Sample Category Title

EUR/USD Continued Short-Term Consolidation Before Another Leg Higher

EUR/USD is consolidating lower. Hourly resistance is now given at 1.1961 (27/11/2017 high). Hourly support is given at a distance at 1.1554 (07/11/2017 low). Expected to show renewed increase.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Market Update – European Session: Germany Inflation Approaching ECB Target, Optimism On Brexit Negotiations

Notes/Observations

German State CPI readings near ECB target

Brexit negotiations have renewed optimism of moving into phase 2 with reports the UK will likely meet the financial settlement terms of the EU

Asia:

North Korea: Confirms fired new type of ICBM at HWASONG-15 that puts entire US in range; launch was successful

North Korea Leader Kim Jung Un: Have begun to complete nuclear program and finally realized the cause of completing the State Nuclear Force; Missile program would not threaten any country as long as they did not “infringe of North Korea sovereign gains”

South Korea said to have responded with land, sea and air missiles towards the east just minutes of the NK missile launch

Japan Chief Cabinet Sec Suga: Trump/Abe agreed China needs to play an increase role regarding North Korea; Trump/Abe did not discuss military options but agreed to boost deterrence capability against NK

US President Trump: Briefed while missile was still in flight; it is situation we will handle; launch doesn’t change US approach to NK issue; will take care of NK issue

Europe:

Reportedly UK and EU agree Brexit divorce bill with tab between €45-55B (vs. EU demands of €60B). The final figure deliberately being left open to interpretation, depending on how each side calculates the output from an agreed methodology. (**Note: Govt official: did not recognize UK Telegraph newspaper account of Brexit negotiations)

Americas:

Senate Budget Committee advances the tax bill. All 12 Republicans vote 'yes' including Senators Johnson and Corker; the 11 Democrats vote 'no'. Budget Committee approval moves the bill to the full Senate, which could consider the bill later this week

Energy:

Weekly API Oil Inventories: Crude: +1.8M v -6.4M prior

Economic Data:

(NL) Netherlands Nov Producer Confidence: 9.1 v 8.2 prior

(NO) Norway Q3 Manufacturing Wage Index Q/Q: 0.9% v 0.4% prior

(CH) Swiss Oct UBS Consumption Indicator: 1.54 v 1.51 prior

(FR) France Oct Consumer Spending M/M: -1.9% v -0.1%e; Y/Y: -0.6% v +1.4%e

(FR) France Q3 Preliminary GDP (2nd reading) Q/Q: 0.5% v 0.5%e ; Y/Y: 2.2% v 2.2%e

(DE) Germany Nov CPI Saxony M/M: 0.3% v 0.0% prior; Y/Y: 2.0% v 1.8% prior

(ES) Spain Preliminary Nov CPI M/M: 0.4% v 0.5%e; Y/Y: 1.6% v 1.7%e

(ES) Spain Preliminary Nov CPI EU Harmonized M/M: 0.3% v 0.4%e; Y/Y: 1.7% v 1.9%e

(SE) Sweden Nov Consumer Confidence: 108.0 v 104.0e; Manufacturing Confidence: 121.9 v 120.3e, Economic Tendency Survey: 114.1 v 111.9e

(HU) Hungary Oct Unemployment Rate: 4.0% v 4.0%e

(SE) Sweden Q3 GDP Q/Q: 0.8% v 0.8%e; Y/Y: 2.9% v 3.5%e

(AT) Austria Nov Manufacturing PMI: 61.9 v 59.4 prior

(DE) Germany Nov CPI Bavaria M/M: +0.4% v -0.1% prior; Y/Y: 1.8% v 1.5% prior

(DE) Germany Nov CPI Brandenburg M/M: +0.4% v -0.1% prior; Y/Y: 1.6% v 1.3% prior

(DE) Germany Nov CPI Hesse M/M: +0.4% v -0.2% prior; Y/Y: 2.0% v 1.6% prior

(CH) Swiss Nov Credit Suisse Expectations Survey: 40.7 v 32.0 prior

(DE) Germany Nov CPI Baden Wuerttemberg M/M: +0.4% v -0.2% prior; Y/Y: 1.8% v 1.5% prior

(DE) Germany Nov CPI North Rhine Westphalia M/M: 0.3% v 0.0% prior; Y/Y: 1.8% v 1.6% prior

(UK) Oct Mortgage Approvals: 64.6K v 65.0Ke

(UK) Oct Net Consumer Credit: £1.5B v £1.5Be; Net Lending: £3.4B v £3.7Be

(PT) Portugal Nov Consumer Confidence: 2.3 v 2.1 prior; Economic Climate Indicator: 2.1 v 2.1 prior

(EU) Euro Zone Nov Business Climate Indicator: 1.49 v 1.51e; Consumer Confidence (Final): 0.1 v 0.1e , Economic Confidence: 114.6 v 114.6e, Industrial Confidence: 8.2 v 8.6e, Services Confidence: 16.3 v 16.7e

Fixed Income Issuance:

(IN) India sold total INR110B vs. INR110B indicated in 3-month, 6-month and 12-month bills

(DK) Denmark sold total DKK12.9B in 3-month and 6-month Bills

(SE) Sweden sold total SEK2.0B vs. SEK2.0B indicated in 2022 and 2032 Bonds

(IT) Italy Debt Agency (Tesoro) sold €1.75B vs. €1.25-1.75B indicated range in 2.05% Aug 2027 BTP bonds; Avg Yield: 1.73% v 1.86% vprior; Bid-to-cover: 1.65x v 1.43x prior

(IT) Italy Debt Agency (Tesoro) sold €1.75B vs. €1.25-1.75B indicated range in Apr 2025 CCTeu (Floating Rate bond); Avg Yield: 0.46% v 0.60% prior; Bid-to-cover: 1.60x v 1.56x prior

(RU) Russia sold RUB16.2B vs. RUB16.4B indicated in Oct 2024 OFZ bonds; Yield: 7.49%

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.6% at 389.3, FTSE -0.5% at 7422, DAX +0.7% at 13148, CAC-40 +0.5% at 5417, IBEX-35 +1.2% at 10267, FTSE MIB +0.6% at 22417, SMI +0.1% at 9330 S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trades mostly higher across the board with the exception of the FTSE100 which trades lower on talk of a Brexit divorce bill has been preliminary agreed between the UK and Europe. A new record close in the US overnight as well as a generally positive session in Asia has helped underpin the rally.

On the corporate front Daimler trades higher after reports Geely Auto proposed to acquire a 5% stake via share issue which was rejected by Daimler. Cineworld underperforms after confirming it has made an approach to acquire Regal Ent, while on the earnings front, Findel trades 20%+ higher on strong results, with Britvic, Poor AG and Telford Home other notable risers. Elsewhere shares of the LSE trade lower after CEO Xavier Rolet stepped down ahead of the originally scheduled. Looking ahead notable earners include Tiffanys and RBC.

Equities

Consumer discretionary [Britvic [BCI.UK] +7% (Earnings), Cineworld [CINE.UK] -14% (Proposed takeover of Regal Ent for $23/shr)]

Industrials: [RPC [RPC.UK] -7.0% (Earnings), Porr Ag [ABS2.DE] +2.5% (Earnings), Philips Lighting [LIGHT.NL] -3.2% (Philips to place 17.1M shares)]

Financials: [Brewin Dolphin [BRW.UK] +2% (Earnings), LSE [LSE.UK] -2.1% (CEO steps down effective immediately)]

Utilities: [Findel [FDL.UK] +21% (Earnings)]

Real Estate: [ Telford Home [TEF.UK] +2.6% (Earnings)]

Speakers

BOE member Cunliffe: UK consumer credit growing fast, need to watch it. Agree with rest of MPC that UK economy’s potential growth had slowed

ECB's Constancio (Portugal) noted that the region must more resilient to possible shocks

EU Chief Brexit Negotiator Barnier: Hope to report to EU Council of sufficient progress in the Brexit negotiations. Still working to reach agreement with Britain about its exit from the bloc. Ireland remained a big problem in negotiations. Will try to prevent a hard Brexit.

ECB Financial Stability Report: Higher rates might trigger concerns on debt servicing. Maintained its overall assessment and saw no generalized overvaluation in Euro Area financial markets. Regional recovery and monetary policy made debt more sustainable. Saw progress on sovereign debt as political risks look

German Bundesbank Financial Stability Report: Resilience for banking sector was good overall; strong economic picture might masks financial risks. Risks from residential property financing were still limited

Sweden FSA Financial Stability Report: Resilience of sector was generally satisfactory but did see significant risks in commercial real estate sector

Russia Central Bank official reiterated its stance to gradually cut interest rates. To look at only long-term inflation changes. 2017 GDP growth seen around 1.7-1.8%

BOJ’s Nakaso: Communication was important for an exit strategy; Reversal rate was a useful theory for policy. Financial stability was the basis for sustainable economic growth. BOJ easing was a factor in greater bank competition but exerted downward pressure on profits. Easing had encouraged more active lending by banks

China Commerce Ministry (MOFCOM): US move on aluminum to hurt bilateral interests (**Note: US Commerce Department initiated anti dumping investigation of aluminum imports from China)

UAE Oil Min Mazrouei: OPEC still debating the length of any extension in production cuts; to also look at other options. UAE did not see a threat from US shale oil production

Currencies

EUR/USD was higher by 0.2% as Various German States reported the Nov CPI data. Several of the Nov CPI readings was above the ECB target of around 2.0%

GBP/USD was at 2-month highs above the 1.34 level as some of the concerns of a hard Brexit was diminished after reports circulated that UK will move closer to the EU demands for the financial settlement. Market expectations of next potential BOE rate hike moved forward to Sept 2018 from Nov as a result of progress in the Brexit negotiations

Fixed Income

Bund futures trade 162.80 down 22 ticks, steady as the German state of Saxony inflation pick up points to rebound in German price growth. Continued upside sees 163.40 then 163.63. A reversal targets 162.50 then 162.38.

Gilt futures trade at 124.76 down 12 ticks as UK makes a Brexit breakthrough. Continued upside eyeing 125.15 then 125.65. Downside targets include 124.24 then 123.75.

Wednesday’s liquidity report showed Tuesday's excess liquidity climbed to €1.863T from €1.850T. Use of the marginal lending facility fell to €291M from €315M prior.

Corporate issuance saw 8 issuers raise $4.5B in the primary market

Looking Ahead

05:30 (EU) ECB allotment in 3-month LTRO (

05:30 (DE) Germany canceled plan sale of €3.0B in 2022 BOBL

06:00 (BR) Brazil Oct PPI Manufacturing M/M: No est v 1.1% prior; Y/Y: No est v 2.1% prior

06:30 (CL) Chile Central Bank (BCCh) Nov Minutes

06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell RUB10B in 2028 OFZ bonds

07:00 (US) MBA Mortgage Applications w/e Nov 24th: No est v 0.1% prior

07:00 (CL) Chile Oct Manufacturing Production Y/Y: +4.4%e v -1.4% prior, Industrial Production Y/Y: 5.8%e v 1.0% prior

07:00 (CL) Chile Oct Total Copper Production: No est v 485.9K tons prior

07:00 (UK) Weekly PM May question time in House of Commons

07:30 (BR) Brazil Oct Primary Budget Balance (BRL): +3.0Be v -21.3B prior; Nominal Budget Balance: -25.5Be v -53.3B prior

08:00 (DE) Germany Nov Preliminary CPI M/M: 0.3%e v 0.0% prior; Y/Y: 1.7%e v 1.6% prior

08:00 (DE) Germany Nov Preliminary CPI EU Harmonized M/M: +0.2%e v -0.1% prior; Y/Y: 1.7%e v 1.5% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Q3 Preliminary GDP Annualized Q/Q: 3.2%e v 3.0% advance; Personal Consumption: 2.5%e v 2.4% advance

08:30 (US) Q3 Preliminary GDP Price Index: 2.2%e v 2.2% advance; Core PCE Q/Q: 1.3%e v 1.3% advance

08:30 (US) Fed’s Dudley (dove, FOMC voter) on US economy

09:00 (UK) BOE Gov Carney at event in London

09:45 (UK) BOE’s Ramsden (Dissentger) at event in London

10:00 (US) Oct Pending Home Sales M/M: 1.0%e v 0.0% prior; Y/Y: +3.0%e v -5.4% prior

10:00 (US) Fed Chair Yellen before joint economic committee

10:30 (US) Weekly DOE Crude Oil Inventories

12:00 (DE) ECB’s Weidmann (GermanY) in Essen

12:00 (CA) Canada to sell 30-Year Real Return Bonds

12:45 (US) Fed Williams (moderate, non-voter) in Phoenix

13:30 (NL) ECB’s Knot (Netherlands) in London

14:00 (US) Federal Reserve Beige Book

GBP/JPY Diving Board Reversal Pattern Targeting D H4 And W L5 Camarilla Levels

The GBP/JPY has formed a variation of a V-shaped pattern named "Diving Board". The diving board is a reversal pattern that forms after the price makes a flat base than drops down with a high momentum that is followed by a straight-line run-up. V-shaped reversal is created, and the price proceeds up. At this point, we can see two POC zones. The first POC is 149.00-149.10 (D H3, W H3, Order block). Because of the strong trend that we can spot, the first POC zone could show a rejection if the price retraces. If we see a broader retracement below POC1 than pay attention to POC2 (50.0, EMA89, W L3) 148.35-148.66. Rejections from any of POC zones should target 149.90 and 150.47.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone

Technical Outlook: USDCAD – Fresh Bullish Acceleration Signals Full Retracement Of 1.2916/1.2665 Correction

The pair advances further on Wednesday and breaks above pivotal barriers at 1.2820 (Fibo 61.8% of 1.2916/1.2665) and 1.2836 (21 Nov former recovery peak).

Break here to confirm higher base at 1.2665/70 for full retracement of 1.2916/1.2665 correction, with lift above 1.2916 to open psychological 1.3000 barrier and signal further retracement of larger 1.3793/1.2061 descend. Next target lies at 1.3131 and marks Fibo 61.8% retracement.

Daily techs are in full bullish setup and support further advance, with weekly cloud twisting at 1.3280 next month and expected to attract bulls.

Bullish cross of 10/20SMA which formed yesterday, further underpins the action, with rising 10SMA marking solid support at 1.2767.

No data from Canada are scheduled today and traders will focus a number of releases from the US for fresh signals.

Res: 1.2857, 1.2916, 1.3000, 1.3071

Sup: 1.2807, 1.2767, 1.2751, 1.2713

Euro Edges Higher, Investors Await German Inflation, US GDP

The euro has edged higher in the Wednesday session. Currently, EUR/USD is trading at 1.1857, up 0.14% on the day. On the release front, Germany releases Preliminary CPI, which is expected to accelerate to 0.3%. French data was a mix. Consumer Spending declined 1.9%, missing the estimate of 0.0%. Preliminary GDP in the third quarter remained unchanged at 0.5%. In the US, Preliminary GDP is expected to post a strong gain of 3.3%, and Fed Chair Janet Yellen testifies before a congressional committee.

The political vacuum in Germany has taken a twist, as President Angela Merkel continues in efforts to form a new government. Coalition talks will now center on Merkel’s conservative bloc (CDU) and the social democrats (SPD). After the election, the SPD announced that it would remain in the opposition. However, coalition talks imploded when the Free Democrats pulled out of the negotiations and there is pressure on the SPD to reconsider in order to avoid elections. The SPD is split on whether to join a coalition with Merkel, as many SPD members don’t want the SPD to be relegated to a junior party in the coalition, as was the case prior to the election. Although the SPD has agreed to exploratory meetings with the CDU, substantial talks of a “grand coalition” are not expected to start before 2018. The SPD is likely to take advantage of Merkel’s weak hand and press demands for greater government spending and a looser immigration policy. The SPD could even demand the powerful finance ministry.

Fed Chair Designate Jerome Powell testified before the Senate Banking Committee on Tuesday. Powell said that he favored tailoring regulations for small banks, leaving the toughest regulations for the big players. Powell was cautious and diplomatic during the hearing, saying that the case is building for a December rate hike, and refused to express an opinion on the Trump tax bill. He will replace Janet Yellen in February, and is widely expected to continue Yellen’s monetary stance of small, gradual rate hikes.

Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a “gradually rising path” for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Gold Stays Still As Silver Slides Lower

Gold faces down a resurgent dollar overnight to remain unchanged but silver suffers as it breaks a key technical indicator.

Gold

Gold traded quietly yet again overnight in a seven dollar range but closed in a flat line with the previous days close at 1294.00. Overall, gold continues to consolidate its slow, medium-term gains near to the top of its two-month range.

One positive is that it has shrugged off a stronger U.S. dollar overnight as the U.S. Senate made progress on the tax reform bill. Conversely, gold has not rallied at all after North Korea’s latest missile test of what appears to be a genuinely Intercontinental class of ballistic missile. It further reinforces that the risk-off safe-haven premiums associated with gold are gone for now. This leaves it entirely at the mercy of U.S. yields and the dollar index.

Gold is unsurprisingly unchanged this morning with resistance at the 1299.00/1300.00 zone followed by 1306.50. Support is at the overnight low at 1290.00, followed by the 100-day moving average and Friday’s low at 1285.00.

The pace of data releases picks up into the 2nd half of the week which will hopefully shake gold from its lethargy.

Silver

Silver did not fare as well overnight as stop losses were triggered sending it lower by 20 cents to close at 17.8500. Having been wedged for the past week between the 100 and 200-day moving averages (DMA), and flirting with its five-month trendline support, this gave way as silver broke the 100-DMA at 16.9900 sending traders scurrying from long positions.

Like gold, silver has comatose in Asian trading, hovering in a barely discernable 16.8700/16.9100 trading range. With Europe’s arrival, things may get more interesting with the next support at the overnight lower of 16.7700 followed by the somewhat distant 16.5400.

Resistance is now the 100-DMA, today at 17.0000, the trendline at 17.0700 and then the 200-DMA at 17.1270.

All in all, silver’s price action looks more vulnerable to further dollar strength than gold’s with reasonably significant layers of resistance much closer to current levels then support.

Crude Remains Sleepless In Singapore Ahead Of OPEC

Crude oil's quiet session today suggests the street is in wait and see mode for tomorrow's OPEC meeting.

Oil has settled into wait and see mode overnight with both contracts finishing ever so slightly low from the previous day. Brent closed down 50 cents at 63.10 and WTI fell a minuscule 10 cents to 57.57, shrugging off a higher than anticipated climb in crude stocks from the American Petroleum Institute's inventory data.

Brent suffered some intra-day wobbles ahead of tomorrow's crucial OPEC/Non-OPEC official meeting in Vienna. Although the market has priced an extension of the production cut until the end of March 2018, rumours continue to circulate that Russia may not be entirely on board or may request a review in June. Either outcome is likely to provoke some heavy selling of crude if cracks appear driven by the world's largest producer.

Brent crude was sleepless in Singapore this morning, almost unchanged at 63.20. Initial support is nearby at 62.90 followed by 62.00 and then the all-import multiday low at 61.25. Brent quietly dropped through its short-term trend line on Monday, and this now intersects with the double top today at 64.45. Above there is the second double top at 64.85.

WTI was also unchanged with support at 57.25 and then 56.75, its two-month trendline support. A break of this level opens up a potentially ugly drop to a series of daily lows at 55.00. Resistance is at 58.00 and then the November high at 57.90.

With so much complacency about a rollover priced into tomorrow's meeting, the balance of probabilities suggests that oil is more vulnerable at the moment to any disappointments from the OPEC summit.

Markets Shrug Off North Korea’s Missile Test | Brexit Negotiations Seen A Major Breakthrough | Jerome Powell Supports Fed...

The UK government has agreed to pay their Brexit bill

Northern Ireland issue is still the thorny matter

the US senate Budget committee decided to push the bill towards full chamber

Global equities are on track to end the year at their record highs and this would be one of the best year since the immediate aftermath of the financial crisis.

A major unexpected breakthrough happened yesterday when it comes to the subject of Brexit. The UK government has agreed to pay their Brexit bill and the amount will be in between 45-55 billion euros. This is surely a substantial amount no matter how you look at it and hopefully the government understands that it is not committing to something which it cannot afford to pay.

However, it should aid the deadlock in the Brexit negotiation and help them to move forward. Picking up the Brexit bill has been the very thorny issue since day one and given that now the government has agreed to a respectable amount, the talks between the UK and the EU (which are set to resume next month) should be smoother. If the EU accepts the bill, then we will be moving to the next hurdle which is securing the EU rights. Nonetheless, the more favourable outcome so far has made some positive impact on Sterling which recovered some of its lost ground.

It is important to keep in mind that we are no way close to be out of the woods when it comes to the smooth negotiation process because the Northern Ireland issue is still the thorny matter.

North Korea's regime confirmed yesterday that they have completed their nuclear program. Initially, the news about another missile test created some uncertainty in the market, but it was short lived due to the fact that the reaction from the US was muted. Usually, Donald Trump would take the matter to Twitter and he would come up with some ballistic and firy comments.

However, we have not witnessed that yesterday. This enabled investors to keep the focus on the earning's story and that continued to help Wall Street to push the indices higher. President Trump vowed yesterday to take care of the situation. The question which investors should be asking, and not underestimating is, if Trump's reaction and action would result in more sanctions on something far larger?

As for the dollar index, the US senate Budget committee decided to push the bill towards full chamber. This simply means that there will be a marathon of debate which could delay the process further if the bill continued to be tossed around. The upcoming Fed chairman confirmed in his testimony to senate that December rate hike case is coming together. He supports the current stance which the Federal Reserve Bank has. Despite his outlook, the dollar index hasn't been able to rock. Even the unexpected improvement in the US confidence date (released yesterday) failed to produce much colourful result.

For Euro traders, they are seeking only outcome when they look at the biggest economy of the Eurozone, which is stability. This is where the grand coalition provides the answers to all the questions which one may have.

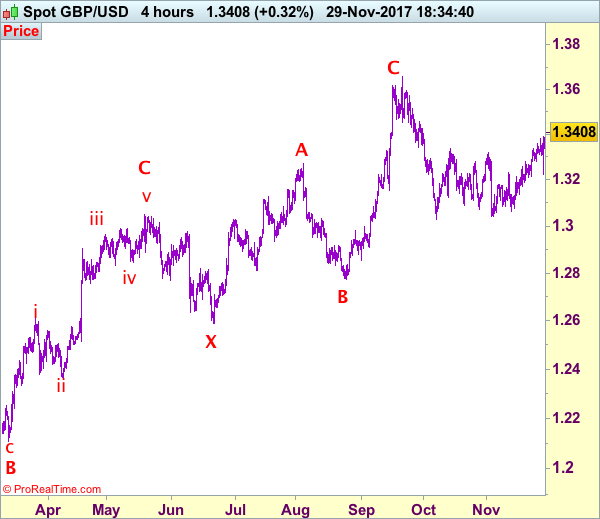

Trade Idea: GBP/USD – Buy at 1.3260

GBP/USD – 1.3341

Original strategy :

Bought at 1.3260, Target: 1.3450, Stop: 1.3200

Position: - Long at 1.3260

Target: - 1.3450

Stop: - 1.3200

New strategy :

Hold long entered at 1.3260, Target: 1.3450, Stop: 1.3330

Position: - Long at 1.3260

Target: - 1.3450

Stop:- 1.3330

As cable found renewed buying interest at 1.3221 yesterday and has rallied, reinforcing our bullishness for recent erratic rise from 1.3027 low to extend further gain to 1.3450, however, near term overbought condition should limit upside and price should falter below 1.3470, bring retreat later. Our preferred count is that (pls see the attached chart) the wave IV is unfolding as a complex double three (ABC-X-ABC) correction with 2nd wave B ended at 1.2774, hence 2nd wave C could have ended at 1.3658.

In view of this, we are holding on to our long position entered at 1.3260. Below 1.3330 would defer and risk weakness to 1.3290-00 but still reckon downside would be limited to 1.3250-60 and said support at 1.3221 should remain intact, bring another rise later.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has ended at 1.7192, the subsequent selloff is the larger degree wave (C) which is still unfolding with minor wave (III) of larger degree wave 3 ended at 1.1986, hence wave (IV) correction is in progress which could either be a triangle wave (IV) of a complex formation but upside should be limited to 1.3500 and price should falter well below 1.4000, bring another decline in wave (V) of 3 for weakness to 1.1500, then 1.1200.

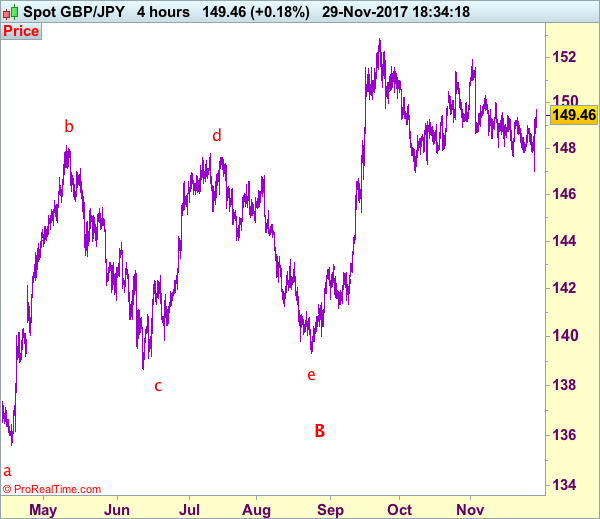

Trade Idea: GBP/JPY – Buy at 148.50

GBP/JPY - 148.40

Original strategy:

Bought at 148.00, stopped at 147.60

Position: - Long at 148.00

Target: -

Stop: - 147.60

New strategy :

Buy at 148.50, Target: 150.30, Stop: 147.90

Position: -

Target: -

Stop:-

Although sterling dropped briefly to 147.00 yesterday, as the pound found good support there and has staged a strong rebound, suggesting low has possibly been formed there and consolidation with upside bias is seen for gain to 150.00 resistance, break there would revive bullishness and signal the fall from 151.90 top has ended, then further gain to previous resistance at 150.30 would follow but reckon 150.90-00 would hold on first testing.

In view of this, we are looking to buy sterling again on dips as 148.40-50 should limit downside. Below 148.00 would defer and risk weakness to 147.50-60 but still reckon said yesterday’s low at 147.00 would hold and bring another rebound later.

Our preferred count is that larger degree wave V with circle is unfolding from 251.12 with wave (I) 219.34, (II): 241.38 and wave (III) is subdivided into 1: 192.60, 2: 215.89 (23 Jul 2008) and wave 3 ended at 118.87 earlier in 2009. The correction from there to 162.60 is wave 4 which itself is a double three and is labeled as first a-b-c ended at 151.53, followed by wave x at 139.03, 2nd a ended at 162.60, 2nd b at 146.75 and 2nd c leg of wave 4 ended at 163.00. Therefore, the decline from 163.00 to 116.85 is now treated as wave 5 which also marked the end of larger degree wave (III), hence wave (IV) major correction has commenced for retracement of the wave (III) from 241.38 and upside target at 183.95-00 (50% Fibonacci retracement of the wave (II) from 241.38) had been met, a drop below 160.00 would suggest wave (IV) has ended at 195.85, bring decline in wave (V) for initial weakness to 130 (already met) and 120.