed by N. Korea's latest missile test. The Hang Seng index was down -0.19%, while the Hang Seng China Enterprises index fell -0.49%.

In China, stocks ended firmer, strengthened by a surge in property shares and resources firms. The Shanghai Composite index was up +0.13%, while the blue-chip CSI300 index was down -0.05%, with its financial sector sub-index higher by +0.77%.

In Europe, regional indices trade mostly higher across the board with the exception of the FTSE 100, which trades a tad lower on talk of a Brexit divorce bill, having been preliminary agreed upon between the U.K and E.U.

In the U.S, stocks look set to open little changed.

Indices: Stoxx600 +0.6% at 389.3, FTSE -0.5% at 7422, DAX +0.7% at 13148, CAC-40 +0.5% at 5417, IBEX-35 +1.2% at 10267, FTSE MIB +0.6% at 22417, SMI +0.1% at 9330 S&P 500 Futures flat.

2. Oil falls on uncertainty over OPEC deal, gold higher

Oil prices are under pressure as doubts set in about Russia's willingness to substantially extend a deal to curb global output.

Ahead of the U.S open, Brent crude futures are down -34c at +$63.27 a barrel, while U.S light crude has fallen -31c to +$57.68 a barrel.

Note: Oil prices have rallied by about +40% since the middle of the year, supported by a deal between the OPEC and non-OPEC members, such as Russia, to reduce crude oil production by -1.8m bpd. The deal expires in March 2018, but it's expected to be extended at tomorrow's meeting.

However, Russia is concerned that a more robust extension could lead the oil price to rally too sharply, which would send the Russian rouble higher and harm exports. It's also worried that a steep price rise could trigger another increase in U.S production.

Note: API data yesterday showed that U.S. crude inventories rose by +1.8m barrels in the week ended Nov. 24. The market was looking for a -2.3m barrel drop.

Gold prices have crept a tad higher amid a weaker dollar, while N. Korea's latest missile test seems to have had little impact on the safe-haven metal. Spot gold is up +0.2% at +$1,295.92 an ounce.

3. U.S yield curve flattens

The U.S Treasury yield curve continues to flatten, with the 10-year note at +2.32%, down -1 bps, while U.S two-year note trades unchanged at +1.74%. The spread trades atop its 10-year low at +58 bps.

Jerome Powell's testimony to the Senate Finance Committee yesterday seems to have assured the market that Trump's nominee would 'not' do much different from Ms. Yellen in setting monetary policy. Powell confirmed market expectations that the case for another +25 bps “is coming together” next month, although he cautioned nothing has been decided.

Fed funds futures are putting a +96% probability on a hike with a probability of another +25 bps hike above +50% by mid-2018. The consensus of Fed watchers call for three rate increases in 2018.

Elsewhere, Germany's 10-year Bund yield has increased +2 bps to +0.34%, the biggest increase in almost three-weeks, the U.K's 10-year Gilt yield increased +6 bps to +1.253%, the highest in more than two-weeks

4. Little support for the 'big' dollar

The U.S dollar is finding it difficult to gain traction, pulled down by broad strength in GBP and EUR as well as worries over a possible U.S government shutdown after Democrats pulled out of a meeting with President Trump yesterday.

Note: The not so 'mighty' dollar is on track for its worst month in four-months, and its worst year in fourteen-years, has dipped another -0.2% against the majors ahead of the U.S session.

The EUR (€1.1867) is +0.2% higher supported by a number of German states reporting a stronger than expected CPI data for Nov – several states readings w ere above the ECB target of around +2.0%.

GBP/USD (£1.3402) is trading atop of its two-month highs as some concerns of a 'hard' Brexit were diminished after reports circulated that U.K will move closer to the E.U demands for a financial settlement. Market expectations of next potential Bank of England (BoE) rate hike seem to have moved forward to Sept 2018 from Nov as a result of progress.

5. Eurozone confidence continues to rise

Euro data this morning brought some good news for the 'single' unit and the European Central Bank (ECB).

The European Commission's Economic Sentiment Indicator continued to rise this month, hitting its highest level in 17-years as the reading of 114.6 slightly exceeded market expectations.

As with last week's German PMI release, the survey bodes well for the economy's momentum going into next year, and there was also a note of encouragement for the ECB in its long battle to boost inflation in the form of another pickup in the rate of price increases expected by consumers over the next year.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bearish momentum yesterday bottomed at 1.1827. The bias is bearish in nearest term testing the lower line of the bullish channel (see my H1 chart below) located around 1.1800 area which is a good place to buy with a tight stop loss. Immediate resistance is seen around 1.1875. A clear break above that area could lead price to neutral zone in nearest term testing 1.1920/50 area. On the downside, a clear break and daily close below 1.1800 and the bullish channel would expose 1.1690 or lower. Overall I remain neutral.

GBPUSD

The GBPUSD was volatile but indecisive yesterday. The bias is neutral in nearest term probably with a little bullish bias testing 1.3400 – 1.3450 region. Immediate support is seen around 1.3330. A clear break below that area could trigger further bearish pressure testing 1.3280 area or lower but as long as stay above 1.3000 I remain bullish and any downside pullback should be seen as a good opportunity to buy. On the upside, a clear break and daily close above 1.3400/50 would expose 1.3615 key resistance.

USDJPY

The USDJPY failed to continue its bearish momentum yesterday topped at 111.64. The bias is neutral in nearest term probably with a little bullish bias especially if price able to make a clear break above 111.65 testing 112.00 – 112.50 region. Immediate support is seen around 111.30. A clear break below that area could trigger further bearish pressure testing 110.65 area. Overall I remain neutral but prefer a bearish scenario at this phase as a part of the bearish pin bar scenario as you can see on my daily chart below.

USDCHF

The USDCHF continued its bullish momentum yesterday topped at 0.9852. The bias is bullish in nearest term testing 0.9875 which is a good place to sell with a tight stop loss. Immediate support is seen around 0.9815. A clear break below that area could lead price to neutral zone in nearest term testing 0.9780 or lower. On the upside, a clear break and daily close above 0.9875 would expose 0.9940 region. Overall I remain neutral.

DAX Soars As Powell Calls for Easier Bank Regulations

The DAX index has posted strong gains in the Wednesday session. Currently, the DAX is at 13,190.00, up 1.00% on the day. On the release front, Germany releases Preliminary CPI, which is expected to accelerate to 0.3%. In the US, Preliminary GDP is expected to post a strong gain of 3.3%. On Thursday, German releases retail sales and the eurozone publishes CPI Flash Estimate.

European stock markets are in green territory on Wednesday, buoyed by comments from Fed Designate Jerome Powell. At his confirmation hearing, Powell said that he favored tailoring regulations for small banks, leaving the toughest regulations for the big players. This boosted bank shares on Wednesday, and the DAX has jumped on the bandwagon. Commerzbank has gained 1.16% and Deutsche Bank has improved 1.17%.

There are new developments in the German political saga, as President Angela Merkel continues efforts to form a new government. Coalition talks will now center on Merkel’s conservative bloc (CDU) and the social democrats (SPD). After the election, the SPD announced that it would remain in the opposition. However, coalition talks imploded when the Free Democrats pulled out of the negotiations and there is pressure on the SPD to reconsider in order to avoid elections. The SPD is split on whether to join a coalition with Merkel, as many SPD members don’t want the SPD to be relegated to a junior party in the coalition, as was the case prior to the election. Although the SPD has agreed to exploratory meetings with the CDU, substantial talks of a “grand coalition” are not expected to start before 2018. The SPD is likely to take advantage of Merkel’s weak hand and press demands for greater government spending and a looser immigration policy. The SPD could even demand the powerful finance ministry.

Bitcoin: Buckle Up!

Bitcoin: to the moon

The price of Bitcoin broke another record yesterday as it crosses the symbolic $10,000 threshold. Not content to stop here, Bitcoin continued to rally during the Asian session and tested the $11,000 level. The pace of Bitcoin appreciation has accelerated recently as both institutional and retail investors keep piling into the crypto market. The likelihood of a bubble doesn’t scare anyone.

I think that there is plenty of room for further Bitcoin appreciation. There are actually several reasons. Firstly, although institutional investors already have a foot in the crypto space, the inflow of money if far from over as many big players haven’t move yet. The arrival of CME and CBOE derivatives will just make BTC investing much easier and will encourage skittish investors to take the leap. Secondly, several key projects, such as Rootstock or Lightning Network, which are built on the top of Bitcoin, that aim as improving Bitcoin’s scalability will be released soon. Finally, people are claiming that Bitcoin and crypto assets in general are in a massive bubble. Just before the dot-com bubble popped in March 2000, the market capitalization of Nasdaq hit $6.7 trillion. AS of this morning, the total market capitalization of crypto assets stands at $330 billions…

However, one should keep in mind that there would be most likely a clean-up in the crypto space next year. Many blockchain projects will just simply not make it.

In my opinion, a correction sounds healthy, as the price of Bitcoin has been on a mad run for the last few months. Nevertheless, investors’ appetite is massive and any corrections will likely be short-lived, as investors would take advantage of the move to buy on a dip.

US: Strong GDP data expected but weakness should remain on the dollar

The second read of the US GDP will be released this afternoon and should be around 3%. The data remains strong and as we mentioned several times over the last few weeks, the inflation is also on the rise. However, markets have recently punished the greenback against the US dollar. The central bank’s ambition about the rate path seems very cautious in regard to the strong data and this is this cautiousness that is weighing down on the dollar. We consider that the Fed must be cautious given the massive amount of money that went into all asset classes.

In the same time, Gold is up stalling below $1300 and the S&P 500 is reaching new all-time high. Only US bonds with short-term maturities are getting slightly lowered. We believe that the Eurodollar has all the inputs for the reaching again 1.20. The short-term decline that happens for the dollar are often temporary and the trend is clearly bullish

Elliott Wave Analysis: NZDUSD Trading In A Temporary Setback, With Support Around 0.6852/0.6840

NZDUSD has been trading bullish since November 17 and unfolded a higher degree wave A), first leg of a bigger three-wave recovery. Well rise has recently stopped near the upper Elliott wave channel line at 0.6945 level and breached lower, ideally for a three-wave correction into wave B). As of today, we see price again rising, but only for a temporary sub-wave B of B), with possible resistance coming in at around 0.6940 region. There a new drop into wave C of B) may follow, with significant support coming in at 0.6852 level former swing low.

NZDUSD, 1h

Technical Outlook: COPPER Extends Steep Descend Below Daily Cloud

Copper hit one-week low on today's extension of steep fall from $3.1750 peak which generated strong bearish signal on break below daily cloud base ($3.0663).

Bears are looking for full retracement of $3.0305/$3.1750 upleg, with growing risk of eventual break below key support at $3.0324 (Fibo 61.8% of larger $2.8930/$3.2580 ascend).

Sustained break here would be strong bearish signal for extension of bear-leg from $3.1750 towards psychological $3.00 support.

Broken daily cloud now acts as resistance and weighs on near-term action.

Stronger dollar on progress in US tax cut plan talks also pressures copper price.

Res: 3.0663, 3.0825, 3.1000, 3.1162

Sup: 3.0324, 3.0305, 3.0045, 3.0000

CRUDE OIL Bearish Retracement

Crude oil has finished its consolidation and is now ready to challenge the 60-dollar level. Expected to show continued increase. Support is given at a distance at 54.81 (14/11/2017 low)

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

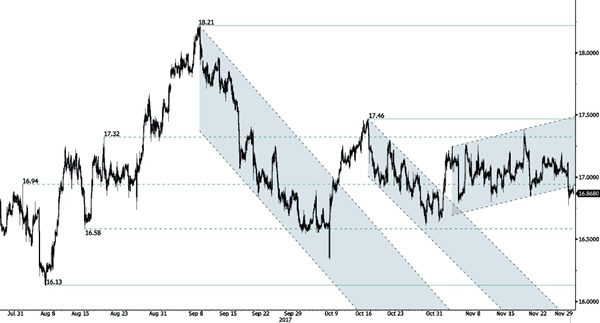

SILVER Monitoring Uptrend Channel

Silver is heading higher. Hourly support can be found at 16.60 (27/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).